ijeab/iStock through Getty Photographs

In November 2023 I wrote my last article about Reckitt Benckiser (OTCPK:RBGPF) and I said my optimism for the long term. And whereas we are able to definitely argue that 4 to 5 months isn’t actually “the long run”, the inventory carried out horrible since my final article.

In the previous few weeks, two main information tales appeared to have a giant affect on the corporate and likewise on the inventory worth – the reported annual outcomes for fiscal 2023 and the litigations concerning the toddler formulation of Mead Johnson (a subsidiary of Reckitt Benckiser). I’ll present an replace within the following article and assess if Reckitt Benckiser remains to be a superb long-term funding regardless of the latest developments. A minimum of the inventory is now 20% cheaper than at first of November 2023.

Annual Outcomes

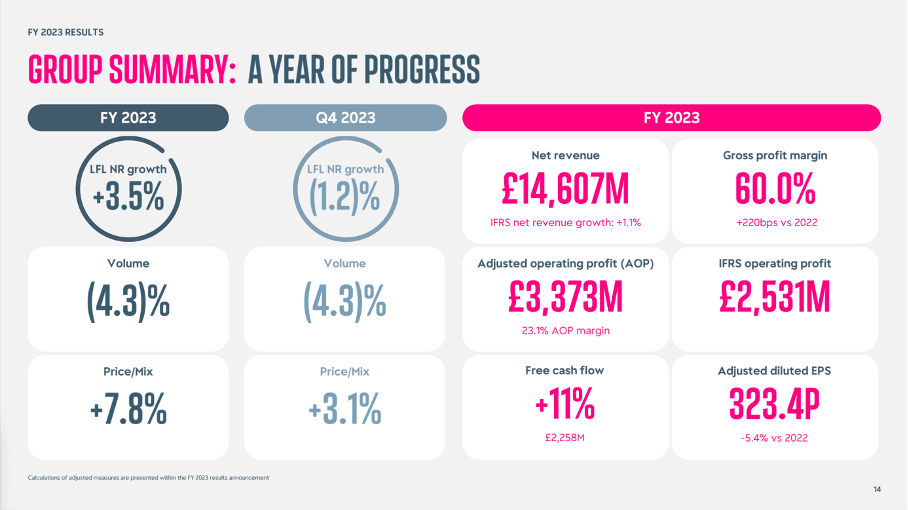

We begin by wanting on the final annual outcomes, which had been reported on the finish of February. And though the outcomes weren’t an entire disappointment, they weren’t nice both. Income elevated barely from GBP 14,453 million in fiscal 2022 to GBP 14,607 million in fiscal 2023 – leading to 1.1% year-over-year progress. And whereas it is a quite low progress fee, like-for-like progress was 3.5% for fiscal 2023 with quantity declining 4.3% and worth/combine growing 7.8%.

Reckitt Benckiser This autumn/23 Presentation

Nonetheless, working revenue declined 22.1% year-over-year from GBP 3,249 million in fiscal 2022 to GBP 2,531 million in fiscal 2023. And eventually, diluted earnings per share declined from 324.7 pence within the earlier 12 months to 228.7 pence in fiscal 2023 – leading to 29.6% year-over-year decline.

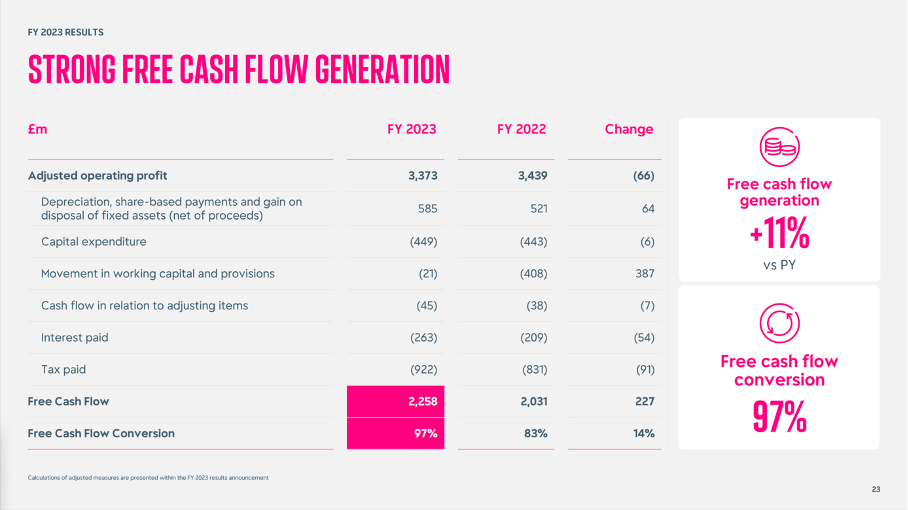

Whereas working revenue and earnings per share declined, free money circulate elevated from GBP 2,031 million within the earlier 12 months to GBP 2,258 million in fiscal 2023 – leading to 11.2% progress. And as free money circulate is likely one of the most vital metrics for any enterprise that is really excellent news for the enterprise. Free money circulate particularly elevated as a consequence of the next conversion fee – as a substitute of 83% in fiscal 2023 it was 97% in fiscal 2023.

Reckitt Benckiser This autumn/23 Presentation

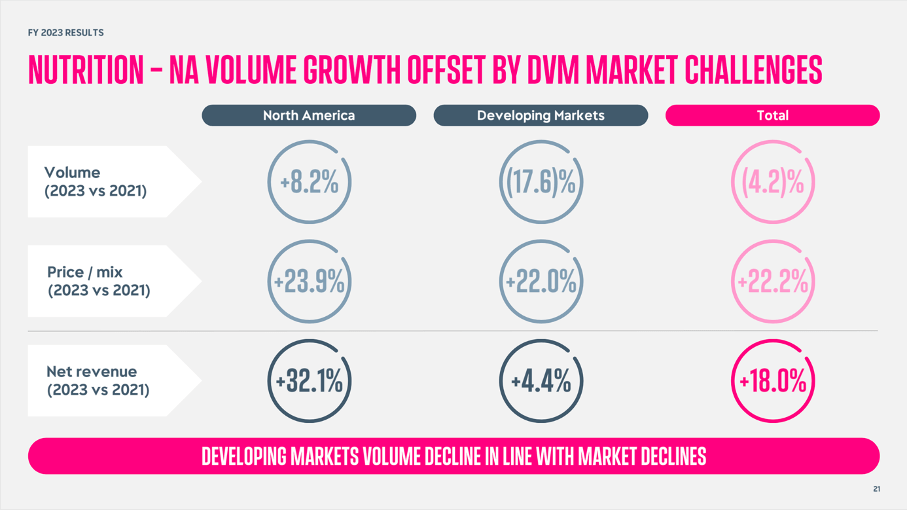

We will additionally have a look at the three totally different segments. The issue little one stays to be Vitamin – a minimum of when taking a look at year-over-year progress charges. However for the diet phase we nonetheless have to bear in mind the availability problem in 2022, which was an enormous tailwind for Reckitt Benckiser. During the earnings call, administration commented:

In Vitamin, we see a mixture of the rebasing in U.S. and North American volumes following the competitor provide problem in 2022 and a few market quantity weak spot in creating markets and I’m going to enter that in somewhat bit extra element in a number of extra charts.

For the complete 12 months of fiscal 2023, Vitamin generated GBP 2,410 million in income – a like-for-like decline of 4.0% for the complete 12 months. However when evaluating the fiscal 2023 outcome to fiscal 2021, we see 18.0% quantity progress – a stable progress fee and financial 2022 have to be seen as optimistic outlier. We additionally should level out that North America is performing nice – when evaluating to fiscal 2021 – whereas the rising markets are struggling.

Reckitt Benckiser This autumn/23 Presentation

The opposite two segments nonetheless may report low-to-mid single digit progress charges. And a minimum of when taking a look at income, these two segments are an important for Reckitt Benckiser with every phase being accountable for greater than 40% of complete income. Hygiene generated GBP 6,135 million in gross sales in fiscal 2023 and reported 5.1% like-for-like progress and Well being grew 5.0% like-for-like and generated GBP 6,032 million in income.

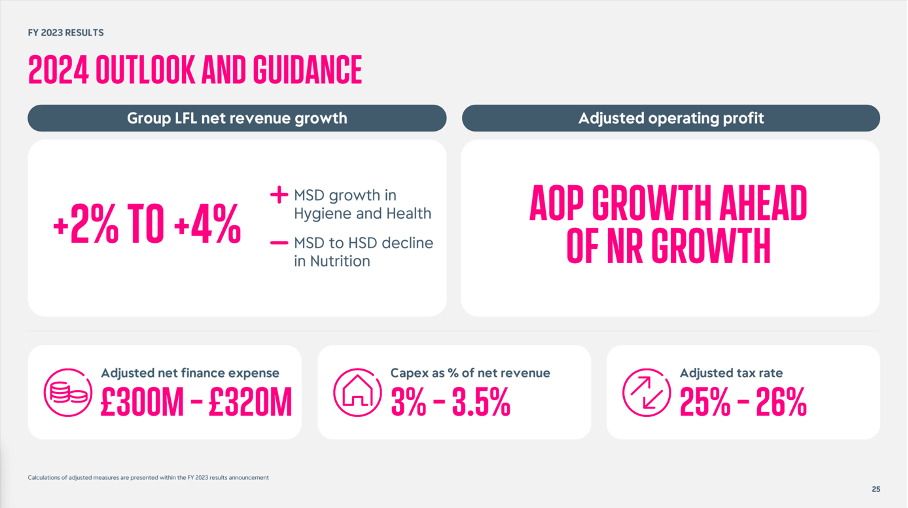

And the outlook for fiscal 2024 is just like fiscal 2023 – not nice but additionally not an enormous disappointment. Income is anticipated to develop between 2% and 4% on a like-for-like foundation. And whereas Well being and Hygiene are anticipated to develop within the mid-single digits, the Vitamin enterprise is anticipated to say no within the mid-single digits as soon as once more. Nonetheless, adjusted working revenue is anticipated to develop with the next tempo than income.

Reckitt Benckiser This autumn/23 Presentation

Outcomes and outlook weren’t good, nevertheless it was sufficient to tank the inventory within the double digits. And the second main drop got here in mid-March after information concerning the Mead Johnson litigations had been introduced.

Mead Johnson Litigation

Following earnings, the inventory declined greater than 13% and mid-March the inventory was despatched down one other 14.6%. This time the explanation weren’t quarterly or annual outcomes, however information about an Illinois jury having ordered Mead Johnson – a subsidiary of Reckitt Benckiser – to pay $60 million to the mom of a untimely child who died after being fed the Enfamil child formulation produced by Mead Johnson.

And for my part, it’s a big downside that Reckitt Benckiser can tell buyers that many instances had been filed towards the corporate, however administration isn’t in a position at this level to state a exact variety of instances associated to the protection and advertising of the Enfamil child formulation.

It looks like over 400 instances had been filed with the Chicago federal court docket, however there may additionally be instances concerned that had been filed towards Abbott Laboratories (ABT) – the opposite main producer of child formulation for untimely infants, which can also be based mostly within the Chicago space. And never surprisingly, Reckitt Benckiser is strongly disagreeing with this verdict and can attempt to struggle it. Administration can also be anticipating that a few of the further filed instances might be dismissed in a preliminary stage. Nonetheless, it takes just a few instances with an identical verdict (to pay $60 billion) to generate an enormous monetary harm to the corporate.

The inventory market is definitely not all the time rational, however as response to the information the market capitalization of Reckitt Benckiser dropped greater than $6 billion hinting that buyers are fearing an enormous harm for the enterprise.

At this level, corporations like Bayer (OTCPK:BAYZF) or 3M Company (MMM) come to thoughts. Each are cautionary examples for companies actually struggling as a consequence of authorized issues and in each instances the shares continued to say no additional and additional and there may be nonetheless no finish in sight. If that is the trail Reckitt Benckiser goes down, it most likely can be greatest to get out of the inventory proper now.

Technical Image

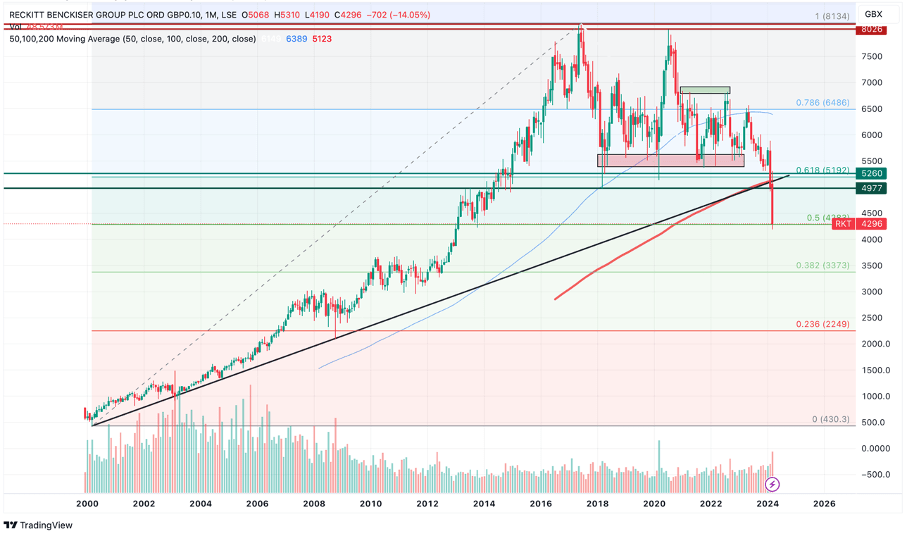

And it looks like Reckitt Benckiser is going through one other downside – its personal chart. Following the annual outcomes and the litigation information, the inventory declined to a 11-year low. And within the means of declining throughout the previous few weeks, the inventory broke by means of a number of sturdy help ranges – most likely explaining why the inventory is declining so steep. For starters, the inventory broke by means of a number of lows from the years 2018 until 2023, which had been a robust help degree till lately. Moreover, the inventory broke by means of a long-time trendline that has been in place since 2000 and it additionally broke by means of the 200-month transferring common.

Reckitt Benckiser: Month-to-month Chart (Creator’s work created with TradingView)

At this level, after breaking by means of a number of help ranges, it doesn’t look good, and we definitely should take note of the chance of even decrease inventory costs. The one glimmer of hope proper now could be the truth that we’re buying and selling on the October 2013 low (however this isn’t actually sturdy help degree). Other than this low, we’re presently on the 50% Fibonacci retracement when connecting the low immediately following the IPO and the highs of 2017 and that may very well be a stronger help degree.

However at this level I might not wager on Reckitt Benckiser already having discovered its backside and the chance of additional declining inventory costs appears to be excessive at this level.

Intrinsic Worth Calculation

However whereas the chart isn’t actually a supporting issue for Reckitt Benckiser proper now, we are able to argue that the inventory appears to be actually low cost at this level. When utilizing the free money circulate of fiscal 2023 (GBP 2,258 million) and a ten% low cost fee in addition to 718.5 million excellent shares, the corporate has to develop barely beneath 3% yearly with the intention to be pretty valued.

At this level, I might argue that Reckitt Benckiser ought to have the ability to develop about 3% yearly until perpetuity. A minimum of for fiscal 2024, administration is anticipating progress charges for working revenue that may exceed 3% progress. Therefore, we are able to make the case that Reckitt Benckiser is a minimum of pretty valued proper now. And in principle I might assume Reckitt Benckiser having the ability to develop with the next tempo, however contemplating the outcomes, the outlook and the lawsuits it is perhaps higher to remain on the aspect of warning.

Conclusion

I stay assured that Reckitt Benckiser is an efficient funding over the long run. Nonetheless, there are two points we must always not ignore – the technical image on the one aspect and the litigations on the opposite aspect. Particularly the lawsuits are an enormous threat that may be very troublesome to evaluate.

To mirror my warning at this level, I’ll downgrade the inventory to a “Hold” – and that’s what I’ll do with my very own shares: I’ll maintain on to them as I nonetheless consider over the long term Reckitt Benckiser might be a stable funding however I might not buy any further shares at this level.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.