undefined undefined

Abstract

Following my coverage of Pushed Manufacturers Holdings (NASDAQ:DRVN), for which I really useful a maintain score as I wished to watch the enterprise’s capacity to enhance margins over the subsequent few quarters, this put up is to present an replace on my ideas on the enterprise and inventory. I’m now upgrading my score to purchase as I consider the share worth weak spot is overdone. Whereas whole EBITDA margin is down, automobile wash EBITDA margin improved considerably, and I foresee two key catalysts that might drive margin to fulfill administration FY26 steering. Concerning the poor steering, I consider it was on account of administration being conservative, and they need to don’t have any points beating it.

Funding thesis

DRVN reported 4Q23 system-wide gross sales development of three% y/y to $1.513 billion, and whole same-store gross sales [SSS] elevated 3.9% y/y. Adj EBITDA got here in at $129 million, above the consensus estimate of $124.7 million, which interprets to an adj EBITDA margin of 23.3% (a 90bps slowdown vs. 24.2% seen in 4Q22). Publish-results, DRVN noticed its share worth drop by >10%, which I consider was means overdone and was primarily because of the weak margin efficiency and poor steering.

On margins, whereas the consolidated margin was down on a y/y foundation, there may be notable enchancment in automobile wash margins—phase margins elevated 600 bps sequentially to 23% in 4Q23 as DRVN higher controls variable prices (resembling detergent, water, and labor) within the home enterprise. Right here is the place it will get attention-grabbing: inferring from administration’s feedback, these enhancements look like structural margin enhancements, as they count on the 23% degree to maintain by means of 2024, with potential enchancment pushed by higher topline efficiency within the US. One level to notice right here is that DRVN can be concentrating on members with higher unit economics as they give attention to driving trade-up. As such, whereas membership penetration has softened (a unfavourable level), it doesn’t imply that the variety of members has stopped rising. The variety of members continues to develop, and as higher unit economics members develop into a bigger mixture of the pool, I believe margins might inflect larger as administration continues to execute on this side.

Hey Chris, Danny once more. So so far as the Automotive Wash membership query, look, we do not get into particular KPIs on the membership aspect. I’ll say we’re pleased with the truth that in 2023 we did develop members. In order that’s good. 4Q23 earnings results call

Administration’s Dream Huge Plan can be on monitor, with a goal to generate $850 million in EBITDA by 2026. By cadence, they count on development in 2025–2026 to double in comparison with 2024, pushed by stabilization in automobile washes and the Glass enterprise unit (extra beneath), upside alternatives from the ramp-up in regional and nationwide insurers for Glass, and economies of scale from the DRVN benefit platform. Particularly on Glass, listening to that integration with Glass is progressing forward of schedule was encouraging. I count on a excessive probability of acceleration in 2H24 as DRVN begins to reap early advantages from regional insurers. These advantages will proceed to pile up into 2025 as DRVN expands its attain to nationwide insurers. On condition that by 4Q23, the whole lot has been streamlined: point-of-sale, cellphone, lead administration, payroll, and compensation plans rolled out throughout all areas, I believe this places DRVN in a stronger place to focus on nationwide insurers in FY25.

DRVN

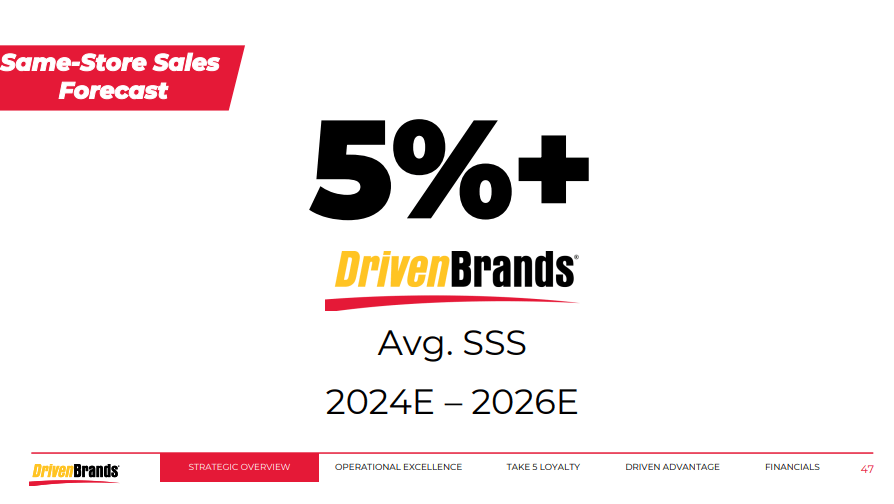

As for the poor steering, I do agree that, on a headline foundation, it was not tremendous constructive. Administration guided to 3-5% SSS development and $535–565 million of adj. EBITDA, which means a 22.8–23.1% margin. That is implicitly a information down (for SSS development) from administration’s earlier information in September 2023, because the excessive finish of the present steering was in keeping with the steering given beforehand. Nonetheless, from the best way I’m seeing it, I believe the information could be too conservative, as administration is incorporating headwinds from the macro backdrop and climate on the decrease finish of its information. The truth that administration truly introduced up climate headwind was attention-grabbing as a result of they’ve by no means famous that as a headwind, so this reveals how conservative they’re. On macro, I believe it is honest to say that issues stay unsure, however I additionally wish to level out that the macro scenario is comparatively higher than in 2023. Whereas the labor market stays sizzling and housing stays an issue within the US, at the very least inflation has come down lots. Let’s additionally not overlook that DRVN nonetheless has a powerful upkeep income stream that continues to be strong—printing 4.7% comps development, reflecting continued power in Take 5.

Valuation

Personal calculation

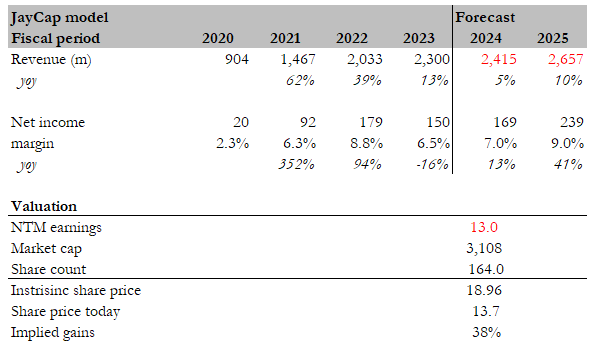

My goal worth for DRVN based mostly on my mannequin is ~$19. My mannequin assumptions are that DRVN will meet the excessive finish of income steering, rising 5% in FY24, as I consider administration steering is simply too conservative contemplating the comparatively higher macro in FY24 vs. FY23 and the potential upside from Dream Huge and Glass integration. My expectation for FY25 stays the identical: ~10% top-line development. Observe that I’m additionally being very conservative on FY25 development expectations, as administration’s FY26 goal consists of income of $3.4 billion, which might indicate a CAGR of ~19% from the midpoint of FY24 steering ($2.4 billion). Importantly, these FY26 targets embrace little to no affect from M&A, because the targets have been formulated utilizing natural development estimates; therefore, there may be potential for upside.

As for earnings margin, I’ve develop into extra assured that margin will speed up in FY25 to 9% given the give attention to driving trade-ups in memberships and contributions from the Dream Huge plan. If DRVN have been to execute as I anticipated, I don’t see an issue with DRVN sustaining the present multiples as earnings development goes to develop a lot sooner than the topline (I count on ~40% earnings development in FY25). For benchmark functions, when DRVN grew earnings at 94% in FY22, the inventory traded at mid-20s ahead PE. My FY25 41%, which is barely lower than half of FY22 development, implies that DRVN ought to commerce at a low-teens a number of.

Threat

There are a variety of potential dangers. For one, if the continuing demand headwinds within the automobile wash business persist, it would affect DRVN income development instantly. As well as, a significant catalyst for margin growth is the Glass enterprise unit integration; any mis-execution right here will affect margin efficiency.

Conclusion

I’m upgrading my score on DRVN from maintain to purchase. Whereas the current share worth weak spot might be attributed to considerations about margin efficiency and steering, I consider that is an overreaction. Regardless of a slight dip in total margins, the automobile wash phase is experiencing vital margin growth. This demonstrates DRVN’s capacity to successfully management prices and enhance profitability inside this core enterprise unit. Additionally notably, the combination of Glass is progressing forward of schedule. Lastly, I consider administration’s steering is overly conservative, incorporating potential headwinds from the macro surroundings and climate into the decrease finish of the vary. Whereas some uncertainty persists, the general macro scenario in 2024 seems barely extra favorable in comparison with 2023.