BeritK/iStock by way of Getty Photos

In a brief house of time, with a a lot smaller funds, Rumble Inc. (NASDAQ:RUM) claims to have constructed a mini Google’ in its most up-to-date Q4 2023 Earnings call. It has expanded its portfolio targeted on censorship-free content material to incorporate video, live-streaming, an promoting centre and since Q1 2024 it’s providing its independent cloud services to the general public on a subscription-based enterprise mannequin. The inventory, thought of a high-growth inventory, has seen some severe momentum these days, rising by 42.25% since my previous article in January 2024. Most of its fashionable content material creators are targeted on politics. Subsequently, political occasions extremely affect consumer exercise, of which there will likely be loads this US election yr. Consequently, this makes the inventory extremely risky and unpredictable as market sentiment is much less about its monetary efficiency. In FY2023, complete income has greater than doubled, however it’s nonetheless solely at $81 million, and there was a major slowdown within the second half of FY2023. Moreover, the corporate lacks sufficient promoting income sources, now we have but to see the monetisation consequence of its cloud providing, its losses are deepening, and the corporate is rising its money burn. A quick comparability of the inventory relative to friends within the business makes it tough to justify the present valuation versus the comparatively disappointing efficiency and lack of development steering. Subsequently, I don’t suggest it for long-term buyers and keep a maintain ranking.

One yr inventory pattern (SeekingAlpha.com)

Rumble – Latest updates

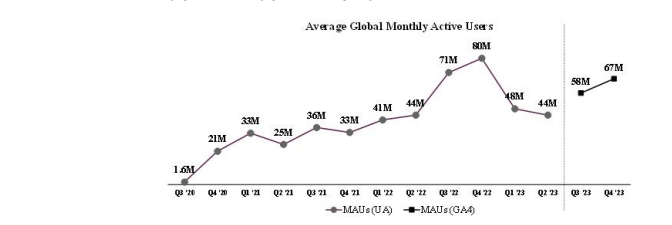

Just lately, I offered an overview of the company. I believe it important to remember that Rumble is attracting an viewers by its anti-censorship, politically nuanced stance, paying a number of massive, polarising content material creators to publish on the positioning. It rapidly constructed up a recurring month-to-month lively consumer base of over 40 million, catapulting its development off the again of an more and more polarised political surroundings within the US since 2020.

Common world month-to-month viewers per quarter (Sec.gov)

It’s attempting to diversify its content material and enhance promoting alternatives by partnerships, reminiscent of Barstool Sports. Most not too long ago, it has expanded its portfolio by publicising its unbiased cloud providing. The most recent cloud offering is on a subscription-based mannequin and can diversify the corporate’s income, which is primarily advertising-based.

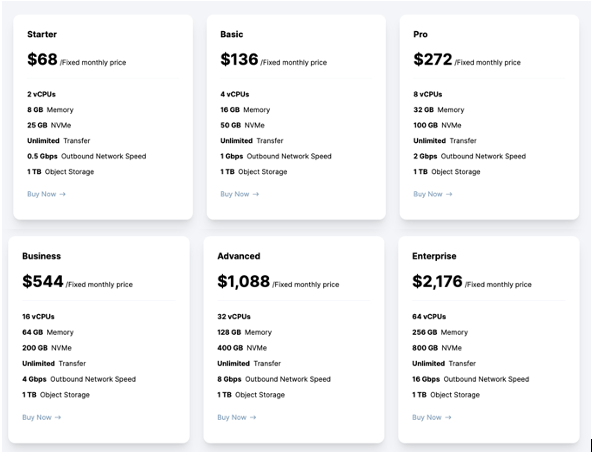

Rumble portfolio (Sec.gov) Rumble’s cloud providing (Firm web site)

Rumble inventory – Challenges and future development

Nonetheless, amidst all these efforts, there are underlying challenges to attracting advertisers and rising content material engagement in an area dominated by Tech Giants with a lot bigger budgets, way more superior infrastructure, a lot higher world attain and extra willingness to adapt their insurance policies to satisfy promoting necessities. Rumble’s loyal (nonpaid) customers are there for the free speech message, keen to simply accept performance deficits and fewer flashy, slower consumer interface experiences. The corporate’s financial efforts have been targeted on promotion. A fast look at Rumble’s trending videos over the past month reveals that the most well-liked movies are largely by people paid to publish on Rumble and beforehand banned from YouTube (GOOGL).

Rumble trending (Rumble.com)

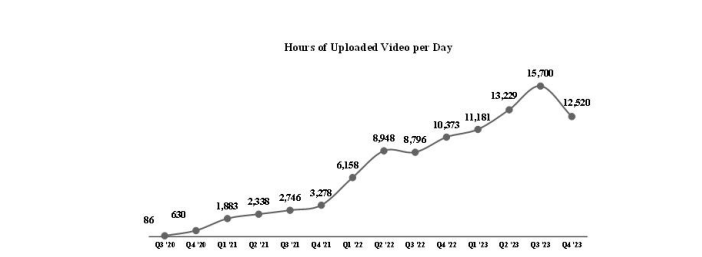

For extra customers to stay round, I imagine heavy investments within the infrastructure will likely be required to achieve long-term lively consumer traction. The significance of performance was proven when YouTube blocked its auto-sync with Rumble. This has had a direct impression on the variety of hours of content material uploaded to the positioning.

Each day hours of uploaded video per quarter (Sec.gov)

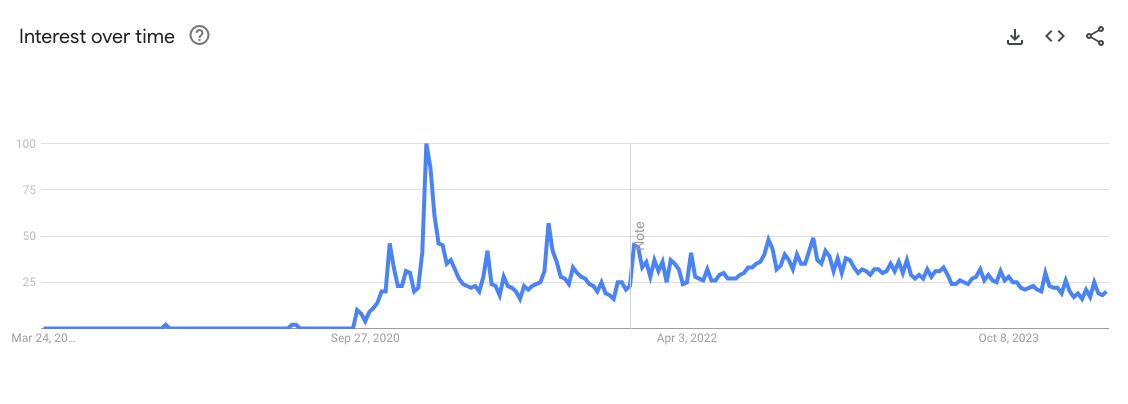

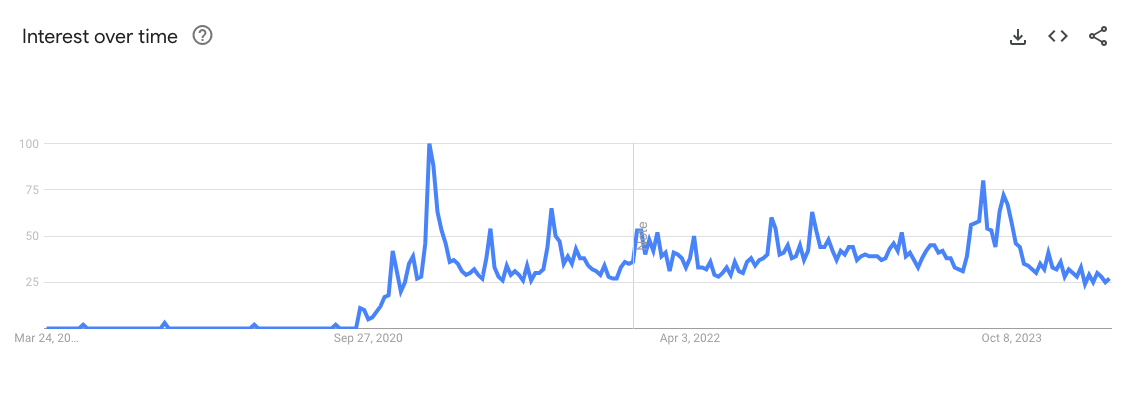

If we take a look at Google Tendencies, we will see that the corporate acquired most of its consideration throughout the earlier US elections in 2020. Nonetheless, outdoors of politically heated and polarising occasions, the corporate has not notably proven an upward pattern in search curiosity throughout the US or globally.

Rumble.com in the USA over 5 years (Trends.google.com) Rumble.com pattern worldwide over 5 years (Google Trends)

For FY2024, it is going to be important to see whether or not the corporate can monetise its rising variety of providers. Monetisation from promoting will likely be essential, permitting the corporate to cut back spending on content material creators and develop its high line. Moreover, we’ll seemingly see spikes in lively month-to-month consumer tendencies because of the US elections. These are to be thought of outliers to common development. Rumble has not but launched steering; nonetheless, it indicated upward outcomes from Q2 2024 and expects to interrupt even by 2025.

Rumble This autumn 2023 earnings overview

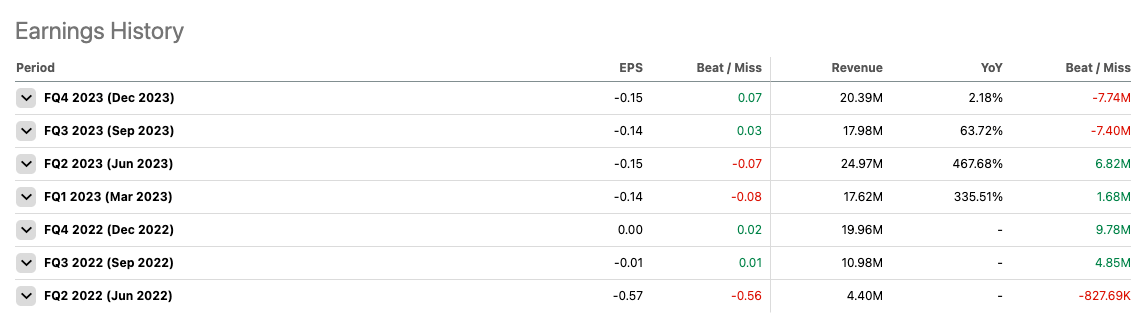

Within the final two quarters, now we have seen a major slowdown within the firm’s top-line income, lacking income expectations for 2 consecutive quarters. That is regarding for a enterprise within the development part and displays the most important problem of attracting and protecting advertisers on a platform targeted on non-censorship. The corporate has established an promoting centre to enhance this and extra service income and has diversified its income right into a cloud providing, however now we have but to see the impression of those initiatives. In This autumn 2023, Rumble beat EPS expectations by $0.08 to realize a GAAP EPS of destructive $0.14. Nonetheless, we will see deepening losses as the highest line fails to cowl the prices of the operations.

Quarterly EPS and income efficiency (SeekingAlpha.com)

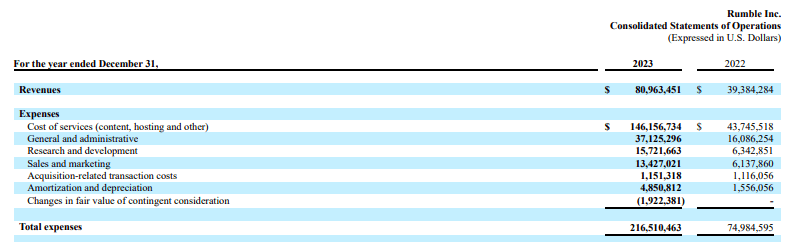

We will see that prices and bills have elevated, however on the similar time, that is additionally resulting from increasing the enterprise, leading to extra content material creation prices, internet hosting charges and different providers.

Bills FY2023 versus FY2022 (Sec.gov)

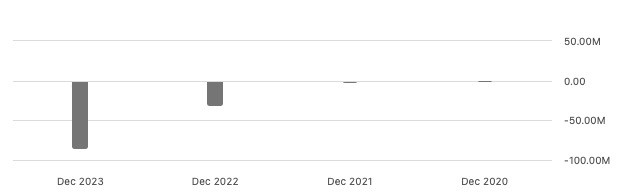

We will see that there’s vital money burn, with levered free money circulate at destructive $84.4 million. An enormous chunk of this money circulate goes in the direction of its content material creators. Rumble goals to cut back this considerably by the tip of 2024; nonetheless, this may stay a difficulty for Rumble so long as these content material creators aren’t bringing in severe cash from promoting.

Annual levered free money circulate (SeekingAlpha.com)

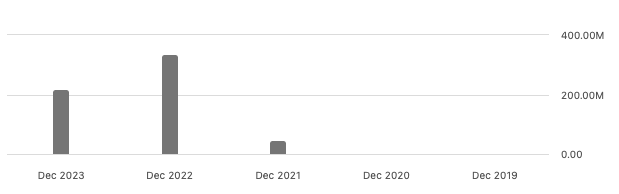

If we take a look at the stability sheet, we will see that the entire money in FY2023 was $218.3 million. Administration believes that it has sufficient money to satisfy its capital necessities. Moreover, it can profit from price financial savings by automated enterprise processes to enhance prices because it scales.

Whole money and brief time period investments (SeekingAlpha.com)

RUM inventory valuation

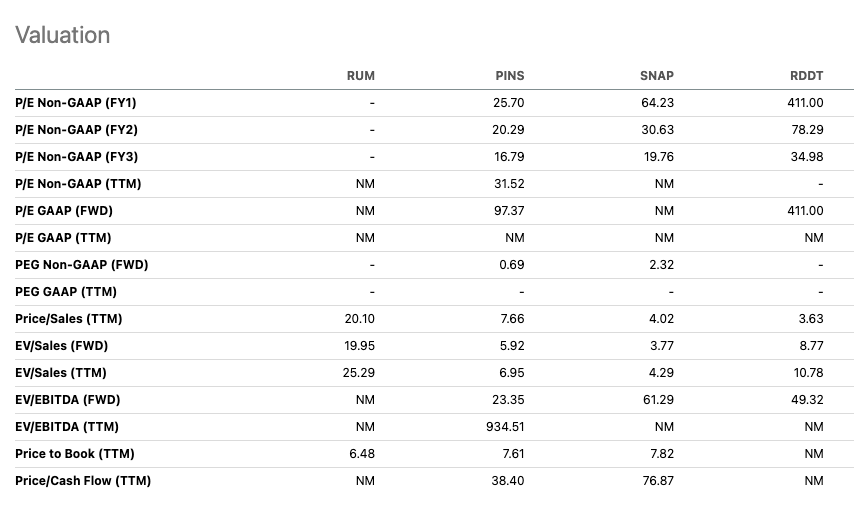

Rumble’s inventory momentum has been fuelled extra by hype and hypothesis than monetary progress, making the inventory inherently dangerous. It has a market cap of $2.26 billion, whereas annual income has but to achieve $100 million, and annual EPS in FY2023 has dropped to $0.58. Moreover, whereas the corporate has elevated its providers, there’s rising uncertainty about how properly they are often monetised below its non-censorship stance. If we examine the inventory in opposition to three friends that make the most of customers’ time spent on-line and generate income by promoting, specifically Pinterest (PINS), Snap (SNAP), and not too long ago public Reddit (RDDT), we will see that its price-to-sales ratio of 20.10 could be very excessive in comparison with its friends. At this stage, the dangers of investing outweigh the rewards, amplified by its peer comparability.

Valuation versus friends (SeekingAlpha.com)

Dangers

Rumble has caught the general public’s consideration by specializing in non-censorship. Nonetheless, it’s struggling to search out monetisation methods to match this message. Moreover, the administration staff has restricted expertise working a public firm, and the corporate has expanded its enterprise in a short time. This enhance in complexity relating to stakeholders and firm operations could require a talent set at the moment not current throughout the govt staff, which may negatively impression the enterprise. The corporate has additionally grown by heavy promotion and funding in sensational content material creators, however much less funding has been made within the infrastructure. After I briefly clicked by some movies on the positioning, I used to be typically met with laggy content material. This might postpone potential customers and impression the general enterprise efficiency in the long term.

Ultimate ideas

Rumble’s inventory worth has seen vital upward momentum over the past three quarters. Nonetheless, there was a dramatic drop in top-line momentum within the earlier two quarters, and the corporate’s losses have deepened YoY, alongside rising money burn. Though administration believes it has sufficient money to put money into the enterprise, and there are some thrilling new providers on provide, the urgent query stays whether or not this enterprise, constructed on non-censorship, can efficiently monetise its efforts in a extremely aggressive on-line house. Moreover, the inventory is extremely risky and impacted by information moderately than financials. Subsequently, I don’t imagine there’s sufficient reward versus the danger for long-term buyers to take a place and keep a maintain place.