onurdongel/E+ by way of Getty Photos

After a troublesome multi-year interval, Roku, Inc.’s (NASDAQ:ROKU) progress and profitability are starting to bounce again. It is troublesome to get excited concerning the firm’s rapid prospects although as Roku is at the moment spending rather a lot to develop a little bit. A few of this has been the results of a post-pandemic hangover, however the aggressive surroundings additionally seems to be robust.

I previously suggested that Roku’s low valuation and bettering fundamentals ought to assist the inventory transfer greater within the coming quarters. I additionally felt that competitors considerations and advert market weak point would most likely restrict positive aspects. The inventory is down almost 30% since then on the again of sentimental This fall outcomes.

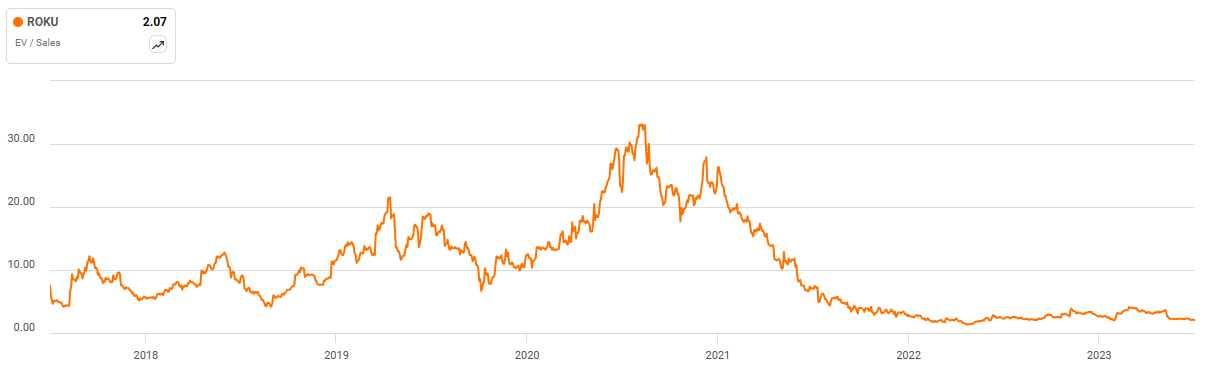

Roku’s income a number of stays close to all-time lows regardless of the corporate’s platform now dominating income and supporting long-term progress and profitability. The inventory is prone to re-rate considerably greater when Roku returns to profitability and constantly sturdy progress, however this might nonetheless be a number of years away.

Market Situations

Video promoting reportedly rebounded in the fourth quarter, serving to to offset weak M&E spend. This power is anticipated to persist into the primary quarter. CPG, well being and wellness, and telecom have been areas of power, whereas classes like monetary providers and insurance coverage are nonetheless comparatively weak. This seems to be a reasonably broad-based enchancment, with Magnite, Inc. (MGNI) and PubMatic, Inc. (PUBM) each anticipating greater CTV progress going ahead.

The variety of ad-supported streaming providers is rising, Which Roku believes will speed up the shift of advert {dollars} from linear TV to streaming. Roku can capitalize on this by serving to streaming providers to develop engagement. Within the close to time period, nonetheless, it will possible result in continued stress on CPMs.

A mixture of sentimental advertiser demand and stable provide progress has pressured pricing lately. Provide progress is coming from a mix of recent streaming providers, extra ad-supported tiers, and an elevated variety of adverts per hour. The launch of adverts on Prime Video additionally will possible influence pricing in 2024 because it has 115 million monthly users within the US. Pricing headwinds ought to start to abate in 2025 although as stock progress begins to normalize and advert spend continues to shift to CTV.

Roughly 60% of viewing hours at the moment are on streaming and but solely round 30% of advert spend is on CTV. It is a massive hole which can possible finally shut, however advertisers want to alter spending habits and advert tech corporations must reveal ROAS. This shift continues unabated as properly. Conventional TV hours declined 16% YoY in This fall whereas streaming hours on the Roku platform have been up 21%.

The market has additionally lately been shaken up by Walmart Inc.’s (WMT) deliberate 2.3 billion USD acquisition of VIZIO Holding Corp. (VZIO). Vizio is considerably of a fringe participant out there, with solely round 18 million energetic accounts, nevertheless it has strategic worth to Walmart. The acquisition ought to help the corporate’s promoting enterprise, which is reportedly producing round $3 billion in gross sales and rising at a double-digit tempo. Whereas this growth actually is not optimistic for Roku, because it might influence {hardware} gross sales and person acquisition, the corporate’s place out there could also be sturdy sufficient that it’s not overly impacted. The deal additionally nonetheless wants regulatory approval and can possible obtain shut scrutiny given Walmart’s dimension. It is troublesome to see a stable motive why the deal ought to be blocked from a contest perspective, although.

Roku is the dominant participant within the US market, accounting for nearly 40% of CTV advert impressions, with opponents pretty even at a lot decrease market shares. Amazon.com, Inc. (AMZN), Samsung Electronics Co., Ltd. (OTCPK:SSNLF) and Alphabet Inc. (GOOG) (GOOGL) are also vital gamers out there, and every has strategic pursuits past simply the CTV market.

Roku Enterprise Updates

There have not been any main updates to Roku’s enterprise in latest quarters, which might be a optimistic after a sequence of technique adjustments lately. Roku’s focus is shifting from cost-cutting to progress, which is considerably odd on condition that the corporate’s losses stay elevated largely as a result of progress investments.

Product innovation might be focused at bettering monetization of Roku’s management over the house display for 80 million energetic accounts globally. The quantity of streaming content material continues to extend, and Roku believes that it might probably assist its customers navigate this content material. Roku additionally will help corporations construct new experiences which are entertaining and interact viewers, serving to them to resolve which app to run. Whereas there’s potential so as to add worth for each customers and publishers, Roku is dealing with M&E spending headwinds within the close to time period.

Roku lately expanded its TV lineup by introducing the Roku Professional Sequence, which is focused on the high-end of the market. The Professional Sequence presents superior options, like a 4K QLED show and enhanced audio know-how.

Roku can be increasing the distribution of its Roku-branded TVs, from Greatest Purchase to Costco and Amazon, which might create channel conflicts. Roku-branded TVs are nonetheless thought of complementary to current applications, although. Roku TVs are being positioned as a means for Roku to innovate in each {hardware} and software program and share enhancements with licensing companions. Given the competitors Roku faces from corporations like Samsung and the specter of competing working programs undermining its partnerships, there’s additionally possible a defensive factor to the transfer.

Regardless of the launch of Roku-branded TVs and sensible house gadgets, Roku’s system gross sales stay comparatively mushy. I view this enterprise as a loss chief designed to assist the corporate purchase platform customers, so this solely actually issues to the extent that it impacts account progress.

Monetary Evaluation

Roku’s income was 984 million USD within the fourth quarter, up 14% YoY. Platform income elevated 13% to 829 million USD, pushed by each streaming providers distribution and video promoting actions, offset by M&E. Streaming providers distribution actions outpaced platform progress, benefiting from elevated subscription sign-ups and SVOD value will increase. Gadgets income elevated 15% YoY within the fourth quarter, pushed by Roku branded TVs.

Roku expects 850 million USD in income within the first quarter, which might symbolize roughly a 15% enhance YoY. Whereas this can be a stable progress price, Roku’s platform enterprise remains to be dealing with M&E headwinds. Political promoting ought to be a tailwind in 2024, however it’s a comparatively small contributor to Roku’s enterprise.

Determine 1: Roku Income (Supply: Created by creator utilizing information from Roku)

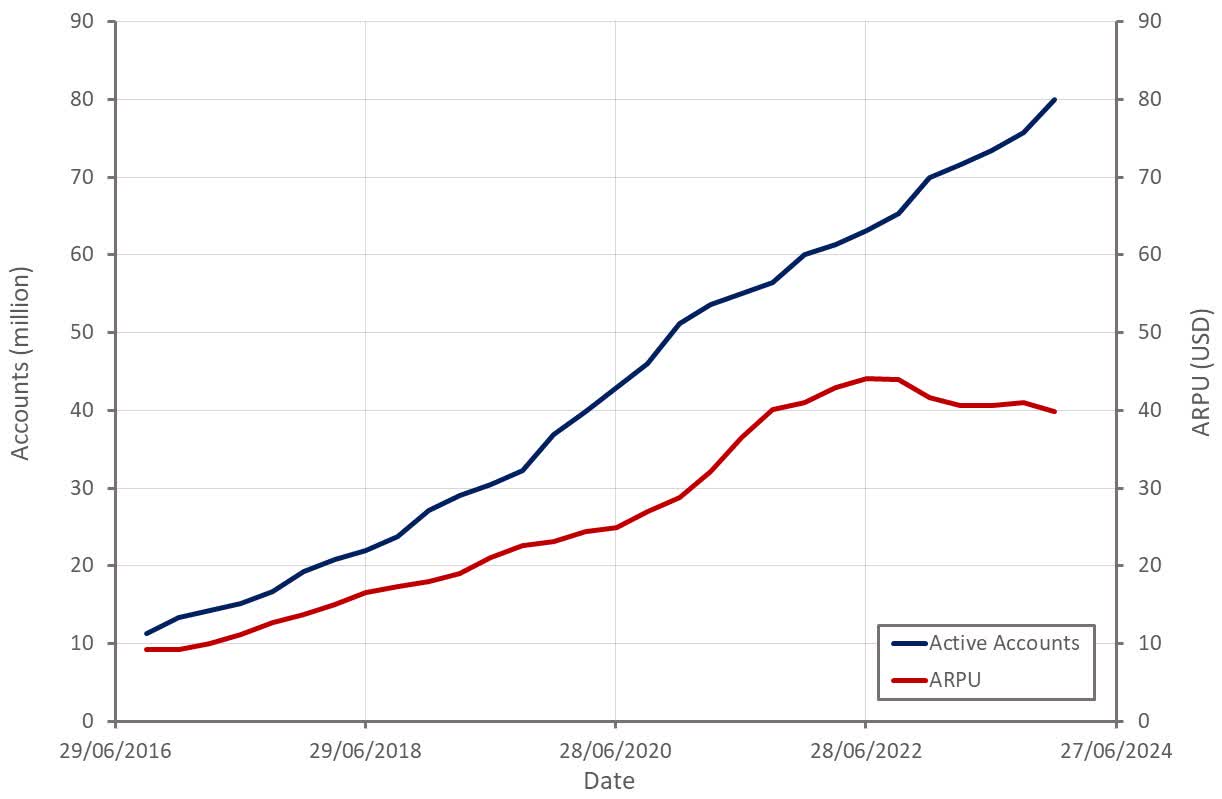

Full-year internet energetic account progress was around 10 million, above 2019 ranges and just like 2022. Roku attributed this to its Roku TV program within the US and worldwide enlargement. Account progress got here regardless of total TV unit gross sales within the US declining YoY in This fall, which was attributed to higher LCD panel prices to greater costs for shoppers.

Engagement additionally continues to extend with common streaming hours per energetic account up roughly 8% YoY. Common hours per account per day remains to be solely 4.1 although, considerably trailing the 7.5 hours per day of conventional TV viewing time within the US.

Roku’s common income per person is being pressured by speedy worldwide account progress, with ARPU within the US nonetheless typically rising. Counterintuitively, I consider that declining ARPU is a optimistic, offered that it is coupled with sturdy account progress, as that is indicative of stable worldwide enlargement.

Determine 2: Roku Energetic Accounts (Supply: Created by creator utilizing information from Roku)

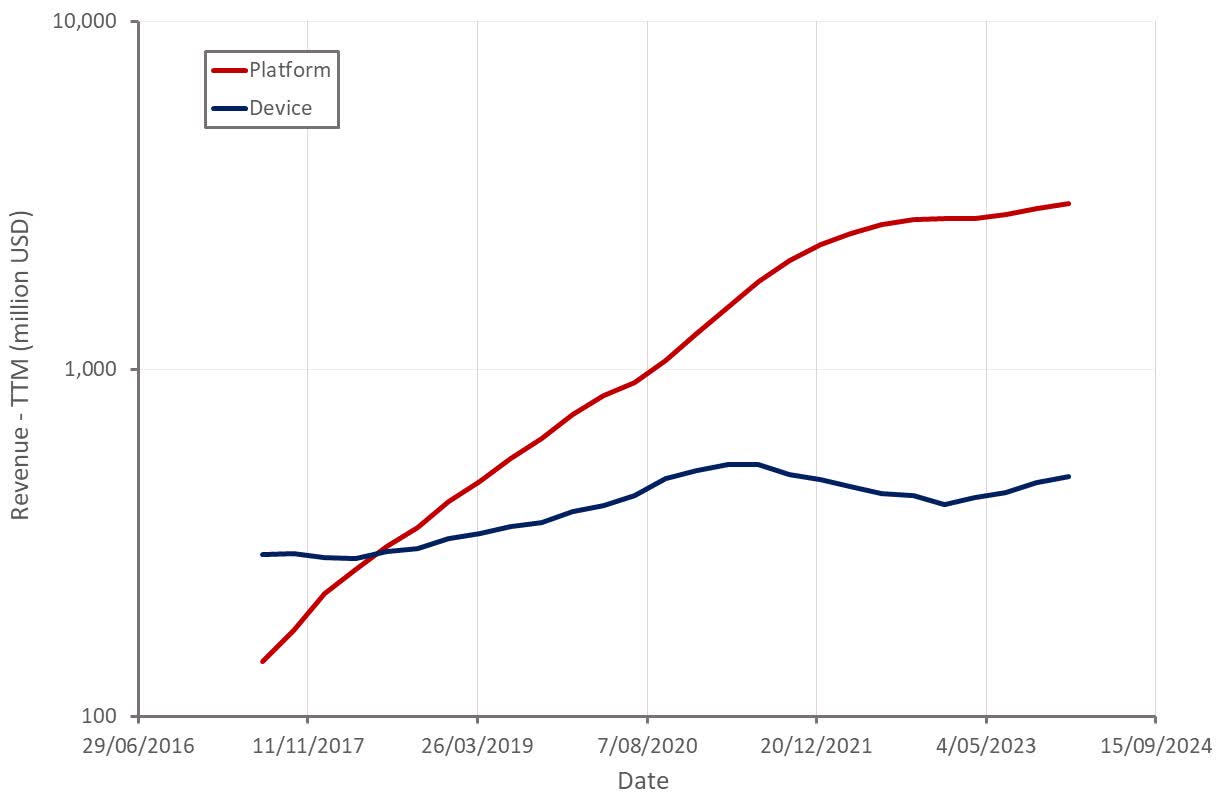

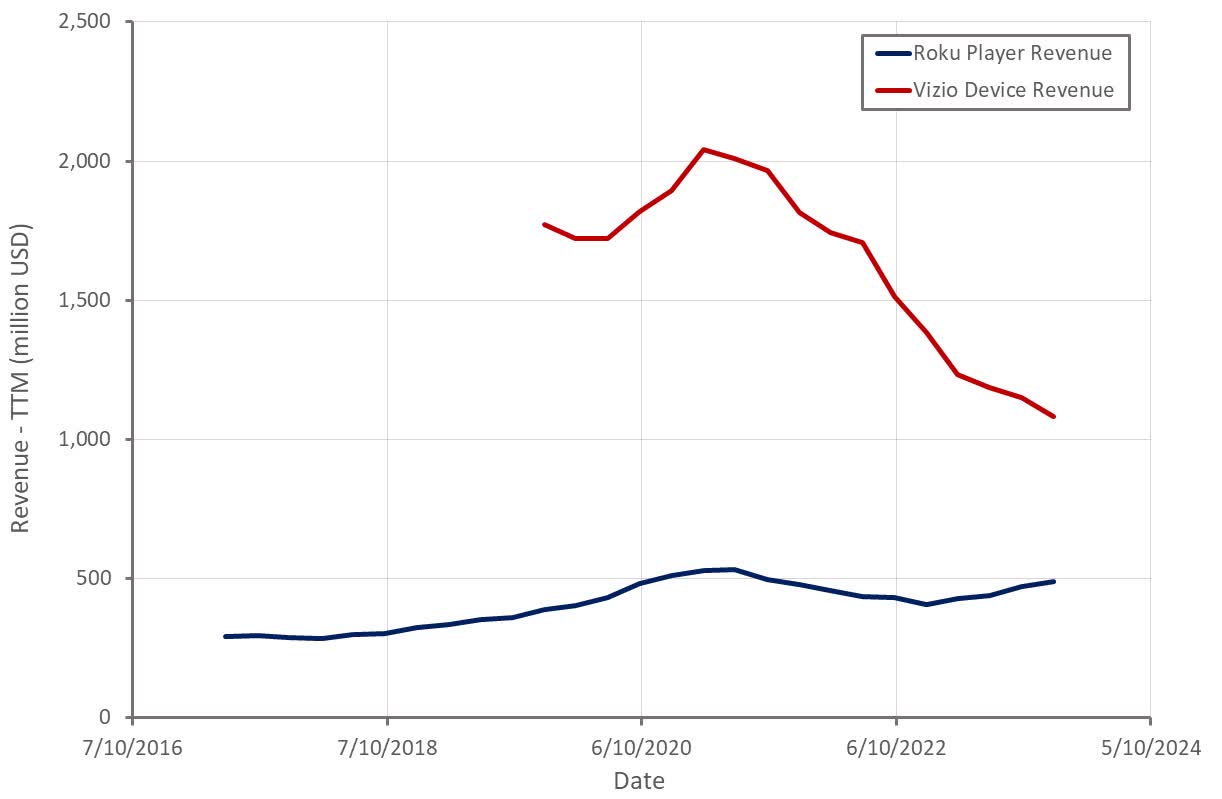

Whereas the efficiency of Roku’s participant enterprise has been mushy, it really seems fairly sturdy compared to Vizio’s enterprise. It ought to be famous that system gross sales are being boosted by the launch of Roku-branded TVs and sensible house gadgets.

Determine 3: Roku Participant Income (Supply: Created by creator utilizing information from firm studies)

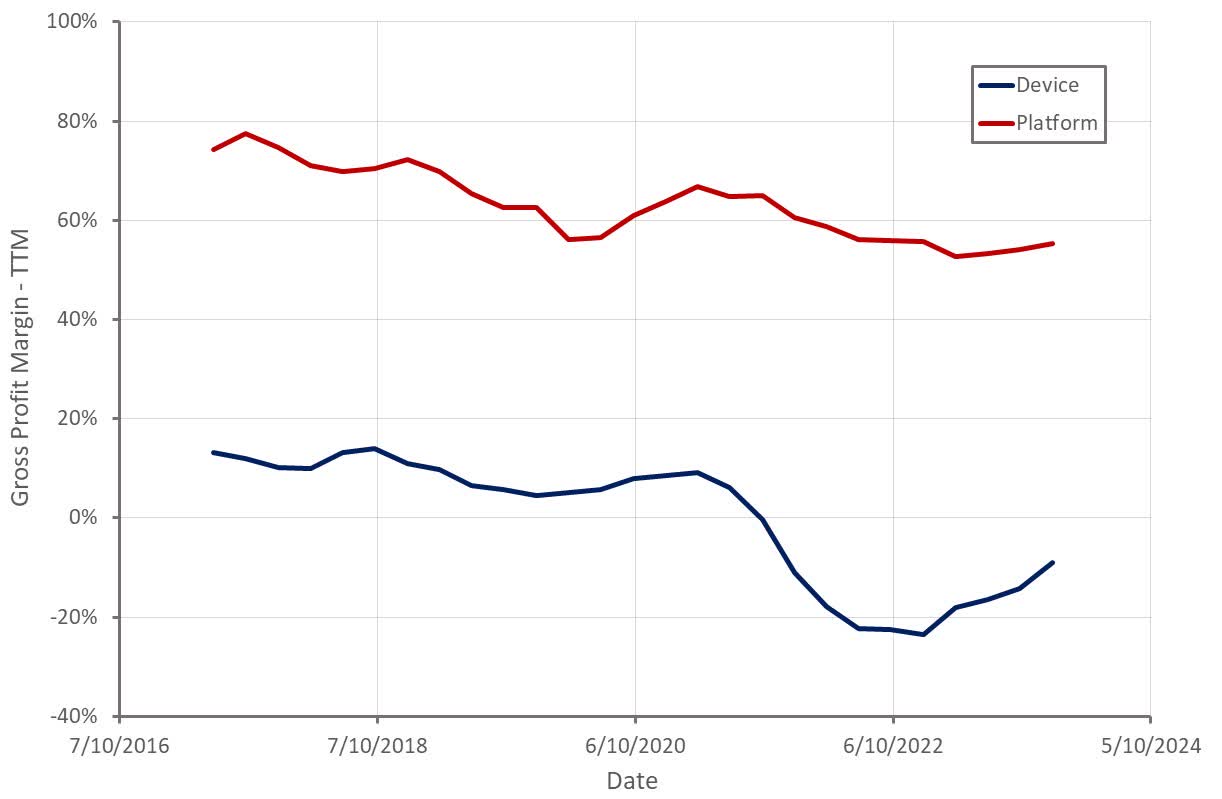

Roku’s gross revenue margins stay depressed though have begun to bounce again in latest quarters. Whereas system margins have been impacted by provide chain points, latest headwinds have possible been pushed by discounting.

Platform margins are being impacted by a mix of:

- Much less excessive margin M&E income.

- Worldwide enlargement.

- Decrease CPMs.

Total gross revenue margin is being supported by the expansion of the platform enterprise relative to system gross sales, although.

Determine 4: Roku Gross Revenue Margins (Supply: Created by creator utilizing information from Roku) Determine 5: Roku Platform Gross Revenue Margin (Supply: Created by creator utilizing information from Roku)

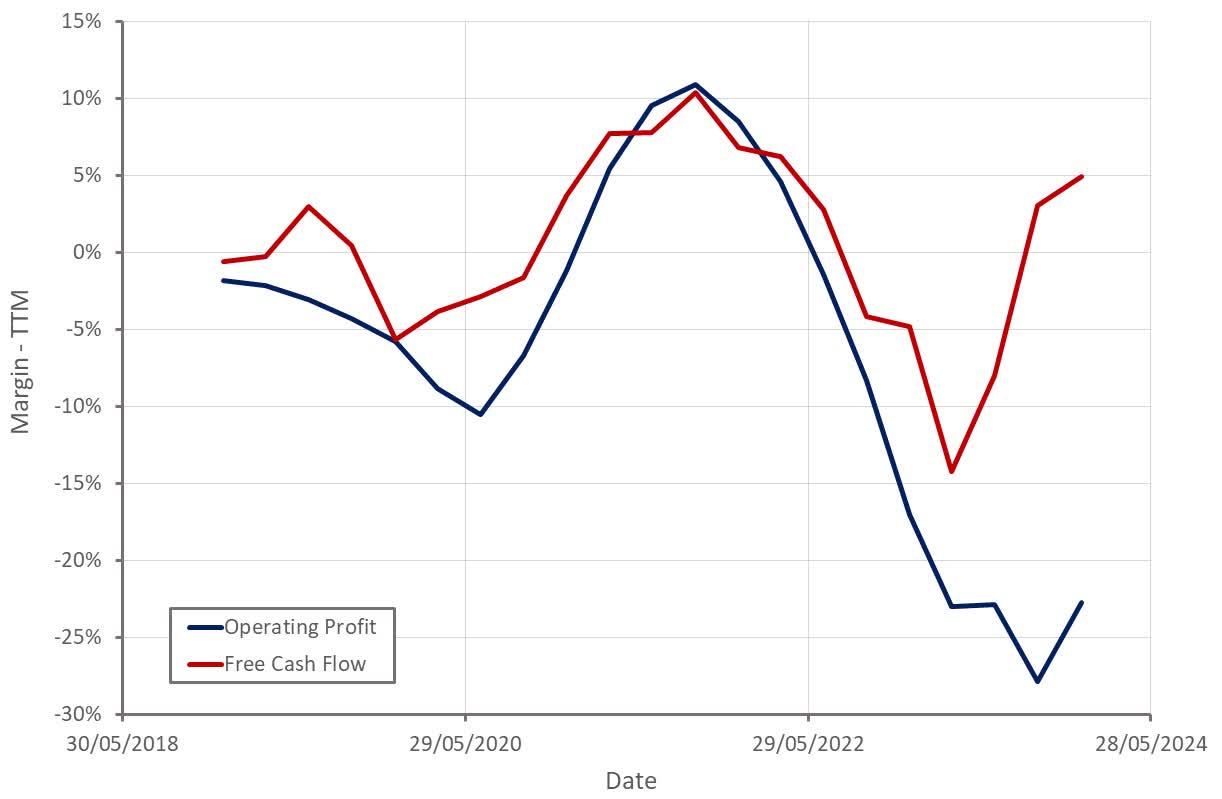

Roku’s margins and money flows have been bettering on the again of cost-cutting efforts and platform income progress, with the corporate reaching optimistic adjusted EBITDA and free money circulate in 2023.

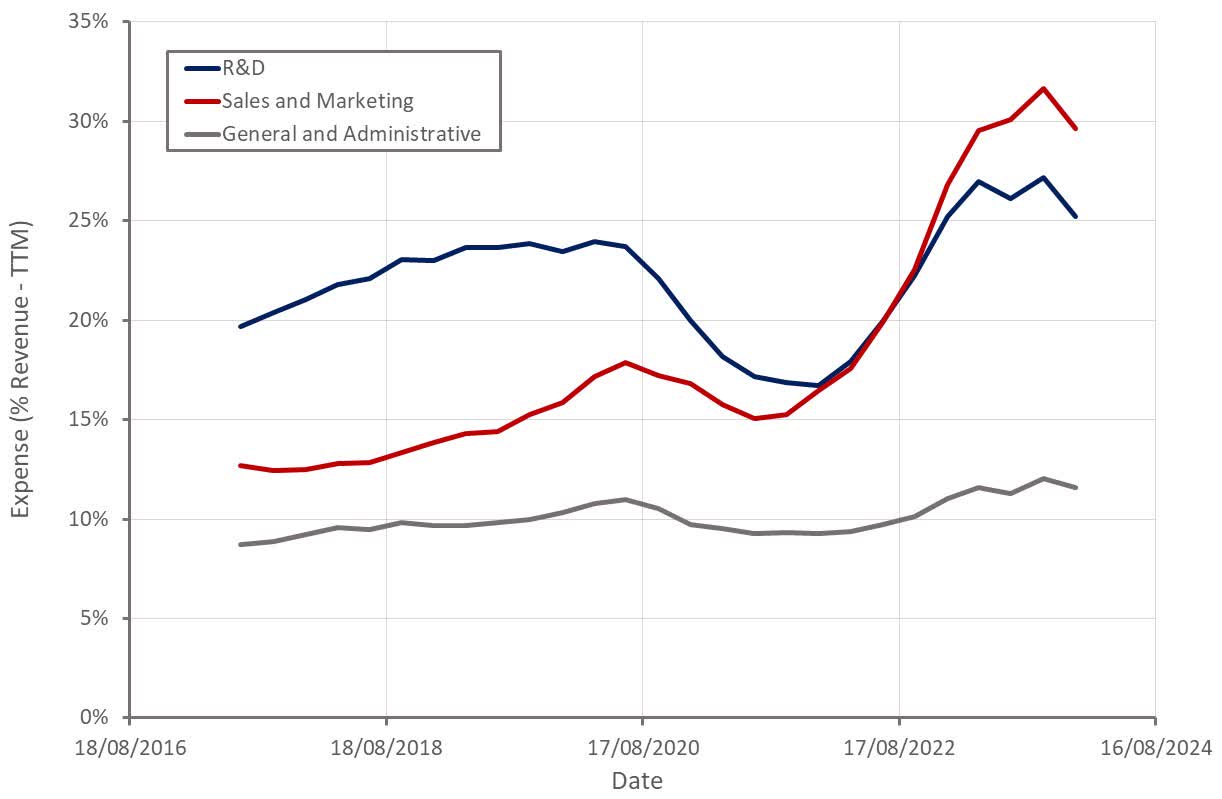

GAAP working losses are nonetheless elevated, though Roku incurred a 42 million USD one-time cost in This fall, primarily associated to lease impairments and workforce reductions. Working bills are anticipated to say no by a low to mid-teen share YoY in Q1. Gross sales and advertising bills are significantly regarding given the corporate’s weak progress.

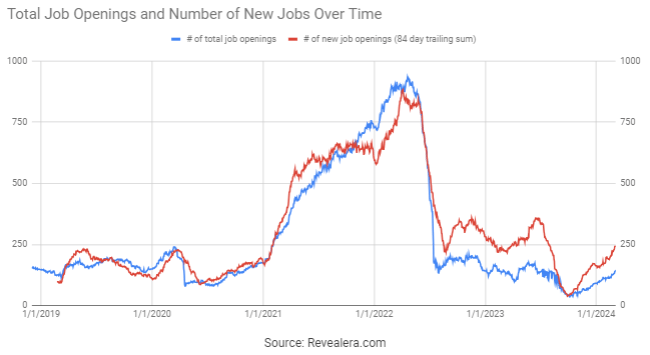

Determine 6: Roku Free Money Move (Supply: Created by creator utilizing information from Roku) Determine 7: Roku Working Bills (Supply: Created by creator utilizing information from Roku) Determine 8: Roku Job Openings (Supply: Revealera.com)

Conclusion

Roku’s valuation stays close to all-time lows, which, I consider, is tough to justify based mostly on fundamentals. Whereas progress is at the moment mushy and the corporate nonetheless is not worthwhile, this example does not mirror Roku’s transition from commodity {hardware} to an promoting platform and media enterprise. Progress and margins ought to enhance within the coming quarters, significantly if CPMs stabilize. Roku’s income a number of is prone to broaden meaningfully sooner or later, however the firm may have to realize GAAP profitability first, and this might nonetheless be a number of years away.

Competitors stays a problem although, significantly internationally, the place Roku is a comparatively late mover. Roku’s enterprise can be pretty inefficient in the intervening time, with the corporate investing a big quantity in R&D, gross sales, and advertising, and product reductions and having little to point out for it.

Determine 9: Roku EV/S A number of (Supply: Looking for Alpha)

![[Watch] CM Punk arrives on WWE RAW](https://whizbuddy.com/wp-content/uploads/2024/01/d0a3d-17047585137093-1920-600x600.jpg)