Ralf Hahn

Focus of Article:

The main focus of this two-part article is to supply a really detailed evaluation evaluating Rithm Capital Corp. (NYSE:RITM) to 19 different mortgage actual property funding belief (mREIT) friends I presently totally cowl. I’m scripting this two-part article because of the continued requests that such an evaluation be particularly carried out on RITM and a few of the firm’s mREIT friends at periodic intervals. For readers who simply need the summarized conclusions/outcomes, I’d recommend to scroll all the way down to the “Conclusions Drawn” part on the backside of every a part of the article.

PART 1 of this text analyzed RITM’s current outcomes and in contrast a number of of the corporate’s metrics to 19 mREIT friends. PART 1 additionally confirmed how RITM’s ebook worth (“BV”) as of 12/31/2023 in comparison with the 19 different mREIT friends. PART 1 helps result in a greater understanding of the matters and evaluation that will probably be mentioned in PART 2. The hyperlink to PART 1’s evaluation is offered beneath:

The main focus of PART 2 of this text is to match RITM’s current dividend per share charges, yield percentages, and several other dividend sustainability metrics to 19 mREIT friends. This evaluation will present current previous knowledge with supporting documentation inside Desk 9 beneath. This text can even talk about RITM’s dividend sustainability which is partially based mostly on the metrics outlined in Desk 9. A extra in-depth evaluation of RITM’s dividend sustainability will probably be offered in Desk 10 beneath.

By analyzing these metrics, one will higher perceive which mREIT typically has a safer dividend charge going ahead versus different friends who typically have the next danger for a dividend lower or the next chance of a dividend improve and/or a particular periodic dividend being declared. When each again testing and projecting the metrics inside this evaluation, the outcomes have continued to be confirmed extraordinarily dependable. This isn’t the one knowledge that must be examined to provoke a place inside a specific inventory/sector. Nevertheless, I imagine this evaluation can be a superb “starting-point” to start a dialogue on the subject. On the finish of this text, there will probably be a conclusion relating to the next comparisons between RITM and the 19 mREIT friends: 1) trailing 12-month (“TTM”) yields based mostly on a inventory value as of three/29/2024 (together with 1- and 5-year dividend change); 2) annual ahead yield based mostly on a inventory value as of three/29/2024; and 3) annual ahead yield based mostly on my estimated CURRENT BV (BV as of three/31/2024). I can even present my present RITM BUY, SELL, or HOLD suggestion, value goal, and dividend per share charge projection for the second and third quarters of 2024.

Aspect Notice: I imagine there are a number of completely different classifications on the subject of mREIT firms. For functions of this text sequence, I’m specializing in 4. For readers who’re new to my articles or for present readers who want a “refresher” on a number of completely different mREIT classifications, please see PART 1 of this text (hyperlink offered above).

Dividend Per Share Charges and Yield Percentages Evaluation – Overview:

Allow us to begin this evaluation by getting accustomed to the knowledge offered in Desk 9 beneath. This will probably be helpful when evaluating RITM to the 19 mREIT friends inside this evaluation.

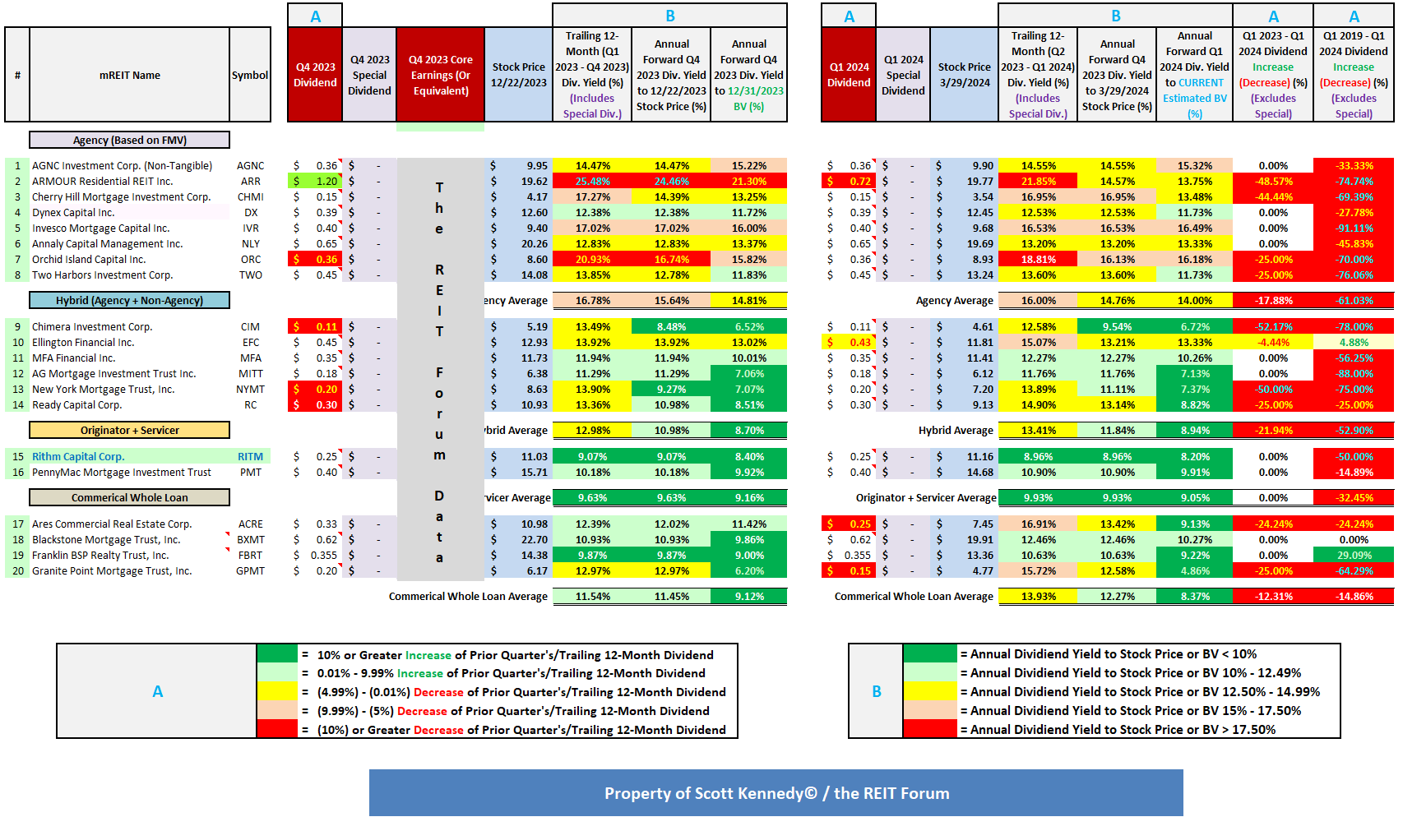

Desk 9 – Dividend Per Share Charges and Yield Percentages

The REIT Discussion board

(Supply: Desk created by me, acquiring historic inventory costs from NASDAQ and every firm’s dividend per share charges from the SEC’s EDGAR Database)

Utilizing Desk 9 above as a reference, the next info is offered (see every corresponding column): 1) dividend per share charge for the fourth quarter of 2023 (for month-to-month dividend payers, the overall month-to-month dividends in the course of the quarter); 2) core earnings (or core earnings equal) for the fourth quarter of 2023; 3) inventory value as of 12/22/2023; 4) TTM dividend yield (dividend per share charge from the primary quarter of 2023 – fourth quarter of 2023); 5) annual ahead dividend yield based mostly on the dividend per share charge for the fourth quarter of 2023 utilizing the inventory value as of 12/22/2023 (for month-to-month dividend payers, the newest month-to-month dividend per share charge in the course of the quarter); 6) annual ahead dividend yield based mostly on the dividend per share charge for the fourth quarter of 2023 utilizing a BV as of 12/31/2023 (for month-to-month dividend payers, the newest month-to-month dividend per share charge in the course of the quarter); 7) dividend per share charge for the primary quarter of 2024 (for month-to-month dividend payers, the overall month-to-month dividends in the course of the quarter); 8) inventory value as of three/29/2024; 9) TTM dividend yield (dividend per share charge from the second quarter of 2023 – first quarter of 2024); 10) annual ahead dividend yield based mostly on the dividend per share charge for the primary quarter of 2024 utilizing the inventory value as of three/29/2024 (for month-to-month dividend payers, the newest month-to-month dividend per share charge in the course of the quarter); 11) annual ahead dividend yield based mostly on the dividend per share charge for the primary quarter of 2024 utilizing estimated CURRENT BV (BV as of three/29/2024) (for month-to-month dividend payers, the newest month-to-month dividend per share charge in the course of the quarter); 12) dividend per share charge for the primary quarter of 2024 versus the primary quarter of 2023 (proportion fluctuation); and 13) dividend per share charge for the primary quarter of 2024 versus the primary quarter of 2019 (proportion fluctuation; exhibits post-COVID-19 and rate of interest/yield influence to every firm’s dividend).

As of three/29/2024, RITM, AGNC Funding Corp. (AGNC), ARMOUR Residential REIT Inc. (ARR), Cherry Hill Mortgage Funding Corp. (CHMI), Dynex Capital Inc. (DX), Annaly Capital Administration Inc. (NLY), Orchid Island Capital Inc. (ORC), Ellington Monetary Inc. (EFC), MFA Monetary Inc. (MFA), AG Mortgage Funding Belief Inc. (MITT), New York Mortgage Belief, Inc. (NYMT), Prepared Capital Corp. (RC), Ares Business Actual Property Corp. (ACRE), Blackstone Mortgage Belief, Inc. (BXMT), Franklin BSP Realty Belief, Inc. (FBRT), and Granite Level Mortgage Belief, Inc. (GPMT) had a inventory value that “reset” decrease relating to every firm’s month-to-month/quarterly dividend accrual. In different phrases, every firm’s “ex-dividend date” for March 2024/the primary quarter of 2024 had already occurred.

As of three/29/2024, Invesco Mortgage Capital Inc. (IVR), Two Harbors Funding Corp. (TWO), Chimera Funding Corp. (CIM), and PennyMac Mortgage Funding Belief (PMT) had a inventory value that had not reset decrease in reference to the corporate’s March 2024/the primary quarter of 2024 dividend accrual. Readers ought to take these factors into consideration because the evaluation is introduced beneath. Allow us to now start the comparative evaluation between RITM and the 19 mREIT friends.

Evaluation of RITM:

Wanting again at RITM’s dividend historical past over the previous 10 years, the corporate elevated its dividend from $0.35 per frequent share in the course of the third quarter of 2014 to $0.50 per frequent share by the fourth quarter of 2019. This consisted of gradual dividend will increase over this span of roughly 5 years. Nevertheless, together with a majority of sector friends, RITM cautiously decreased the corporate’s quarterly dividend to only $0.05 per frequent share in the course of the first quarter of 2020 as a direct results of worry surrounding the COVID-19 “pandemic panic”. Throughout this timeframe, previous to the Federal (“Fed”) Reserve’s fast, decisive motion to calm markets by each rate of interest and financial coverage, repurchase (“repo”) settlement and hedging counterparties rapidly (and incorrectly in my view) initiated margins calls on most sector friends which created a “snowball” impact on this particular market. This included each company and non-agency mortgage-related investments.

In different phrases, there was a fast, sharp leverage/liquidity disaster throughout sure pockets of credit score markets the place sure property/investments are used as collateral to underlying excellent borrowings/debt. Most sector friends both voluntarily, or had been pressured, to deleverage and lift money throughout this time interval. Outcomes assorted vastly from peer-to-peer relating to the severity of every firm’s funding portfolio lower and dividend discount. Bear in mind, on the time, an unlimited quantity of worry/hypothesis surrounded markets relating to future financial efficiency. Relating to RITM, this primarily pertained to residential housing points; specifically strains on mortgage servicers from the potential “influx” of missed mortgage funds and a servicer’s duty to “front” principal and curiosity funds to traders (who’re then reimbursed by government-sponsored enterprises [GSEs] relating to company MSRs). The truth is, a number of broader sector friends suspended dividends for a number of quarters out of an abundance of warning.

Nevertheless, as worry/warning rapidly subsided, RITM elevated the corporate’s dividend to $0.10, $0.15, and $0.20 per frequent share in the course of the second, third, and fourth quarter of 2020, respectively. RITM subsequently elevated the corporate’s dividend to $0.25 per frequent share in the course of the third quarter of 2021 which has remained fixed since. I’d remind readers that whereas many sector friends have decreased dividends over the previous 2 years, RITM has been one in all uncommon exceptions to this pattern (particularly when in comparison with the company and hybrid mREIT sub-sectors and extra not too long ago some throughout the industrial complete mortgage sub-sector).

Utilizing Desk 9 above as a reference, RITM declared a dividend of $0.25 per frequent share for the fourth quarter of 2023. This was an unchanged dividend lower when in comparison with the prior quarter. RITM’s inventory value traded at $11.03 per share on 12/22/2023. When calculated, this was a TTM dividend yield of 9.07%, an annual ahead yield to RITM’s inventory value as of 12/22/2023 of 9.07%, and an annual ahead yield to the corporate’s BV as of 12/31/2023 of 8.40%. When evaluating every yield proportion to RITM’s originator + servicer mREIT peer inside this evaluation, the corporate’s TTM dividend yield proportion, annual ahead yield proportion based mostly on its inventory value, and its annual ahead yield proportion based mostly on its estimated CURRENT BV had been barely (at or better than 0.50% however lower than 1.00%) beneath common.

As was mentioned in PART 1 of this text, RITM’s at-risk leverage ratio (on- and off-balance sheet) was decrease when in comparison with the corporate’s lone sub-sector peer inside this evaluation, PMT. Traditionally talking, RITM has usually run decrease leverage versus PMT. From charting previous traits, usually a leverage ratio has equated to beneath common dividend yield percentages. After all, there are numerous different elements at play relating to dividend sustainability (particularly in gentle of the occasions surrounding the COVID-19 pandemic panic again in March 2020). Nevertheless, an organization’s leverage ratio is one “general” metric which I imagine must be analyzed.

I proceed to imagine an necessary metric to investigate when assessing RITM’s near-term dividend sustainability is the corporate’s quarterly core earnings (and adjusted core earnings). RITM’s earnings accessible for distribution (“EAD”) is now the equal to the corporate’s beforehand disclosed core earnings. As such, the phrases are interchangeable inside this text. Presently, RITM’s core earnings/EAD is the closest metric to the corporate’s “true earnings power” relating to its funding portfolio’s efficiency. To clarify/talk about this metric, Desk 10 is offered beneath.

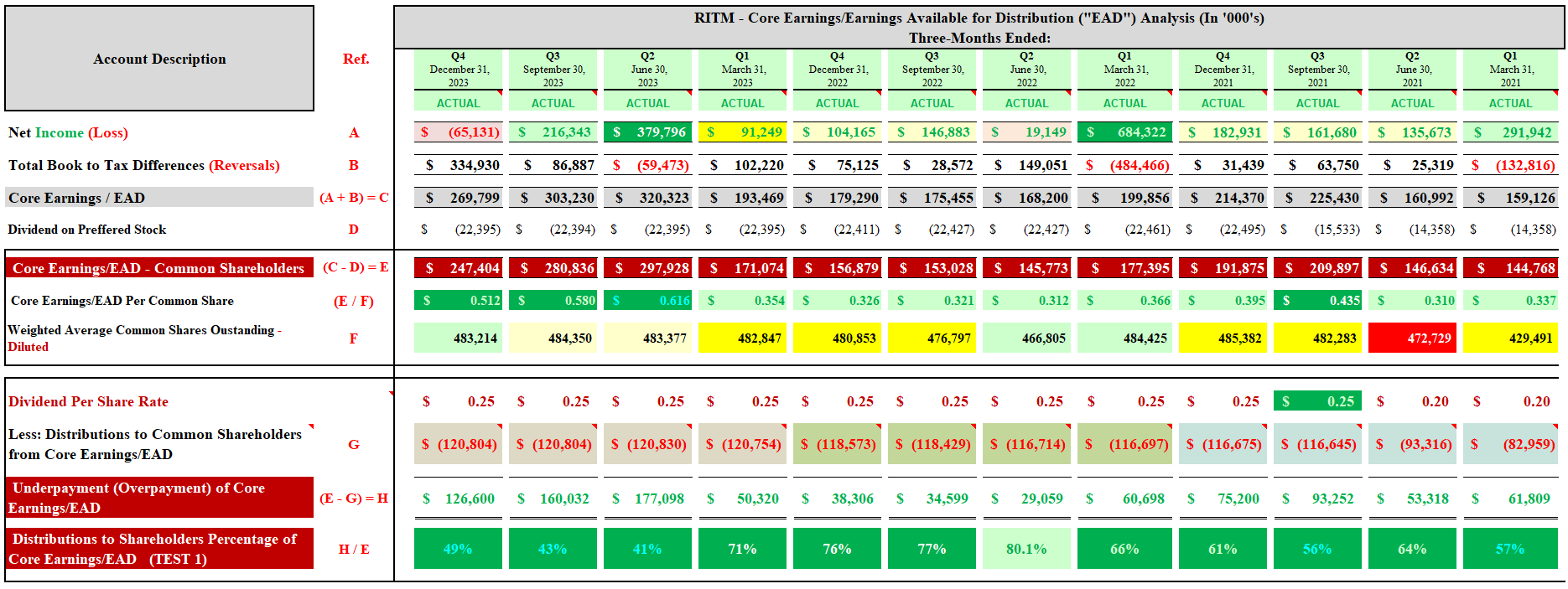

Desk 10 – RITM Quarterly Core Earnings/EAD Evaluation (Q1 2021 – This autumn 2023)

The REIT Discussion board

(Supply: Desk created by me, partially utilizing knowledge obtained from RITM’s quarterly shareholder presentation for the first quarter of 2021 – fourth quarter of 2023)

Utilizing Desk 10 above as a reference, RITM reported core earnings/EAD accessible to frequent shareholders of $144.8, $146.6, $209.9, and $191.9 million for the primary, second, third, and fourth quarter of 2021, respectively (see crimson reference “E”). When calculated, RITM had core earnings/EAD accessible to frequent shareholders of $0.34, $0.31, $0.44, and $0.40 per share, respectively (see crimson reference “E / F”). These figures had been notably above the corporate’s dividend of $0.20, $0.20, $0.25, and $0.25 per frequent share for the primary, second, third, and fourth quarter of 2021, respectively. This calculates to a quarterly dividend distributions payout ratio of 57%, 64%, 56%, and 61% for the primary, second, third, and fourth quarter of 2021, respectively (see crimson reference “H / E”). Merely put, a really engaging quarterly dividend distributions payout ratio all through 2021; even after a dividend improve of $0.05 per frequent share in the course of the third quarter of 2021.

Transferring to 2022, RITM reported core earnings/EAD accessible to frequent shareholders of $177.4, $145.8, $153.0, and $156.9 million for the primary, second, third, and fourth quarter of 2022, respectively. When calculated, RITM had core earnings/EAD accessible to frequent shareholders of $0.37, $0.31, $0.32, and $0.33 per share, respectively. This calculates to a quarterly dividend distributions payout ratio of 66%, 80%, 77%, and 76% for the primary, second, third, and fourth quarter of 2022, respectively. Merely put, a gorgeous – very engaging quarterly dividend distributions payout ratio all through 2022. This even contains the actual fact short-term charges/borrowing prices quickly elevated throughout 2022.

Transferring to 2023, RITM reported quarterly core earnings/EAD accessible to frequent shareholders of $171.1, $297.9, $280.8, and $247.4 million for the primary, second, third, and fourth quarter of 2023, respectively. When calculated, RITM had core earnings/EAD accessible to frequent shareholders of $0.35, $0.62, $0.58, and $0.51 per share, respectively. This calculates to a quarterly dividend distributions payout ratio of 71%, 41%, 43%, and 49% for the primary, second, third, and fourth quarter of 2023, respectively. Merely put, a really engaging quarterly dividend distributions payout ratio throughout 2023. A VERY constant theme for RITM which has been a uncommon incidence relating to the broader mREIT sector.

Nevertheless, to stay non-bias, when excluding a one-time good thing about $0.20, $0.15, and $0.11 per frequent share in direct relation to the sale of extra MSRs in the course of the second, third, and fourth quarter of 2023, RITM reported adjusted core earnings/EAD of $0.42, $0.43, and $0.40 per frequent share for the second, third, and fourth quarter of 2023, respectively. Nonetheless, this calculates to a quarterly dividend distributions payout ratio of 60%, 58%, and 62% for the second, third, and fourth quarter of 2023, respectively.

Usually talking, repurchase settlement (“repo”) financing charges have probably peaked in late 2023. Borrowing/Financing charges exterior repo agreements probably have peaked in early 2024. Internet curiosity spreads throughout the broader sector have probably “bottomed out” in late 2023 – early 2024. Then, a sluggish, gradual improve in internet spreads will probably start by mid 2024. This additionally considers the derivatives facet of the equation.

It also needs to be famous 100% of RITM’s 2023 dividends had been categorized as “ordinary income”. In different phrases, 0% of RITM’s 2023 dividends had been categorized as a “return of capital” (“ROC”) distribution. This must be thought of a constructive catalyst/pattern.

As soon as once more utilizing Desk 9 as a reference, RITM declared a dividend of $0.25 per share for the primary quarter of 2024. This was an unchanged dividend when in comparison with the prior quarter. RITM’s inventory value traded at $11.16 per share on 3/29/2024. When calculated, this was a TTM dividend yield of 8.96%, an annual ahead yield to RITM’s inventory value as of three/29/2024 of 8.96%, and an annual ahead yield to the corporate’s estimated CURRENT BV of 8.20%. When evaluating every yield proportion to RITM’s originator + servicer mREIT peer inside this evaluation, the corporate’s TTM dividend yield proportion, annual ahead yield proportion based mostly on its inventory value, and its annual ahead yield proportion based mostly on its estimated CURRENT BV remained barely beneath common. Going ahead, I imagine RITM ought to have an annual ahead yield close to the originator + servicer mREIT common. As such, RITM continues to have a notable “cushion” relating to future dividend sustainability; even when there’s a modest lower to the corporate’s core earnings/EAD throughout 2024.

A Couple Comparisons Between RITM and the Firm’s 19 mREIT Friends in Rating Order:

Extra warning/danger ought to presently be assigned to AGNC, ORC, and IVR (nothing too alarming with AGNC although). We already know ARR declared a notable dividend discount in January 2024 from $0.40 to $0.24 per frequent share. Nevertheless, earlier quarters’ Tables 11 and 12 had “foreshadowed” this notable dividend discount since early 2023. As well as, even with the pretty current ORC month-to-month discount from $0.16 to $0.12 per frequent share, ORC’s annual ahead dividend yield (relative to estimated CURRENT BV) stays excessive and wishes continued monitoring. As is at all times the case, that is one thing I/we’ll constantly monitor as 2024 unfolds.

I’d level out ORC accounts for the corporate’s premium amortization expense/low cost accretion revenue equal otherwise when in comparison with its company mREIT sub-sector friends. First, this results in timing variations which might “prop up” weighted common yields throughout sure rate of interest cycles. As such, ORC’s yield percentages proceed to be above the company mREIT sub-sector common. Second, this will “appear to buoy” ORC internet unfold metrics when, in actuality, a reclassification of the corporate’s equal to premium amortization expense would present a way more modest internet unfold revenue metric (or vice versa when low cost accretion revenue is reported). That is additionally usually why a bigger than common company mREIT proportion of ORC’s dividend declarations over the previous a number of years have been categorized as a “return on capital” (“ROC”) distribution. Merely put, ORC continues to distribute dividends in extra of the corporate’s annual REIT taxable revenue (“AREITTI”). Additional dialogue of this ORC subject is past a RITM sector comparability article (additionally has been extensively lined in prior ORC mREIT articles over time).

The severity of RC’s (17%) dividend lower in the course of the fourth quarter of 2023 was disappointing and was instantly in relation to the continued underperformance throughout the firm’s acquired Broadmark Realty Capital Inc. (beforehand BRMK) investments. As well as, the BRMK merger resulted in a notable discount in leverage and RC obtained a superb quantity of non-/underperforming-assets. Now some readers could also be asking nicely why did RC purchase BRMK if stated property are producing a low yield (or no yield in any respect)? The reply is fairly easy. Bear in mind, RC acquired BRMK at a really notable low cost so buying actual property owned (“REO”)/troubled property was at all times a part of the method. The acquisition value mainly justified the acquisition. The worth is when RC finally sells these property and redeploys this newly-acquired capital into the corporate’s “niche” investments (and builds leverage again as much as extra historic ranges). Nevertheless, this course of/technique has merely taken longer versus what RC initially anticipated which is disappointing. I proceed to undertaking future RC earnings progress however that is going to take some extra time to play out.

Conclusions Drawn (PART 2):

PART 2 of this text in contrast RITM to 19 mREIT friends with reference to current dividend per share charges, yield percentages, and several other different dividend sustainability metrics. This text additionally mentioned RITM’s previous dividend traits/historical past. Utilizing Desk 9 as a reference, the next had been the current dividend per share charge and yield percentages for RITM:

RITM: $0.25 per frequent share dividend for the primary quarter of 2024; 8.96% TTM dividend yield; 8.96% annual ahead yield to the corporate’s inventory value as of three/29/2024; and eight.20% annual ahead yield to my projected CURRENT BV.

When combining this knowledge together with metrics inside Desk 10 (core earnings/EAD) and different modeling sources, the next chance relating to RITM’s near-term dividend sustainability is offered:

RITM: Very Excessive (90%) chance of a steady dividend for Q2 2024

RITM: Very Excessive (90%) chance of steady dividend for Q3 2024

Q1 2024 Projected Adjusted Core Earnings/EAD: $0.370 – $0.420 per frequent share

Preliminary Q2 2024 Projected Adjusted Core Earnings/EAD: $0.365 – $0.415 per frequent share*

* = Assuming a RITM spin-off doesn’t happen previous to the top of the second quarter of 2024

As defined in PART 1 of this text, RITM’s portfolio composition, leverage, borrowing prices, hedging protection ratio (danger administration technique), and prepayment speeds additionally must be thought of when discussing the corporate’s core earnings/EAD.

Whereas I imagine RITM’s core earnings/EAD will stay comparatively unchanged over the subsequent couple of quarters as short-term funding prices stay elevated and MSR prepayment speeds “tick higher”, as evidenced in Desk 10 this mREIT has a really giant “cushion” relating to dividend sustainability.

My BUY, SELL, or HOLD Suggestion:

From the evaluation offered above, together with extra catalysts/elements not mentioned inside this text, I presently charge RITM as a SELL once I imagine the corporate’s inventory value is buying and selling at or better than a 5% premium to my projected CURRENT BV (BV as of three/31/2024; $12.20 per share), a HOLD when buying and selling at lower than a 5% premium by lower than a (7.5%) low cost to my projected CURRENT BV, and a BUY when buying and selling at or better than a (7.5%) low cost to my projected CURRENT BV.

Due to this fact, with a closing inventory value of $10.85 per frequent share as of 4/3/2024, I presently charge RITM as UNDERVALUED from a inventory value perspective.

As such, I presently imagine RITM is a BUY suggestion.

Nevertheless, to stay non-bias, I/we had a NOTABLY UNDERVALUED classification (STRONG BUY suggestion) on RITM (and a lot of the broader mREIT sector) in early 2023 which rapidly “paid off” to readers who heeded our recommendation with the current rally. So, presently some good worth with RITM however technically, sure, not as nice of worth versus early 2023.

My present value goal for RITM is roughly $12.80 per frequent share. That is presently the worth the place my suggestion would change to OVERVALUED/a SELL suggestion. The present value the place my classification/suggestion would change to APPROPRIATELY VALUED/a HOLD suggestion is roughly $11.30 per frequent share. Put one other approach, the next are my CURRENT BUY, SELL, or HOLD per share suggestion ranges:

$12.80 per share or above = SELL

$11.31 – $12.79 per share = HOLD

$9.76 – $11.30 per share = BUY

$9.75 per share or beneath = STRONG BUY

Together with the info introduced inside this text, this suggestion considers the next mREIT catalysts/elements: 1) projected future MBS/funding value actions; 2) projected future spinoff valuations; and 3) projected near-term (as much as 1-year) dividend per share charges. As mentioned earlier, this contains all current, present, and projected macroeconomic indicators and FOMC financial coverage. This additionally considers the potential RITM future spin-off of the corporate’s origination/servicing/mortgage operations.

My Private RITM Previous + Present Inventory Disclosures:

The next are my RITM (previously NRZ) previous and present inventory disclosures and complete returns since I’ve been writing on Looking for Alpha:

Desk 14 – RITM Previous + Present Inventory Disclosures/Returns

The REIT Discussion board

Supply: Taken Immediately from the REIT Discussion board’s © Spreadsheets/Information

Last Notice: All trades/investments I’ve carried out over the previous 7+ years have been disclosed to readers in “real time” (that day on the newest) by way of both the StockTalks characteristic of Looking for Alpha or, extra not too long ago, the “live chat” characteristic (which can’t be modified/altered). By way of these sources, readers can lookup all my prior disclosures (buys/sells) relating to all firms I cowl right here at Looking for Alpha (see my profile web page for a listing of all shares lined). By way of StockTalk disclosures and/or the reside chat characteristic, on the finish of March 2024 I had an unrealized/realized achieve “success rate” of 90.3% and a complete return (contains dividends obtained) success charge of 97.2% out of 72 complete previous and current mREIT and enterprise improvement firm (“BDC”) positions (up to date month-to-month; a number of purchases/gross sales in a single inventory depend as one total place till totally closed out). I encourage different Looking for Alpha contributors to supply actual time purchase and promote updates for his or her readers which might finally result in better transparency/credibility. Starting in January 2020, I transitioned all my real-time buy and sale disclosures solely to subscribers. All relevant public articles will nonetheless have my “main ticker” buy and sale disclosures (simply not real-time alerts).

Merely put, a contributor’s/staff’s suggestion monitor report ought to “count for something” and will at all times be thought of on the subject of credibility/profitable investing.

Understanding My/Our Valuation Methodology Relating to mREIT Widespread and BDC Shares:

The fundamental “premise” round my/our suggestions within the mREIT frequent and BDC sectors is worth. Relating to operational efficiency over the long-term, there are above common, common, and beneath common mREIT and BDC shares. That stated, better-performing mREIT and BDC friends may be costly to personal, in addition to being low cost. Simply because a well-performing inventory outperforms the corporate’s sector friends over the long-term, this doesn’t imply this inventory must be owned at any value. As with all inventory, there’s a value vary the place the valuation is affordable, a value the place the valuation is dear, and a value the place the valuation is suitable. The identical holds true with all mREIT frequent and BDC friends. As such, relating to my/our investing methodology, every mREIT frequent and BDC peer has their very own distinctive BUY, SELL, or HOLD suggestion vary (relative to estimated CURRENT BV/NAV). The higher-performing mREITs and BDCs usually have a suggestion vary at a premium to BV/NAV (various percentages based mostly on total outperformance) and vice versa with the common/underperforming mREITs and BDCs (usually at a reduction to estimated CURRENT BV/NAV).

Every firm’s suggestion vary is “pegged” to estimated CURRENT BV/NAV as a result of this manner readers can monitor when every mREIT and BDC peer strikes throughout the assigned suggestion ranges (every day if desired). That stated, the underlying reasoning why I/we place every mREIT and BDC suggestion vary at a special premium or (low cost) to estimated CURRENT BV/NAV relies on roughly 15-20 catalysts which embody each macroeconomic catalysts/elements and company-specific catalysts/elements (each constructive and unfavourable). This investing technique is not for all market contributors. As an illustration, not going a “good fit” for terribly passive traders. For instance, traders holding a place in a specific inventory, regardless of the worth, for say a interval of 5+ years. Nevertheless, as proven all through my articles written right here at Looking for Alpha since 2013, within the overwhelming majority of situations I’ve been capable of improve my private complete returns and/or decrease my private complete losses from particularly implementing this explicit investing valuation methodology. I hope this gives some added readability/understanding for brand new readers relating to my valuation methodology utilized within the mREIT frequent and BDC sectors.

Every investor’s BUY, SELL, or HOLD resolution relies on one’s danger tolerance, time horizon, and dividend revenue objectives. My private suggestion is not going to match every reader’s present investing technique. The factual info offered inside this text is meant to assist help readers on the subject of investing methods/selections. Please disregard any minor “cosmetic” typos if/when relevant.