AlexSecret

We beforehand coated RTX Corporation (NYSE:RTX) in September 2023, discussing its combined prospects, due to the extra $3B pre-tax influence from the Pratt & Whitney powder metallic challenge previous to the FQ3’23 earnings name.

With the inventory plunging then, we had advisable an entry level of $70s for an improved margin of security and expanded ahead dividend yield, with it nonetheless being a viable dividend play because the Looking for Alpha Quant rated the inventory’s dividend security at B+.

On this article, we will focus on why the RTX inventory’s discounted valuations stay a present for value-oriented traders, on account of its rising backlog over the subsequent 15 years, due to the strong industrial and protection spending traits over the subsequent few quarters.

This enables the administration to maintain its (potential) dual-pronged returns via capital appreciation and dividend revenue, triggering our Purchase score right here.

The Defensive RTX Funding Thesis Stays Sturdy Right here

For now, RTX has reported a double beat FQ3’23 earnings call, with adj revenues of $18.95B (+3.4% QoQ/+11.7% YoY) and adj EPS of $1.25 (-3.1% QoQ/+3.3% YoY) in October 2023, with the previous adjusted upward for a $5.4B cost associated to the beforehand disclosed Pratt powder metallic defect.

Regardless of the noise surrounding the defect, the administration continues to report a rising backlog of $190B (+2.7% QoQ/+13% YoY), with $115B comprising industrial aerospace contracts (+2.6% QoQ/+13.8% YoY) and $75B comprising protection contracts (+2.7% QoQ/+11.9% YoY).

These numbers suggest that RTX’s prime line is just about set for the subsequent decade since as much as 45% of its backlog spans over the next 15 years.

In consequence, we imagine that the powder metallic defect is probably going temporal regardless of the noise surrounding the additional regulatory inspections, with many of the accelerated upkeep inspection headwinds seemingly baked in already.

If something, readers can also need to notice the a number of army conflicts occurring globally, which is able to seemingly drive demand for RTX’s defense offerings, constructing upon its long-term backlog.

A part of the enhance is attributed to the US authorities restock of supplies shipped to Ukraine and the precautionary armament in Europe, with issues prone to additional elevate with the continued Israel-Gaza battle.

That is why RTX’s army gross sales have been rising YTD to $27.01B (+3.5% YoY), with a near-term tailwind forward, attributed to the latest announcement of a $250M military package to Ukraine on December 27, 2023.

Whereas it stays to be seen if the $106B worth of funding could also be ultimately accredited, we imagine that protection spending might be elevated till a everlasting cease-fire is achieved.

Moreover, readers should notice that RTX operates within the industrial sector, with YTD adj revenues of $27.38B (+19.6% YoY), with the spectacular progress attributed to the normalizing industrial journey pattern post-pandemic.

Market analysts from AITA already anticipate the industrial airline business to outperform in 2024, primarily based on the projected revenues of $964B (+7.6% YoY) and web earnings of $25.7B (+10.3% YoY), with as much as 4.7B passengers anticipated, properly exceeding 2019 ranges of 4.5B.

On account of these promising developments, it’s unsurprising that RTX already reported glorious progress in its YTD general adj gross sales to $19.19B (+14% YoY), with a reasonably increasing working margin of 10.7% (+1 level YoY).

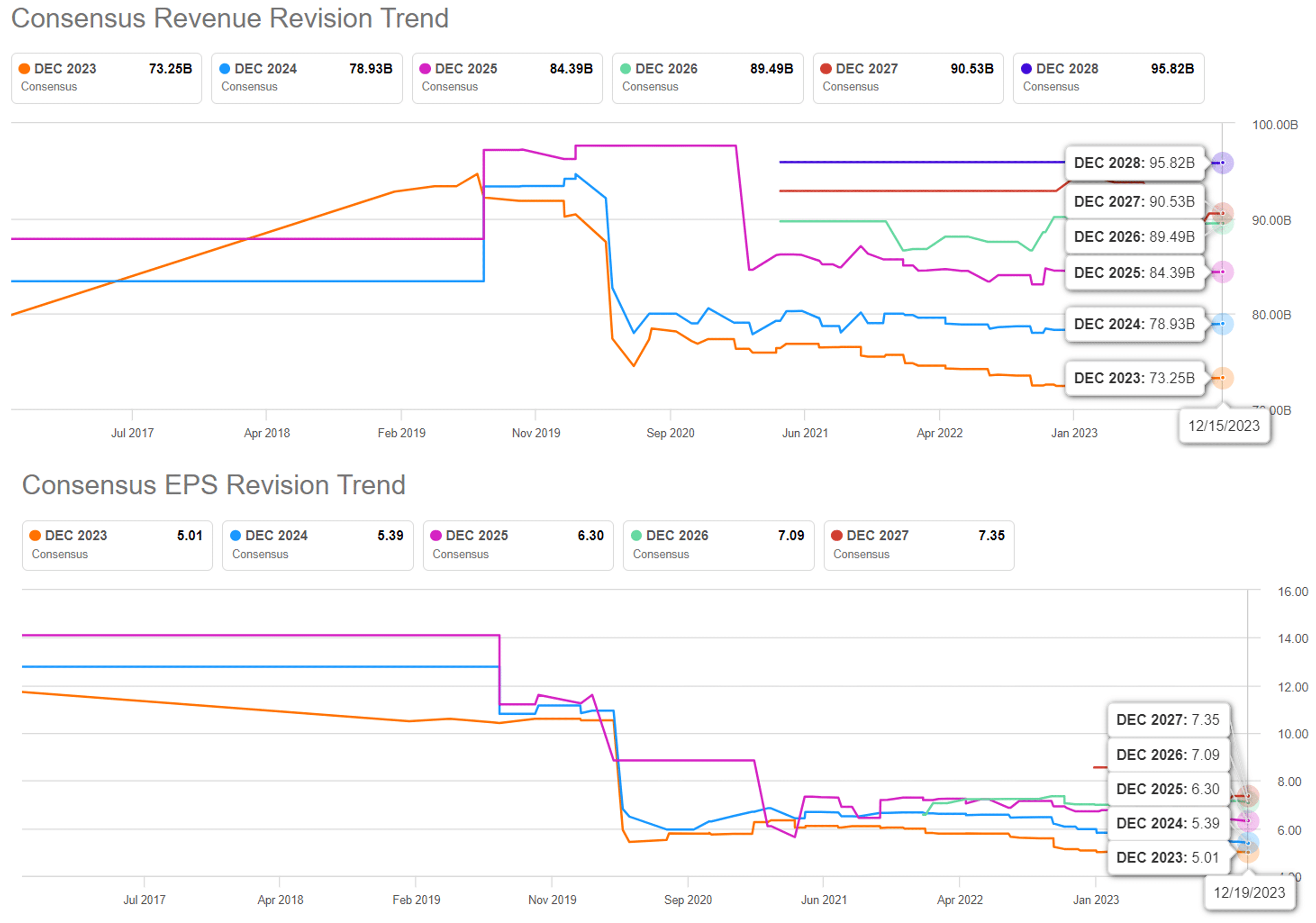

The Consensus Ahead Estimates

Looking for Alpha

The identical optimism has been estimated by the consensus, with RTX anticipated to generate a prime and backside line CAGR of +8% and +9.6% via FY2025.

That is considerably much like the earlier estimates of +8%/+11.97% whereas constructing upon the sustained progress at a historic CAGR of +2.8%/+16.9% between FY2020 and FY2022, respectively.

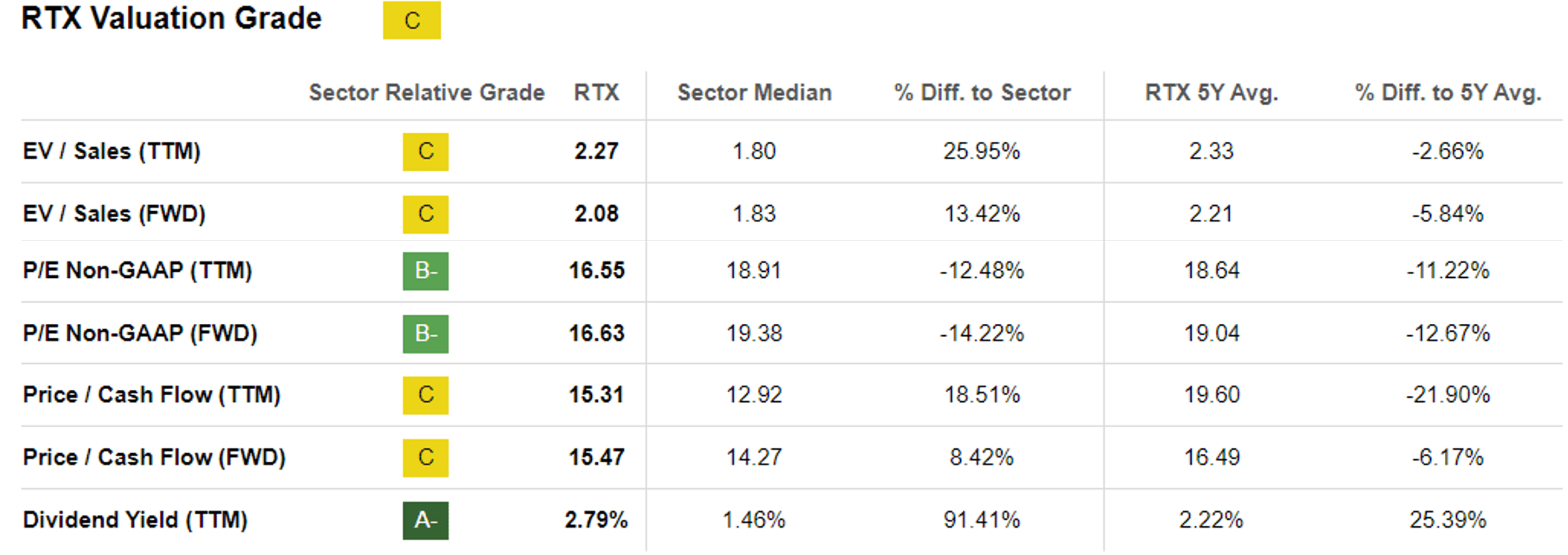

RTX Valuations

Looking for Alpha

RTX’s prospects have been notably discounted certainly, regardless of the considerably constant ahead consensus estimates as mentioned above, attributed to the impacted FWD P/E valuation of 16.63x and FWD Value/Money Movement valuation of 15.47x.

That is in comparison with its 1Y imply of 17.70x/20x, 3Y pre-pandemic imply of 17.73x/20x, and the sector median of 19.38x/14.27x, respectively.

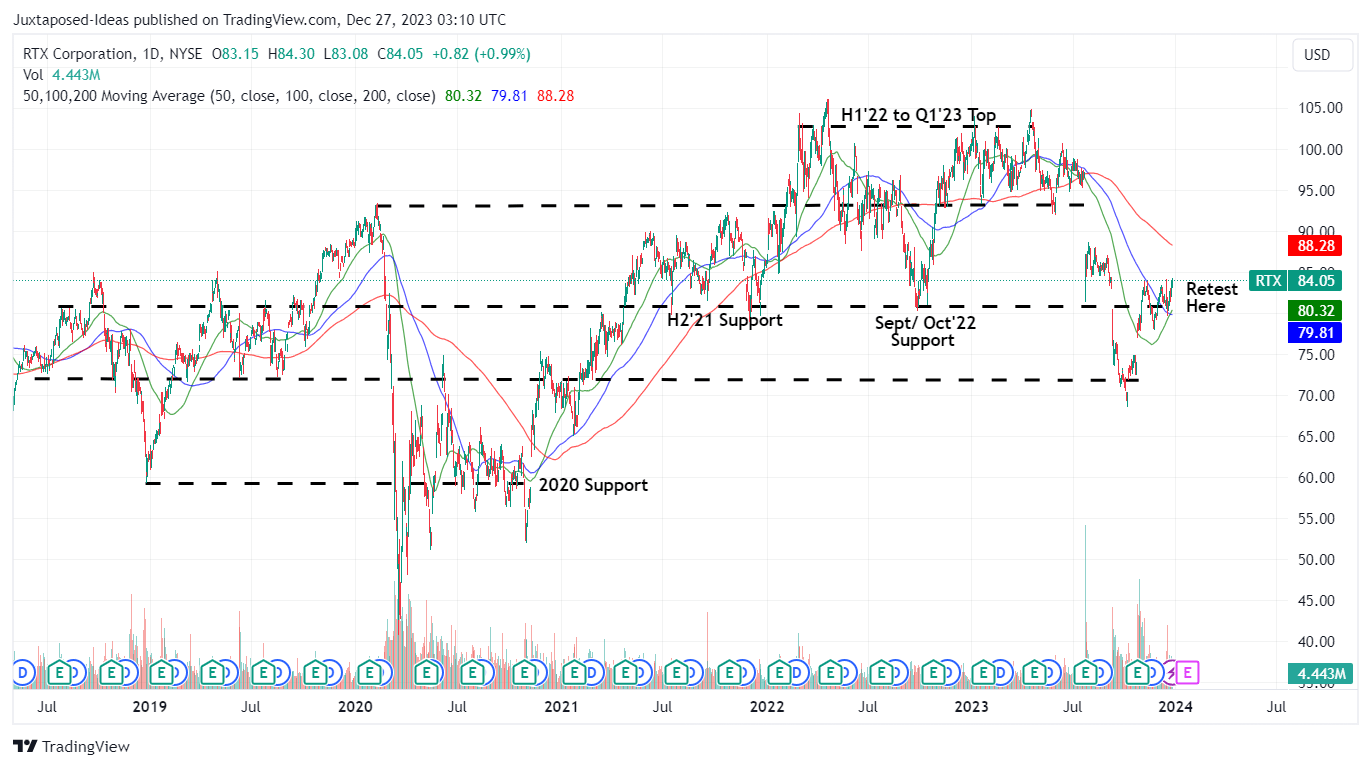

So, Is RTX Inventory A Purchase, Promote, Or Maintain?

RTX 5Y Inventory Value

TradingView

On account of the impacted valuations and pessimistic market sentiments surrounding the powder metallic defect, we will perceive why the RTX inventory has but to climb out of its present rut, with its upward momentum from the October 2023 backside stalling on the $80s.

There may be, after all, a danger that the defect could unfold to different fashions, triggering additional headwinds to its profitability whereas doubtlessly impacting client confidence.

For now, we desire to take a look at the inventory’s growth as a very good one as an alternative, with RTX prone to be well-supported at present ranges, providing traders with an improved upside potential of +27.4% to our long-term value goal of $107.10.

That is primarily based on the consensus FY2025 adj EPS estimates of $6.30 and the eventual re-rating of its FWD P/E valuations to its normalized ranges of 17x as soon as the defect has been absolutely resolved.

RTX’s dividend funding thesis stays strong as properly, due to its glorious working money circulation from persevering with operations of $7.8B (+38% sequentially) and free money circulation era of $5.33B over the LTM (+62.9% sequentially), towards the $3.26B of dividend obligations (+5.8% sequentially).

Mixed with the expanded ahead dividend yields of two.84%, in comparison with its 4Y common of two.48% and sector median of 1.46%, we imagine that RTX gives a comparatively respectable funding thesis throughout capital appreciation and revenue for value-oriented traders.

Readers should additionally notice that the inventory market is forward-looking, with the rising long-term backlog additional making certain the protection of its prime and backside line efficiency over the subsequent few years, as with its dividend payouts.

Due to this fact, we proceed score the RTX inventory as a purchase.