patty_c

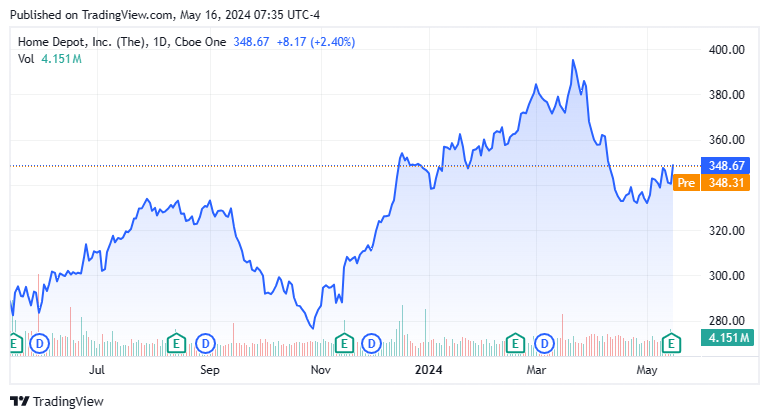

Giant retailer The Home Depot, Inc. (NYSE:HD) posted their Q1 results on Tuesday, May 14th. The stock managed to climb 2.4% in trading on Wednesday in what can be described as a relief rally, as the shares are still down more than 10% from recent highs. Time to buy the dip in the large retailer that has created so much shareholder value over the decades? Or are the shares too expensive even after the pullback? An analysis follows below.

Seeking Alpha

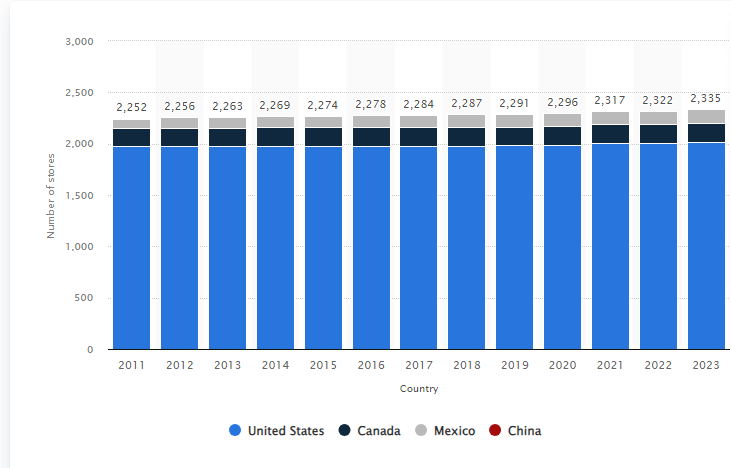

Home Depot needs no introduction. The Atlanta-headquartered retail giant dominates the home improvement category, as is a staple in any decent sized town across the nation. The company has nearly a $350 billion dollar market capitalization. Since its founding in 1978, the company has grown to just over 2,000 stores in the United States. Its closest competitor, Lowe’s Companies (LOW), has an approximate $135 billion market capitalization and approximately 1,750 stores. Home Depot also has a footprint in Mexico, Canada and China.

Home Depot Stores By Country (Statista )

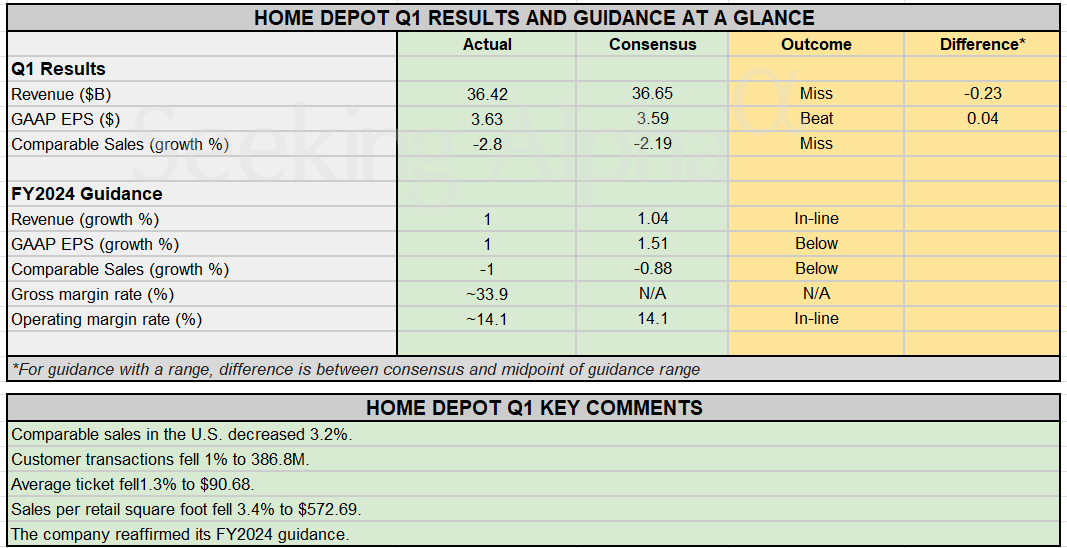

First Quarter Numbers:

The company delivered $3.63 a share of non-GAAP earnings in the first quarter. This was four cents a share above the consensus. Sales fell 2.4% on a year-over-year basis to $36.4 billion, $250 million light of expectations. Overall, same store sales fell 2.8% from the same period a year ago. This was worse than the consensus calling for a 2.2% same store sales decline. U.S. same store sales dropped 3.2%.

Seeking Alpha

Management expects revenue growth of just one percent overall in FY2024 and for same store sales to decline by one percent. It should be noted, there is an extra (53rd week) of sales in Home Depot’s FY2024. It expects to open a dozen new stores during the year. It is also important to note guidance does not include the company’s recent over $18 billion purchase of SRS Distribution at the end of March.

The acquisition was made to expand Home Depot’s offerings and reach to home professionals and contractors. An article on Seeking Alpha right after that purchase went into the purchase cost and the new opportunities this acquisition will provide Home Depot.

Management also noted there was a weather-impacted delayed start to the spring selling season and consumers are increasing reluctant or delaying making purchase of big-ticket items.

Analyst Reaction & Balance Sheet:

Analyst firm reaction was immediate and mixed on Home Depot’s earnings report. 13 analyst firms, including Piper Sandler, UBS and Barclays, have assigned/maintained Buy/Outperform ratings on the stock since quarterly earnings hit the wire. Price targets proffered range from $372 to $425 a share. Eight analyst firms, including RBC Capital and HSBC, have reissued Hold/Sell ratings on the stock, with price targets between $300 and $377 a share.

There has been no insider buying during the recent dip in the stock. The only insider activity in HD so far this year happened in late February, when several insiders sold approximately $45 million worth of shares collectively. With the purchase of SRS Distribution, the company suspended its stock buyback program. Management expects interest costs on its debt to come at $1.8 billion in FY2024.

The company hasn’t filed its 10-Q for the first quarter, but its 10-K filed for FY2023 showed just under $4 billion in cash and marketable securities against just over $42 billion in long-term debt.

Conclusion:

Home Depot made $15.11 a share in FY2023 on just over $153 billion in revenue. The current analyst firm consensus has earnings creeping up slightly to $15.30 a share on $154 billion in sales. They project FY2025 profits of $16.31 a share on three percent sales growth.

This leaves the shares trading at just under 23 times forward earnings and 2.25 times forward sales. The shares pay a dividend yield of a bit over 2.6%. The company should experience little growth in FY2024 and FY2025, and the housing market is likely to a headwind until mortgage rates fall significantly. (2023 had the lowest level of existing homes sales since 1995.) In way of comparison, LOW trades at just over 19 times forward earnings and 1.55 times forward sales. The stock also pays a 1.86% dividend yield.

Perhaps in a ZIRP environment, one could justify paying those sorts of valuation multiples given Home Depot’s track record. It is hard to ever say Sell on a stock like HD that has rewarded shareholders so richly over the decades. However, with growth prospect tepid, the Fed Funds rate at over five percent and a challenging housing environment, The Home Depot, Inc. stock seems to be a solid Avoid at current trading levels.