imaginima

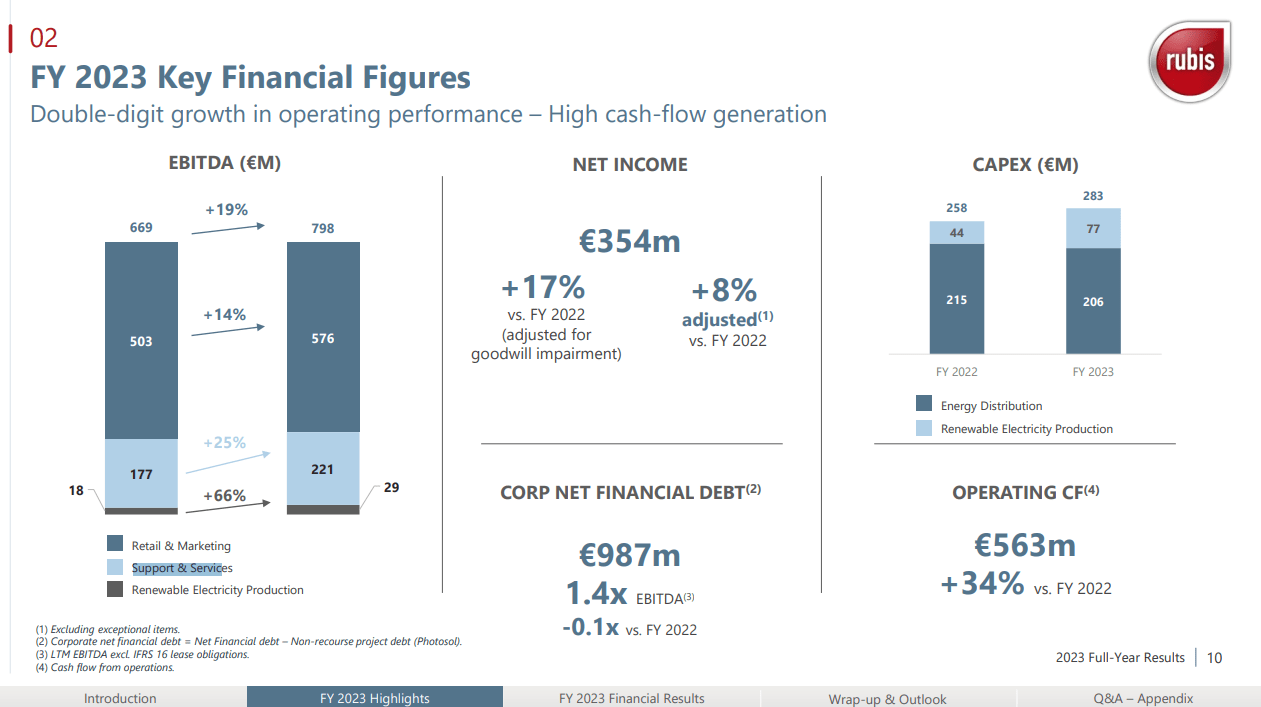

Rubis (OTCPK:RBSFY) delivered a very good quarter. Help and companies would have been the buying and selling angle this yr as delivery charges climb, however the retail phase pushed by the Caribbean noticed wonderful efficiency, and Haiti dragged much less. The majority liquid storage J.V is doing nicely on the again of investments that had been lately accomplished and at the moment are being monetised. Within the renewable power enterprise, which we regard with suspicion as per our final protection, grew in EBITDA on the again of continued giant investments within the phase. We nonetheless do not discover these investments significantly economical or spectacular, and we be aware the influence that the bigger debt burden is having on the power for the efficiency increased up the sheet to translate into the underside line. Nonetheless, the inherent working leverage of the enterprise, the excessive chance progress drivers and the safety in being strategic infrastructure has introduced the enterprise clearly ahead whereas being valued clearly at a a number of not typical for infra, which universally goes into the double digits even now.

Earnings Breakdown

IS (FY PR)

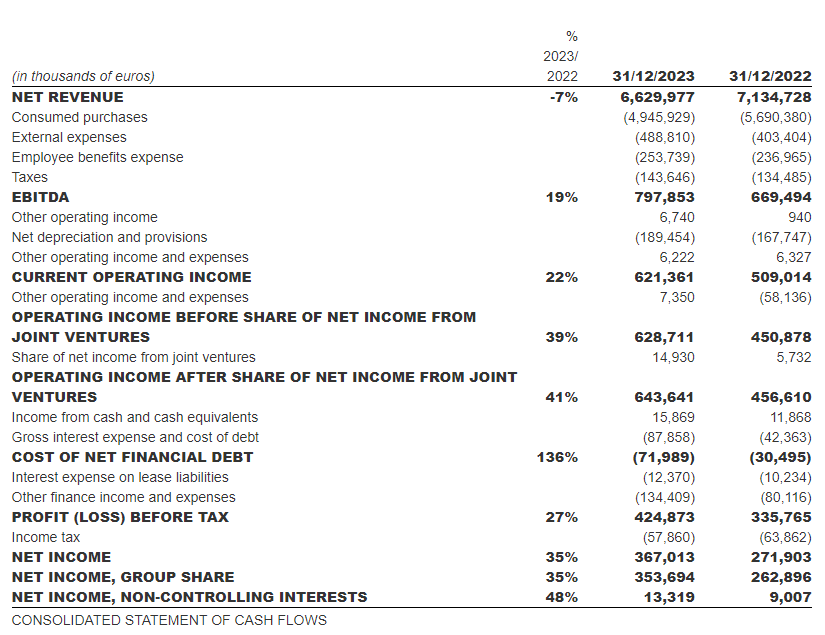

The outcomes had been sturdy. Firstly, the topline is irrelevant and will be ignored. EBITDA is the place to start out, or gross margin which is provided in the PR.

Help and companies noticed progress of 25%, a very solid result. A part of the explanation for that is that they do delivery and buying and selling, and with the conflicts within the Center East, longer constitution intervals and fewer ship availability has induced delivery charges to reflate as soon as once more. It helps that the fleet additionally grew additional in H1 2023, earlier than the conflicts truly occurred and when much less ship house owners could be scrambling for brand spanking new vessels. The SARA refinery within the French Antilles, which operates with a set regulated margin, continues to offer a powerful and steady underpinning to assist and companies.

Highlights (FY Pres)

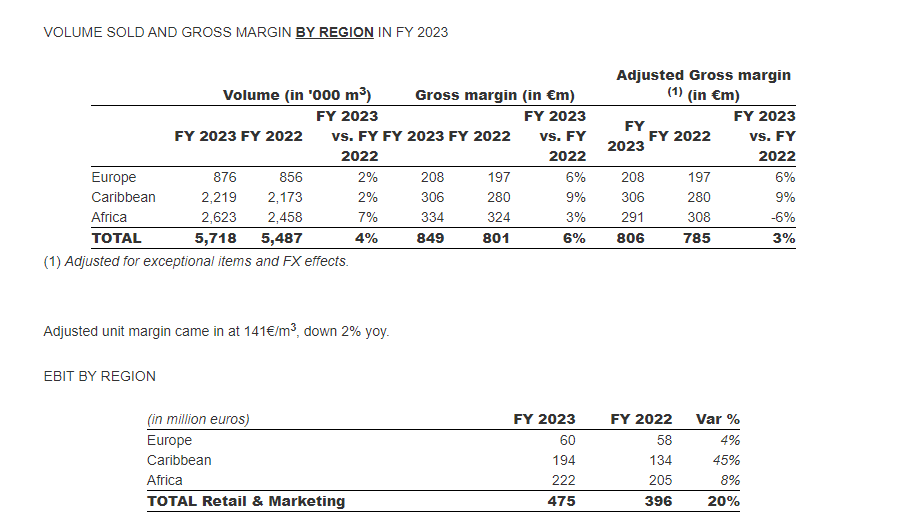

The retail and advertising and marketing phase noticed about 60% of the expansion come from considerably higher working leads to the Caribbean. Volumes had been up 2%, and 5% excluding Haiti, with market share positive factors and the power to push increased margins within the area rising outcomes considerably by 45% within the area. The restoration in tourism, and common energy in tourism, drove the dynamics on this enterprise. Europe was steady in volumes and noticed some gross margin enhancements.

Regional Figures, Retail & Advertising (FY PR)

Africa did nicely when it comes to volumes, however FX results impacted outcomes. This was regardless of down volumes in bitumen, the place Rubis is positioned to offer bitumen in Africa to assist infrastructure improvement. Aviation volumes had been sturdy in Africa this yr, pushed by Kenya, along with them being sturdy within the Caribbean.

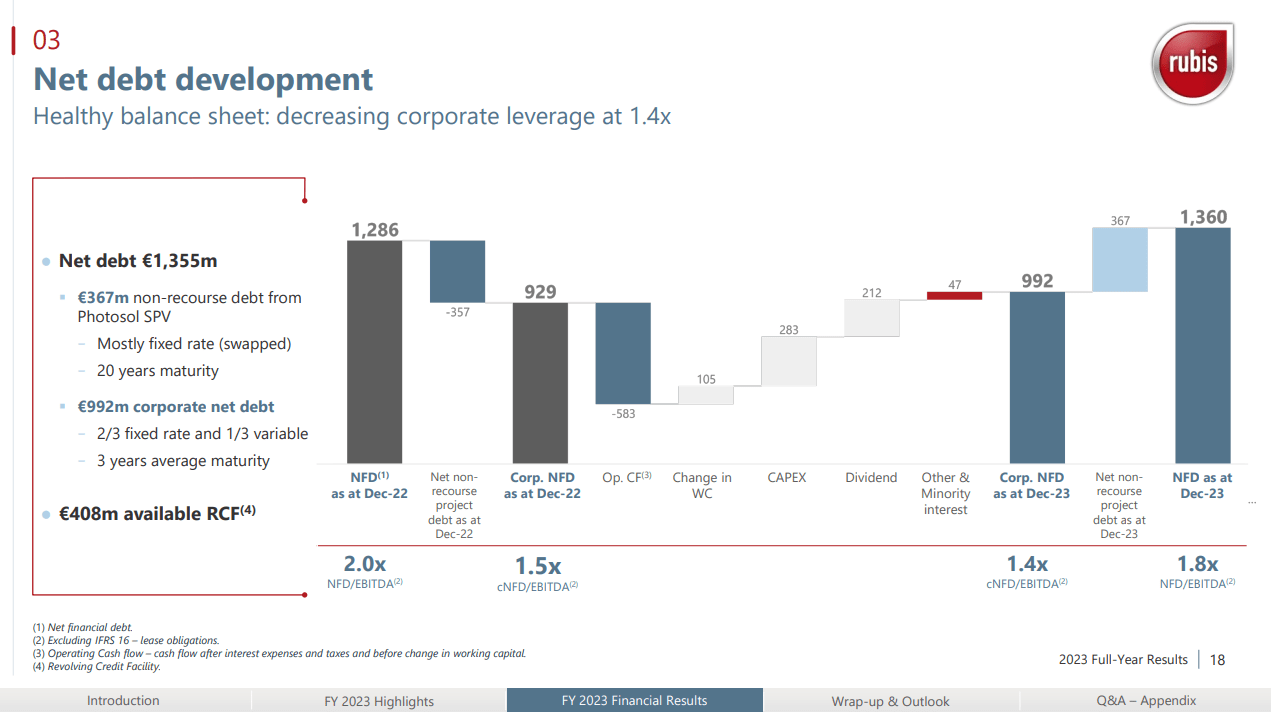

Photosol noticed elevated EBITDA as new capability comes on-line. It continues to be the principle CAPEX sink, and is the only real trigger for will increase of internet debt in a excessive curiosity setting.

Internet Debt Growth (FY Pres)

We be aware the dramatic improve in complete curiosity prices within the revenue assertion which dampened the influence of upper working outcomes on the underside line, with adjusted earnings (adjusted for an impairment of Haiti final yr and a litigation achieve this yr) solely rising 8%.

Nevertheless, to the phase’s credit score, it’s fairly worthwhile and at some point will begin lowering leverage coming from the non-recourse debt used to finance the Photosol tasks. Nevertheless, as we detailed in our last coverage, terminal yields should not going to be that prime, generously perhaps forward of 8% pre-tax, and the corporate states that the tasks may have an IRR round 7-9% unlevered. Whereas it is an alright fee, it is nonetheless beneath what the corporate might obtain with substantial buybacks and deleveraging, significantly given the present fee setting, or reinvesting in its flagship companies. However relying on the funding alternatives that might be out there in a few years’ time, a 7% IRR would not be that unhealthy if they’ll ship. Additionally, this enterprise works on PPA agreements, typically agreed previous to improvement and on a reasonably long-term foundation, so it’s steady. We simply do not assume the yield is there in comparison with alternate options, and given debt prices.

Backside Line

We proceed to be impressed with the strategic worth in its assist and companies enterprise. We had anticipated some downturn within the enterprise attributable to its publicity to delivery, the place constitution charges had been a part of the overall deflation in commodities and commodified companies. In any other case, retail and advertising and marketing continues to carry out nicely, and is equally strategic for the governments that require Rubis provide to develop.

For the storage J.V which we’ve not talked about up to now, we see very stable income progress and in-line EBITDA progress as inflation is handed on to prospects. Utilisations stay very excessive at 95% pushed by reserves of non-fuel merchandise.

Markets have responded nicely to this information, with the inventory now exceeding pre-dividend ranges mid-2023, presumably starting an extended restoration from its extremely depressed inventory costs, which were sinking now for years, comparatively inexplicably.

The one causes we might consider had been dividend sustainability, weak-ish FCF conversion because of the Photosol tasks and common capital depth, and presumably the rising market focus. Whereas there are rising market dangers, with Madagascar making a stink final yr with value caps and Haiti being a weight on the Caribbean enterprise, it is not actually a great clarification for the progressive declines because it’s at all times been the case that Rubis serves these markets. We actually do not just like the Photosol enterprise, significantly as a result of each the dividend yield and earnings yield, in different phrases, in each approach you account for inventory worth, it might be extra helpful to do a buyback than make these Photosol investments. There was additionally numerous leverage from earlier than that would have been introduced down, and certainly some methods to sink money into their present companies extra meaningfully.

At any fee, the technique is already underway, so taking a look at outlook, nothing will be concretely predicted exterior of the continuation of the secular tendencies in demand for provide of power in rising markets, in addition to entry into new markets like Guyana and Suriname that are dangerous however might have a whole lot of potential. For assist and companies, ongoing battle continues to assist that enterprise’ income exterior of the SARA enterprise, however it might flip down if situations normalise once more. Photosol will proceed to deliver new capability on-line. Based mostly on “under construction” operations in Photosol, round a 20% capability improve appears cheap to anticipate in 2024 as a baseline, as much as the opportunity of doubling if all ready-to-build tasks are realised as nicely. Adjusted internet revenue is predicted to develop one other 10% or so, however earlier than the appliance of the brand new international minimal tax, which is able to offset all progress and trigger a flat evolution. Equally, they appear to anticipate EBITDA to remain kind of flat. That is not a nasty final result, and appears fairly good for an infrastructure play with a 10x PE and an 8% dividend revenue proposition, the place infra multiples usually get fairly stratospheric and yields moderately compressed. A 5.3x EV/EBITDA is clearly low for infra.

We have been following Rubis for a long-time, and the valuation case has at all times been compelling, in addition to yield, however we simply do not like how they’re sinking money and insisting on this renewable improvement. It does not appear optimum, and it appears like they’re fishing for ESG factors, and we would moderately press on with simply as low-cost companies, normally with higher economics, in different markets.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.