xijian

Based in 1991, RADCOM (NASDAQ:RDCM) is an organization that gives a community high quality assurance platform for telecommunication operators and communication service suppliers (CSP).

All-time share efficiency has been disappointing since going public in 1997 at a value of $45.5. The inventory initially carried out fairly properly, hitting all-time excessive of $78 in the course of the dot-com increase in 2000. Nevertheless, share value has plunged and has been buying and selling below $20 value stage for more often than not since then. RDCM has gained some momentum as of late regardless of the current pullback. Over the previous 12 months, the inventory had truly been up over 20% and reached $11.8 per share till April, when it ended up seeing a correction to $9 value stage upon the information of its recently-appointed CEO, Man Shemesh, stepping down. The inventory stays on the identical value stage at present, although the inventory continues to be up over 18% YTD.

I fee RDCM a purchase. My 1-year value goal of $10.7 tasks over 13% upside. I imagine RDCM will proceed to learn from secular catalysts and a strong positioning within the 5G community monitoring market. The current pullback additionally offers engaging entry level.

Monetary Evaluations

ycharts

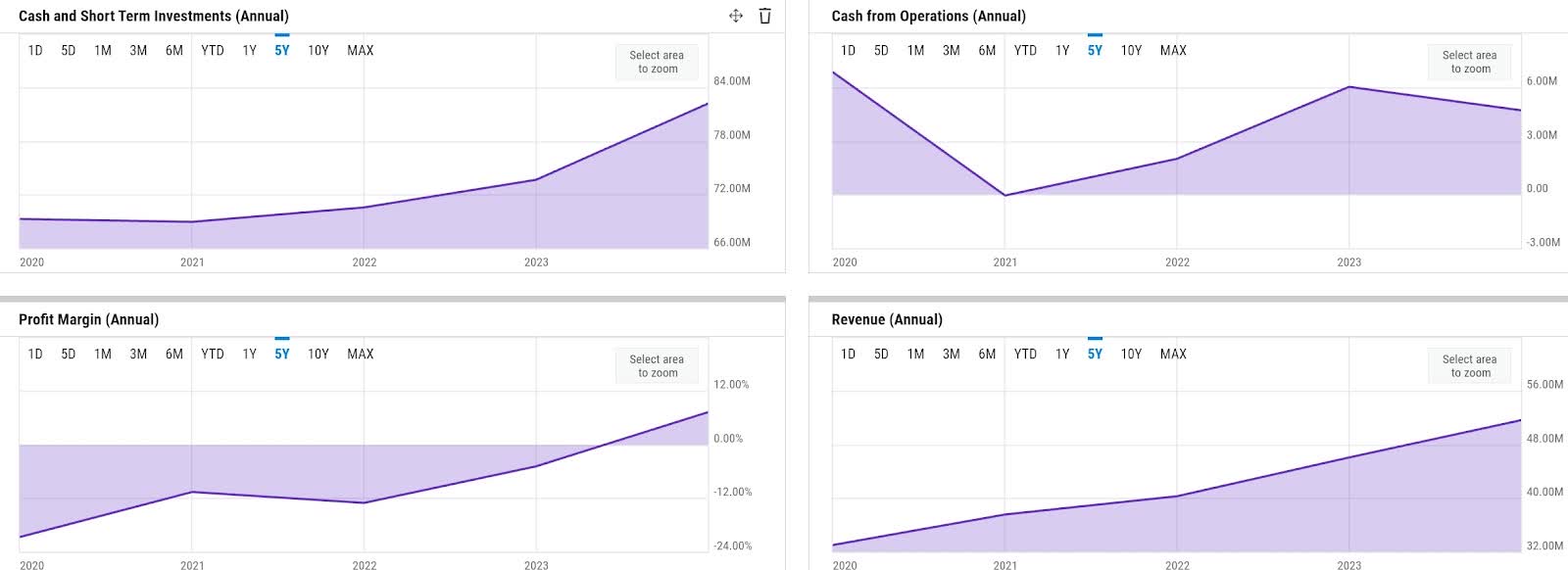

Fundamentals are comparatively first rate. Excluding 2021, when RDCM noticed weak point in its LATAM enterprise, income progress has been comparatively regular above 12% in current instances. In FY 2023, RDCM delivered $51.6 million of income, an over 12% progress YoY. RDCM additionally reached breakeven in FY 2023, with GAAP web margin increasing to over 7% in FY 2023. Having been unprofitable yearly for the previous 5 years, the breakeven in FY 2023 can be a milestone 12 months for RDCM.

Although working money move (OCF) technology has declined to $4.7 million in FY 2023, it has total been on an growth since 2021. Extra importantly, RDCM seems to have demonstrated an excellent functionality to maintain its personal operations. RDCM’s liquidity has expanded over the previous 5 years, and it has not as soon as relied on exterior financing over the identical interval. In FY 2023, RDCM’s liquidity stood at over $82 million. Given the very minimal CAPEX wants yearly, I might think about RDCM to be at a comparatively strong liquidity place at present.

Catalyst

I anticipate RDCM to proceed to learn from the secular 5G tendencies in 2024 and past. General, this may assist improve demand for its providing. RDCM is well-positioned to seize this chance, for my part, resulting from its robust merchandise and market-leading fame it has gained by means of its success in touchdown blue-chip CSP purchasers.

In This autumn earnings name, the administration indicated that RDCM will proceed to embrace AI to boost community monitoring high quality to assist ship higher 5G service assurance:

As they undertake next-generation cloud know-how to optimize value and roll out 5G, the present macroeconomic panorama presents new alternative for RADCOM, a number one international cloud-native assurance resolution. We proceed to boost our software program with further automation, analytics and intelligence and AI-based capabilities to convey worth and broaden use instances for our prospects because the adoption of the 5G know-how progress.

Supply: Q4 earnings call.

Service assurance is a mission-critical exercise for CSPs, because it serves as the idea for numerous key facets of the core enterprise, akin to community efficiencies, SLA (service stage settlement) compliance, and even monetization technique, for my part. Given the rise of 5G adoption, many CSPs might want to deal with growing a brand new type of service assurance functionality that’s totally different from the prevailing ones. As highlighted by an article by TMN, 5G service assurance must be extra “contextual”:

Contextual service assurance in a 5G community refers back to the means to observe a horizontal infrastructure working a number of service sorts that may be dynamically requested, scaled and terminated. This community may also deal with such extraordinarily giant knowledge volumes – each by way of buyer site visitors and community signaling. Conventional service assurance instruments and the handbook oversight by engineers of the community within the operations heart will probably be neither sensible nor potential.

Supply: TMN.

As such, I imagine the AI integration ought to create worth for RDCM not solely as a result of it helps enhance operational efficiencies by means of monitoring value discount, but additionally resulting from its doubtlessly stronger functionality to mechanically determine troubleshoot alternatives.

There may be additionally a transparent purpose why CSPs would think about RDCM’s choices as a platform of selection, for my part. RDCM stays as a frontrunner on this house, for my part, given its observe document of working with blue-chip CSPs all over the world. AT&T, Dish, and Rakuten are RDCM’s prospects at present, whereas Vodafone has not too long ago been added to the shopper base in FY 2023. Most not too long ago simply over the previous week, Rakuten extended its multi-year partnership deal with RDCM, which speaks quantity about RDCM’s aggressive positioning within the house.

Danger

Although enterprise threat could appear minimal, I see idiosyncratic dangers, such because the current administration shakeup, to stay as a threat issue buyers want to observe. Simply two months after RDCM introduced the appointment of Man Shemesh as CEO within the This autumn earnings name in January, Shemesh stepped down, citing “personal reasons”. Shortly after, RDCM noticed virtually a -10% pullback.

Although the exit motivation stays unclear and will not be made public, I imagine there could possibly be two potential threat elements that buyers want to bear in mind earlier than dipping in at present. First off, if any, an abrupt exit on the govt stage could doubtlessly point out dangerous tradition that would result in long-term underachievement. Secondly, the absence of a key management determine on the high may point out a interval of instability forward.

Valuation / Pricing

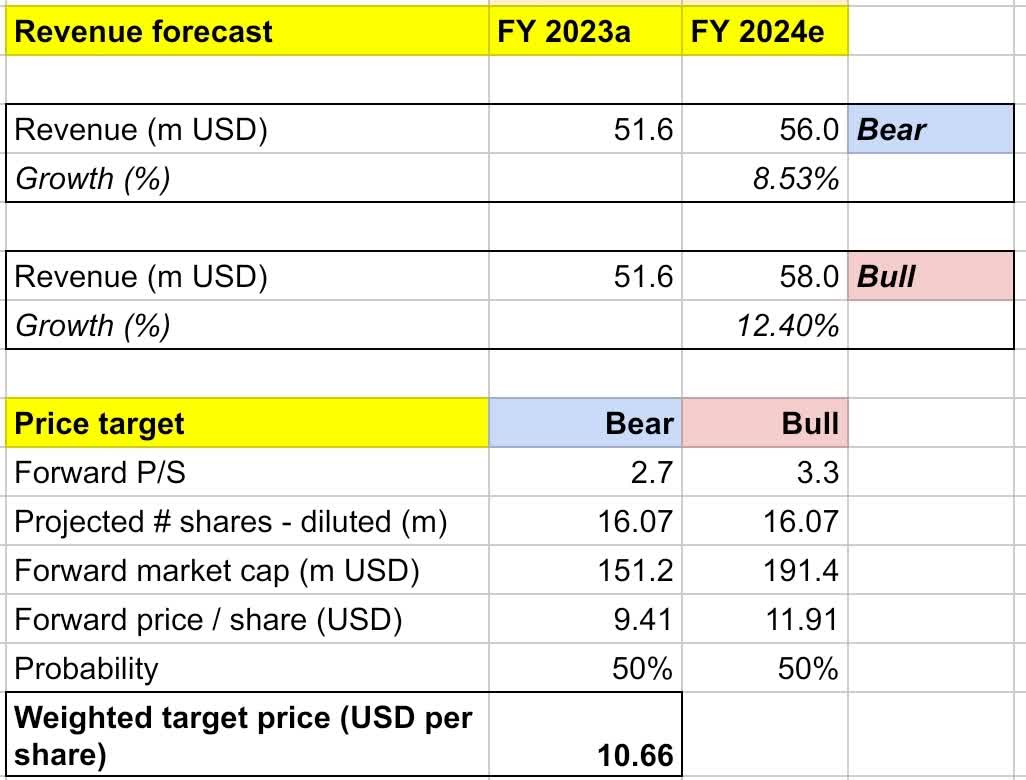

My goal value for RDCM is pushed by the next assumptions for the bull vs bear eventualities of the FY 2024 projection:

-

Bull situation (50% likelihood) assumptions – I anticipate RDCM to realize an FY 2024 income of $58 million, a 12.4% progress YoY, in line with the market’s estimate. I assume a ahead P/S to broaden to three.3x, implying a share value appreciation to $11.9. On this situation, I anticipate the market to worth RDCM increased because it makes significant progress within the subsequent few quarters, successfully demonstrating functionality to nonetheless ship outperformance even after the current administration shakeup.

-

Bear situation (50% likelihood) assumptions – RDCM to ship FY 2024 income of $56 million, an 8.5% YoY progress, lacking the market’s estimate barely. I assign RDCM a ahead P/S of two.7x, projecting a sideways value motion across the $9 vary, the place it has been because the 10% pullback in April.

personal evaluation

Consolidating all the knowledge above into my mannequin, I arrived at an FY 2024 weighted goal value of $10.7 per share, projecting an over 13% 1-year achieve from the present value of $9.45. I might fee the inventory a purchase. I imagine risk-reward stays fairly engaging at current. I might additionally disclose that I utilized a extra conservative strategy in my projection, assuming a 5% improve in share rely, a decrease bear-case estimate, and a 50-50 weighted likelihood regardless of seemingly engaging secular catalysts at current.

Conclusion

RDCM is a number one firm within the 5G community monitoring software program house. Its platform’s functionality to ship higher 5G service assurance seems to be confirmed by its blue chip CSP shopper base, which incorporates AT&T, Dish, and Rakuten. Furthermore, Rakuten’s current renewals additional validates RDCM’s strong aggressive positioning. The administration shakeup as of late has offered a little bit of a possible draw back threat, because it may result in a interval of instability. This has brought about a pullback, which additionally resulted in a shopping for alternative, for my part. At $9.45 at present, the value stays engaging. I set a 1-year goal value of $10.7, projecting over 13% upside. I fee the inventory a purchase.