jax10289

Two quarters have handed since I first covered Santander Brasil (NYSE:BSBR) with a Purchase ranking. These have been disappointing six months. The inventory briefly touched above $6.5 on the finish of FY’23, however began to slip down once more as soon as FY’24 began and have dipped even decrease after the discharge of This fall earnings. Notice that Santander trades barely above the worth of my first article in BRL phrases, which means that excluding FX and together with dividends it will doubtless be consistent with the S&P 500. Though I could have been early on my Purchase name, I nonetheless imagine I am proper with my expectations, as we’re nonetheless within the early days of Brazil’s financial cycle.

To start with of my earlier article, I highlighted 4 completely different the explanation why Brazil’s economic system was doubtless turning a nook and that banks can be a few of the key beneficiaries. First, I signaled that the Brazilian Central Financial institution (BACEN) was prone to begin slicing charges in August – which it did, adopted by different cuts in September, November, December and January, bringing the Interest Rate to 11.25% from 13.75%. Second, I anticipated that delinquency had peaked within the 1H’23 and that’s confirmed by the graphs on this article. Third, that inflation would proceed to gradual after hitting 3.16% in June, however, sadly, this one did not occur, and we closed 2023 at 4.62% of inflation. Fourth, that Brazil’s GDP can be even stronger than preliminary projections, which is precisely what occurred as Brazil is projected to have grown close to 3% in FY’23 versus lower than 2% once I wrote my earlier article.

The concept of this piece is to focus on Santander’s This fall earnings, replace among the graphs used within the first article to verify main enhancements within the final two quarters and test if my forecast continues to face. I like to recommend studying my earlier article, in case you have not. In the long run, I keep my preliminary Purchase primarily based on the anticipated Curiosity Charge declines and the increase that may carry to Santander’s Web Curiosity Margin (“NIM”).

An Replace on This fall’24 Earnings

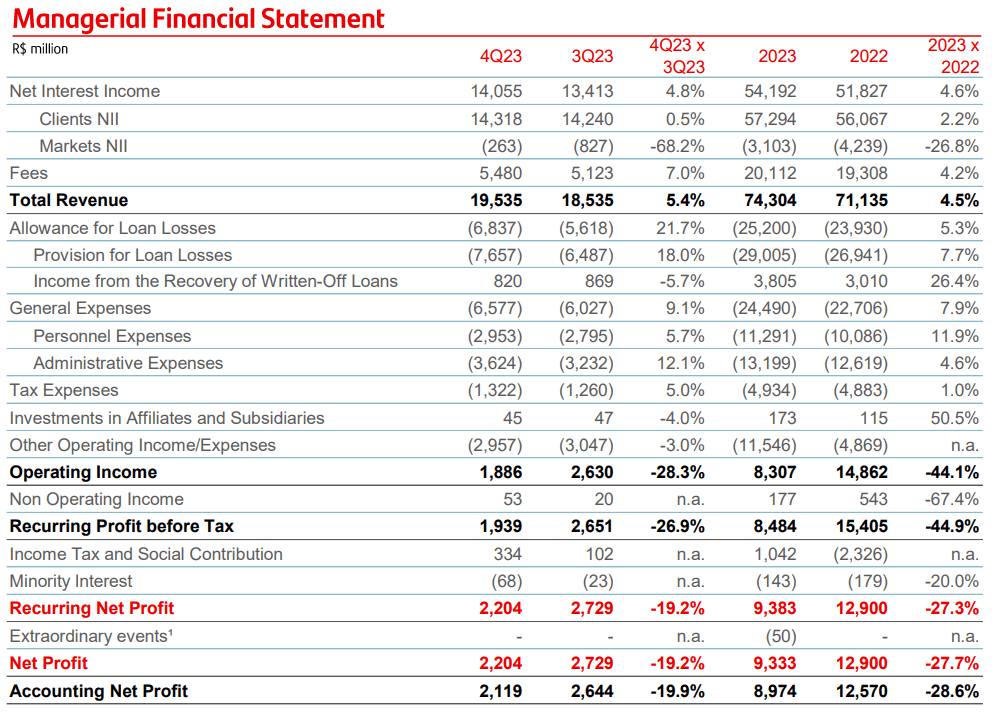

It appears that evidently what wasn’t properly acquired by the market was the earnings miss of R$ 650 million. That was additionally in need of what I anticipated for Santander to finish FY’23, however I anticipated R$ 9.8 billion, and it delivered R$ 9.3 billion, so my variance was a bit lower than versus market expectations. Nonetheless, be aware that this miss wasn’t pushed by Web Curiosity Earnings, which grew YoY by 4.6% and QoQ by 4.8%, however by Provision for Mortgage Losses that grew an surprising 18.0% QoQ.

Santander Brasil P&L FY’23 (Santander IR)

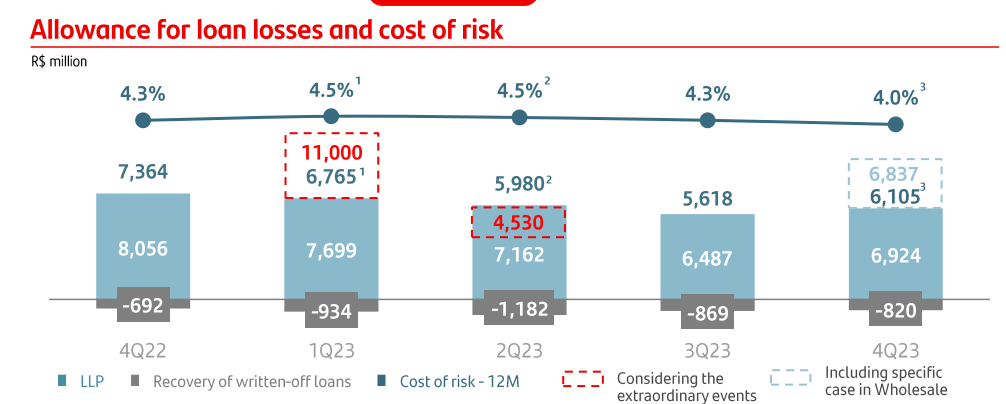

It has been highlighted by administration {that a} “specific case in Wholesale” was accountable for R$ 0.7 billion, making the adjusted quantity for the entire Allowance for Mortgage Losses near R$ 6.1 billion as an alternative of the $ 6.8 billion reported. That’s just about the scale of the miss that drove the inventory down after earnings. The Allowance for Mortgage losses would nonetheless be a rise in comparison with Q2’23 and Q3’23, however a lot decrease than what we noticed all through 2022 and in Q1’23.

QoQ Allowance for Mortgage Losses and Write-Off Restoration (Santander IR)

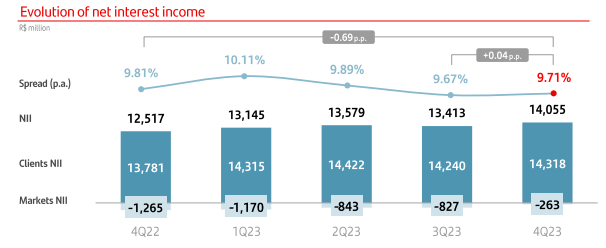

On the optimistic developments, it is vital to notice that Web Curiosity Earnings with shoppers has grown YoY doubtless pushed by decrease rates of interest, regardless of being flat all through FY’23. The lower in Curiosity Charges is critical for Santander as a result of the financial institution attracts numerous its funding from operations with the market. A decrease rate of interest means Santander pays much less for these funds, which could be seen in an enchancment of Markets NII from R$ (1.3) billion in This fall’22 to $(0.2) billion in This fall’23. Thus, Web Curiosity Earnings enchancment of R$ 1.5 billion YoY is pushed by R$ 0.5 billion from extra loans or higher margins to/with prospects and R$ 1.0 billion from decrease prices with funding as a result of lowering rates of interest. This pattern of low rate of interest just isn’t but over as markets proceed to forecast a 9.0% interest rate on the finish of FY’24 which is a big drop to the 11.25% simply introduced on January thirty first.

Web Curiosity Earnings QoQ Development (Santander IR)

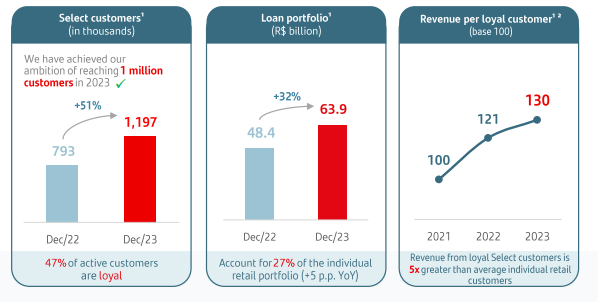

Additionally, it is good to see that Santander has been capable of obtain its objective of 1 million prospects in its Choose section (e.g. higher service for increased charges) as this was one of many key pillars I highlighted for future development. Mortgage portfolio in Choose section additionally exhibits important improve and is meant to be of upper high quality.

Key Efficiency Metrics of Santander Choose (Santander IR)

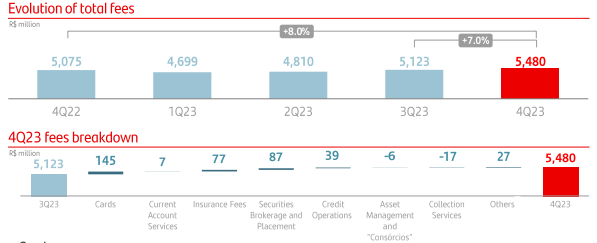

The ultimate optimistic improvement are Charges which have proven 8.0% development YoY. Fundamental drivers of development had been Credit score Playing cards and I can verify empirically that they’ve been very aggressive with bank card acquisition just lately.

Charges QoQ Development (Santander IR)

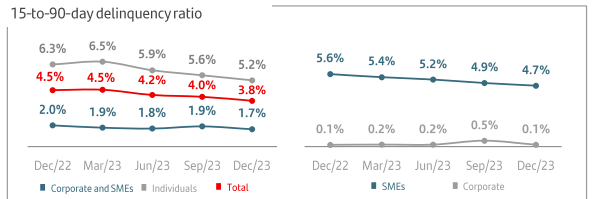

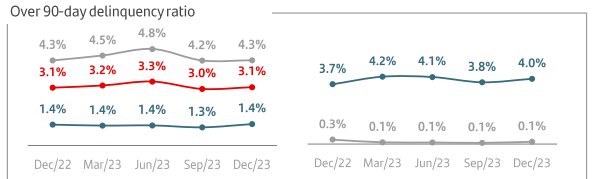

On a combined be aware, delinquency could be seen with optimistic eyes as a result of its continued enchancment within the 15 to 90 Days interval throughout all segments, however with a stabilization within the Over 90 Days interval. Normally, a 15 to 90 Days interval is a number one indicator for future habits within the Over 90 Days, so I might nonetheless anticipate to see a continued downward pattern within the Over 90 Days. Nonetheless, the stabilization may doubtless present that renegotiations weren’t very profitable throughout This fall’23, which can be a unfavorable signal on the economic system.

15 to 90 Days Delinquency Ratio (Santander IR)

Over 90 Days Delinquency Ratio (Santander IR)

Updating My Valuation Mannequin

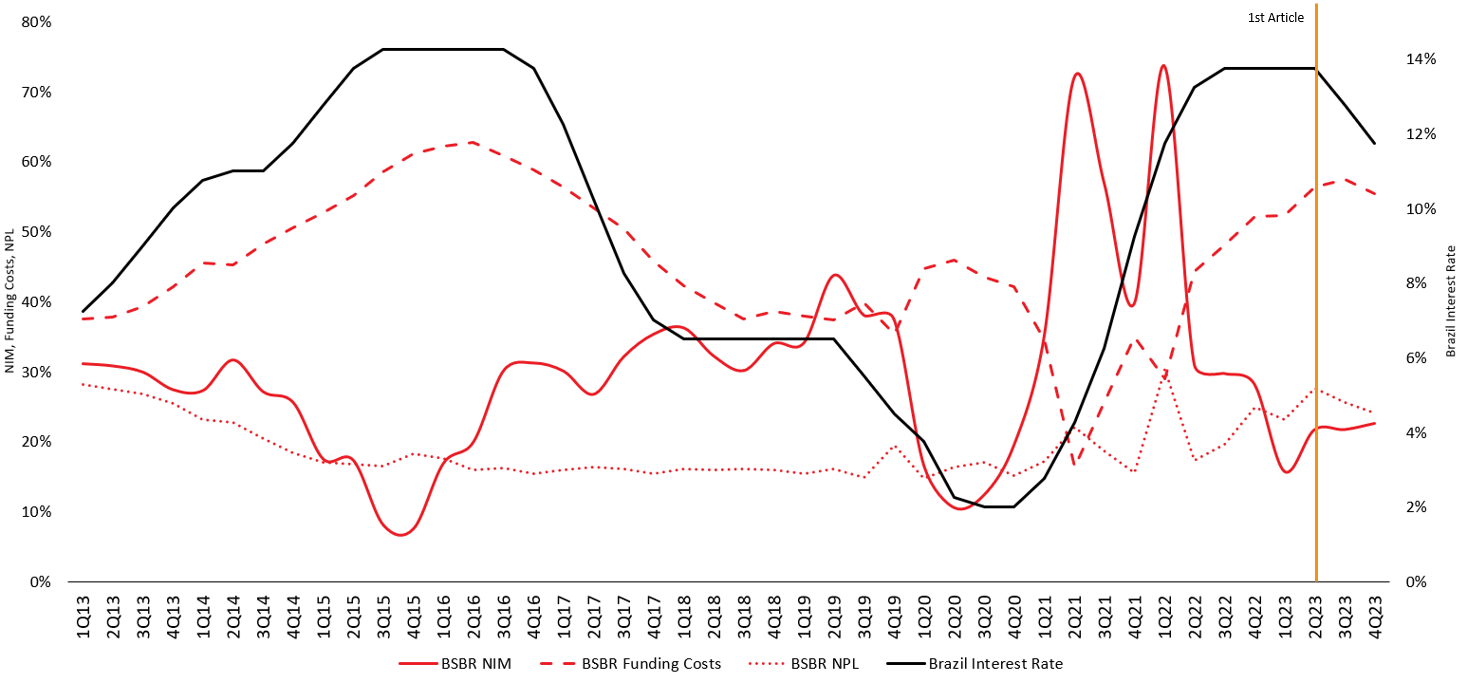

After together with the This fall earnings into my mannequin, I can replace the identical graph introduced in my first article the place I examine Santander’s NIM, Funding Prices and Non-Performing Loans (NPL) with Brazil’s Curiosity Charge. Notice that Curiosity Charge has began to return down on a tempo much like 2016. When Curiosity Charge falls, NIM is anticipated to extend as a result of Funding Prices are anticipated to go down. Though NIM hasn’t proven a big restoration from its backside, Funding Prices have already began its downward pattern.

Santander Brasil NIM, Funding Prices and NPL versus Curiosity Charge (Santander IR, BACEN, Writer)

The rationale why Funding Prices are so vital for Santander is {that a} majority of its funding just isn’t made by Deposits, however with transactions within the open market. These transactions are priced consistent with the Curiosity Charge and are rather more costly than paying curiosity on Deposits. So a lower in Curiosity Charge mechanically decreases Funding Prices for Santander and makes the financial institution extra worthwhile. Within the graph I take advantage of a rolling 12 months to calculate NIM, Funding Prices and NPL to clean out any outlier, but when we overview Funding Prices by quarter the This fall’23 confirmed 50.5% of Funding Prices as % of Income versus 60.9% in This fall’22 when Curiosity Charges peaked. In Q2’22, when charges had been nonetheless mountain climbing and in a stage much like the place it’s now, Funding Prices had been lower than 46%.

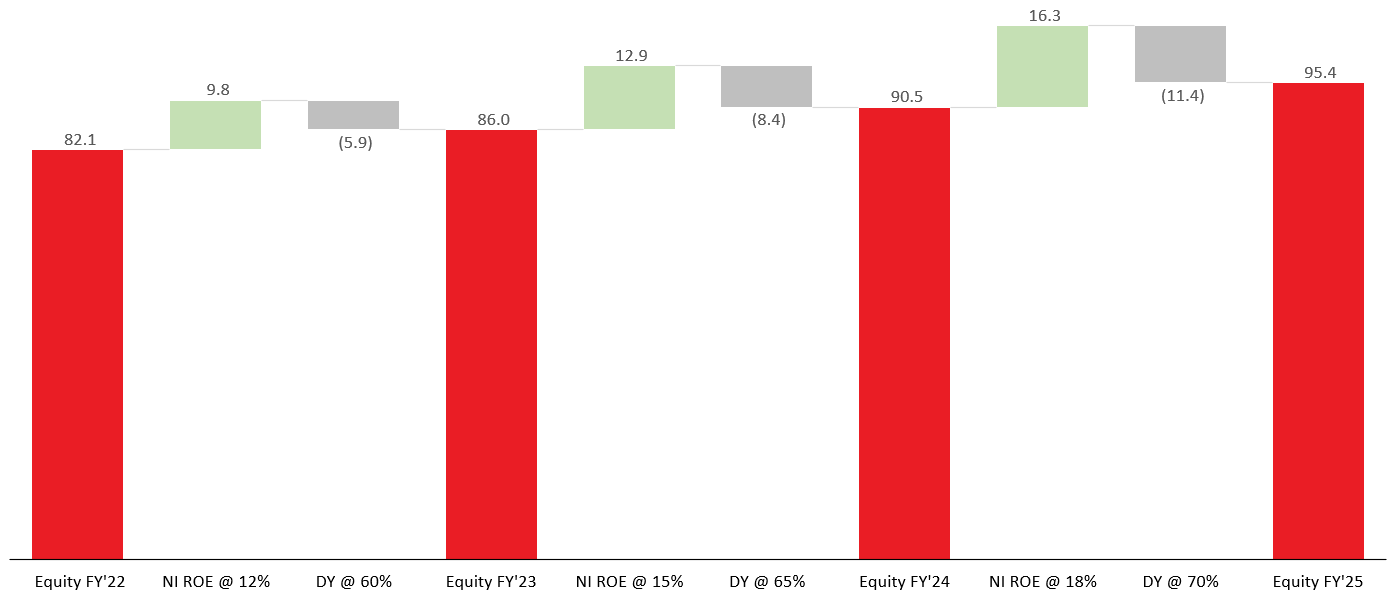

If Funding Prices proceed its descent aligned with declining Curiosity Charges, its % as Income may lower to ranges much like the 2018 and 2019 interval, the place it hovered round 40%. This 10% lower, coupled with an enchancment on NPL, may propel NIM near 30% (once more, much like the 2018 and 2019 interval). A 30% NIM would have meant virtually R$ 6 billion enchancment in Web Earnings on prime of the R$ 9 billion reported in FY’23. This continues to be similar to what I anticipate Santander to attain throughout FY’25 as highlighted within the graph under.

Estimated Santander’s Fairness between FY’22 and FY’25 (Writer)

This is similar graph shared in my first article and though FY’25 appears fairly far, I do not anticipate the markets to rerate Santander solely then. As soon as the quarterly earnings come out throughout FY’24 and level to this NIM enchancment I am forecasting, then Santander Brasil will speed up its motion upwards. Notice that I am sustaining Web Earnings and Dividend in FY’23 as forecast, not Actuals, simply to protect my authentic argument. The Fairness in FY’23 ended at R$ 86 billion, precisely what I utilized in my forecast.

If the investor buys Santander inventory right this moment, they’ll purchase an organization with R$ 86 billion (as This fall’23) in Fairness buying and selling at 1.3 PB. If my expectations of a decrease Curiosity Charge going ahead are right, then we may even see an enchancment of NIM, primarily in Santander’s funding prices with the market, which might gas Web Earnings, ROE, Dividend Yield and an appreciation when it comes to PB. By utilizing my R$ 95.4 billion estimate of Fairness on the finish of FY’25 and a PB of two, market cap goes to virtually R$ 200 billion – the equal of a 75% improve within the inventory worth or near $10.3 USD at a USD/BRL of 5.0. When together with the anticipated 8% to 10% of Dividend that traders might get, we arrive at virtually 40% CAGR on the finish of FY’25.

Last Ideas

In August I highlighted a number of issues that needed to occur earlier than Santander may enhance its financials. Nearly all of them have occurred, however the inventory has but to make a big and sustained motion upward. I anticipate this to occur throughout FY’24 as NIM improves as a result of falling Curiosity Charges. The market remains to be uncertain of Santander’s restoration, however my take is that the primary piece of restoration is because of macroeconomic elements and people are ongoing. The second piece, which might imply Santander pushing in direction of 18% to twenty% ROE, is extra inner and depending on good leads to FY’24. The principle dangers to this thesis are:

- If Curiosity Charges do not proceed to go down. BACEN might discover itself in a troublesome place if the US does not reduce its rates of interest quickly.

- The New Industrial Policy designed by the government and the continued finances deficits may spike inflation again up, which might drive BACEN to extend rates of interest.

- An operational incapacity by Santander to attain high-teens ROE.

- Digital banks discover a strategy to seize company and wealthier shoppers from the massive banks.