passion4nature/iStock Editorial by way of Getty Photos

Revolutionary Options and Assist Inc. (NASDAQ:ISSC) is a enterprise title that evokes no hype, no creativeness, and no aptitude. The obscure, generic title sounds just like the boilerplate tag line utilized by a advertising and marketing staff belonging to any firm. ISSC actually has a boring title; and the enterprise itself – producer and provider for avionics – is simply as boring. To me – it is superb. Within the phrases of Peter Lynch:

An organization that does boring issues is sort of pretty much as good as an organization that has a boring title, and each collectively is terrific. – Peter Lynch.

Throw in the truth that there are apparently no Wall St. analysts masking the corporate, and never even a Quant Score by In search of Alpha, and it is simple to see how ISSC flies below the radar in obscurity. Nonetheless, below the snoozefest is a enterprise that’s quickly rising with a refreshed administration staff and prudent capital allocation aligned with a realistic worthwhile progress runway. Rising gross sales and earnings 79% and 40%, respectively, within the final quarter is something however boring – neither is rising gross sales at 20% CAGR over 5 years and working earnings 300% since 2018.

I imagine the enjoyable meter with ISSC is simply beginning to flip to eleven and count on shares to hit the ~$20 mark as soon as their manufacturing facility is totally utilized, maybe as early as FY27.

Some Historical past . . . and Why this Alternative Exists

Founder Geoffrey Hendrick Years

I imagine that an funding in any small firm requires a cautious consideration of the tradition, integrity, and keenness of the corporate and its operators. Often, a big firm can survive a awful administration staff – generally for lengthy intervals of time – however that may very well be the loss of life knell for a small firm. With that stated, some historical past for ISSC is warranted to understand its tradition, but in addition, to know why this chance now exists.

ISSC has been a public firm since 2000 – and based in 1988. Founder Geoffrey Hedrick was an esteemed engineer and grew the corporate from nothing on the backs of dozens of patents which have made their manner into industrial plane. It is no marvel that half of the corporate’s title “Innovative Solutions” displays this quantity of inventiveness. It is the second half of the corporate’s title – “Support” – that has allowed small ISSC to determine robust relationships with their clients and develop them through the years.

“Provide innovative solutions to technical problems,” he stated. Then he added: “You’ve got to provide support, and I said, ‘Damn it, we’ll put that in the name of the company, too.'” – Geoffrey Hedrick

The give attention to “support” could seem to be an simply neglected facet for any firm, however within the context of aviation, it means all the pieces. Tragedies each within the commercial world, such because the Boeing 737 Max plane, and military world, such because the V-22 Osprey, are fixed reminders of the necessity for the very best ranges of security on each element and widget that make up an plane.

ISSC’s excessive dedication to security and assist materialized into tangible outcomes for traders when the FAA mandated that aircraft reduce vertical separation altitude from 2000-ft to 1000-ft within the early 2000s. Regardless of competing towards a lot, a lot bigger firms reminiscent of Honeywell (HON), Garmin (GRMN), and Collins Aerospace (RTX), ISSC’s resolution captured the vast majority of market share of retrofitting world enterprise plane and generated $100 million in money, a lot of which has been reinvested into the enterprise to develop its product portfolio and manufacturing facility capability.

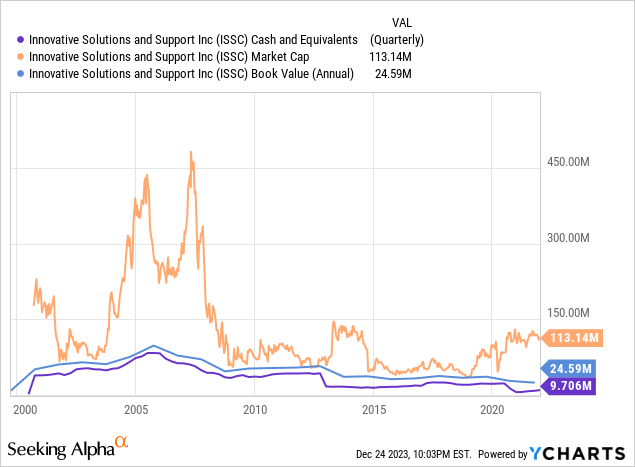

It might be a disservice to state that ISSC is solely under-covered, under-analyzed, and basically unknown to the market, and chalk up alternatives that come up to that truth alone. I don’t imagine within the environment friendly market speculation, not less than, not for small-cap firms, and there’s a plethora of case-studies to that time. That stated, regardless of his brilliance as an engineer and his dedication to clients, Mr. Hedrick was maybe not the best capital allocator. He had created a gentle firm by 2010, and my conjecture is that he was content material with the expansion the corporate had achieved. I arrive at this postulation as a result of significant special dividends the corporate paid out in 2008 ($16 million), 2013 ($25 million), and 2021 ($20 million). That is maybe additionally attributable to Mr. Hedrick’s conservative nature, as the corporate has held a considerable amount of money (normally between $30 million and $50 million) for a corporation with a historic market cap between $60 million and $100 million. After all, he was additionally a big shareholder at 20% of the float. Throughout his tenure, ISSC took on no debt.

Present Alternative Beneath the Askarpour Years

Quick ahead to current occasions, Mr. Hedrick died in 2022, and his successor is Dr. Shahram Askarpour, who has been with the corporate since 2003 in varied roles. Like Mr. Hedrick, Dr. Askarpour is deeply engrained within the engineering surrounding the aviation trade, and I might think about has been closely influenced by the mentorship of Mr. Hedrick. Dr. Askarpour continues to emphasize to traders throughout earnings calls and convention shows that security and dedication to clients are his priorities.

The place now-CEO Askarpour differs from the late Mr. Hedrick is in capital allocation and a reinvigorated imaginative and prescient for (worthwhile) progress. That is the important thing distinction for why ISSC has develop into investable. CEO Askarpour has introduced to traders a multi-faceted progress technique fueled by each natural technological developments, primarily based on a deep understanding of the route the aviation trade is heading, and inorganic value-accretive M&A.

Inorganic Progress

On the inorganic facet, it took ISSC almost two years to seek out an acquisition that was inexpensive and will slot in properly with the present manufacturing facility that the corporate owns. Throughout this time, ISSC was sitting on a considerable money pile. I take this as affected person self-discipline as a result of the eventual Honeywell acquisition for $36 million in Q3 2023 has – up to now – executed precisely what Shahram wished: purchase merchandise with comparable ISSC gross margins of 60%+ at an affordable a number of that complement and increase the present ISSC choices, whereas being value-accretive. It is uncommon to seek out profitable M&A that does not destroy shareholder worth, however up to now, after one full quarter of buying the Honeywell merchandise, integration is on tempo, Y/Y gross sales elevated 79%, and Y/Y internet earnings elevated 63%.

ISSC took on $20 million of debt to fund this acquisition – which might be unparalleled below Hedrick’s tenure. With present LTM EBITDA of $7.7 million, ISSC sits at a internet debt to EBITDA leverage ratio of two.2x. Nonetheless, the corporate is able to gushing out free money circulate. To that time, Shahram informed traders in December 2023 that the corporate paid down a big chunk of debt from accounts receivable changing to money and refinanced the time period mortgage right into a revolver with their financial institution amounting to $12 million.

We’re lucky to have an ideal relationship with our financial institution PNC, they usually have been very supportive of our progress technique. This week, we transformed our $20 million time period mortgage to a revolving line of credit score that has enabled us to scale back our complete debt from $20 million to lower than $12 million. – CEO Shahram Askarpour, Q4 FY23 Earnings Call.

All of this occurred in lower than half a yr, and now the leverage ratio is at 1.6x. The good information is that even after the Honeywell merchandise are totally built-in, ISSC expects their Exton, PA manufacturing facility to nonetheless solely be 50% capability utilized, and Sharam has indicated inorganic progress stays a key a part of the expansion technique.

As a reminder, we’re concentrating on smaller bolt-on acquisitions which might be round $25 million and proceed to be actively engaged in evaluating potential acquisitions. There’s nonetheless one other 50% extra capability to be leveraged as we anticipate producing extra cash from the elevated revenues mixed with further borrowing capability. We may have greater than enough assets to proceed to implement our technique. – Q3 FY23 Earnings Call

Which means that the corporate doesn’t should spend money on capex to increase manufacturing capability to proceed rising – and in the event that they attain the purpose the place they do, then the corporate is prone to be in a really robust place. Contemplating the power for ISSC to spit out money to shortly pay down debt and get again on the M&A practice, in addition to the current profitable execution and acquisition of the Honeywell merchandise, I’m optimistic in regards to the continued prospects of M&A.

If this is not a transparent signal that ISSC is now not the stodgy enterprise of the earlier period, then I am unsure what’s.

As an apart, one would possibly marvel why Honeywell would promote these merchandise within the first place (i.e., did ISSC get the brief finish of the stick?). Honeywell is creating subsequent era avionics, and these merchandise are now not core to their enterprise. That stated, there’s substantial worth in earlier era merchandise – simply ask Dassault Aviation (OTCPK:DUAVF), who’ve been promoting their Rafale jet fighters like hotcakes, or Textron’s (TXT) RQ-7B Shadow drone which has been the Military UAV mainstay since 2002. Remember the fact that Honeywell is a large conglomerate that prints ~$5 billion in free money circulate prefer it’s nothing. The Honeywell merchandise generated $9.5 million in internet earnings in FY22, so ISSC was in a position to purchase these merchandise for 3.75x earnings a number of! This acquisition is a rounding error for Honeywell (however transformative for ISSC), and it’s my suspicion that Honeywell was far more involved with making certain a powerful match and good dwelling for his or her earlier era than the most effective provide on the desk. In any case, Honeywell’s repute and relationships with clients are on the road in an trade the place, I remind you, security is (and must be) second-to-none. I imagine that is the place ISSC’s spotless repute gave it a bonus.

Natural Progress: Autonomous Flight Options

Earlier than you roll your eyes, this isn’t a promise of pie-in-the-sky AI-powered flight or industrial plane drones (as a lot because the airliners would love that). I encourage potential traders to take heed to Shahram converse on the November ISSC investor conference to get a extra full image of ISSC’s plans to understand autonomous flight.

Briefly, ISSC plans to organically develop and produce avionics that assist lowering pilot workload, steadily arriving on the level the place just one pilot could should be in-flight, with one other on the bottom (generally known as fly-by-wire).

When you have by no means been in a cockpit of an plane, there’s an absurd quantity of knowledge to watch and contemplate – most introduced with outdated shows – that instructions fixed diligence by the pilot(s). ISSC already has in-house developed merchandise reminiscent of their ThrustSense Autothrottle system and Utility Management System which carry out some autonomous capabilities pertaining to plane actuator management and monitoring, lowering pilot cognitive load. These are at the moment produced for his or her contracts with key plane by OEMs Boeing (BA) and Textron (TXT).

ISSC administration is planning for the fly-by-wire part to start out turning into a part of the dialog with airliners within the 2027-2030 timeframe. Afterward, within the 2030+ timeframe, the expectation is that demand by airliners will result in additional merchandise and growth towards full autonomous flight computer systems with pilots on the bottom. After all, this will probably be hotly contested by the pilot union – however could be extra a query of when than if. The pilot shortages of 2022-2023 (and actually, it is nonetheless ongoing) are a transparent signal of the upcoming demand by airliners for such options.

The funding thesis for ISSC doesn’t depend upon any of this turning into actuality, however the incremental positive aspects that ISSC is particularly and purposefully concentrating on ought to make in-roads for this buyer demand and improve top-line gross sales. I count on cargo plane owned by logistic firms to be the avant-garde in adopting this know-how. Market research suggests autonomous options are a multi-billion-dollar enterprise, at the moment valued at ~$9 billion in 2023 and anticipated to develop almost 20% CAGR into the following decade. There are main gamers on this house, together with Textron and BAE Programs (OTCPK:BAESY), however ISSC would not want a lot of a slice to see outsized affect to their enterprise. And moreover, ISSC has a historical past of punching far above their weight.

Valuation

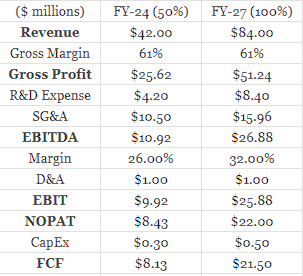

I current two valuations, one the place ISSC hits 50% capability utilization after full integration of the Honeywell merchandise, and one the place ISSC reaches 100% capability utilization.

ISSC guided for the Honeywell merchandise in FY24 to result in 40% income progress and 75% EBITDA progress – primarily based on the most recent earnings name, that is on observe. This suggests revenues of ~$42 million for 50% of manufacturing facility capability, which is 40% from revenues at time of acquisition of ~$30 million. Administration has divulged that they’ve important working leverage of their autonomous manufacturing facility, such that $50 million in gross sales would drop to the bottom-line with round 30% EBITDA margins. R&D can also be a serious a part of the corporate tradition, usually round 13% income. Nonetheless, given the fast progress of income, administration acknowledged R&D as a share of income will not preserve tempo, and supplied 10% because the goal.

For my FY24 estimate of fifty% utilization, I assume revenues of $42 million, gross margins according to historic efficiency of 61% (and post-acquisition), and EBITDA margins of 26%, R&D of 10%, and CapEx of $0.3 million (according to historic charges).

For my FY27 estimate of 100% utilization, I assume a linear relationship to income progress, gross margins of 61%, EBITDA margins of 32% (which is conservative contemplating that ISSC is already working effectively above their mounted prices and 30% margins are anticipated to be achieved at solely 50% capability), and CapEx of $0.5 million. Given administration’s current actions to maintain leverage below management, I count on the overwhelming majority of working money circulate to in the end circulate to fairness by FY27.

Writer Projections

ISSC has traditionally traded round 15x – 20x FCF. Utilizing a variety of 12x – 20x offers $5.59 – $9.32 for FY24E.

The mixing for Honeywell’s merchandise is predicted to finish FY24 and all messaging from administration indicators getting proper again to M&A. I count on this expertise will assist to combine the following acquisition much more easily. Utilizing the identical FCF a number of vary brings the value vary to $14.79 – $24.64, with a 15x a number of touchdown at $18.48. This might suggest an EV/EBITDA a number of round 12x, which is much decrease than friends Honeywell, Garmin (GRMN), and Howmet Aerospace (HWM) who all commerce at 15x+ EBITDA multiples and expertise decrease progress and with worse steadiness sheets.

ISSC can also be sufficiently small to be acquired by any of the large producers as a easy bolt-on. For priority, the a lot bigger Collins Aerospace was acquired by UTC (now Raytheon (RTX)) at ~16x EBITDA in 2017.

Dangers

As with most small-caps, buying and selling quantity is commonly a problem, and that’s positively true for ISSC as effectively. In actual fact, it has been such a problem for giant traders to enter the inventory that when an anchor investor purchased in 2022, the inventory value rocketed from the $6 space to over $9. ISSC has accepted an at-the-money share providing, and Shahram defined that is to handle the liquidity difficulty for the following big-monied investor who desires to purchase in to the corporate. Due to this fact, don’t count on to have the ability to soar out and in of this inventory with important sums of money.

The second danger to ISSC is M&A execution danger. That is at all times a danger for any firm that considers M&A a key a part of their technique, and the most effective we as traders can do is study the administration staff and any previous M&A offers. To this point, ISSC administration has a very good observe report right here, however it’s nonetheless admittedly early days; the corporate has one other 50% of manufacturing facility capability to replenish. A much bigger danger could merely be that administration has a tough time discovering one other acquisition that is smart and is inexpensive and worth accretive. It took administration over a yr to land on the Honeywell merchandise, and whereas avoiding horrible acquisitions is clearly a very good factor, it does extend the expansion story if acquisitions are laborious to come back by.

Cyclicality of the aviation trade is a average danger, however ISSC has a considerable aftermarket enterprise at 40% of gross sales, in addition to long-term (decade-long) OEM manufacturing contracts with Boeing and Textron at 20% gross sales. The aviation trade is within the midst of worldwide manufacturing booms, however ISSC administration is prudently deleveraging whereas fueling its progress – avoiding the everyday growth craze mentalities – which mitigates liquidity points throughout a downcycle. Administration additionally cited rising its army presence, enabled by each the Honeywell product acquisition and their in-house autothrottle know-how – which can assist diversify away from cyclicality within the industrial house. Lastly, when plane manufacturing finally slows down, plane house owners and operators nonetheless restore, improve, and retrofit their plane, which is the unique ISSC enterprise and bread and butter.

Conclusion

On the floor, ISSC is boring. You’d be forgiven for considering the identical factor. I’ve additionally skimmed over the corporate when it confirmed up on my screeners and Aerospace & Protection trade lists. It wasn’t till my curiosity finally gained over that I discovered that what this firm truly does is actually not boring. A minimum of, not when you like fast-growing, high-quality small firms, and good administration. And airplanes.

I’ve discovered loads throughout my lively investing years, and maybe a very powerful questions I’ve discovered to ask myself are: “Do I trust this management team? Are they experts in this industry, and do they understand what is needed by relevant customers?” After learning ISSC, the reply to my questions, not less than for me, is sure.

I fee ISSC a Sturdy Purchase.

![New Report Highlights Key Tricks to Maximize LinkedIn Efficiency [Infographic]](https://whizbuddy.com/wp-content/uploads/2024/02/bG9jYWw6Ly8vZGl2ZWltYWdlL2xpbmtlZGluX2FsZ29faW5zaWdodHMyLnBuZw.webp-600x435.webp)