AndreyPopov

The massive-cap pharmaceutical group has lagged the inventory market badly over the previous yr, relative to the S&P 500 bounce of +25% or high-flying NASDAQ 100 index spike of +40%. So, I take into account this sector a very good looking floor for bargains. Since late summer season, I’ve written bullish views on Pfizer (PFE) here and Bristol-Myers Squibb (BMY) here, however neither has been capable of get out their funk, as buyers fret over the destructive long-term results of Medicare negotiations on future pricing/profitability and main drug-patent expirations at every.

One other Huge Pharma identify with equally sound valuations, however the added assist of earnings progress kickers approaching in 2025, is Sanofi (NASDAQ:SNY), primarily based in Paris with almost 60% of gross sales happening exterior America. Every U.S. ADR creation represents 1/2 of an extraordinary share for Sanofi (OTCPK:SNYNF) traded in Europe (usually priced in Euros).

The corporate is greatest identified for the marvel drug Dupixent [co-developed with Regeneron (REGN)], which generates about 25% of complete firm income at the moment. In line with the 2023 20-F Annual Report,

DUPIXENT (dupilumab) is a totally human monoclonal antibody that inhibits the signaling of the interleukin-4 (IL-4) and interleukin-13 (IL-13) pathways and isn’t an immunosuppressant. Dupilumab is collectively developed by Sanofi and Regeneron underneath a worldwide collaboration settlement. To this point, dupilumab has been studied throughout greater than 60 scientific trials involving greater than 10,000 sufferers with varied persistent ailments pushed partially by sort 2 irritation. The dupilumab growth program has proven vital scientific profit and a lower in sort 2 irritation in Part 3 trials, establishing that IL-4 and IL-13 are key and central drivers of the sort 2 irritation that performs a serious function in a number of inflammatory ailments, corresponding to atopic dermatitis (AD), bronchial asthma, persistent rhinosinusitis with nasal polyposis, eosinophilic esophagitis and prurigo nodularis. DUPIXENT is available in both a pre-filled syringe to be used in a clinic or at dwelling by self-administration as a subcutaneous injection or in a prefilled pen for at-home administration, offering sufferers with a extra handy possibility. DUPIXENT is out there in all main markets together with the US (since April 2017), most European Union international locations (the primary launch was in Germany in December 2017), Japan (since April 2018), and China (since June 2020).

Sanofi can be a serious vaccine provider to the world, which represented nearly 20% of internet gross sales in 2023. It’s a maker of flu pictures and a number of vaccines to guard youngsters/infants throughout the globe from varied ailments.

Sanofi Web site – March twenty second, 2024

Administration is contemplating spinning off its Shopper Healthcare division (12% of 2023 gross sales), to deal with prescribed drugs. Allergy, Cold & Sinus, Digestive Wellness, and Pain medication manufacturing and belongings (which many people use annually) might be listed as a brand new firm. Present shareholders would personal shares in each the brand new client well being enterprise and legacy Sanofi operations. The brand-name listing of OTC objects consists of Allegra, Xyzal, DulcoLax, IcyHot, Aspercreme, Unisom, Oscal-D, and quite a few others.

A sturdy rebound in working earnings is projected by Wall Avenue analysts after a transition yr in 2024. Rising gross sales on common present medication, anticipated new pharmaceutical approvals, and a price slicing program concentrating on €2 billion in reductions by the end of 2025 ought to every add underlying shareholder worth over time.

For forward-looking affected person buyers, shopping for shares now could show a superb resolution. Why? My bullish take is concentrated on (1) a steady and simply coated 4% dividend fee, (2) a stronger stability sheet than most within the trade, (3) a valuation that’s method too low if earnings progress picks up in 2025-26, and (4) patrons look like getting the higher hand vs. sellers in March on the technical charts. Let’s shortly overview the opportunistic setup.

Dividend Story

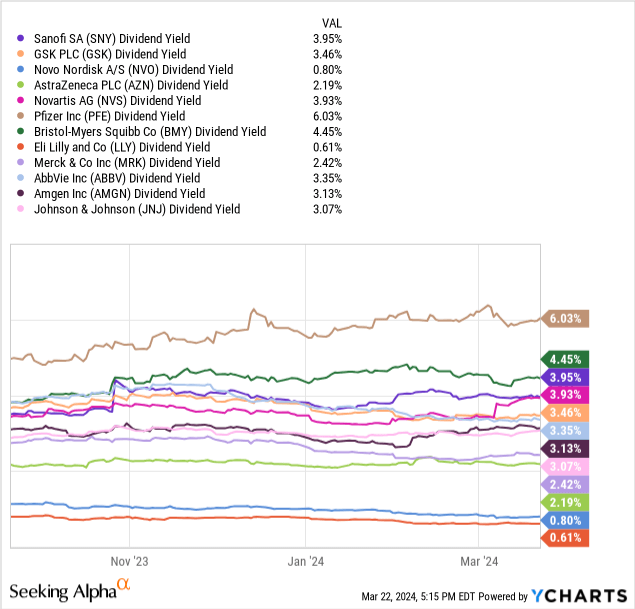

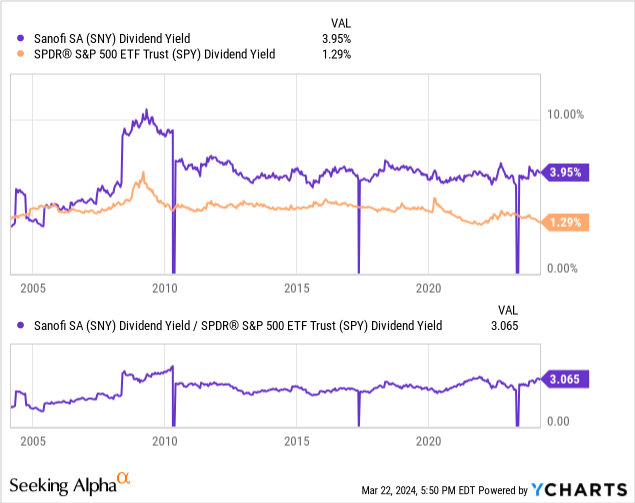

For starters, the revenue crowd and defensive buyers ought to be drawn to the sound dividend payout at Sanofi. Immediately’s tough 4% yield for money distributions is without doubt one of the highest within the Huge Pharma area. Beneath I’ve drawn a 6-month chart evaluating Sanofi to yields from friends GSK plc (GSK), Novo Nordisk A/S (NVO), AstraZeneca PLC (AZN), Novartis AG (NVS), Pfizer, Bristol-Myers Squibb, Eli Lilly (LLY), Merck (MRK), AbbVie (ABBV), Amgen (AMGN), and Johnson & Johnson (JNJ).

YCharts – Sanofi vs. Huge Pharma, Dividend Yield, 6 Months

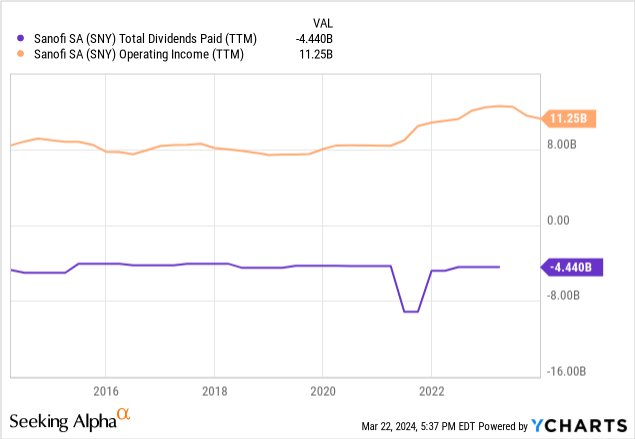

And, the 2x protection from working revenue in 2020 has risen to 2.5x in 2023-24. Primarily, the dividend yield has the strongest protection in over a decade and is best coated than the overwhelming majority of Huge Pharma names. So, the chances of a dividend reduce are fairly restricted, whereas the chance for dividend payout progress is uniquely excessive.

YCharts – Sanofi, Dividend Protection from Working Earnings, 10 Years

Lastly, the Sanofi yield is sitting at the very best “relative” fee to the S&P 500 index since 2010. On the chart beneath, you’ll be able to overview how the trailing 3.95% yield is considerably greater than the SPDR S&P 500 ETF (SPY) equal variety of simply 1.29% right this moment. For revenue buyers on the lookout for security, Sanofi’s dividend is 3x the extent of standard U.S. blue chips!

YCharts – Sanofi vs. S&P 500 ETF, Dividend Yield, 20 Years

Conservative Steadiness Sheet

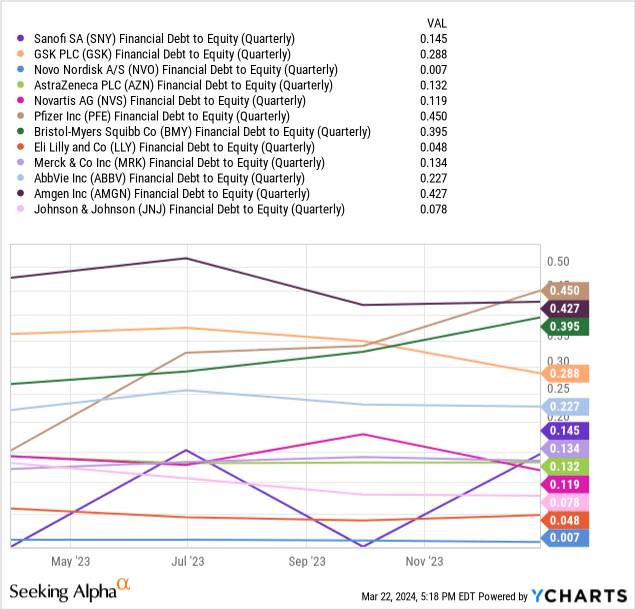

One other thought to ponder in your purchase resolution course of is Sanofi runs probably the most conservative stability sheets in Huge Pharma. Debt to fairness is extraordinarily low at 0.14x, within the backside half of the peer group.

YCharts – Sanofi vs. Huge Pharma, Debt to Fairness, 1 12 months

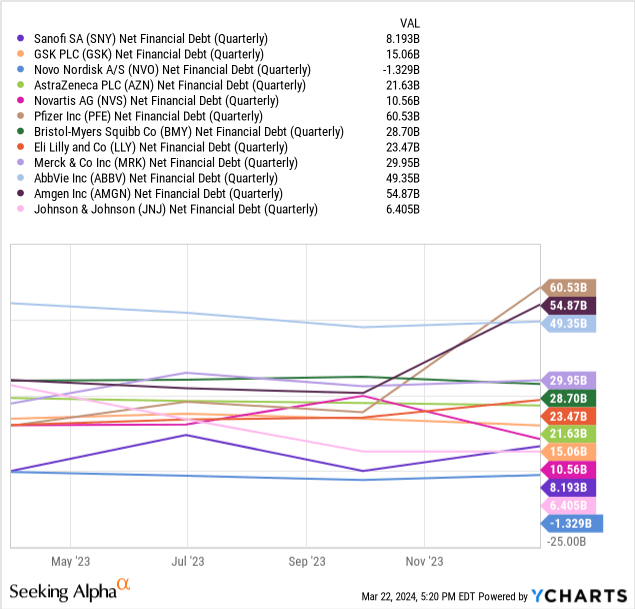

Plus, “net” monetary debt (complete debt minus money readily available) is without doubt one of the lowest within the group, sitting at a minor US$8.2 billion vs. right this moment’s fairness market capitalization of $120 billion.

YCharts – Sanofi vs. Huge Pharma, Web Monetary Debt, 1 12 months

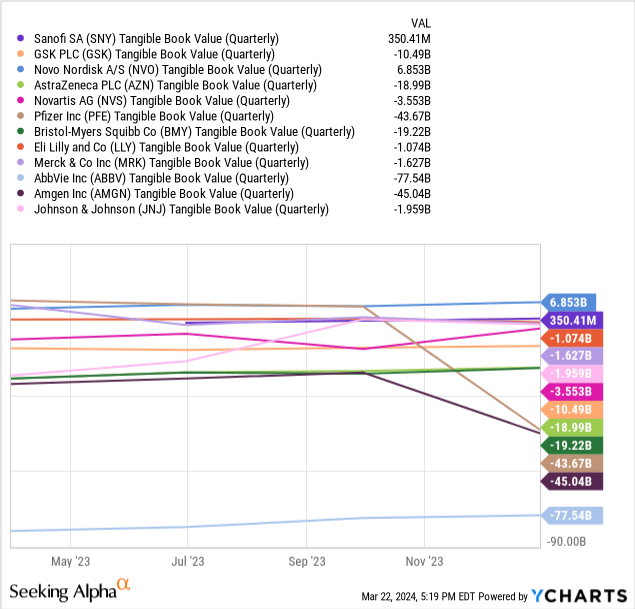

When it comes to underlying internet asset price and monetary flexibility, the corporate additionally has a optimistic tangible guide worth quantity, which is uncommon for the drug trade. With takeover goodwill accounting and patents structured as intangible belongings primarily based on projected future drug gross sales/revenue, the most important pharmaceutical companies historically have NEGATIVE tangible guide values. Though US$350 million in TBV sounds gentle, it is much better than friends.

YCharts – Sanofi vs. Huge Pharma, Tangible E book Worth, 1 12 months

Undervalued Development Proposition

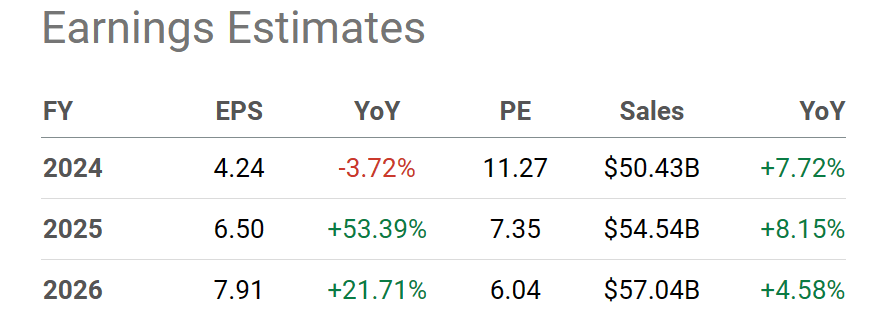

In abstract, Sanofi has a terrific dividend story and a rock-solid stability sheet as a basis for inventory features. However, the really bullish motive to personal the inventory is its valuation could not correctly low cost a brilliant earnings future beginning subsequent yr. 2024 is predicted by analysts to be a yr of restructuring and maybe an organization cut up. Primarily based on the enterprise setup right this moment, earnings per share of US$6.50 subsequent yr and $7.91 in 2026 have but to be priced into the inventory.

In search of Alpha Desk – Sanofi, Analyst Estimates for 2024-26, Made March twenty first. 2024

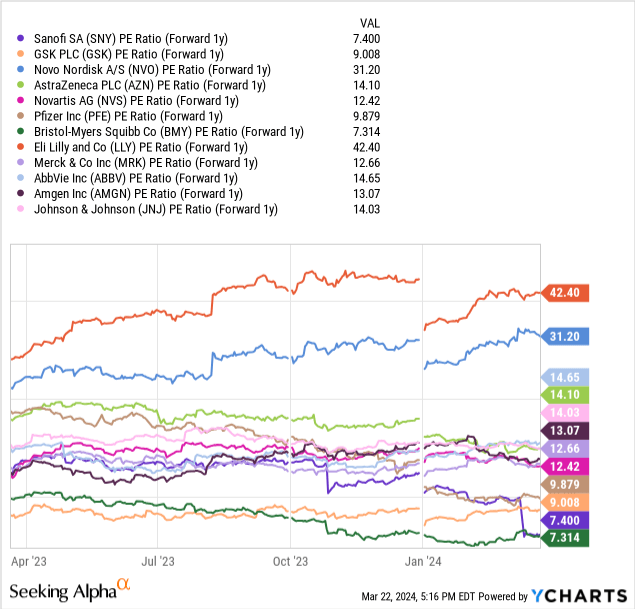

Once we take a look at the peer group and ahead 1-year earnings in 2025, solely Pfizer matches up with Sanofi at a projected P/E of 7x. And, should you weigh 2026 estimates, Sanofi is much and away the most affordable of this group.

YCharts – Sanofi vs. Huge Pharma, P/E Ratio on Projected 2025 Outcomes, 1 12 months

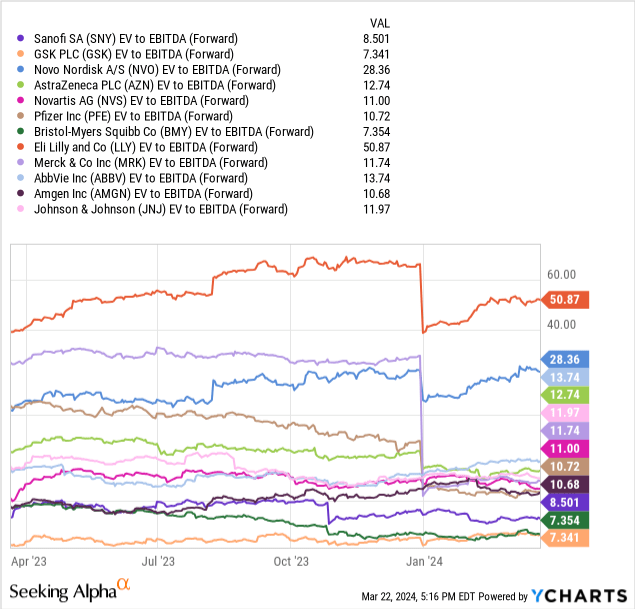

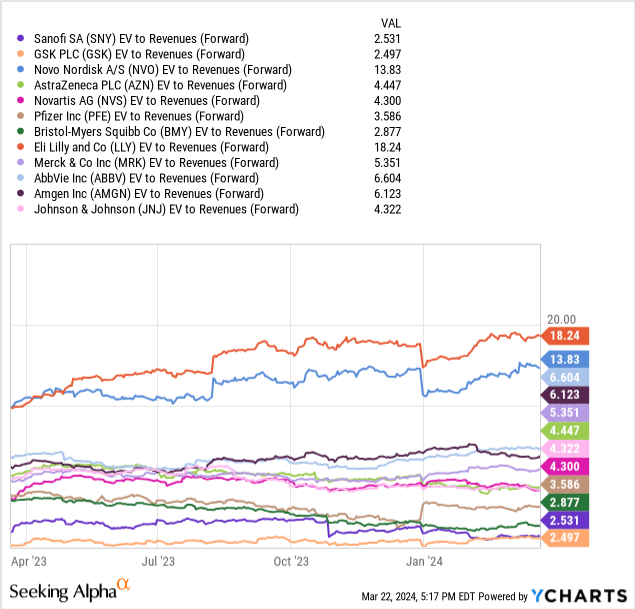

Additional, after we have in mind the corporate’s low stage of internet debt, enterprise valuations on ahead estimated EBITDA (8.5x) and revenues (2.5x) scream SNY is completely a cut price vs. trade opponents. Notice: the sector progress leaders of Eli Lilly and Novo Nordisk are valued richly on their weight-loss GLP-1 drug prospects.

YCharts – Sanofi vs. Huge Pharma, EV to EBITDA on Projected 2024 Outcomes, 1 12 months YCharts – Sanofi vs. Huge Pharma, EV to Gross sales on Projected 2024 Outcomes, 1 12 months

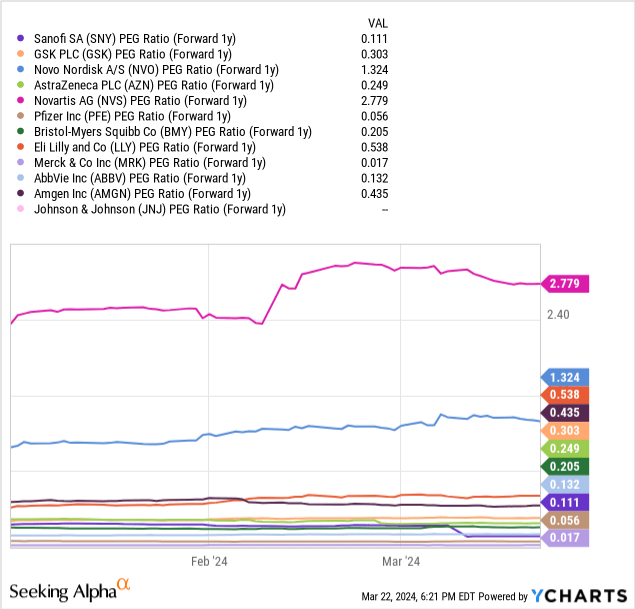

If you cross projected earnings progress charges vs. present P/Es, the PEG valuation for Sanofi is extraordinarily bullish right this moment. Truthfully, most Huge Pharma names look like worthwhile purchase concepts on this metric.

YCharts – Sanofi vs. Huge Pharma, Ahead PEG Ratio on Projected 2025 Outcomes, 3 Months

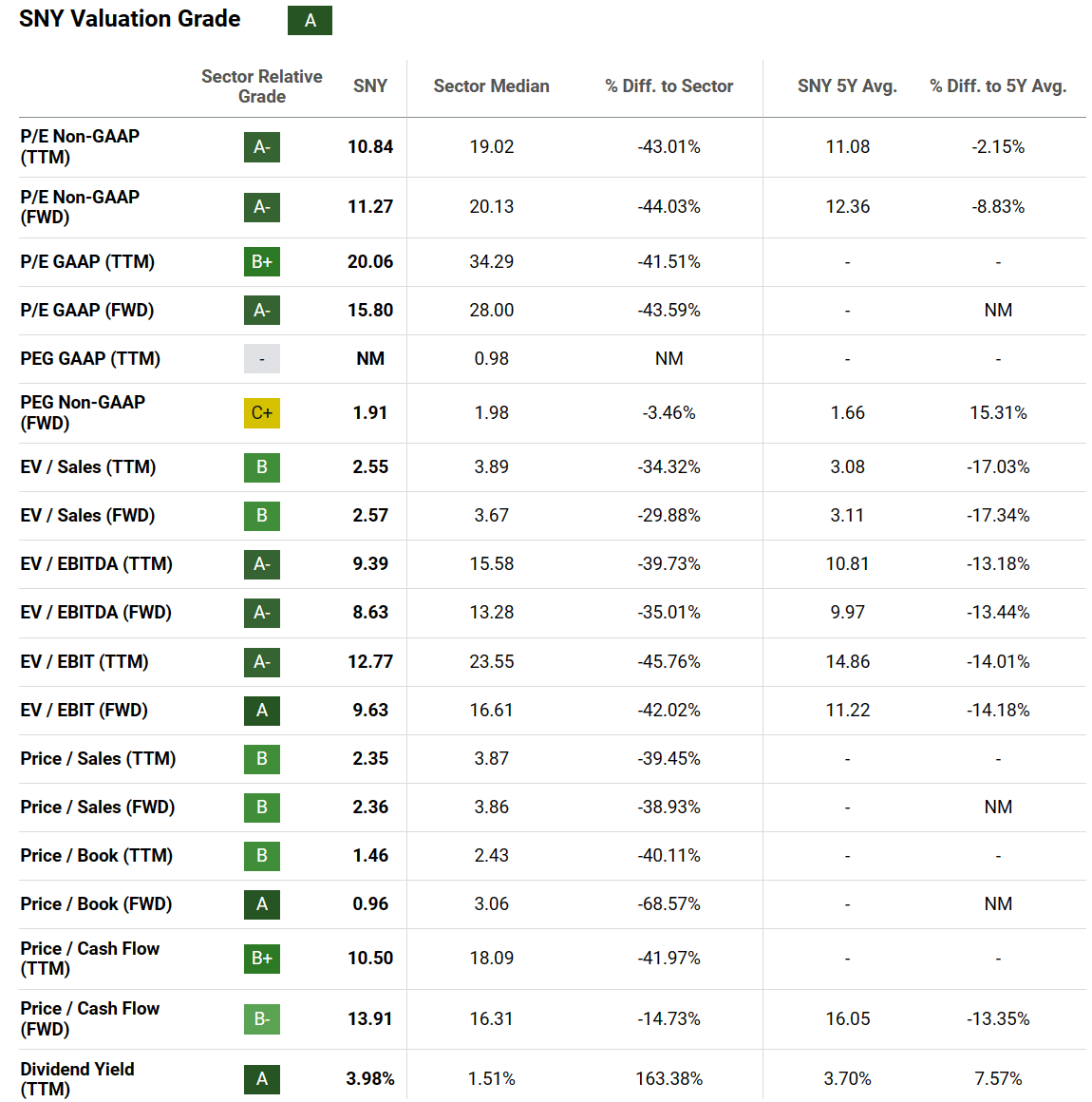

Rounding out my valuation overview, In search of Alpha’s computer-scored Quant Valuation Grade of “A” stands out within the sector. It is the identical optimistic rating as my different two worth favorites within the sector: Pfizer and Bristol-Myers Squibb.

In search of Alpha Desk – Sanofi, Quant Valuation Grade, March twenty first, 2024

Technical Sample

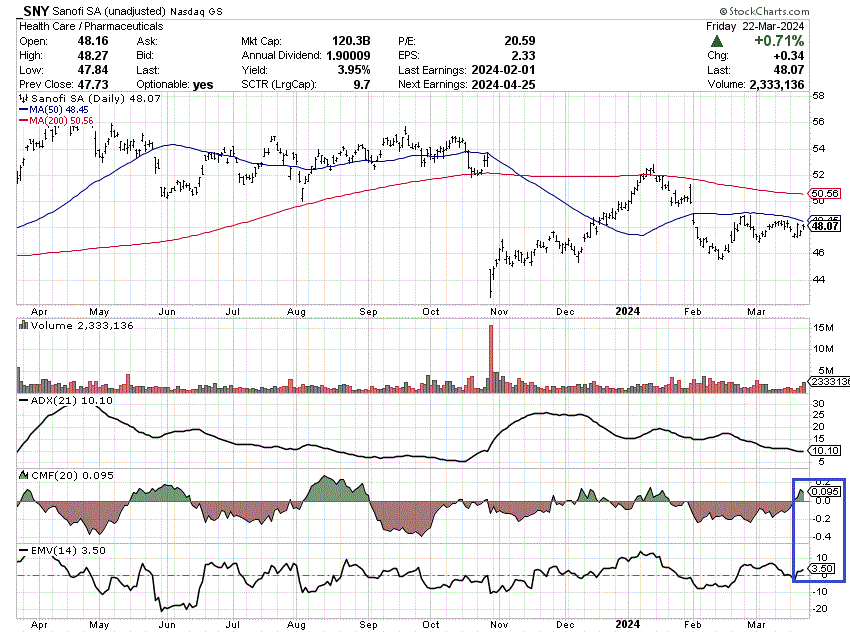

At first look, there’s nothing thrilling to search out on the Sanofi chart of every day buying and selling beneath. Over the previous yr, value has zigzagged decrease, with a big dump in late October on administration’s announcement of weaker-than-expected outcomes and its restructuring as a response.

Nonetheless, hints of shopping for quantity inflows overwhelming sellers are beginning to seem after a interval of consolidating October’s value loss. Actually, in latest days, one thing of an equilibrium in share provide/demand (indicated by the low 21-day Common Directional Index rating of 10) could also be witnessing a bullish flip for the higher for shareholders. I’ve boxed in blue the newly optimistic readings within the 20-day Chaikin Cash Circulate calculation, alongside the 14-day Ease of Motion studying which has been above zero for weeks already. Notice: the growth of shopping for highlighted by these two indicators may be very totally different than the online promoting of early October.

In my analysis, when each CMF and EMV are turning greater, share pricing will observe with features over the following 2-3 weeks about 60% of the time. But, after we add the low ADX rating into the equation, and issue within the inventory’s undervaluation and sizable enchancment in enterprise fundamentals coming quickly, SNY might be prepared for a big upturn in value.

StockCharts.com – Sanofi, 12 Months of Every day Value & Quantity Modifications, Creator Reference Level

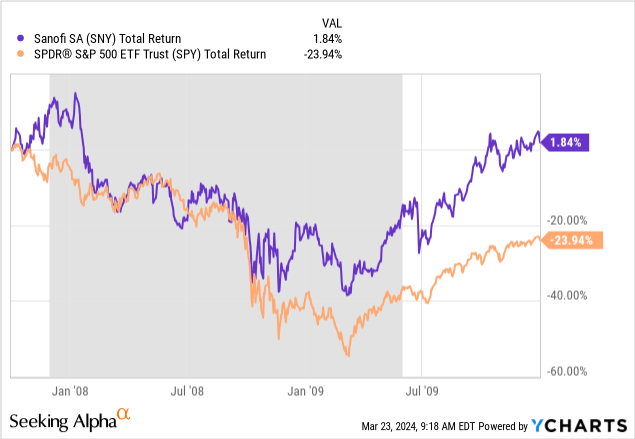

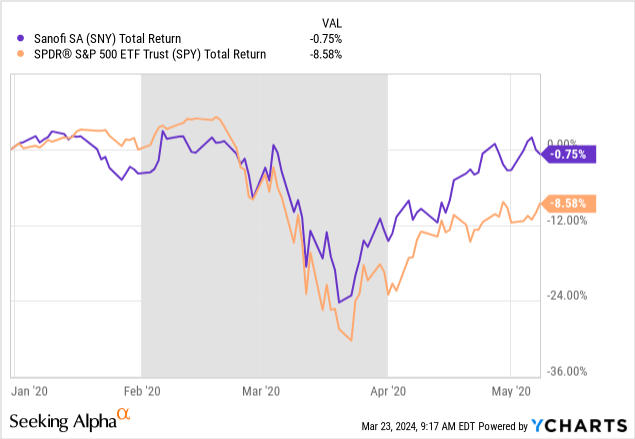

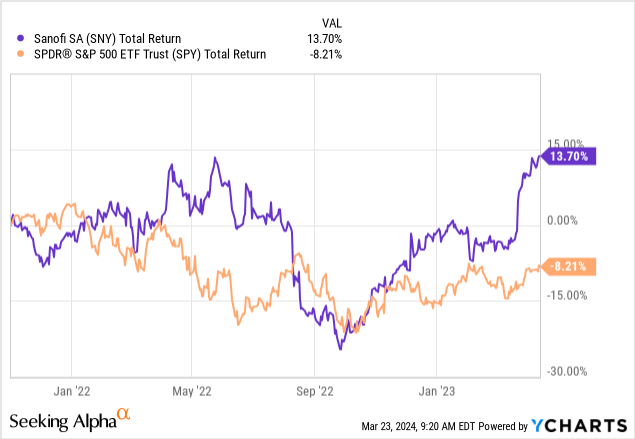

Shares are additionally an attention-grabbing defensive, flight-to-safety decide. Reviewing previous recession and bear market efficiency since 2007, Sanofi has a historical past of outlining barely higher complete returns than the S&P 500, when bother hits the economic system. I’m together with charts of the 2007-09 Nice Recession, first-half 2020 pandemic expertise, and 2022 to early 2023 bear market in U.S. equities.

October 2007 to December 2009

YCharts – Sanofi vs. S&P 500 ETF, Complete Returns, Recession Shaded, Oct 2007 to Dec 2009

January to Might 2020

YCharts – Sanofi vs. S&P 500 ETF, Complete Returns, Recession Shaded, Jan to Might 2020

November 2021 to April 2023

YCharts – Sanofi vs. S&P 500 ETF, Complete Returns, Nov 2021 to April 2023

Closing Ideas

My funding conclusion is Sanofi could have the very best mixture of worth, progress, and dividend traits of all of the Huge Pharma decisions. I imagine the inventory is a best choice within the growth-at-a-reasonable-price [GARP] space of market analysis. The key drug corporations have a historical past of defensive complete returns in recession and bear markets. As well as, it seems SNY patrons are beginning to outnumber sellers in share buying and selling for the primary time since early January.

What are the dangers to your funding in SNY? A slowdown in Dupixent gross sales can be danger #1 to ponder, in my opinion. The corporate is projecting annual gross sales of the drug will develop additional to 13 billion Euros yearly quickly (from a little bit over 10 billion Euros right this moment). If this forecast proves overly optimistic, I doubt analyst revenue projections will show correct.

A normal inventory market crash state of affairs can be main danger #2 to weigh in your resolution course of. Whereas right this moment’s low share valuation ought to assist Sanofi to outperform in common bear market and recession eventualities, a straight down transfer in all shares will have an effect on SNY equally. Do not chuckle however the AI bubble of 2023 and early 2024 has pulled crash odds as much as 10% to twenty% later in 2024 (most years I’d place crash odds effectively underneath 5%).

U.S. fairness market valuations specifically are fairly excessive in March on (1) trendy file value to gross sales for the S&P 500, (2) complete market worth vs. GDP output remaining near 2021’s file excessive, and (3) nosebleed CAPE ratio scores utilizing long-term trailing P/Es. Extremely, buyers appear to be overlooking nonetheless excessive recession odds, successfully placing sky-high valuations on shares close to a peak within the financial cycle. You must return to the unique dot-com Tech bubble peak throughout the yr 2000 or the madness of 1929 to discover a comparable mismatch setup.

In any other case, assuming Dupixent gross sales stay excessive and a inventory market crash is prevented this yr, I anticipate Sanofi to be a profitable and productive funding choice over then subsequent yr or two. I’m putting a Purchase score on SNY, with expectations of good “outperformance” of the S&P 500 over the following 12-24 months.

Thanks for studying. Please take into account this text a primary step in your due diligence course of. Consulting with a registered and skilled funding advisor is advisable earlier than making any commerce.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.