Adam Gault

Comparatively just lately, I issued a bullish article on one of many actual property centered Cohen & Steers closed finish funds – Cohen & Steers Whole Return Realty (NYSE:RFI).

Within the article, I outlined how the deal with excessive high quality REITs and their mounted revenue in addition to most popular share securities ought to warrant an honest upside potential, whereas offering juicy streams of present revenue.

Additionally, within the article I contextualized RFI with a carefully associated CEF: Cohen & Steers REIT & Most popular Earnings Fund (NYSE:RNP). RNP successfully carries a really related publicity to that of RFI, and the one materials distinction lies in the truth that RNP depends closely on exterior leverage to enlarge the underlying yield potential. Due to this and the upper for longer backdrop, I made a decision to downgrade RNP, which has since then misplaced circa 8% of its share value.

Now, the query is whether or not the Cohen & Steers High quality Earnings Realty Fund (NYSE:RQI) displays an analogous danger profile to RNP that will in flip justify a extra conservative stance from the investor facet.

Thesis evaluate

My newest piece on RQI was circulated again in December 2023, the place the general message was relatively constructive because of the duration-loaded issue, which underneath a state of affairs of rate of interest cuts ought to elevate the inventory value considerably increased from the current ranges.

It’s not a shock that the Fund has registered disagreeable returns (~ 3% drop) because the consensus pertaining to the variety of hikes has clearly modified, assuming a stronger increased for longer state of affairs.

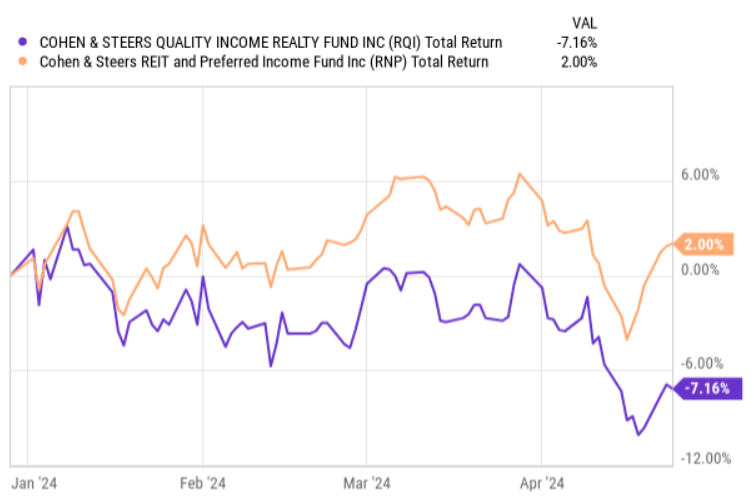

Apparently, if we take a look at the chart beneath, we will discover that RQI has truly massively underperformed RNP regardless of having virtually an identical portfolio allocations.

Ycharts

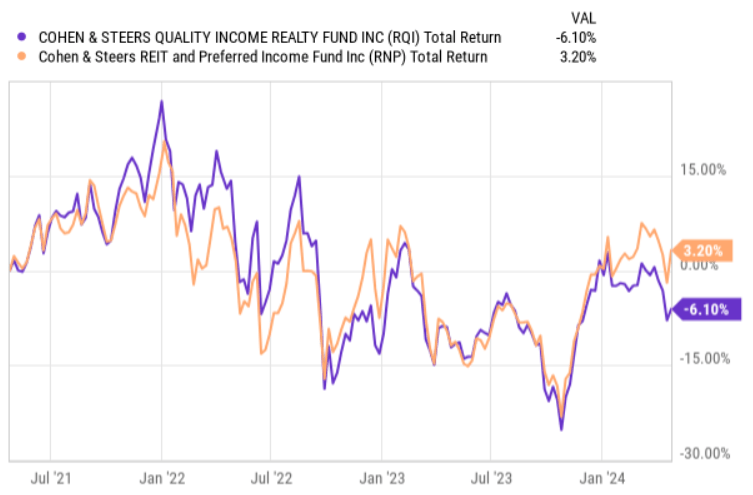

Furthermore, the next chart helps additional seize the essence right here:

Ycharts

Specifically, zooming again to a historic 3-year interval, we will observe how tightly correlated each of those names have been and likewise that there have been a number of cases by which, say, RNP briefly exceeds RQI after which after a comparatively brief interval the connection returns to a stability (oftentimes the opposite Fund taking the lead function within the subsequent second of deviation).

So, theoretically, one may argue that the YTD return dynamic is a short lived factor that may ultimately smoothen out. In my view, there’s a undoubtedly a component of reality on this, but when we peel again the onion a bit and take a extra cautious take a look at RQI’s asset allocation combine, we rapidly perceive why RQI has been at the least to some extent punished accurately by the market.

The important thing distinction is basically the portion of property which have been positioned into mounted revenue like securities, the place in RQI’s case the share quantities to 19% of the NAV, whereas for RNP the related phase consumes 48% of the portfolio.

Within the context of upper for longer and the looming recessionary dangers, the market has clearly favored allocations and revenue streams, which exhibit stronger defensive traits and carry a restricted danger of registering a discount in distributions.

But, the important thing difficulty with RQI is an identical to RNP’s state of affairs, the place the dangers which are related to the exterior leverage render the car overly speculative and depending on a well timed discount within the rates of interest.

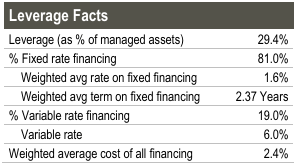

Cohen & Steers

The desk above reveals how RQI is presently benefiting from a sound hedging technique and the reliance on mounted fee borrowings. In different phrases, as of now, RQI has 81% of its whole leverage stipulated towards mounted fee financing, which sits at 1.6%, whereas the market-level fee is nearer to six% as we will infer it from the above mirrored variable fee financing fee. This can be a notable benefit, permitting RQI to capitalize on spreads between the price of financing and portfolio yield ranges which have risen because the rates of interest have gone up.

Nevertheless, this desk additionally signifies a danger that may ultimately materialize as soon as RQI is compelled to refinance or roll over the hedges on its 1.6% mounted fee element. Granted, the rates of interest would possibly go down by the point the debt maturity wall kick in, however it’s extremely unlikely that RQI will handle to maintain the rate of interest so depressed as it’s now.

In truth, taking a look at FOMC dot plot, the consensus signifies that in ~ 2 years from now (which largely corresponds to the time RQI must refinance) the SOFR will revolve round 3.1%. In RQI’s case we’ve so as to add some credit score danger premium on prime of this, which ends up in at the least doubling of the prevailing mounted fee financing fee.

With that being stated, buyers must be cognizant of the chance that the rates of interest keep this excessive for longer than what’s baked into the FOMC projections.

The underside line

All in all, I nonetheless stay bullish on the underlying fundamentals of RQI simply as for RNP and RFI, the place, in my view, an publicity to top quality fairness REITs will ultimately generate outsized returns because the rates of interest start to fall a bit.

Nevertheless, the chance that stems from RQI’s leverage profile introduces simply an excessive amount of of a dependence on the rate of interest path, which is inherently unimaginable to foretell, particularly if we glance again on the revisions (and deviations from consensus) prior to now couple of quarters. In case the rates of interest keep this excessive for the following 2-3 years, RQI’s value of financing would skyrocket, which, given the truth that ~30% of the AuM is accommodated by debt, wouldn’t solely shrink the money era, but additionally power the Fund to even revisit its present dividend in my view.

Due to this, I’m downgrading the Cohen & Steers High quality Earnings Realty Fund (RQI) to carry.