Vladimir_Timofeev/iStock via Getty Images

Investment Thesis

The Enterprise Storage Systems (ESS) market has become very competitive, with many OEMs fighting for market share. Making it even worse, the market size declined in 2023 due to the enterprise slowdown and macro challenges. Furthermore, the ODMs (Original Design Manufacturers), and hyperscalers have also entered the storage arena, making it even more difficult for companies to achieve growth. Despite these obstacles, Pure Storage (NYSE:PSTG) has successfully navigated these challenges and executed a winning strategy.

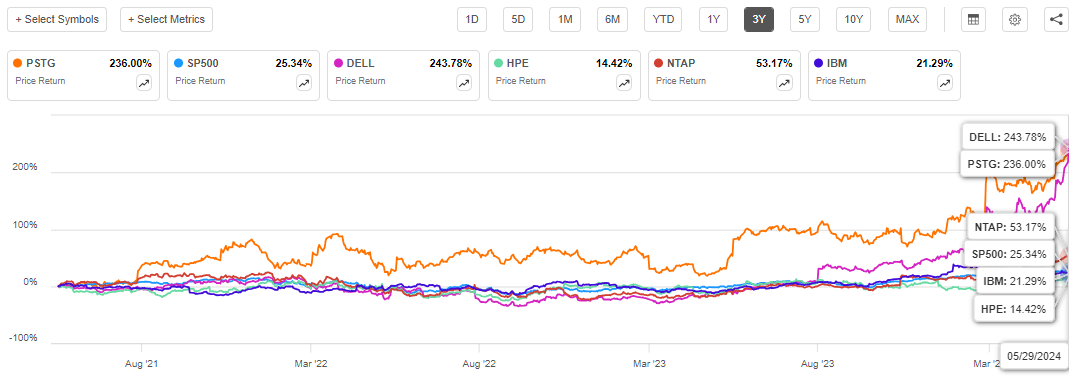

Over the past three years, Pure Storage stock price more than doubled. The company outperformed the S&P 500 and many of its ESS peers by a wide margin (see below). Most of that rise was thanks to its effective growth strategy and solid execution.

PSTG price performance (Seeking Alpha)

At Miletus Research, our mission is to find successful companies that can beat the market and deliver outsized returns. Our analysis shows that these companies share certain strategic attributes that set them apart from the rest. We think Pure Storage has the potential to be one of these successful companies. In this article, we will share our analysis of the company and its potential for long-term success.

Solid Q1 Earnings

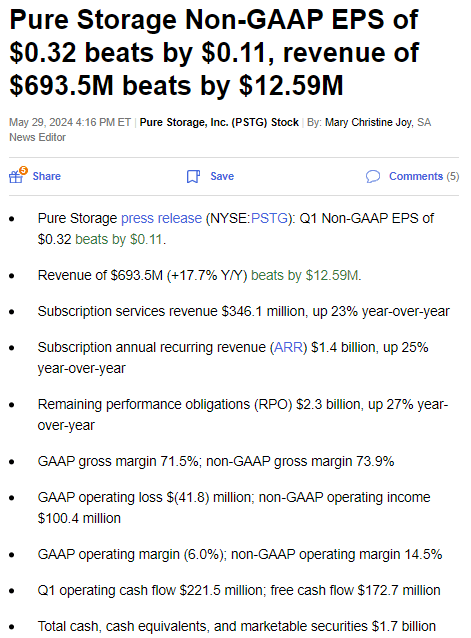

Pure Storage reported a strong Q1 quarter recently, with both top and bottom-line beats. The company reported revenue of $694 million (+18% YoY), beating consensus by $13 million. Non-GAAP EPS was $0.32, a $0.11 beat. The company also maintained its FY 2025 guidance of $3.1 billion. See below the results:

Pure Storage Q1 earnings (Seeking Alpha)

Market Opportunity – Pure Storage Gaining Share

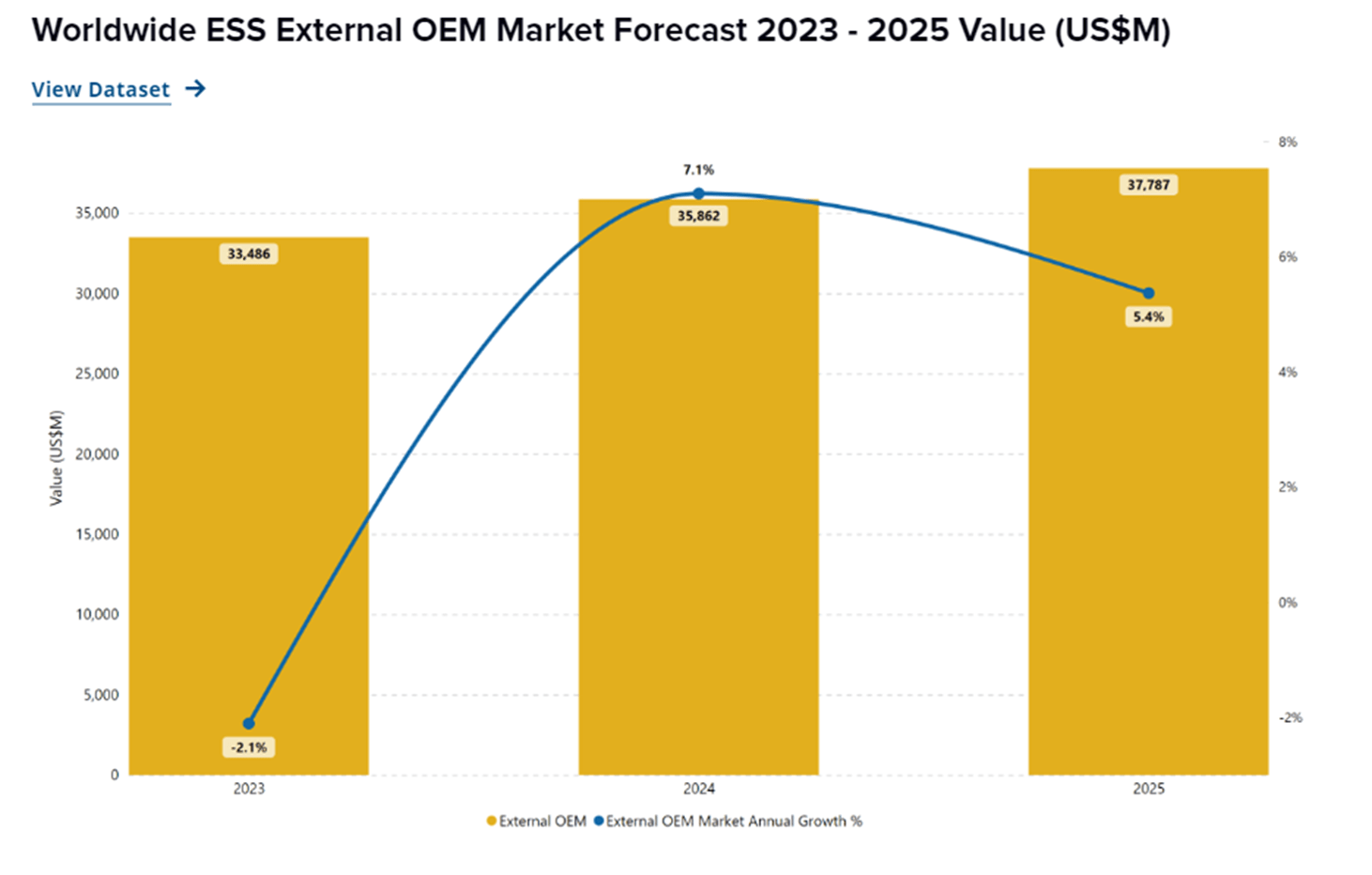

The ESS market size is worth around $35 billion with many established players including Dell, Pure Storage, NetApp, Huawei, Hitachi, and HPE (note that the ESS market only measures external storage sold by OEMs and excludes internal storage or storage sold directly by ODMs to hyperscalers). As per IDC, the ESS market declined by 1.2% in 2023 mainly due to the enterprise slowdown and macro factors. However, IDC believes that the market has reached a turning point and expects 7% growth in 2024 and 5% growth in 2025. It is projected that the increased demand will come from All Flash Array storage (AFA) which is the ideal high-speed storage for AI training and inferencing deployments.

ESS Market forecast (IDC)

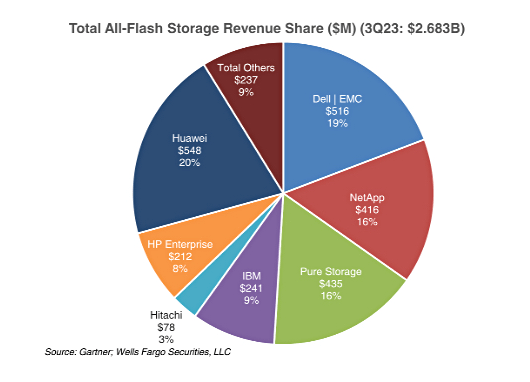

The AFA storage market, which Pure Storage is part of, accounts for about half of the ESS market. According to Gartner, Huawei leads the AFA market with a 20% market share, followed by Dell with 19% share, and Pure Storage with 16% share. Below chart shows market share among the top suppliers:

AFA Storage top suppliers (blocksandfiles.com)

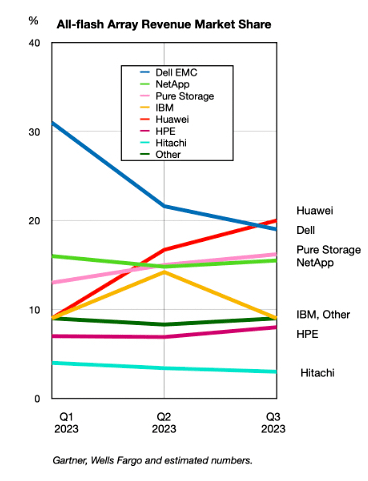

Pure Storage is showing a positive trajectory in terms of market share gains in the AFA market. In Q2 2023, the company had 14% market share, and was behind NetApp. However, it gained an additional 2% share in Q3 and overtook NetApp. Besides, Huawei passed Dell and became the world’s biggest AFA supplier (see below).

AFA revenue market share (blocksandfiles.com)

Strategic Focus: Product Leadership and Innovation

Successful companies differentiate themselves in the market by having a strategic focus. Pure Storage’s strategic focus is on product leadership. Thanks to its high-end flash offerings which are offered through a consumption model (as-a-service), the company has differentiated itself from the competition. We believe that this approach has enabled the company to become a leader in the ESS market, gaining market share in the process.

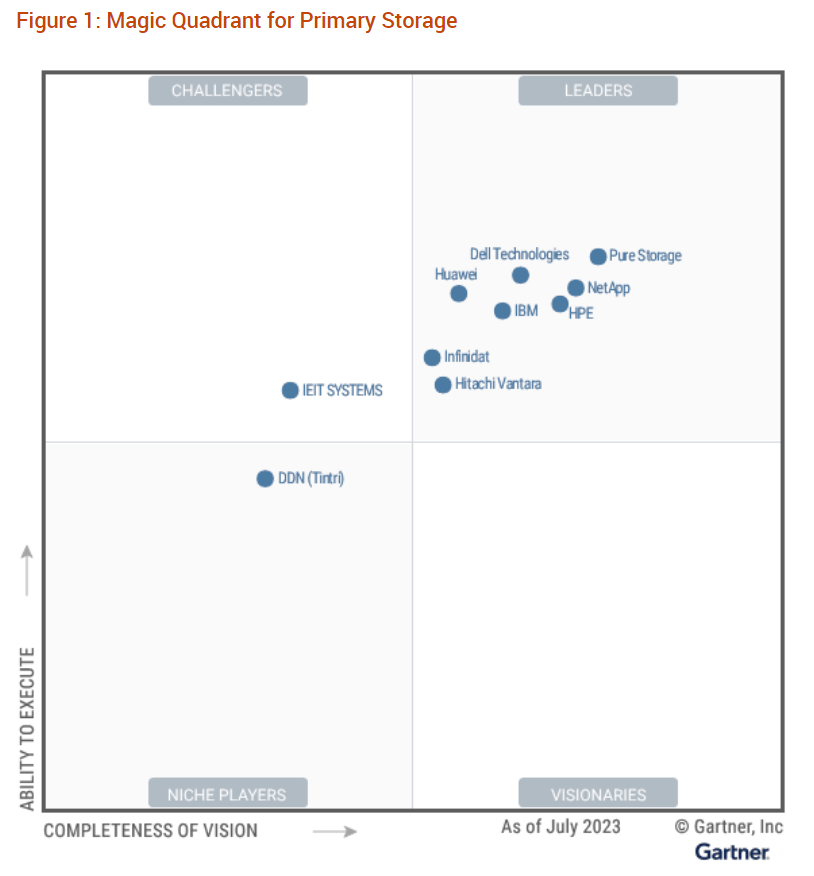

This strategic focus on high-end products has also helped the company to gain leadership positions in industry reports. Gartner’s magic quadrant shows Pure Storage as a leader in the primary storage category and points out its high performance and flexible consumption models as key strengths (see below)

Magic Quadrant for primary storage (Gartner)

We expect Pure Storage to continue its innovation strategy, investing in R&D and strategic M&A’s to maintain its competitive edge.

Bold Response to Competitive Threats

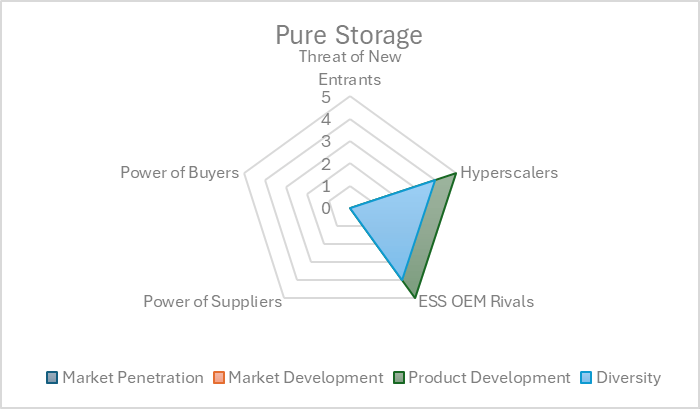

To assess Pure Storage’s competitive threats, we used the Porter’s 5 Forces model. We also applied the Ansoff matrix to understand how the company responds to these competitive threats (see below)

Porter’s Five Forces (Author)

In the model, we identified two main threats challenging Pure Storage’s position in the market:

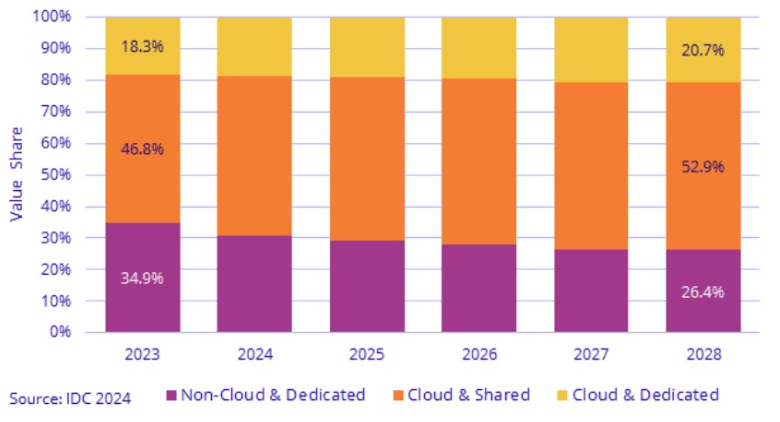

The rise of hyperscalers cloud storage offerings. As per IDC, Hyperscalers and Service Providers are becoming the main buyers of servers and storage. They currently account for over 60% of combined revenues, and their share is projected to reach 75% by 2028 (see below)

Storage spending projection (IDC)

The hyperscalers are mostly buying their storage from ODMs rather than OEMs. This creates a threat for Pure Storage, as its customers might prefer cloud-based storage solutions if they migrate to the cloud. The company’s mitigation strategy here is to position its hybrid cloud storage solution, which spans across on-premise and public cloud environments. Also, the company offers its Pure storage portfolio to hyperscalers to help them drive cost-savings. The company believes its Pure products offer hyperscalers multiple advantages, such as enhanced performance and cost savings on power, space and cooling costs.

ESS OEM Competition: The other risk for the company is the competition from OEMs. To mitigate this risk, the company positions itself on the high-end of the market and offers its products through a subscription model. This ensures its products are always up-to-date with the latest technology, which creates a moat against other vendors.

In summary, Pure Storage shows the necessary agility to mitigate competitive risks. The company continues to execute its growth strategy through product leadership and portfolio diversification.

Pure Storage Shows Strategic Execution

We want to check the company’s strategic priorities and how they align to its financial metrics. See below Pure Storage’s strategic priorities:

- Maintain product leadership with a high-value, high-margin storage strategy.

- Increase recurring revenue through subscription-based storage-as-a-service consumption model.

- Differentiate with a hybrid storage approach by integrating on-premise and cloud storages.

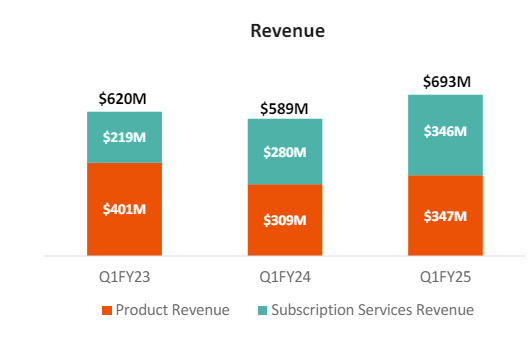

When we look at the company’s financial metrics, we see strong alignment of its execution and strategic priorities. The company’s revenue is accelerating double-digits. In Q1, revenue grew from $589 million to $693 million, up 18% YoY (see below)

Q1 earnings presentation (Pure Storage)

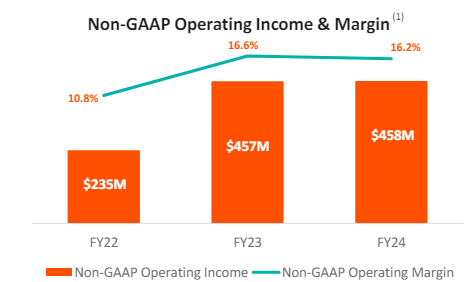

Also, the increase in operating margins shows that the company is able to maintain a premium offering strategy (see below)

Q1 earnings presentation (Pure Storage)

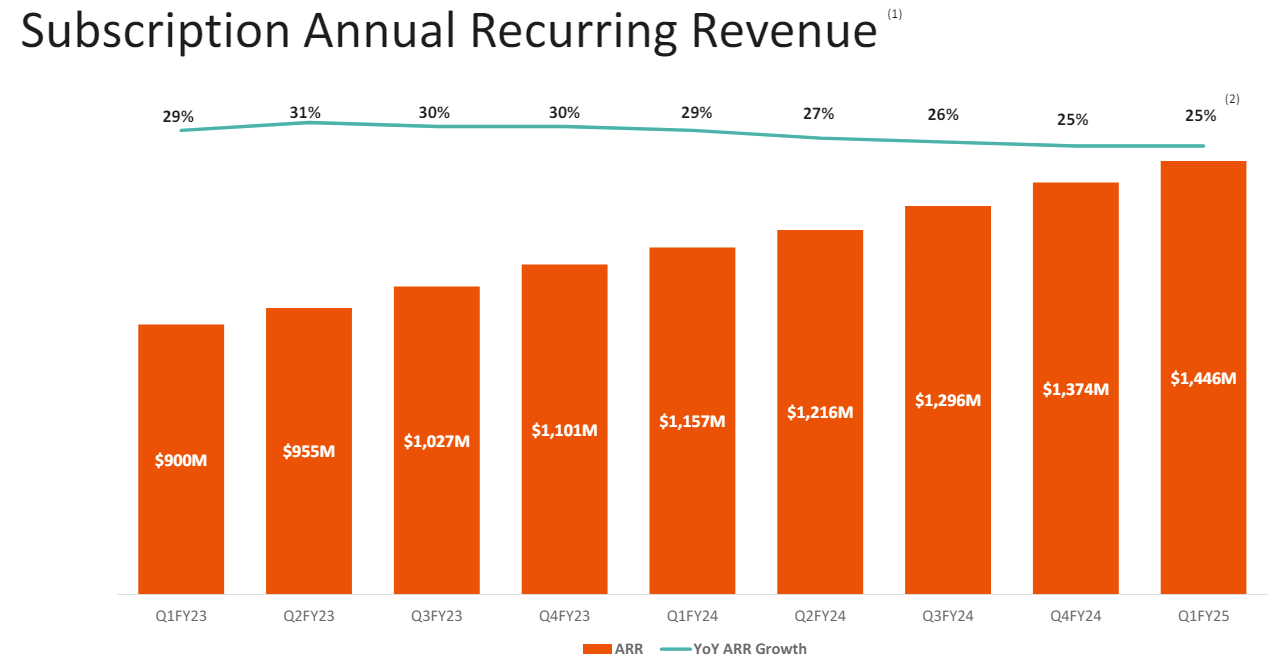

The subscription ARR metric measures the recurring revenue stream and is one of the most critical growth metrics to monitor (see below). It was $1.45 billion in Q1, up 25% YoY.

Q1 earnings presentation (Pure Storage)

The strong growth in revenue, ARR, and margins shows Pure Storage’s successful execution of its strategic objectives. It reflects the company’s success in maintaining its product leadership, and scaling its subscription-based consumption models.

Operational Discipline – Expanding Margins

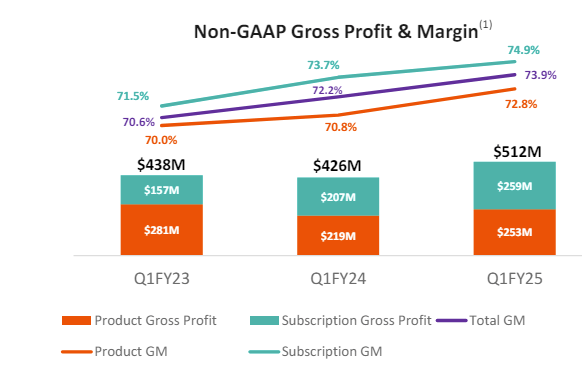

The company continues to show operational discipline, by keeping operational expenses under control. In Q1, gross margin increased to 74%, from 72% a year ago (see below).

Q1 earnings presentation (Pure Storage)

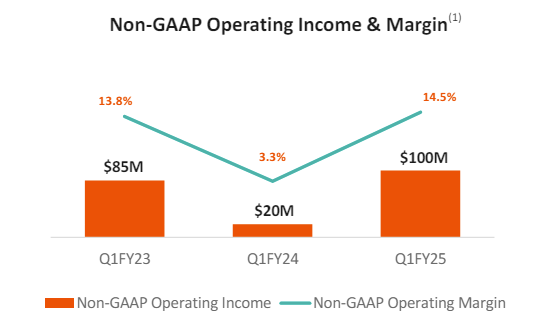

Q1 operating margin was 14.5%, up 3% YoY and exceeded guidance. The company is guiding for 17% operating margin in FY 2025. Management has a goal of increasing operating margins by one to two percentage points every year. From the FY 2024 Q4 call:

Kevan Krysler (CFO):

Margin for FY ’25 is in line with our longer-term goal of expanding operating margin by a percentage point or 2 each year and represents a 2-point increase from our FY ’24 guide that we communicated at the beginning of the year.

Q1 earnings presentation (Pure Storage)

The company also generated $222 million operating cash flow, 22% increase from last year. For the balance sheet, it ended the quarter with $1.7 billion in cash and $273 million in debt. Overall, it’s a very strong balance sheet.

Based on our analysis, we expect Pure Storage to maintain its operational discipline and expand its margins further due to the increasing mix of recurring revenue.

Valuation – Upside Potential

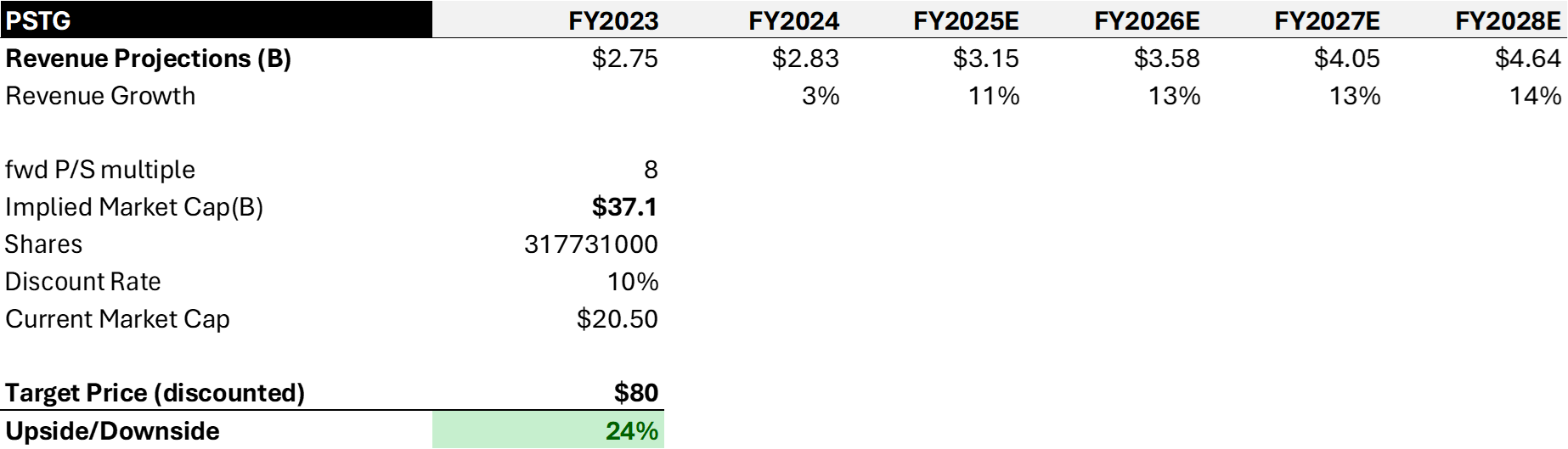

We will use the forward P/S multiple to value the company. The company is guiding for $3.1 billion revenue for FY 2025. Our revenue growth projection for the 2024-2028 period is a 13% CAGR due to the large AI storage potential that we see for the company.

We are assigning a forward sales multiple of 8, and assume the company will continue to grow at double-digit rate and expand its margins steadily. With a discount rate of 10%, our price target is $80. This indicates a 24% upside potential from the current price levels (see below).

Valuation model (Author)

Risks

We identified two major risks for the company. First one is the hyperscalers with their cloud storage offerings. Microsoft, Google and Amazon are all offering a variety of storage solutions as part of their cloud services, which could create challenges for Pure Storage. Secondly is the increased OEM market competition. More players are entering the market, including white-label ODM manufacturers. This situation can potentially pressure pricing and margins if the company cannot maintain its market leadership position.

Conclusion

We believe that Pure Storage is a great company and has key strategic attributes. The company brings innovation to the industry, shows product leadership, and is gaining market share in a difficult market. And due to its advantageous market position, the company is ready to capitalize on the significant AI storage opportunity.

Based on our analysis, we believe that Pure Storage can sustain its current price performance. We assign a fair value of $80 to the company.