photovs/iStock by way of Getty Photos

Introduction

Rockwool A/S (OTCPK:RKWBF) is a Danish firm specializing in the manufacturing of insulation, which accounts for 77% of its whole income. That was an issue in 2023 because the sharp enhance in inflation and key curiosity charges decreased the demand for insulation merchandise as fewer houses had been constructed or renovated. Apparently, the corporate’s margin widened as Rockwool reported a better EBIT on a decrease income.

The opposite 23% of the corporate’s income comes from the Techniques phase which manufactures merchandise to soundproof workplace areas; the Rockfon model produces stone wool acoustic tiles which is a reasonably good area of interest enterprise however as the primary utility for these merchandise is within the workplace renovation enterprise, this phase is hurting as nicely.

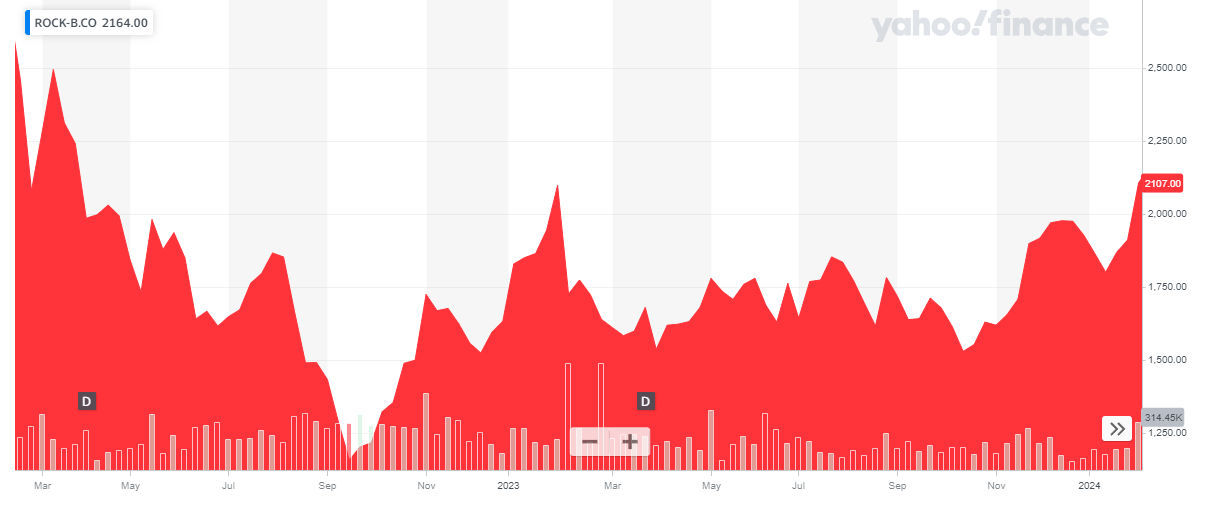

Yahoo Finance

Though Rockwool is a Danish firm with its most liquid itemizing on the Danish Inventory Alternate, it presents its monetary leads to Euro. I’ll use the Euro as base foreign money all through this text and the place relevant, I’ll convert Euros into DKK utilizing an EUR/DKK trade fee of seven.45 DKK per Euro. The ticker symbol in Denmark is ROCK-B and the common day by day quantity for Rockwool on its main trade is 35,000 shares. There are presently 21.6M shares excellent (10.8 million A-shares with 10 votes and 10.8M B-shares with one vote – the B-shares are extra liquid and that is the fairness class I’ll consult with all through this text), leading to a market cap of 46.7B DKK which is roughly 6.3B EUR.

Sadly, the corporate’s web site accommodates fairly a couple of ‘obtain solely’ hyperlinks, however you will discover all related data I’ll consult with on this page.

A slowdown within the development market weighs on the outlook

Rockwool’s monetary outcomes for FY 2023 had been a combined bag. On the one hand, the income was hit by the slowdown in development and renovation actions all through the world however that did not actually matter as the corporate’s EBIT and EBIT margin elevated sharply because of decrease power costs.

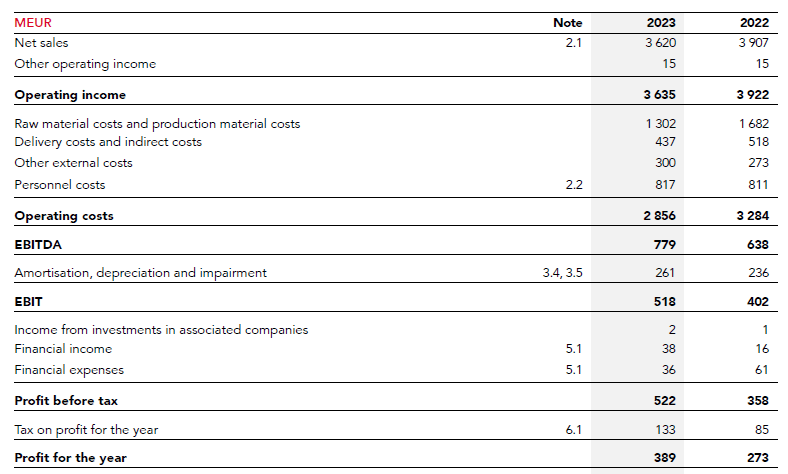

Because the revenue assertion under signifies, Rockwool reported a total revenue of 3.64B EUR which is a 7% lower in comparison with the earlier monetary yr. However there is not any want to fret because the uncooked materials prices decreased by in extra of 20% whereas the supply prices fell by virtually 16% to 437M DKK. The whole quantity of working prices decreased by a surprising 13% and this resulted in an EBITDA of 779M EUR which represents a 22% enhance in comparison with FY 2022. That is why I do not significantly thoughts the decrease income; there’ll all the time be volatility within the firm’s numbers as some years shall be higher than others. However so long as Rockwool is ready to shield its margins, I am not too apprehensive.

Rockwool Investor Relations

Though the depreciation and amortization bills elevated by roughly 10%, the EBIT nonetheless jumped by virtually 30%. And with a internet finance revenue of 4M EUR in comparison with a 44M EUR internet expense in FY 2022, Rockwool was additionally capable of profit from this to put up a pre-tax revenue of 522M EUR and a internet revenue of 389M EUR. This represents an EPS of 18 EUR per share which is a rise of virtually 42% in comparison with the EPS end in 2022.

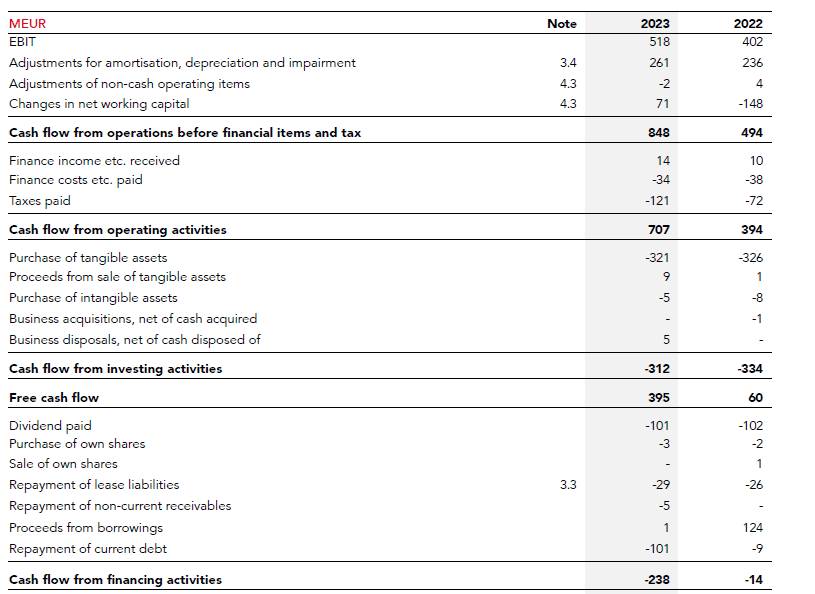

Apparently, Rockwool continues to spend money on growth. Because the money stream assertion under exhibits, the corporate spent about 350M EUR on capex and lease funds though its whole depreciation and amortization bills had been simply 261M EUR.

The reported working money stream was 707M EUR however this features a 71M EUR working capital launch. After deducting that 71M EUR once more, and after deducting the 29M EUR in lease funds, the adjusted working money stream was 607M EUR. And in the event you’d additionally use the quantity of taxes owed quite than the money taxes paid, the underlying working money stream was 595M EUR.

Rockwool Investor Relations

The whole capex was 321M EUR which leads to a internet free money stream of 274M EUR. Divided over the 21.6M shares which are presently excellent, the web free money stream was 12.7 EUR per share. That is just below 95 DKK per share.

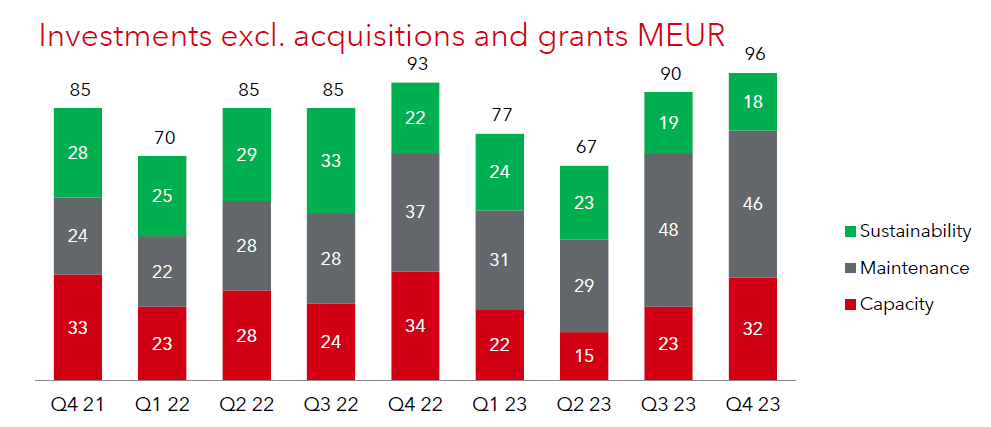

If we might look into the capital expenditures in additional element, we see the full sustaining capex was simply 154M EUR. The corporate additionally spent 84M EUR on sustainability and 92M EUR on capability growth. If we might assume the investments in sustainability are additionally ‘sustaining’ capital expenditures, the full capex excluding capability growth was 228M EUR. Making use of this to the aforementioned adjusted working money stream calculation leads to a internet free money stream of 367M EUR or 17 EUR per share.

Rockwool Investor Relations

We may additionally argue that not the entire sustainability investments must be counted as upkeep capex. In accordance with Rockwool, the vast majority of the sustainability capex is expounded to the preparation for the electrification of a French plant and the set up of {an electrical} melter in Switzerland. These are all non-recurring gadgets and investments so maybe they should not be seen as ‘pure’ sustaining capex.

Because of the robust money flows, Rockwool presently has a internet money place of virtually 240M EUR. This implies the recently announced share buyback program to the tune of 160M EUR is totally funded by the prevailing money place whereas the incoming money stream within the present monetary yr will clearly additionally assist. Rockwool will solely be repurchasing the B Shares which carry one vote every.

Rockwool can be proposing to pay a dividend of 43DKK per share which represents roughly 5.8 EUR. The dividends are topic to the usual Danish dividend withholding tax of 27%.

For the present monetary yr, Rockwool is anticipating a steady income in native currencies with an EBIT margin of ’round 13%’. That is considerably disappointing in comparison with the 2023 EBIT margin of simply over 14% however the 13% EBIT margin is de facto simply reversing to the imply because the margin was very constantly 13-13.5% within the 2019-2021 period. Additionally it is fully attainable the Rockwool administration is quite cautious given the relatively limited visibility within the first half of the present monetary yr. And may the scenario enhance, we will probably anticipate a steerage hike.

Funding thesis

Utilizing the EBIT margin steerage and a 1% income enhance, the EBIT will probably lower by roughly 43M EUR. Making use of a mean tax fee of 25%, the web revenue and internet free money stream could be hit by roughly 32M EUR or 1.50 EUR per share, leading to an anticipated EPS of 16.5 EUR per share. This is able to additionally point out the sustaining free money stream (excluding development and excluding sustainability investments) could be roughly 20 EUR per share. That is roughly 150 DKK on the present trade fee which implies Rockwool is presently buying and selling at an underlying free money stream yield of 6.9% which actually is not dangerous in any respect.

That is comparatively engaging contemplating I anticipate the demand for insulation merchandise to proceed to extend. And though 2024 could also be a troublesome yr because of the prohibitive rate of interest surroundings, I anticipate Rockwool to have the ability to present a income and EBIT enhance from 2025 on once more. In the meantime, the share repurchase program will assist to enhance the efficiency on a per-share foundation though I hope the corporate shall be selective when it buys again inventory and aggressively repurchases shares on weak moments.

I presently don’t have any place in Rockwool, however my curiosity within the firm and inventory has now been triggered. I’ll for certain regulate this firm.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.