Jay Yuno

Synopsis

Riskified (NYSE:RSKD) is an organization that provides software program as a service specializing in fraud and chargeback prevention expertise, significantly within the e-commerce sector.

RSKD’s historic income progress has been sturdy, rising within the double-digit vary. Nevertheless, bottom-line margins are unfavorable, and losses have expanded. These losses had been primarily pushed by rising SG&A bills. In 3Q23, income continued to develop strongly because of the profitable execution of its go-to-market technique, and there was an enchancment in its web losses, pushed by efficient SG&A administration.

Wanting forward, anticipated progress in e-commerce and rising e-commerce fraud circumstances are anticipated to positively influence RSKD’s future progress outlook. Nevertheless, ongoing uncertainties attributable to inflation have led administration to revise the 2023 income steerage downward. Given this combined outlook and the modest single-digit upside potential in its share worth, I’m recommending a maintain score for RSKD at this juncture.

Historic Monetary Efficiency

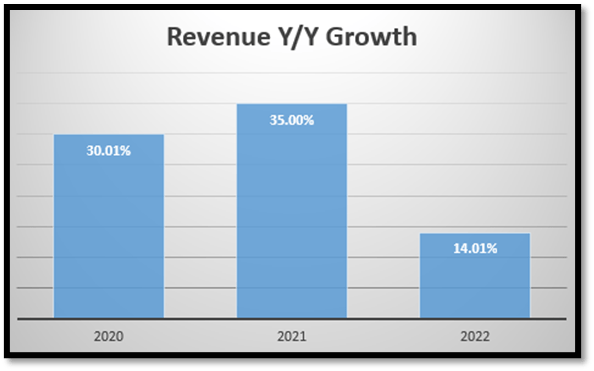

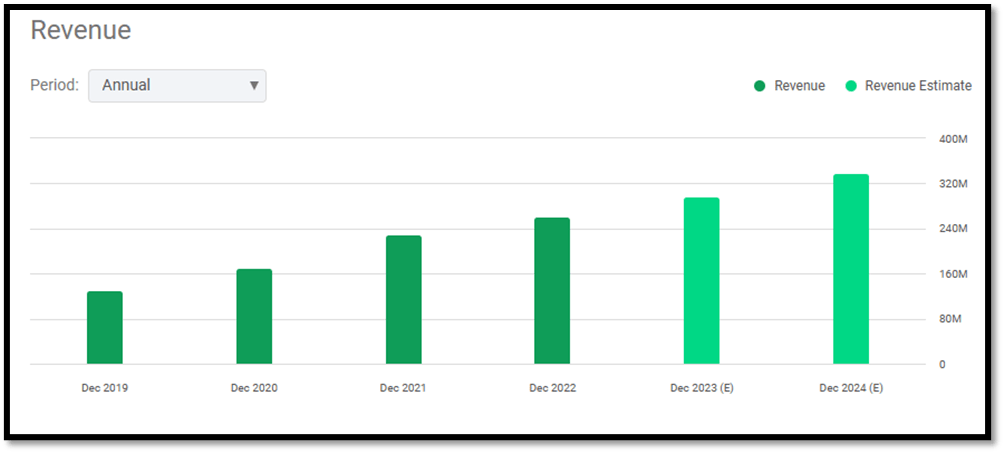

From 2020 to 2022, RSKD’s income progress has been rising strongly, and it’s within the double-digit vary. In 2020 and 2022, progress was within the 30% vary as COVID-19 boosted gross sales within the e-commerce sector, which benefited RSKD because it supplies e-commerce danger administration options. In 2022, progress slowed right down to ~14.01%. I consider the slowdown in 2022’s income progress has to do with RSKD’s strategic resolution and focus to enhance profitability by lowering total bills. On account of this, administration determined to slow down hiring. Nevertheless, administration doesn’t anticipate the hiring slowdown to have any unfavorable influence on its progress outlook in the long run.

Writer’s Chart

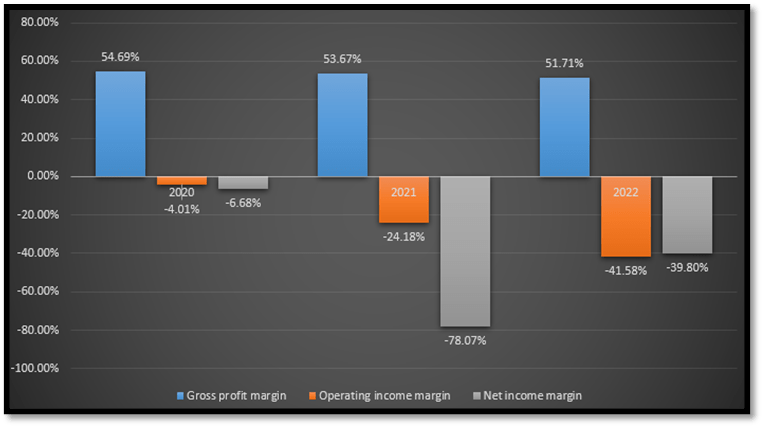

After I analyze RSKD’s margins, it’s clear that it’s unprofitable on the backside line. As of 2022, each working revenue and web revenue margin are in unfavorable territory. There’s a stark distinction compared with 2020 when its losses had been in single-digit percentages. Subsequent, let’s dive deeper into its P&L and attempt to perceive what drove its losses deeper into the crimson.

Writer’s Chart

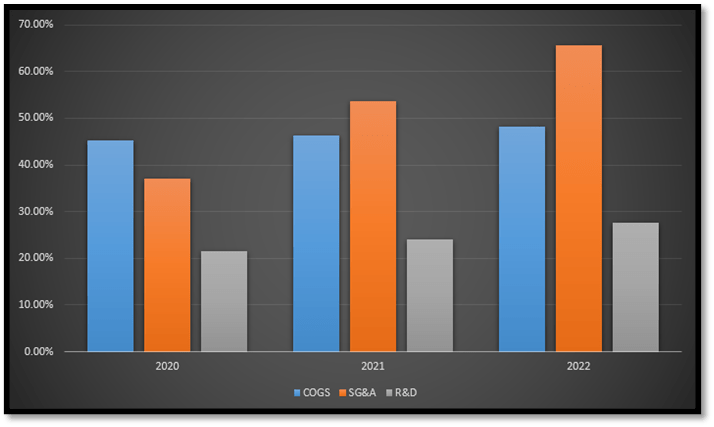

Primarily based on the next chart I’ve created, it’s clear that the primary driver of price is SG&A. In 2020, it solely accounted for ~37.11% of whole income, however by 2022, it had skyrocketed to ~65.73%. This vital rise in SG&A was because of the must drive top-line income progress, which is widespread for younger expertise companies akin to RSKD. By way of COGS and R&D, it has been fairly steady over the past three years.

Writer’s Chart

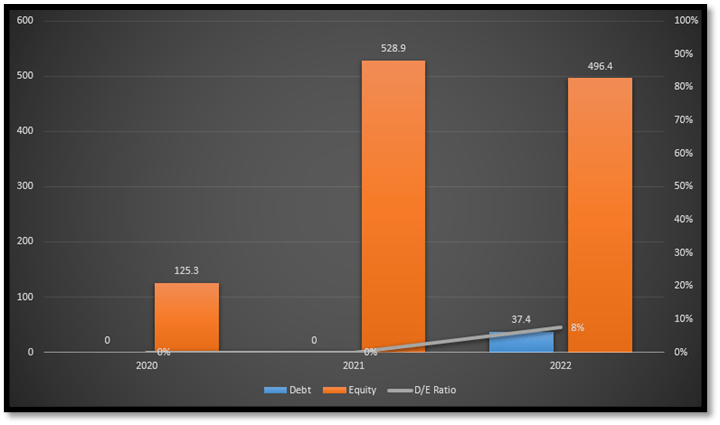

With unfavorable margins, it is essential to check out its debt ranges on its steadiness sheet, because it provides us a way of its present liquidity and solvency scenario. Primarily based on the next chart, it is fairly clear that its debt-to-equity ratio [D/E] is extraordinarily low, within the single-digit vary. Nevertheless, I do discover there’s a slight uptick in debt in 2022, inflicting D/E to rise to ~8%.

Writer’s Chart

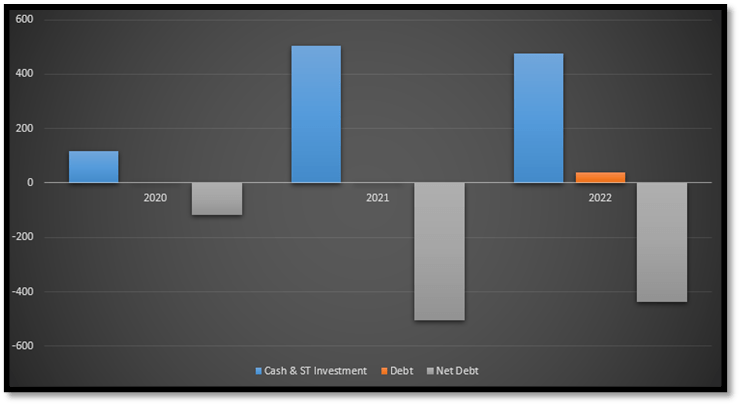

Though it could be nerve-wracking to see debt alongside unfavorable margins, I consider that inspecting the online debt supplies a clearer understanding of RSKD’s monetary energy. Web debt is outlined as whole money and short-term [ST] investments minus whole debt. From the next chart, it’s clear that RSKD has greater than sufficient liquid money to cowl its debt ranges. Due to this fact, I don’t count on any points arising from its money owed.

Writer’s Chart

Analyzing RSKD’s 3Q23 Earnings

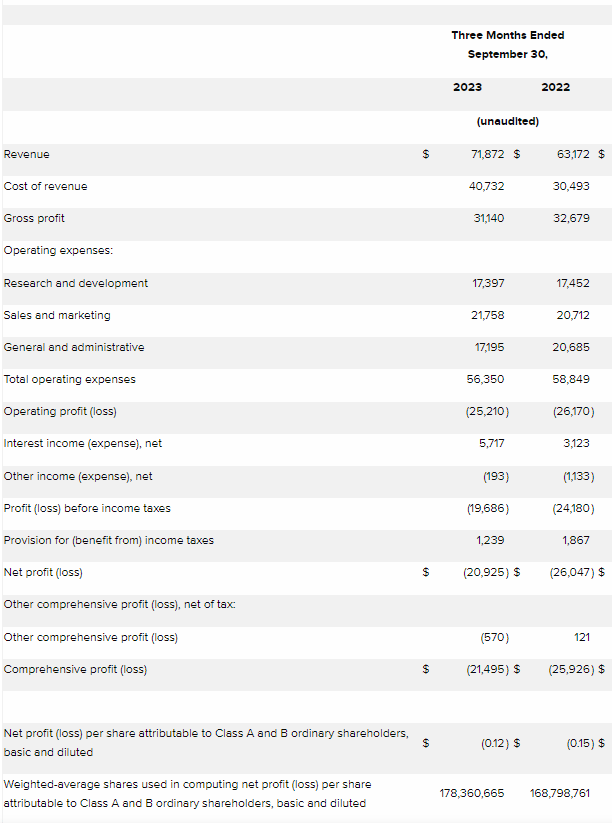

In 3Q23, RSKD reported income progress of ~14% year-over-year, pushed by its profitable execution of its go-to-market technique. RSKD has been profitable in including new retailers, retaining and upselling current ones, and increasing market share.

Taking a look at its 3Q23 margins, it’s clear that there are enhancements in its working revenue and web revenue margin as each of its losses contracted. For 3Q23, the working revenue margin improved ~6% to unfavorable 35%. Web revenue margin improved ~12% to unfavorable 29%.

In 3Q23, I seen a slight contraction within the gross revenue margin, which was on account of a major fraud occasion reported by one in every of its largest retailers. Nevertheless, administration believes and states that they don’t anticipate this occasion affecting the following quarters. Due to this fact, I count on to see the gross revenue margins return to normalized ranges within the upcoming quarters.

Writer’s Chart

The development in margins is attributed to efficient SG&A price administration. In 3Q23, SG&A as a share of whole income contracted year-over-year to ~54%, down from 2Q22’s ~66%. This represents an enchancment of ~12% in SG&A prices. However, R&D was not sacrificed with a view to enhance margins, and that is particularly essential for a younger expertise agency that focuses on software program options.

Writer’s Chart Riskified IR

Robust E-Commerce Progress Will Assist RSKD’s Future Progress

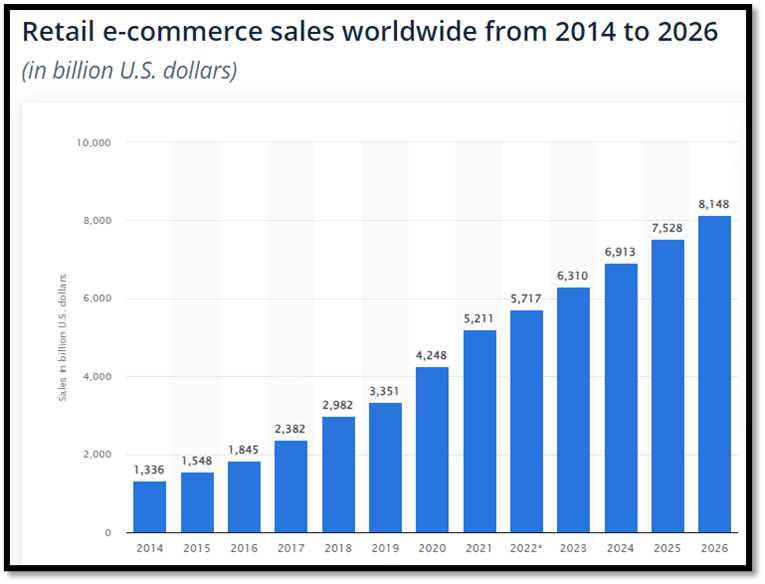

In 2022, world e-commerce gross sales reported a determine of ~$5.7 trillion, and it’s anticipated to achieve ~$8.1 trillion by 2026. This represents a CAGR of ~14.9% [2014–2026], and it’s anticipated to proceed rising till 2026. This sturdy double-digit progress within the world e-commerce market will bolster RSKD’s future income because it sells e-commerce danger administration software program options akin to fraud and chargeback prevention expertise.

Statista

With rising e-commerce gross sales, e-commerce fraud is certain to extend. Primarily based on statistics launched by Mastercard, it was acknowledged that world e-commerce fraud has been rising. In 2022, losses reached a staggering $41 million, and they’re anticipated to proceed to extend in extra of $48 million by 2023. Out of all of the international locations globally, North America [NA] has the best stage of e-commerce fraud, accounting for ~42% of all e-commerce fraud globally.

In response to the next quote by RSKD’s CFO, Aglika Dotcheva, the US is RSKD’s largest area. Due to this fact, I anticipate that the rising fraud circumstances within the US because of the anticipated progress in e-commerce gross sales will improve the demand for RSKD’s resolution.

Quote: “Finally, we also saw revenue growth across all geographies. Our third quarter revenue in the United States, our largest region, grew by 9% year-over-year”

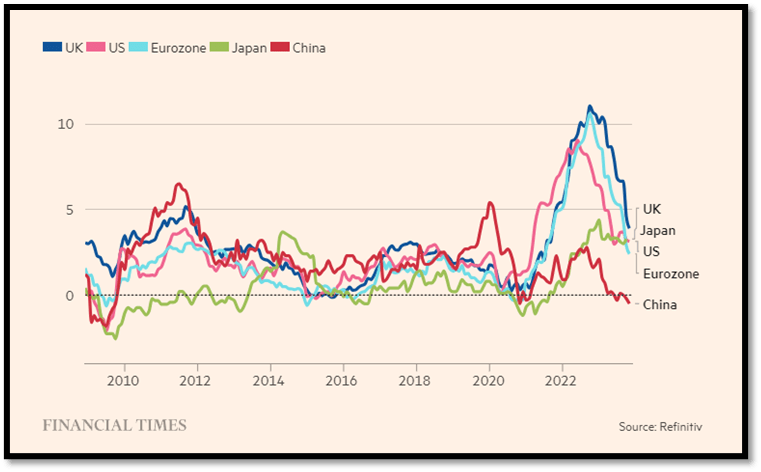

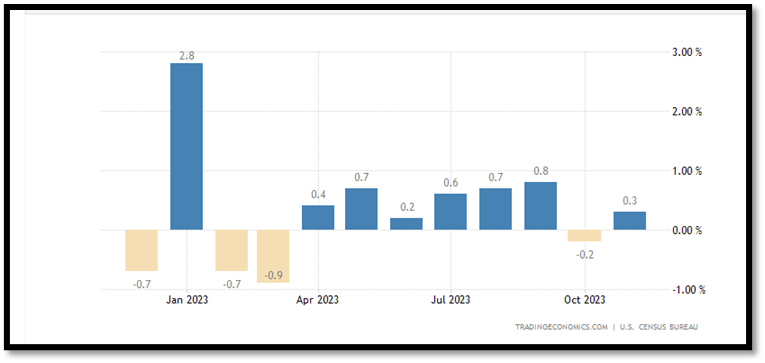

Inflation Is Nonetheless Casting Shadows and Uncertainty

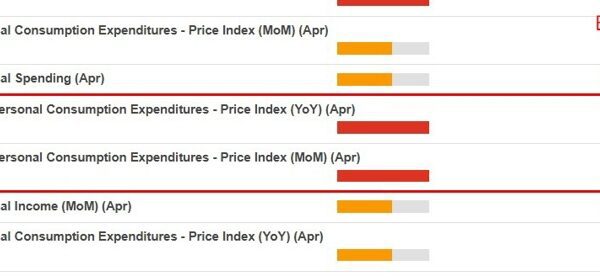

Primarily based on the global inflation chart, there’s a clear pattern towards cooling inflation. Consequently, this lower in inflation has bolstered retail spending. The second chart exhibits clear indicators that US retail spending has been rising since April 2023, apart from October 2023, partially because of the United Auto Employees strike, which affected the provision of automotive automobiles. The development in retail spending is more likely to profit RSKD as it’ll assist e-commerce gross sales, thereby enhancing its progress outlook.

Nevertheless, it is essential to notice that whereas inflation has considerably cooled from the 2022 spike, it stays above the goal fee of ~2% in lots of international locations. This example continues to create macroeconomic uncertainties globally, because the market remains to be unsure about when inflation will stabilize, which is a key think about figuring out the path of central banks’ rates of interest.

Monetary Instances Buying and selling Economics

Up to date Steering Displays the Macro Setting Unsure

Because of the uncertainty attributable to inflation being above the central financial institution’s goal fee, RSKD has up to date its 2023 guidance. Beforehand, income was within the vary of $298 to $303 million, but it surely has been revised to $297 to $300 million.

On the EBITDA aspect, it has been revised from a spread of unfavorable $17 to $12 million to unfavorable $14.5 to $12.5 million. I welcome this EBITDA adjustment because it indicators administration’s confidence in its price administration initiatives and shows its dedication to drive margin enchancment.

Comparable Valuation

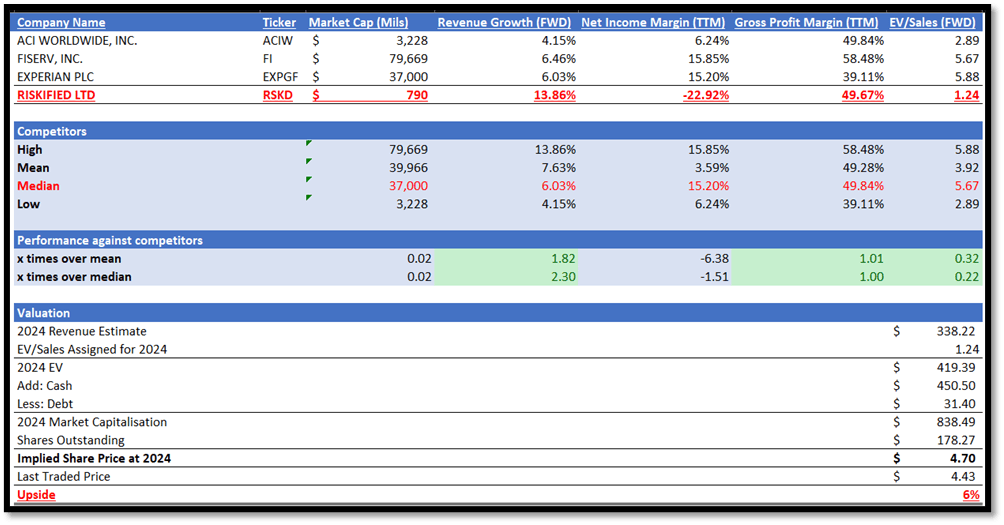

Earlier than transferring on, I need to make clear the comparable firms listed in my valuation mannequin. Whereas RSKD operates within the utility software program business and makes a speciality of fraud and chargeback prevention software program expertise, the three opponents I’ve recognized additionally provide on-line transaction safety, fraud detection, and danger administration options, making them extra appropriate for comparability.

Proper off the bat, it’s clear that RSKD is way smaller than its opponents. Its market capitalization is ~$790 million, whereas opponents’ median is ~$37 billion. By way of dimension, RSKD is barely 2% of opponents median. Regardless of its smaller dimension, its ahead progress outlook is twice that of its opponents. RSKD’s progress outlook is ~13.86%, whereas opponents’ median is ~6.03%. Nevertheless, it’s fairly widespread for smaller firms to develop quicker on account of simpler comparable years, also referred to as the bottom impact.

In terms of profitability, the narrative shifts. Amongst all the businesses listed, RSKD is the one one reporting a web loss, the drivers of which have been mentioned in depth earlier. Nevertheless, when it comes to gross revenue margins, RSKD aligns with the median of its opponents.

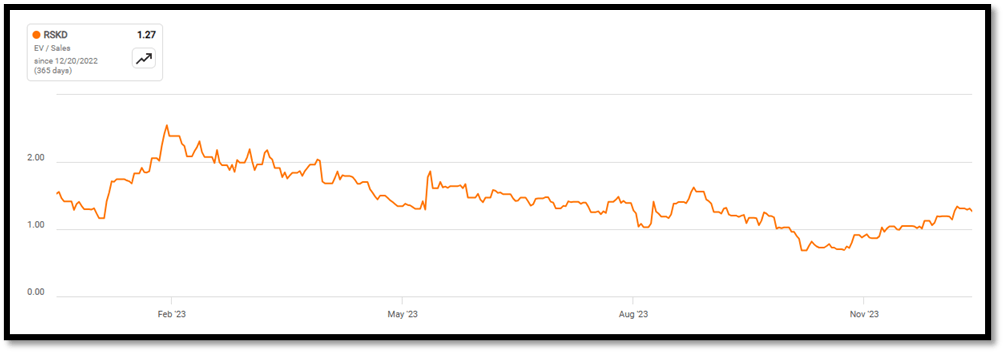

On account of its web losses, RSKD is presently buying and selling at 1.24x ahead EV/Gross sales, whereas its opponents are buying and selling at 5.67x. Taking a look at RSKD’s 1-year common EV/Gross sales, it’s in keeping with its present ahead EV/Gross sales. Due to this fact, I consider that there’s a low danger that its present EV/Gross sales is over or undervalued. With these supporting elements, I consider that the EV/Gross sales market assigned to RSKD is honest and justified.

I utilized its 1.24x ahead EV/Gross sales to its 2024 market income estimate, and my goal worth for RSKD is ~$4.70, which represents a modest upside potential of ~6%, which for my part lacks margin of security. Due to this fact, I’m recommending a maintain score for RSKD.

Writer’s Valuation Mannequin In search of Alpha In search of Alpha

Upside Threat to My Maintain Score

For my part, I consider inflation would possibly simply be the catalyst for RSKD’s share worth to understand. In my evaluation of RSKD, I discussed that its margins had been in unfavorable territory and that it was primarily pushed by SG&A. If inflation cools even additional, it’ll drive its SG&A bills down, which finally results in margin growth. As well as, administration is taking lively steps to handle its present price scenario. Within the occasion that margins had been to be higher than anticipated, its share worth would possibly admire.

Secondly, as mentioned above, income steerage was up to date on account of uncertainty attributable to inflation. Once more, if inflation cools greater than anticipated and upcoming income beats expectations, it’ll trigger its share worth to understand.

Conclusion

In conclusion, RSKD’s historic monetary efficiency is combined. High-line income is rising robustly within the double-digit vary, however I did discover a slowdown in 2022 on account of administration’s concentrate on profitability. It has additionally reported a web loss that’s exacerbated by rising SG&A prices, however administration has expressed its dedication to bolstering bottom-line margins. In 3Q23, RSKD continued to report sturdy income progress. On the identical time, margins are bettering via SG&A expense administration.

Shifting forward, I count on the anticipated progress within the world e-commerce market will drive demand for RSKD’s options and thus assist a constructive progress outlook. As well as, world e-commerce fraud is rising in keeping with the expansion of the e-commerce market. I consider this may even drive demand for RSKD’s merchandise.

Though inflation has cooled from 2022’s peak, it’s nonetheless above the central financial institution’s goal charges. Therefore, it’s casting doubt and uncertainty available in the market. Consequently, administration has revised their 2023 income steerage downward to raised replicate the present market outlook.

After I carried out my comparable valuation, it revealed that RSKD is trailing its opponents when it comes to web revenue, but it surely has outperformed them when it comes to progress outlook. Its present EV/Gross sales ratio is decrease than the median of its opponents, reflecting its web loss scenario. As well as, its present EV/Gross sales ratio can also be in keeping with its historic common. Thus, these elements assist my perception that its present valuation assigned by the overall market is justified. With an absence of margin of security in my goal worth, I’m recommending a maintain score at this second for RSKD.