RobertHoetink/iStock Editorial by way of Getty Pictures

Related British Meals plc (OTCPK:ASBFY) is a enterprise that’s onerous to grasp by most traders. Not as a result of the corporate operates in quite a few completely different sectors, however reasonably due to the best way it’s managed.

When listening to ASBFY’s administration convention calls a growth-oriented investor within the fairness market might typically be perplexed by the selections made on the firm. From protecting massive money piles at hand to suspending sure funding alternatives for the sake of retaining a excessive return on invested capital.

This technique is in the end aimed toward serving long-term shareholders and never succumbing to stress from short-term oriented market individuals. The disadvantage right here is that ASBFY might find yourself underperforming the market over lengthy intervals of time when the corporate is laying the inspiration for its subsequent development stage.

In recent times we’ve got additionally seen quite a few important headwinds for the corporate within the type of Brexit, and pandemic lockdowns – which resulted within the non permanent closure of all Primark shops.

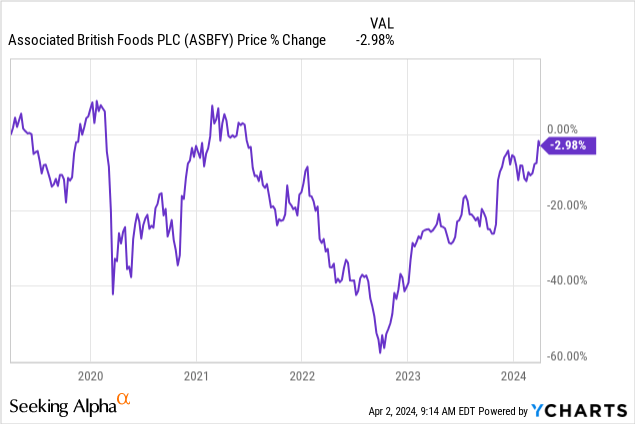

These developments created important headwinds for ASBFY lately, simply as administration has turn out to be extra cautious within the enlargement of Primark in america. Thus, it isn’t shocking that the inventory value efficiency has been, to say the least – disappointing over the previous 5-year interval.

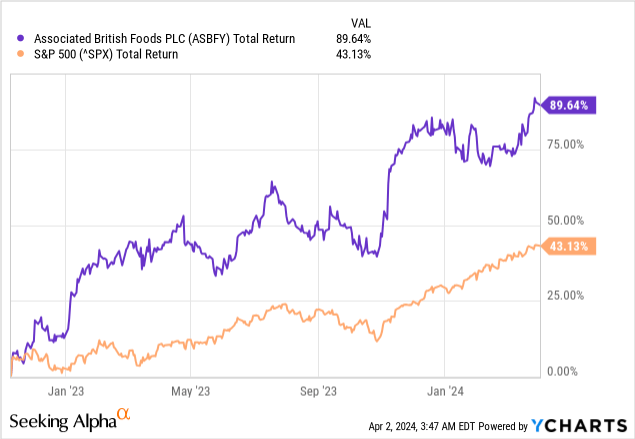

Nevertheless, I’ve been making the most of the current lows by including extra shares into my private portfolio and have additionally rated the inventory as a high-conviction purchase for my subscribers in November of 2022. At that cut-off date, ASBFY had reached unsustainably low ranges and the extraordinarily low inventory value justified the excessive conviction score. ASBFY’s whole return since then is plotted on the graph beneath, which speaks for itself.

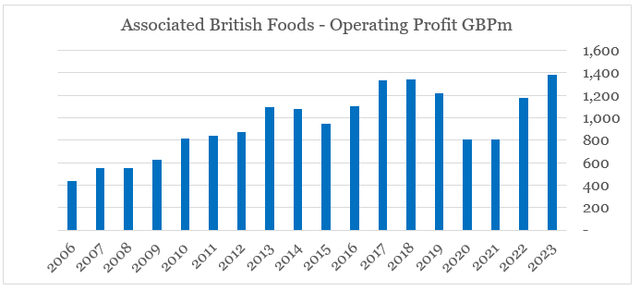

Along with the aforementioned headwinds now being behind us, Related British Meals is gearing for a interval of upper high line development in areas the place the enterprise is incomes excessive returns on capital employed. In consequence, the corporate’s working revenue is already above its pre-pandemic ranges, and as administration steps up, its reinvestments into enterprise this upward trajectory is prone to proceed.

ready by the writer, utilizing knowledge from annual stories

Bettering Fundamentals

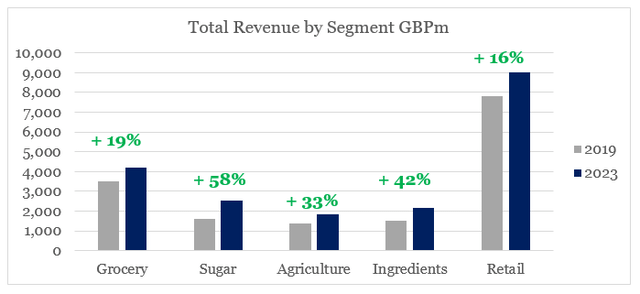

Despite its stellar efficiency since November of 2022, Related British Meals inventory nonetheless trades beneath its pre-pandemic ranges. On the similar time, nonetheless, income has grown considerably in every of the corporate’s 5 enterprise segments proven within the graph beneath.

ready by the writer, utilizing knowledge from annual stories

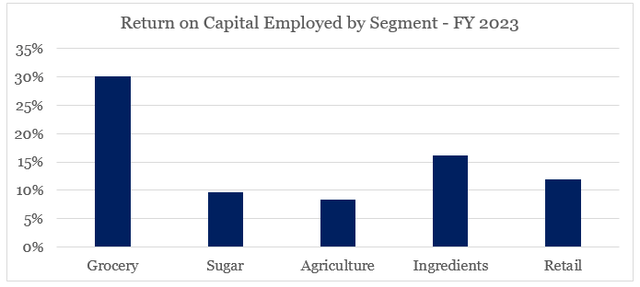

In Grocery, Elements and Retail the corporate achieves a return on capital employed in extra of 10% with the Grocery enterprise unit now having a ROCE of 30%.

ready by the writer, utilizing knowledge from investor displays

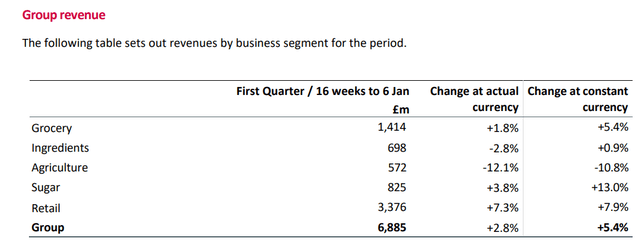

High line development within the two most essential segments remained elevated throughout the first quarter of the present fiscal 12 months, with income in Grocery rising at 5.4% in fixed forex and gross sales of Primark rising by 7.9%.

Related British Meals Buying and selling Replace

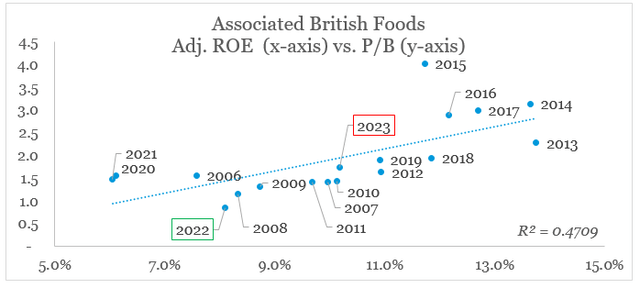

As development in excessive ROCE segments stays elevated, Related British Meals stays well-positioned to additional enhance its return on capital. Based mostly on the sturdy relationship between the inventory’s Worth/Guide a number of and its adjusted Return on Fairness, this might result in an upward a number of repricing within the coming years on high of the excessive income development.

ready by the writer, utilizing knowledge from annual stories and In search of Alpha

Proper now ASBFY trades in keeping with its ROE based mostly on the connection we see on the graph above, which signifies that the market doesn’t anticipate any additional enhancements within the firm’s return on capital. A situation that for my part is simply too conservative given the funding alternatives forward.

Investing The place It Issues

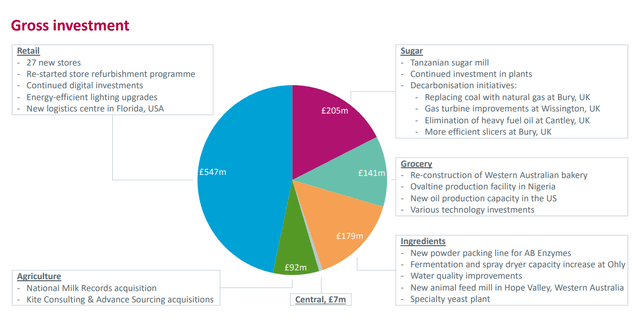

In FY 2023, ASBFY spent practically £1bn on capital expenditure which was a significant improve from the £680m spend in FY 2022. That is additionally 113% from the annual depreciation and amortization expense which signifies that the corporate is as soon as once more in development mode.

Almost half of that quantity is spent on the Primark enterprise, which is now in its early levels of increasing into america. The Sugar and Elements divisions additionally take a large chunk of ASBFY’s annual gross funding funds.

Related British Meals Investor Presentation

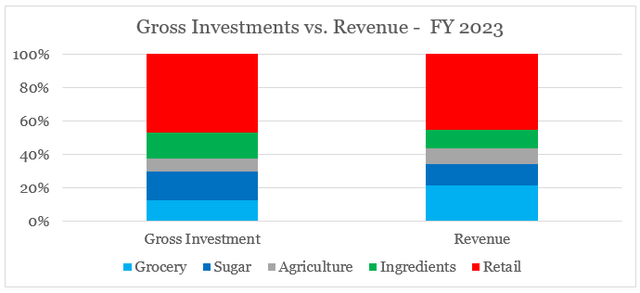

After we examine these numbers to the precise income derived from every of the 5 divisions, we are able to see that the Sugar and Ingredient divisions have been allotted a bigger share of the gross funding funds to their respective shares from the corporate’s whole gross sales.

ready by the writer, utilizing knowledge from annual stories

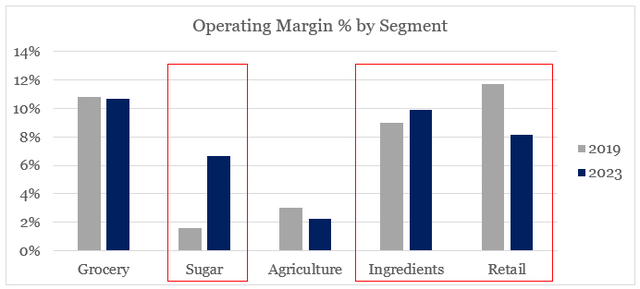

Each Sugar and Elements have skilled a notable enchancment in margins to their pre-pandemic ranges, whereas Retail – the most important division by the entire quantity spent on Capex remains to be struggling to return to its FY 2019 ranges.

ready by the writer, utilizing knowledge from annual stories

The current inflationary pressures and the sturdy U.S. greenback have been main headwinds for Retail’s margins as Primark competes on price and most of its suppliers are invoicing the corporate in {dollars}.

Though these pressures are prone to persist in calendar 2024, the excessive anticipated income development from the ongoing expansion within the U.S. market could be the important thing driver for shareholder returns.

Related British Meals Investor Presentation

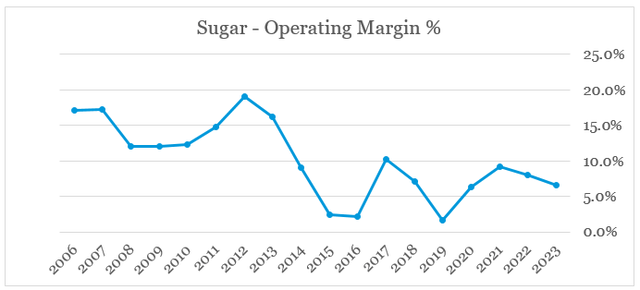

Sugar, alternatively, is the place ASBFY now faces a serious margin alternative as sugar costs skyrocketed lately.

FRED

The upper promoting costs, nonetheless, didn’t result in margin enhancements in 2023 as unhealthy climate and better vitality prices have been an offset to gross sales enhancements.

ready by the writer, utilizing knowledge from annual stories

Wanting forward, ASBFY’s sugar division is in a very good place to report greater margins in FY 2024 as promoting costs stay excessive and the co-product electrical energy offsets greater vitality prices.

Turning to sugar operations; we have seen, I believe, two offsets that give us confidence within the stability of our sugar companies. Sure, the crop was down, however costs have been greater. Sure, vitality — fuel costs have been greater within the UK, however the co-product electrical energy nearly offset all the additional fuel costs we have been seeing. So net-net throughout British sugar within the 12 months that regarded prefer it might have been calamitous.

Supply: Related British Meals This fall 2023 Earnings Transcript.

Conclusion

Related British Meals’ inventory delivered excellent returns over the previous 12 months or in order the enterprise recovers from the pandemic lockdowns and the upper inflationary pressures. Future returns are prone to cool off a bit because the a number of repricing alternative just isn’t as engaging because it was again in November of 2022. Nonetheless, elevated income development and future margin enhancements in sure divisions don’t seem like priced in in the meanwhile, which is prone to drive above-market returns for Related British Meals plc inventory within the coming years.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. alternate. Please concentrate on the dangers related to these shares.