Mike Dupre

Thesis

I wrote my last article on RH (NYSE:RH) when Berkshire Hathaway (BRK.A) exited its place and two different tremendous traders remained invested in RH. Sadly, Lone Pine additionally exited their position in Q3, promoting their 1.7 million shares. This was regardless of RH holding a 5% place in Lone Pine’s portfolio. In order that they as soon as had a whole lot of confidence within the firm. Different traders akin to Polen Capital and First Eagle Funding additionally decreased their holdings considerably.

The difficult atmosphere for the luxurious furnishings retailer and residential furnishings firm has left its mark. However simply because these traders are out doesn’t imply everybody ought to promote. As we have now seen with Netflix (NFLX) and Meta (META), many big-name traders might be mistaken. Nonetheless, the state of affairs for RH has modified for the more serious, and I’ll clarify why within the subsequent few chapters.

Steadiness Sheet

RH Investor Presentation

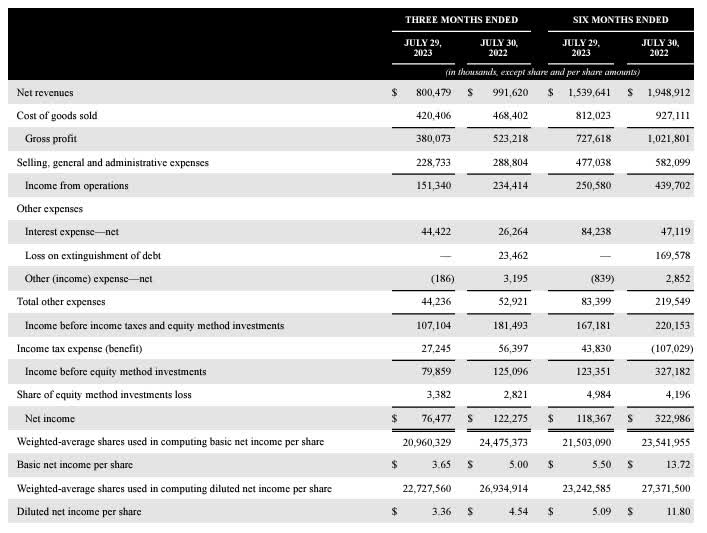

I believe RH’s steadiness sheet was higher. Money decreased from $1.5 billion to $417 million, whereas web debt elevated from $1 billion to $2 billion. In consequence, curiosity expense elevated from $47 million to $84 million attributable to larger curiosity expense on the time period mortgage. Web gross sales for the final 6 months additionally fell sharply, from $1.9 billion final 12 months to $1.5 billion this 12 months. In consequence, web earnings fell from $322 million to $118 million, representing a margin decline from 16.6% to 7.7%.

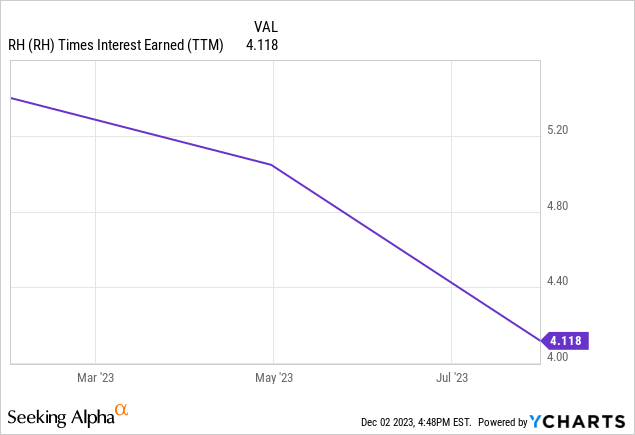

This ends in a ~4x curiosity protection ratio, effectively under the ~10x curiosity protection ratio of the S&P 500. So the chance of the debt state of affairs has elevated in contrast to a couple quarters in the past, and maybe the cash spent on share buybacks might have been higher used.

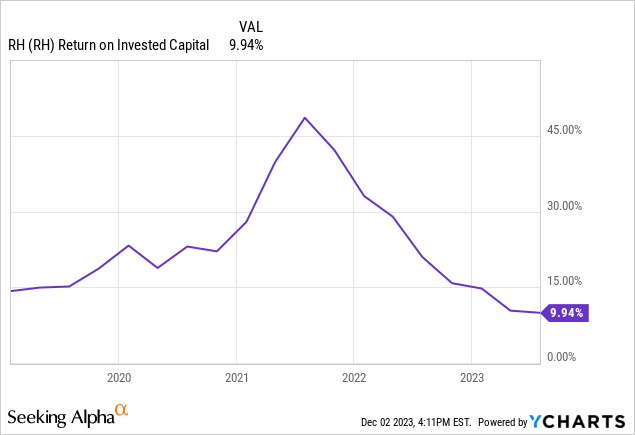

RH’s Capital Allocation

Because the risk-free charge elevated this 12 months, the price of fairness additionally elevated, leading to a better WACC. This mixed with declining ROIC is just not an excellent state of affairs because the ROIC-WACC unfold is narrowing. If we add within the rising debt, it’s attainable that RH is destroying worth proper now, as they might actually have a unfavorable unfold. Within the excellent case, the unfold will nonetheless be constructive, however it’s prone to be solely 2%. ROIC ought to come again as revenues and earnings normalize, however the query is how lengthy it is going to take. The time till that occurs might be troublesome for shareholders. However since RH has proven that they’ll earn a better return on their capital, now could also be an excellent time to speculate, as corporations that improve ROIC are usually a few of the finest performing shares.

Reverse DCF

Writer

My favourite software to see what’s priced right into a inventory is a reverse DCF. On this case, the bottom is a TTM diluted EPS of $13.22 and my low cost issue is 15% as a result of I believe this hurdle charge offers us an excellent margin of security. On this case, EPS must develop by 17% over the subsequent 10 years to justify the present share value. A really formidable goal, however the 5Y CAGR is 26.25%, so RH has been capable of beat that during the last 5 years. For an organization that likes to purchase again shares and sees itself as a progress firm, that is throughout the realm of risk. It is not going to be a simple job, however it’s not a very unrealistic aim, and if RH achieves it, shareholders might be handsomely rewarded.

Nonetheless, ought to income and margins proceed to say no, the buybacks alone is not going to be sufficient to safe the EPS progress charge going ahead. However, when RH repurchased a big portion of its excellent shares in 2017, they picked the suitable time. To this point, their timing on share repurchases has been impeccable. Let’s have a look at the way it goes this time.

Is There Sufficient Room For RH To Develop?

Worldwide enlargement with Dusseldorf and Munich in 2023 and Paris, Brussels and Madrid in 2024 will possible drive income, however the EU is a special market than the U.S., with completely different tastes and a special sense of aesthetics. As well as, the variations between international locations within the EU are additionally severe. The Germans, for instance, will not be identified for his or her affinity for vogue / design, whereas the Italians put a whole lot of emphasis on it.

As well as, RH Visitor Homes, RH Residences, RH Tub Home & Spa supply additional progress alternatives. Nonetheless, as they’re just like the core enterprise by way of luxurious and but new, this might result in ‘diworsification’.

Are There Important Dangers?

The $1.2 billion they used for buybacks, believing the inventory to be undervalued, might pose a danger if RH’s financial state of affairs doesn’t enhance within the subsequent few years. As a result of many would argue, as some are actually, that they might have used the cash for one thing extra helpful, like deleveraging or investing in additional future progress alternatives. As a result of the steadiness sheet is now worse than earlier than, and as web debt has elevated, the chance profile has change into much less favorable.

What To Watch For On The Subsequent Earnings Name?

As Gary Friedman’s earnings calls are all the time entertaining, and he says what he thinks, it is going to be attention-grabbing to see what he thinks about when it’s the proper time to purchase RH inventory and if his opinion a few powerful FY2024 has modified. In the last earnings call, his outlook for the remainder of 2023 and 2024 was fairly pessimistic. However corporations like Pulte (PHM), which is a homebuilder, have grown their revenues this 12 months, however with a whole lot of that coming from backlog. So it appears just like the housing market has not been hit as laborious as many feared.

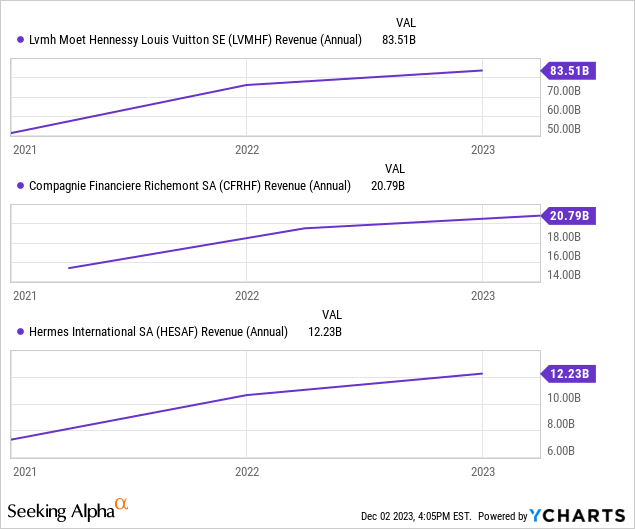

LVMH (OTCPK:LVMHF), Richemont (OTCPK:CFRHF), Hermes (OTCPK:HESAY) have additionally not felt the impression on their revenues as a lot as RH. So different luxurious and actual property corporations have weathered the disaster higher.

Constructing the RH ecosystem is one thing attention-grabbing, so I wish to hear some feedback from administration about it and what the plans are for the long run and if the event goes as deliberate.

Conclusion

RH rode a wave of straightforward cash that actually benefited luxurious and actual property corporations, however they’ve been hit laborious recently. Subsequently, their EPS CAGR of the final 5 years is prone to be elevated, and the subsequent 5 years will look completely different. RH is certainly an excellent firm with a polarizing CEO and an attention-grabbing thought that might work. Nonetheless, I’d not spend money on them proper now as a result of I believe there’s a whole lot of uncertainty across the firm and many various eventualities might happen. Nonetheless, if margins, ROIC and revenues rebound, RH might be a really attention-grabbing long-term funding from that time ahead.