On this article, I supply a commerce concept: brief junk bonds with put choices. I additionally recommend a hedging technique that ought to assist mitigate the price of the commerce. I believe it is a very low-risk commerce with large potential upside. After explaining the small print of the commerce, I’ll focus on the financial assumptions that underpin my advice.

As at all times, I might enormously admire any suggestions, particularly disagreements. If I’m fallacious about one thing, I wish to know. I don’t wish to lose cash any greater than you do.

The Commerce: Quick Excessive-Yield Bonds with “HYG” Places

My funding concept is to brief junk bonds. To me, this looks like such an apparent and low-risk alternative as to make me wonder if there could possibly be one thing vital that I’m lacking.

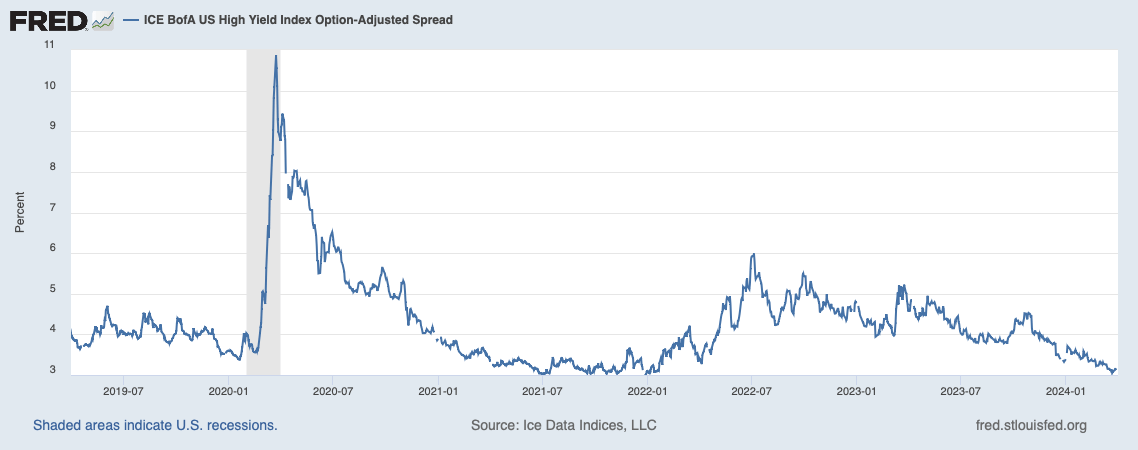

Possibility-Adjusted Excessive Yield Spreads (St. Louis Federal Reserve)

Because the graph exhibits, “option adjusted high-yield spreads” are approaching all-time lows. I count on this unfold to widen sharply over the following 12 months. This may stress junk bond costs and generate earnings for anybody brief these securities. I believe this can show to be a worthwhile commerce by itself, however may also be an efficient and cheap hedge for an fairness portfolio.

I’m shopping for put choices on the iShares iBoxx $ Excessive-Yield Company Bond ETF “HYG”. Premiums on these choices are fairly low cost. Implied Volatilities are solely 6-9% in comparison with 12-15% for many equities. One should purchase $100,000 in notional worth of at-the-money HYG places for $3,000 to $4,000. I’ve been shopping for at-the-money put choices with 6-to-9-month expirations. These sometimes have a delta of round 50%, so on this instance one would successfully be brief $50,000 of HYG.

I recommend that you just think about hedging a minimum of a few of your brief HYG place by shopping for 3–5-year Treasury notes or associated ETF’s. The typical maturity of belongings within the HYG is roughly 4.5 years, and its common period is roughly 3.5 years. You can additionally write a placed on a Treasury ETF. When you determine to write down a put, make sure you purchase a put that’s additional out of the cash; as Nassim Taleb would possibly say, make sure you minimize off your tail (threat.)

There are two causes to hedge your brief place. First, you’ll be able to defray the price of your HYG premiums. When you purchase Treasury notes, the curiosity you obtain will just about pay for the HYG premiums. When you elect to write down places, the premium you gather will assist offset the price of your “long HYG puts.” As you’ll be able to see from the graph, credit score spreads can stay slim for a very long time earlier than they reverse discipline.

A extra vital cause to hedge is that risk-free rates of interest may decline, attenuating and even offsetting any good points made on HYG spreads widening out. That is very more likely to happen if we enter a recession.

When you choose, you may at all times write out of the cash places on the HYG. Nonetheless, as famous above, premiums on these choices are constrained. Furthermore, as you’ll be able to see from the graph above, expansions in high-yield spreads may be fairly violent, and also you wouldn’t wish to miss such a transfer. Plus, if junk spreads do widen dramatically, it’s possible that HYG choices volatility will bounce.

A extra oblique solution to hedge is to purchase housing-related shares (or write places for premium.) Residence constructing shares are a sensible choice, however I choose mortgage insurers and title insurers. If charges drop sharply, these will profit from each new and current residence gross sales. Additionally, whereas I don’t now personal New York Neighborhood Bancorp. (NYCB), keep in mind that, with its Flagstar acquisition, it now has a really massive nationwide mortgage operation.

Hopefully, our commerce will work whatever the final financial end result. If the economic system softens, as I count on, I think that long term rates of interest could stay elevated as a result of immense overhang of Treasury debt issuance and potential inflation considerations if the Fed eases sharply. However even when rates of interest do collapse, our hedges ought to profit whereas credit score spreads widen.

If the economic system had been to strengthen, it’s nearly sure that long term rates of interest would rise, which can generate good points. As charges rise, assume, this can be very unlikely that spreads will slim considerably additional.

One cautionary be aware. When buying and selling HYG choices, or any illiquid possibility, ALWAYS use restrict orders. Whereas I’ve had no issue shopping for longer dated HYG choices, they will have gaping bid / ask spreads.

Why are Credit score Spreads so Slim?

Frankly, I’m puzzled by investor’s complacence about junk bonds, particularly contemplating their latest freak-out about industrial actual property. Junk bonds have about the identical refinancing dangers as industrial actual property credit score. Plus, Junk debt typically has no collateral.

In actual fact, default charges on high-yield debt have already begun to rise. For empirical proof, please seek advice from this SA article by Macrotips.

It’s my speculation that junk yields are being suppressed by the general “risk on” funding local weather and a flood of liquidity into personal credit score funds that now have money burning a gap of their pockets. However for causes enumerated under, I believe that this liquidity is about to change into scarcer.

Moreover, till very not too long ago buyers had been anticipating DRAMATIC price cuts by the Federal Reserve, which might have generated large good points in Junk bonds and mitigated refinancing threat. However clearly, short-term price cuts is not going to be as dramatic as most anticipated initially of the yr (absent a disaster.)

After all, it’s potential that there’s something extra elementary occurring that’s eluding me. I’ve heard many individuals contend that junk bond debtors in the present day are larger high quality than they as soon as had been. I’ve been unable to corroborate this rivalry, nevertheless it definitely appears potential and deserves additional investigation.

However even when this rivalry is true, there could possibly be an offsetting issue. Non-investment grade borrowing over the previous couple of many years more and more has been “covenant lite.” This enhances the borrower’s capacity to additional leverage in addition to his bargaining place relative to the creditor.

The composition of the HYG doesn’t appear to corroborate the high-quality argument. Client cyclical corporations characterize the largest sector at 18% adopted by communications at 16%, client non-cyclical at 12% and capital items at 11%. I used to be stunned to find that power corporations represent solely 12% of the HYG. I had thought power’s share was a lot larger.

Credit score Spreads are More likely to Widen

After all, simply because credit score spreads are slim doesn’t imply {that a} hole wider is imminent. Because the above chart exhibits, spreads can stay suppressed for a very long time.

Nonetheless, I count on a number of forces to conspire to change what has been a positive credit score setting.

First, I think the economic system just isn’t as sturdy because it seems to be. Earlier than a slight latest uptick, main indicators had declined for 14 consecutive months. I’ll admit that the latest sturdy payroll quantity was a shock to me. Besides, many employment indicators such a JOLTS and quits are declining.

Furthermore, whereas the March payroll quantity was sturdy and exhibits jobs rising by 3 million up to now 12 months, the family survey exhibits basically zero progress.

Complete Employment (Family Survey) (St. Louis Federal Reserve)

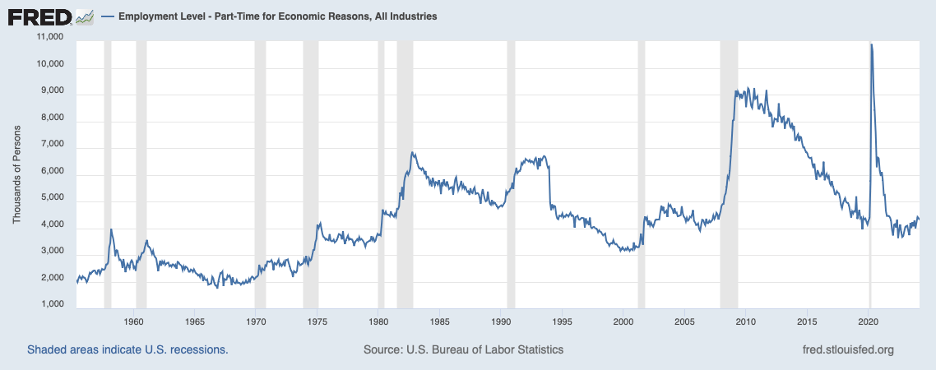

Or think about this chart. It presents certainly one of my favourite indicators; “workers employed part-time for temporary reasons.” As you’ll be able to see, this metric has been an especially good main indicator of recession, with only a few false positives. The variety of part-time staff declines throughout financial expansions, however then begins to extend simply earlier than recessions.

Half time employment (St. Louis Federal Reserve)

I ought to emphasize that lately I’ve even much less religion in financial (and political) surveys than I used to. For a number of causes, there are critical issues with information assortment. As an example, nobody anymore solutions telephone calls from unfamiliar numbers. Plus, latest immigration tendencies in all probability distort a few of these numbers.

Anyway, my main causes for anticipating a slower economic system hinge on Federal Reserve coverage. I consider the Fed is primed to reverse its accommodative insurance policies and switch extra restrictive.

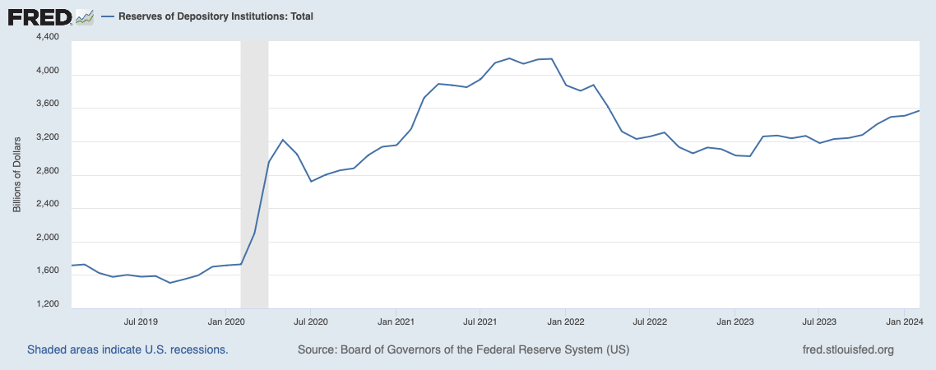

For a few years, I’ve been deeply involved about systemic liquidity. (see The Looming Liquidity Crunch). ). After flooding the system with a firehose of liquidity through the COVID disaster, the Fed in early 2022 started to take away liquidity by means of “Quantitative Tightening.” When this coverage helped trigger the failures of three massive regional banks in March 2023, the Fed reversed course.

Financial institution Reserves (St. Louis Federal Reserve)

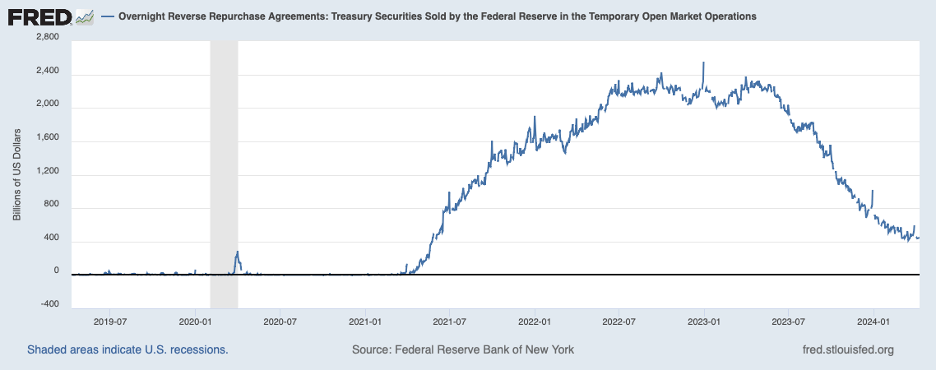

To make certain, the Fed continued “QT” however targeted on paying off “Reverse Repo” debt whereas permitting financial institution reserves to develop (Keep in mind that in in the present day’s topsy-turvy world, when the Fed raises the rate of interest it pays banks on reserves, it really will increase reserves and eases liquidity circumstances.) Since MMMF’s merely swapped RRP into newly issued T Payments, there was minimal impression on systemic liquidity. (I’ve borrowed a lot of this evaluation from Stephen Anastasiou . I believe he does wonderful work.)

Reverse Repos Federal Reserve (St. Louis Federal Reserve)

At the moment, the Reverse Repos are nearly gone. If the Fed needs to proceed QT, it should begin lowering financial institution reserves as soon as once more. This may drain systemic liquidity. As reserves decline, banks might be obliged to promote long term belongings to fulfill regulatory liquidity hurdles. Plus, after all, the persevering with humongous authorities debt issuance will work to cut back liquidity, the whole lot else equal. If the Fed elects to proceed QT, it may precipitate a critical liquidity crunch.

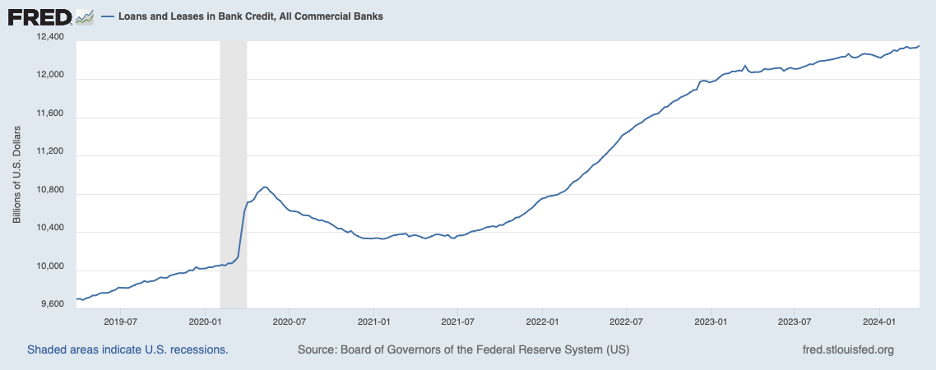

However my greatest concern is expressed within the chart under. Traumatized by arbitrary and punitive regulation, financial institution lending is grinding to a halt. Since February 2022, financial institution loans have elevated lower than 2% (lower than the speed of inflation) regardless of the close to 20% yr to yr bounce in reserves. Our financial institution bureaucrats have lastly achieved regulatory nirvana; banks are refusing to imagine any threat by any means. Absent a dramatic change within the regulatory regime, I see no cause why banks will start to lend extra freely.

Loans and Leases in Financial institution Credit score (St. Louis Federal Reserve)

As is well known, a lot latest US credit score progress has come from shadow financial institution and personal credit score sources. However do not forget that these entities can not create deposits. They’ll solely lend so long as they will borrow (or elevate fairness) from a 3rdcelebration. At the moment, their enterprise depends upon extra systemic liquidity. At its core, new credit score should in the end derive from banks (or from the federal government itself, which is the place a lot of in the present day’s money originated.)

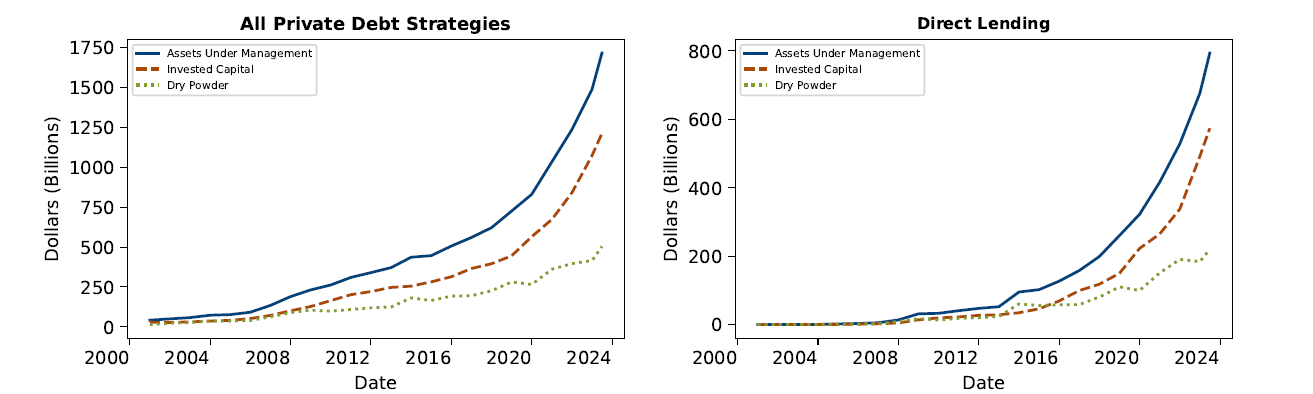

I’ve borrowed these graphs from a superb February 23, 2024 Federal Reserve report.. Be aware that although personal credit score has elevated dramatically, it’s nonetheless lower than 15% of complete financial institution lending.

Non-public Credit score Lending and “Dry Powder” (Federal Reserve)

One remaining level. It’s important that buyers preserve an eagle eye on Treasury auctions. With immense issuance which can solely develop and banks woefully constrained, I believe {that a} “failed” public sale is very possible. On this occasion, long term rates of interest will spike sharply larger.

underworld111/iStock by way of Getty Photographs