Paper Boat Artistic/DigitalVision by way of Getty Pictures

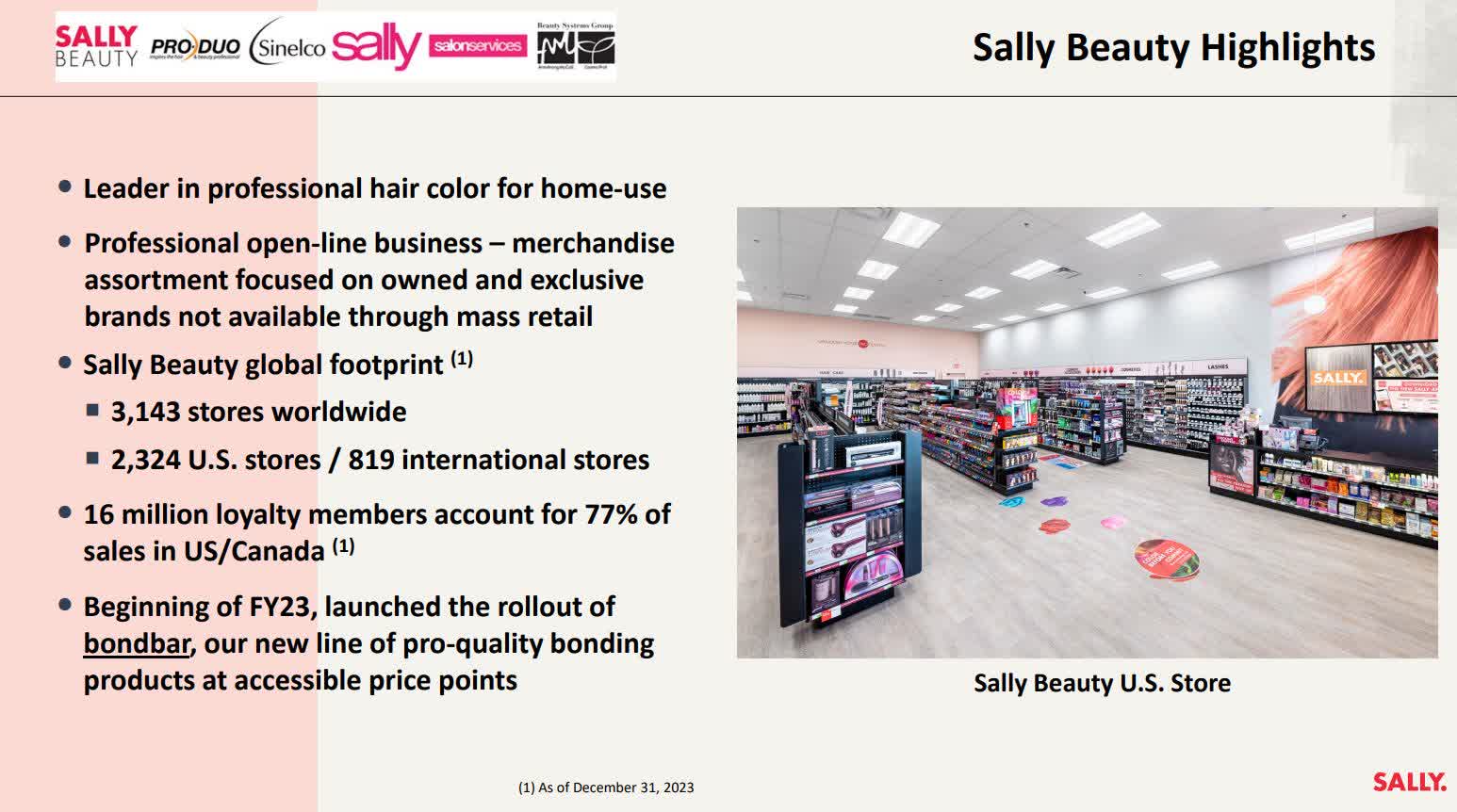

Sally Magnificence Holdings, Inc. (NYSE:SBH) is a number one cosmetics and sweetness care firm. It sells to shoppers by its “Sally Beauty” chain of shops, and it sells to professionals by its “Beauty Systems Group” division. It has over 4,500 shops globally, and sells on-line as properly and thru direct gross sales consultants. The Sally Magnificence division accounts for about 57% of revenues, and the Magnificence Methods Group generates round 43% of whole gross sales, every year. This firm has efficiently developed a lot of its personal manufacturers which provide excessive margins and it has unique distribution agreements with many main manufacturers as properly. As proven beneath, it additionally has 16 million loyalty members which account for about 77% of gross sales within the U.S. and Canada.

Sally Magnificence Holdings, Inc.

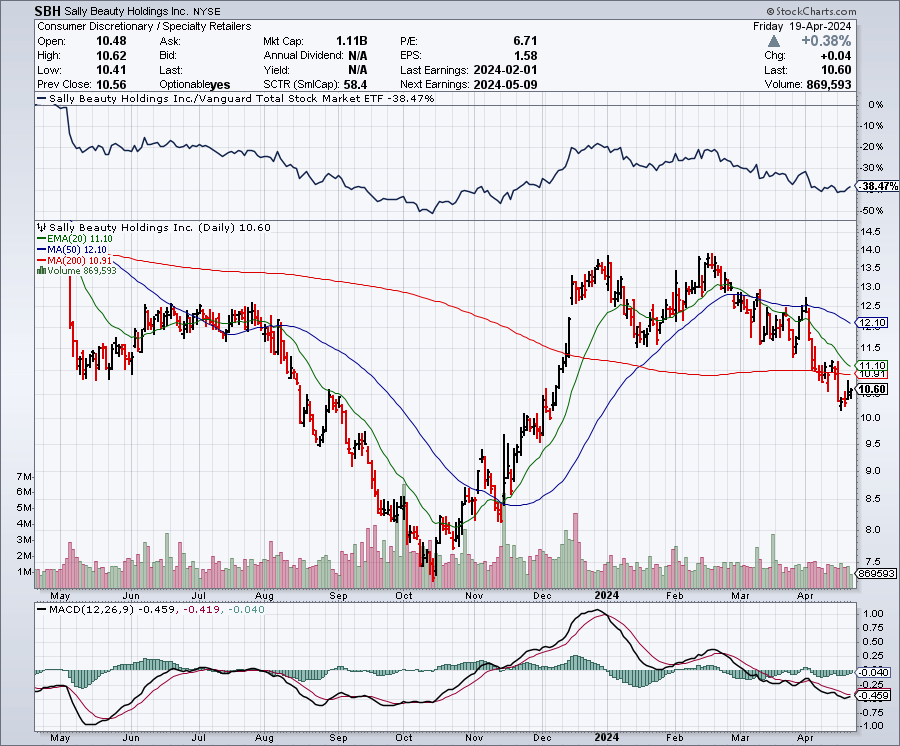

The Chart

Because the chart beneath exhibits, this inventory was buying and selling round $14 per share in February, however since then it has declined to lower than $11. This decline appears to have been largely prompted by a competitor warning of a slowdown in magnificence gross sales. Firstly of 2024, a bullish “Golden Cross” shaped for the reason that 50-day transferring common which is $12.10, crossed over the 200-day transferring common which is about $10.91. The Golden Cross continues to be displaying on the chart however it’s now in danger, since this inventory is now buying and selling for about $10.60 per share.

StockCharts.com

Strategic Targets May Considerably Profit The Backside Line In 2025 and 2026

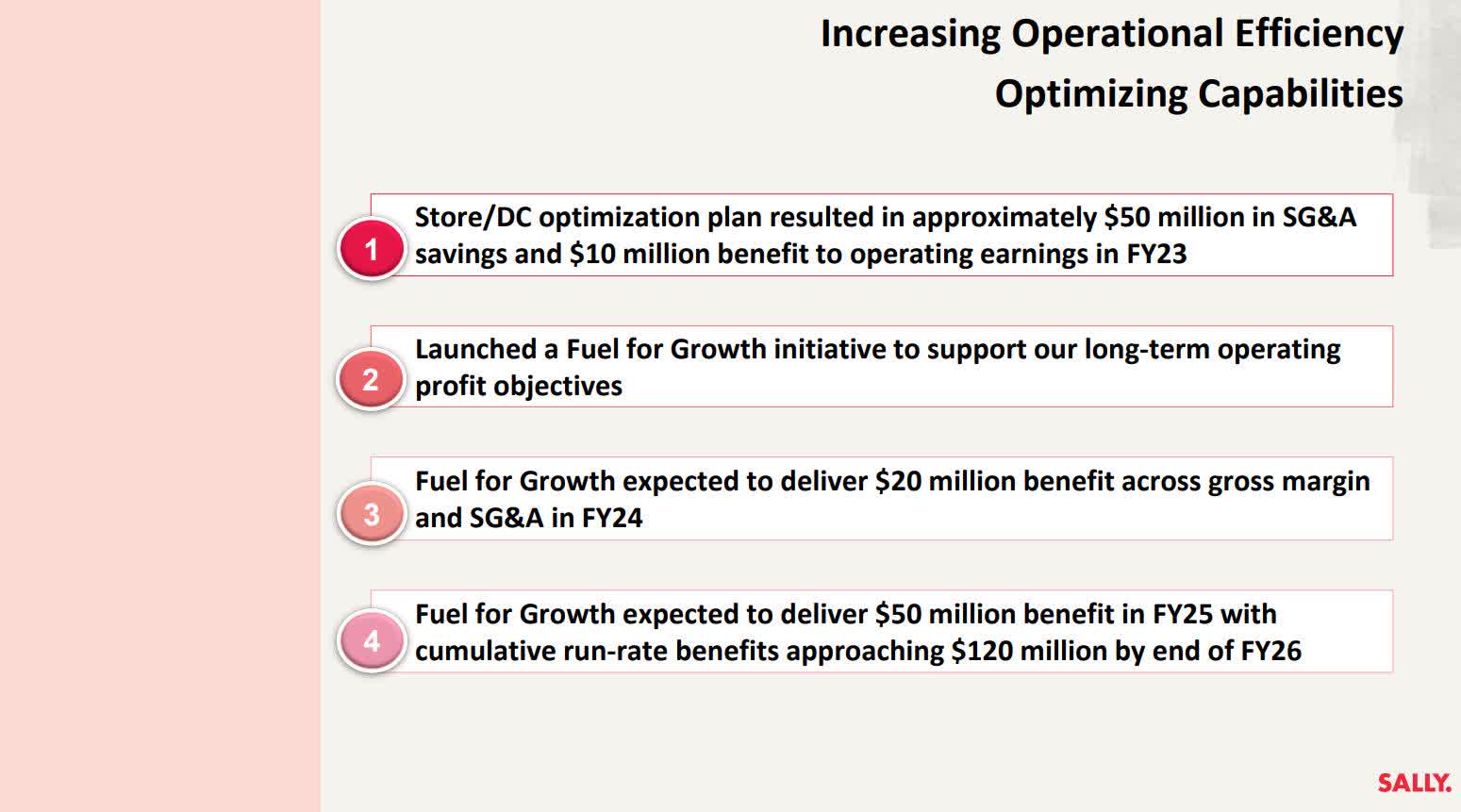

Sally Magnificence has just a few strategic targets it has set that might result in improved monetary outcomes over the following couple of years. The fourth aim proven beneath might result in $50 million in useful price financial savings in fiscal 12 months 2025, and even better advantages of $120 million in 2026. This firm has practically 105 million shares excellent, so price financial savings of $50 million might probably deliver practically $0.50 per share to the underside line and $120 million in price financial savings might probably affect the underside line in a optimistic approach, by over $1 per share.

Sally Magnificence Holdings, Inc.

Some Positives To Contemplate

Up to now few years, it looks as if persons are extra targeted on their look, whether or not it’s for a video name, or for pics that they need to submit on social media websites. The massive enhance in selfies, movies and video calls, ought to proceed to learn the wonder trade.

In March, 2024, DoorDash (DASH) announced a brand new partnership with Sally Magnificence, and mentioned that each one these shops would now be obtainable for supply on DashPass. This is a perfect strategy to tremendously broaden supply choices and allow same-day supply, making Sally Magnificence in a position to compete with on-line giants like Amazon (AMZN) which provide fast supply.

Some analysts and buyers imagine that Sally Magnificence may very well be a lovely takeover goal. This might make sense for just a few causes, however the low valuation of this inventory may very well be the most important purpose. This In search of Alpha article places forth just a few potential suitors, together with Amazon (as a part of Amazon Magnificence).

The Warnings From Ulta

On April 3, 2024, SA Information Editor Clark Schultz gave details on an enormous drop in Ulta Magnificence (ULTA) shares which occurred after the corporate offered on the J.P.Morgan (JPM) Retail Spherical Up Convention. Ulta Magnificence warned that they noticed some strain on shoppers due to excessive ranges of bank card debt and rates of interest. The steerage was not too unhealthy in my view as a result of the corporate was nonetheless guiding for low single-digit progress. That’s not adequate in case your inventory has a excessive value to earnings ratio, however it nonetheless represents progress. It is value noting that Ulta Magnificence trades for about 16 occasions earnings. Against this, Sally Magnificence trades for nearly 6 occasions earnings. A gross sales slowdown goes to affect a inventory with a a lot increased value to earnings ratio much more than a inventory that trades for about 6 occasions earnings. Sally Magnificence shares have dropped by about 20% since this warning got here from Ulta Magnificence. I feel that’s an overreaction and a shopping for alternative.

Earnings Estimates And The Steadiness Sheet

Analysts expect this firm to earn $1.87 per share in 2024, with revenues coming in at $3.72 billion. Earnings estimates for 2025, are at $1.98 per share, on revenues of $3.76 billion. Earnings are seen as rising to $2.33 per share in 2026, and revenues are anticipated to rise to $3.87 billion. These estimates counsel that Sally Magnificence shares are buying and selling for nearly 6 occasions earnings. That’s extraordinarily undervalued when in comparison with different shares on this sector, or to the market usually. The S&P 500 Index (SPY) presently trades for about 21 occasions earnings. On the balance sheet, Sally Magnificence Holdings has $121 million in money and about $1.66 billion in debt.

Potential Draw back Dangers

A slowdown may very well be within the works for the U.S. financial system, however this inventory already seems to be priced for a gentle slowdown at simply round 6 occasions earnings. However, if the Federal Reserve fails to chop charges earlier than lengthy, we might simply see the arduous touchdown situation play out. This might affect retail shares considerably and presumably ship Sally Magnificence shares into the one digits. Aggressive threats from giant corporations is one other potential draw back danger.

In Abstract

This isn’t a inventory or a sector that I might make investments some huge cash in, however I feel a small funding on this firm is sensible after the pullback we’ve seen. Sally Magnificence trades for simply round 6 occasions earnings, which is deeply undervalued when in comparison with some rivals and to the inventory market usually. With the potential for earnings to develop within the coming years because of the strategic price financial savings plans, this inventory might shock to the upside.

No ensures or representations are made. Hawkinvest just isn’t a registered funding advisor and doesn’t present particular funding recommendation. The data is for informational functions solely. You must all the time seek the advice of a monetary advisor.