AzmanJaka

Funding Thesis

Quest Diagnostics (NYSE:DGX) is an exceptionally steady firm that operates a incredible enterprise. During the last 10 years, its complete return has exceeded that of the S&P500, and within the final 20 years, its shares have by no means fallen by greater than 36%, even in the course of the crises of 2008 and 2020. This reality underscores the resilience and power of the enterprise.

Nevertheless, in 2020, the corporate benefited from COVID-19 testing, which atypically boosted development and margins, resulting in an overvaluation of Quest. The corporate just lately offered Full 12 months 2023 outcomes, the place it could possibly be noticed that earnings had been already absolutely normalized. For my part, this offers an splendid entry level, as we’d not be shopping for inflated earnings.

Complete Return vs S&P500 (Looking for Alpha)

Enterprise Overview

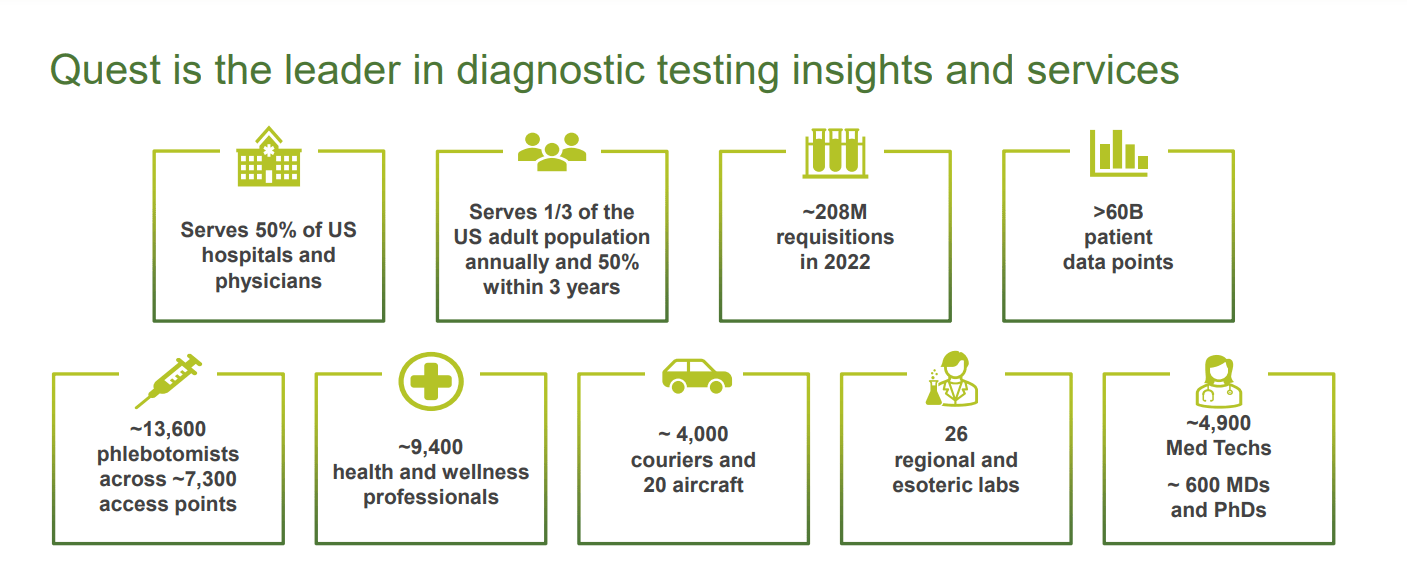

Quest Diagnostics is a number one supplier of diagnostic data companies. The corporate affords a broad vary of companies, together with laboratory testing reminiscent of routine blood work, infectious illness testing, genetic testing and different diagnostic options. They serve a wide range of clients, together with sufferers, physicians, hospitals, and employers.

Quest Diagnostics performs an important function within the healthcare trade by offering correct and well timed diagnostic data that helps healthcare professionals make knowledgeable choices about affected person care. The corporate operates an enormous community of laboratories and affected person service facilities, making it one of many largest and most well-known diagnostic testing firms globally.

Quest Investor Presentation

M&A Alternatives and Economies of Scale

The diagnostic companies market is very aggressive but in addition very fragmented, with quite a few ‘Mother-and-Pop’ companies that had been based years in the past however function just a few regional clinics. These companies are sometimes necessary M&A targets for the corporate, as, in lots of instances, these operators didn’t develop succession plans, making promoting their enterprise an inexpensive choice to exit.

The corporate estimates that between 2023 and 2026, acquisitions might add not less than 1 to 2% annual development. This added to the organic growth typical of the sector is kind of useful in the long run, because it permits the corporate to proceed growing its scale and geographical growth, which is important in the sort of enterprise.

Quest Investor Presentation

Scale is important for a laboratory since every check requires somebody to carry out it and somebody to research it, each of whom obtain a wage (clearly). As an instance, let’s take into account a small regional laboratory with a medical analyst incomes $100 USD per day and often dealing with one shopper per day. The fee per check for the laboratory could be $100.

Nevertheless, if the laboratory operates on a bigger scale and manages to serve 100 shoppers in someday, the fee per check could be $1 as usually a single medical analyst can carry out and analyze many exams concurrently. Moreover, there’s an growing quantity of equipment (reminiscent of that manufactured by Danaher and Thermo Fisher) that automates this course of, permitting extra samples to be analyzed with fewer analysts. These developments finally replicate within the revenue margins of bigger companies. That is exactly how the corporate tasks that its margins might develop between 0.75% and 1.5% within the subsequent three years.

Quest Investor Presentation

Key Ratios

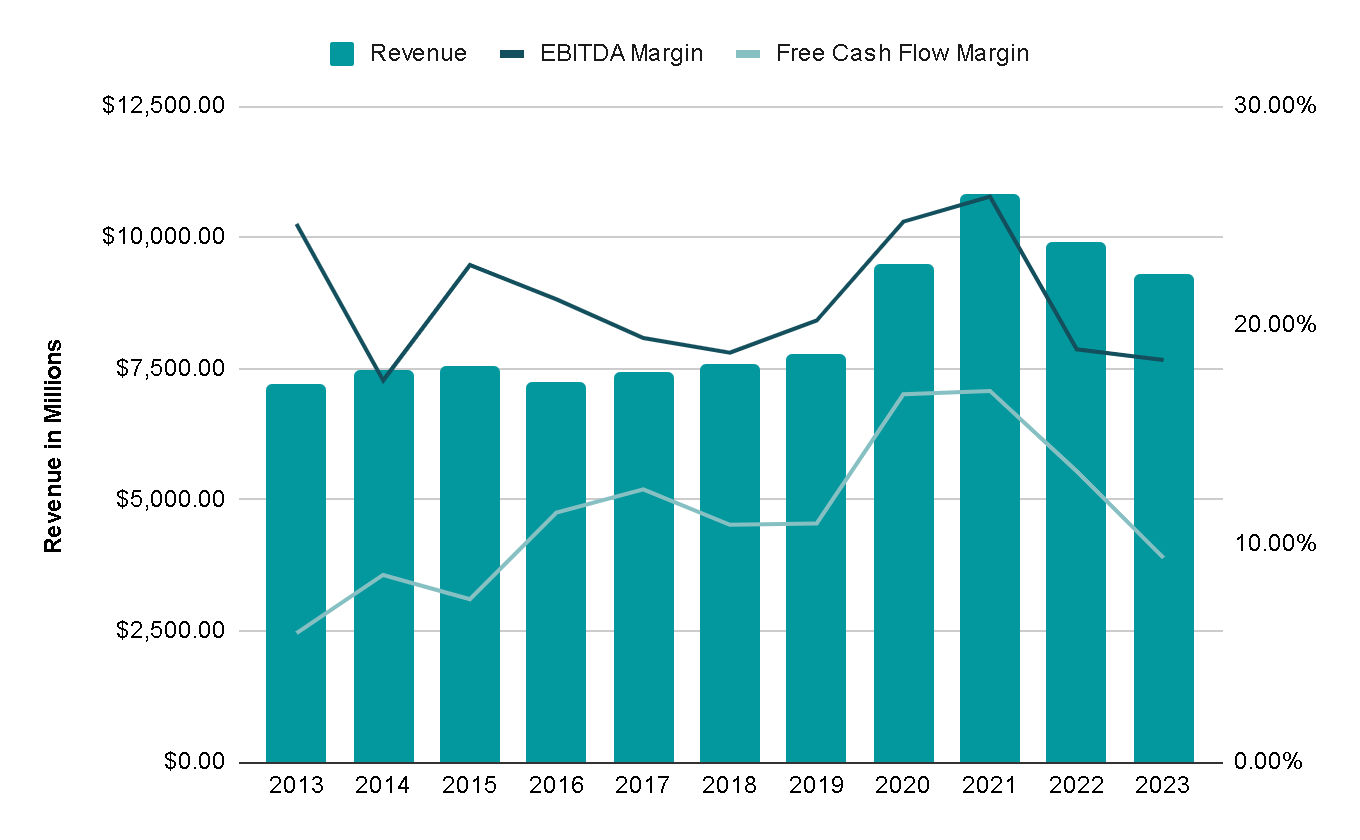

On February 1, the corporate introduced its outcomes for the Full 12 months 2023. This 12 months, the corporate skilled a 6% lower in its high line, bringing the expansion fee for the final decade to 2.5% yearly. Moreover, the EBITDA margin returned to ~18%.

Whereas these outcomes could initially seem unfavorable, the fact is that this adjustment was vital to contemplate Quest as a long-term funding.

Creator’s Illustration

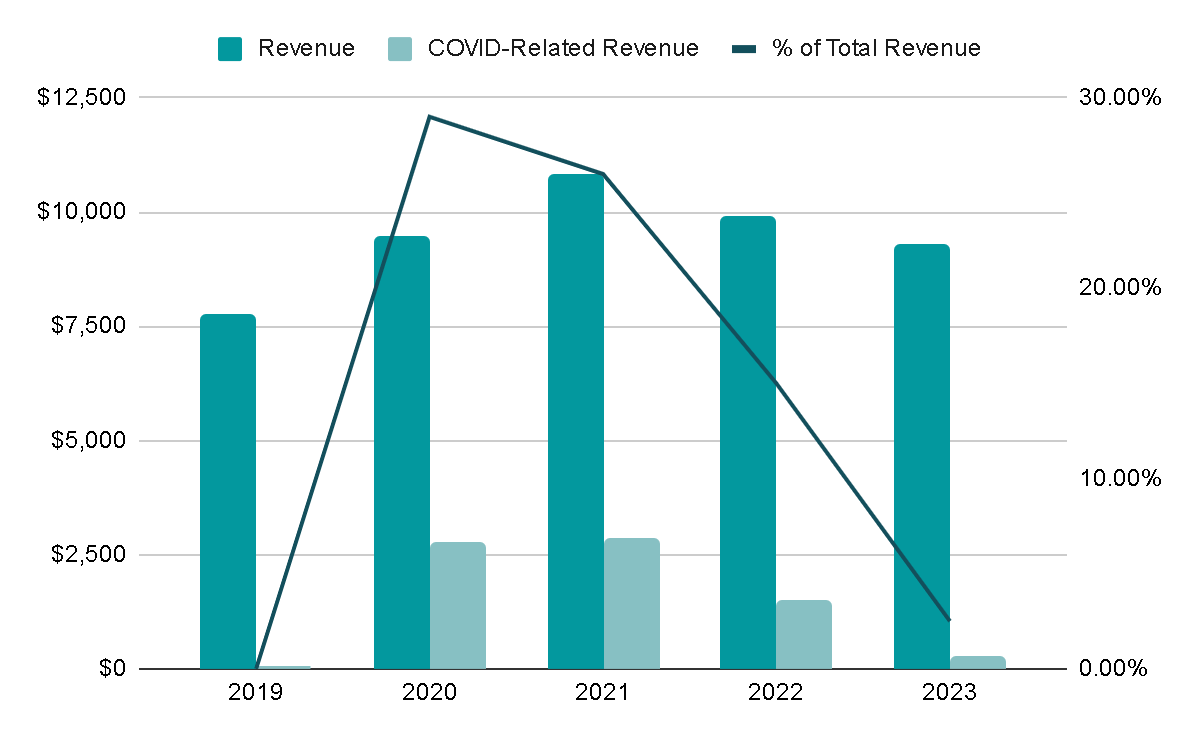

It’s because, in 2020, the corporate skilled a ‘increase’ in its earnings resulting from COVID-19 exams, which had increased margins than regular. This surge led to a development fee of 15-20% throughout these years, with margins reaching 25%. Nevertheless, this stage of development and margin shouldn’t be sustainable and was distorting the true worth of the corporate.

The state of affairs has now normalized, and if one had been to purchase the inventory immediately, they might not be buying inflated earnings. In 2020, COVID-related income represented 30% of complete income, and at present, it’s lower than 3%.

Creator’s Illustration

Over the last 12 months, the corporate as soon as once more issued debt, particularly virtually $2.6 billion. This follow was already frequent in earlier years when the corporate relied on debt to finance its operations.

It’s noteworthy that in 2020 and 2021, years during which rates of interest had been traditionally very low, the corporate selected to not difficulty debt and as a substitute financed itself purely from the money generated by the enterprise. Nevertheless, now that charges are rising, they’ve opted to difficulty a big quantity of debt. For my part, this represents a poor capital allocation choice and doesn’t communicate effectively of the administration. They didn’t reveal a long-term imaginative and prescient by securing debt at low charges once they had the chance, they usually might have saved the surplus money generated by the COVID-related income for a time when this earnings would doubtlessly disappear.

Creator’s Illustration

Concerning the standard use of capital, during the last 5 years, the corporate has allotted ~10% to reinvest within the enterprise and make acquisitions, 35% to repay debt, and 45% to remunerate shareholders by inventory buybacks and dividends, utilizing the surplus money generated in the course of the COVID years.

Basically, this looks like an inexpensive capital allocation technique, and I do not see any notable factors, neither optimistic nor adverse.

Creator’s Illustration

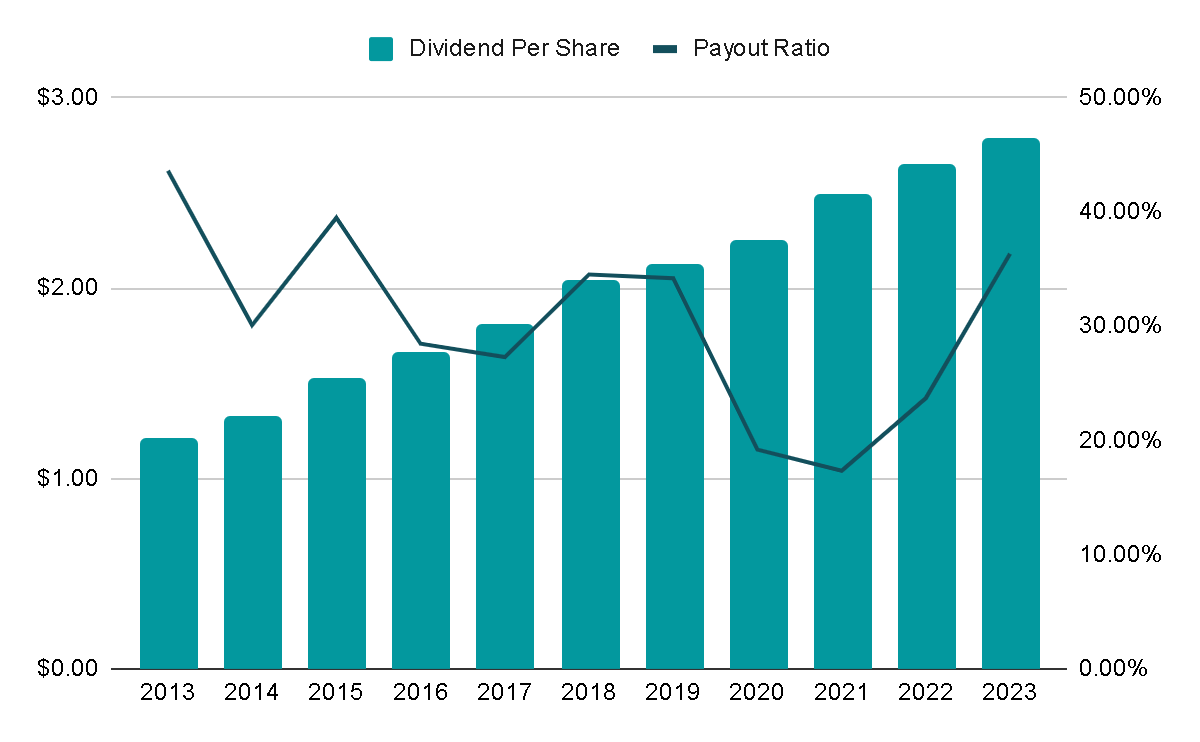

What does seem attention-grabbing is the rising dividend distributed by the corporate. This has elevated at an annual fee of 8.7% during the last decade, and the Free Money Circulate Payout Ratio is barely 36%, offering ample room for additional will increase by distributing extra of the generated money.

At present, the Dividend Yield is ~2.4%, so though we could not take into account it a pure dividend inventory, it does generate attention-grabbing further money move in a steady enterprise

Creator’s Illustration

Valuation

Contemplating every little thing we have now analyzed in the course of the analysis, I consider {that a} cheap and even conservative development for the highest line could be 3% yearly within the subsequent 5 years, together with a margin growth of 200 foundation factors.

This might lead to roughly $1.2 billion of earnings generated by 2028, which, with a 15x PER a number of, would translate to a Market Capitalization of $20 billion. This might signify an annual return of ~11%, plus the dividend of two.4%. Provided that the assumptions are very possible and the enterprise is kind of strong, I discover this to be a beautiful sufficient return.

Creator’s Illustration

I selected the PER based mostly on the historic common a number of. Nevertheless, if we take into account that in 2021 the a number of was artificially low, we might conclude {that a} vary of 15 to 20x earnings wouldn’t be uncommon. Subsequently, the valuation has a number of catalysts that might subsequently shock and ship a higher return than anticipated.

P/E Ratio (Looking for Alpha)

Dangers

The corporate’s most vital threat is its susceptibility to American authorities laws. As an example, the Defending Entry to Medicare Act (PAMA) is laws in the USA geared toward reforming the cost system for scientific diagnostic laboratory exams, together with these supplied by firms like Quest Diagnostics.

PAMA was enacted to determine a market-based cost system for scientific laboratory companies, making certain that Medicare pays correct and truthful costs for these companies. Consequently, Quest Diagnostics could expertise modifications in reimbursement charges for exams lined by Medicare. If the market-based charges are decrease than historic charges, it might affect the corporate’s income. The corporate is effectively conscious of this threat and is taking vital measures. In actual fact, evidently Congress has postponed the choice on PAMA, and there will likely be no verdict in 2024. Subsequently, we could have better certainty for this 12 months. However, sooner or later, the corporate should adapt to those modifications, and this consideration should be taken under consideration.

Quest Investor Presentation

Last Ideas

It’s clear to me that the market, and even the administration itself, significantly overvalued the corporate in the course of the COVID period, resulting in the 28% drop for the reason that final all-time excessive. However, this drawdown of lower than 30% in an organization that had inflated earnings and has seen a 40% lower in its EBITDA during the last two years signifies how strong this enterprise can usually be.

Concerning the basics of the enterprise, they continue to be the identical and are even higher than earlier than COVID-19. The valuation offers sufficient margin of security to attain a 12-13% return on a strong enterprise that’s not buying and selling with inflated earnings. For all these causes, I consider that on the present value, the corporate is a ‘purchase‘.