Wirestock

Expensive readers/followers,

Banco Santander, S.A. (NYSE:SAN) is an organization that I stay invested in at a mid-level. Since my previous couple of articles on the corporate, this financial institution has posted a really strong efficiency that additionally has seen its valuation climb fairly a bit – and, since my final article, the corporate has outperformed by rising 7% above the S&P500 return of round 6.5%. Not a big outperformance by any means or measurement, however a good efficiency for this financial institution nonetheless.

Above all, I stay excessive in my conviction that this firm’s trajectory going ahead goes to be a constructive one, and that the outcomes introduced by Santander over the previous few months are going to help this considerably increased valuation.

Is that this financial institution probably the most essentially secure monetary play on earth? No, definitely not. That is why this financial institution funding is about half the dimensions of my different monetary investments, and why I am sometimes fairly sluggish including to it – however I nonetheless say that it is a good general funding.

So, on this article, I will replace on Banco Santander, S.A. (SAN) and we’ll see the place we’ve got this financial institution going ahead. You will discover my newest article from August 2023 with the earlier thesis for the financial institution here.

I have been masking this financial institution for over a yr at this level and have remained excessive in my conviction regardless of the volatility within the inventory because of what I imagine to be operational outperformance potential, ensuring this operational outperformance stays possible as the corporate experiences its newest outcomes. My key replace will subsequently be to make sure that this funding nonetheless has the upside that I am on the lookout for.

Banco Santander – An upside of double-digits stays right here

Santander has been a financial institution that just about for the reason that GFC has not carried out all that effectively. 2011 and 2012, it dropped. 2013 til 2019, it just about went nowhere, and in 2020, the earnings crashed once more. Nevertheless, following the COVID-19 disaster, which is after I began investing in Santander, the financial institution appears to have turned over a brand new leaf.

The corporate’s fundamentals are improved. It is now A+ rated. The corporate’s earnings trajectory has been a endless strong story since basically late 2020, with 2021 seeing an 80% EPS enchancment and the present expectation for near double-digit earnings enchancment yearly.

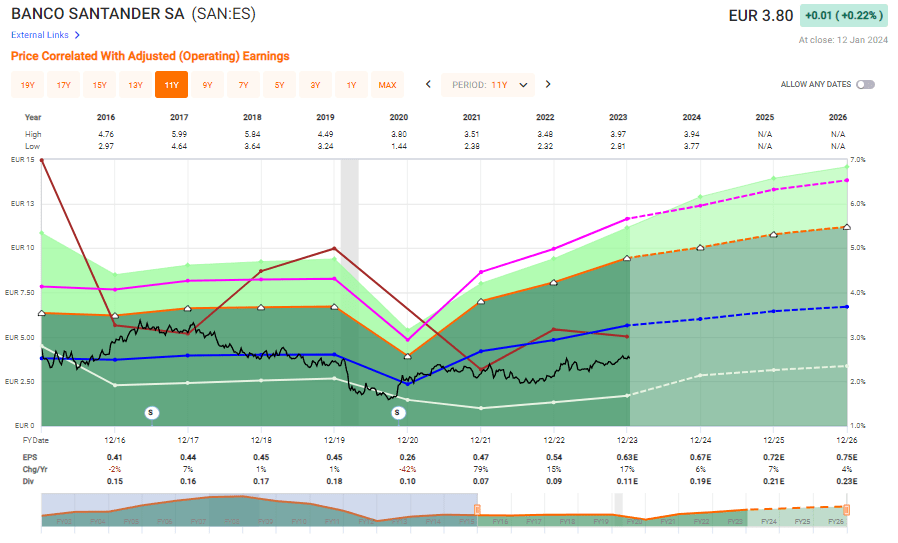

This financial institution has over €60B price of market cap, a complete fairness worth of over €500B, and will, regardless of the low dividend of round 3%, have a complete return potential with a really excessive eventual valuation, as soon as the market normalizes to ranges of 12-13x P/E the place this financial institution has been earlier than.

It at present trades at round 6-7x.

Why do I imagine on this diploma, or degree of normalization relative to at the moment’s valuation? In my work, I put a non-trivial weight to historic averages, particularly over an extended interval, which means 10-20 years. That is how I’ve managed to outperform the market – by investing when valuations for an organization have been effectively beneath historic averages for that firm and the market – ideally each. That is the case for Santander because it stands at the moment – a 6-7x normalized P/E is round half the a number of the corporate has commanded throughout a 20-year common. This may be justified if the corporate was in some kind of longer-term earnings stoop, or a elementary deterioration – however the case is the precise reverse, which we’ll see from quarterly outcomes.

3Q23 is the newest set of outcomes we’ve got (You can find those here) reported in October, and it is a clear and concise continuation of the constructive trajectory we have seen for Santander.

In what approach?

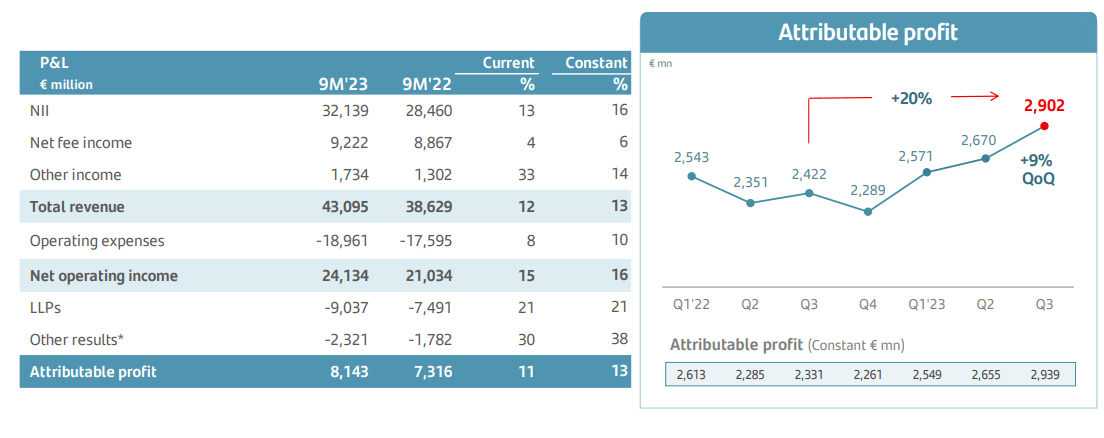

The corporate noticed a YoY 20% enchancment in revenue, 11% on the 9M interval. In order that double-digit enchancment, that is confirmed. The corporate’s RoTE improved by over 125 factors, with a straight, bottom-line EPS enchancment of 17%.

The corporate nonetheless is not a market chief in CET1, however nonetheless has seen enchancment on this as effectively.

Santander IR (Santander IR)

What is that this coming from, except for the plain rate of interest traits? The corporate is rising by way of general buyer revenues, but additionally bettering in effectivity. It is now totally on monitor to ship the 2023E monetary targets of double-digit income development at 13%, and a 44-45% effectivity ratio, with a CET-1 of over 12%.

Most of that is natural development. The corporate additionally improved the dividend, however at these ranges, that’s an absolute given, with the low dividend fee we’ve got at the moment. The corporate additionally combines this dividend return with buybacks and introduced that since 2021 and going with the complete authorization, Santander can have purchased again near 10% of shares excellent, which in fact goes an extended solution to help the present valuation as effectively.

A beaten-down financial institution inventory like this wants to supply constant and unerring proof that it does handle to develop its earnings and different KPIs, and the corporate remains to be solely someplace at the start of that development, as I see it.

However the alerts, for many who wish to look, are all there.

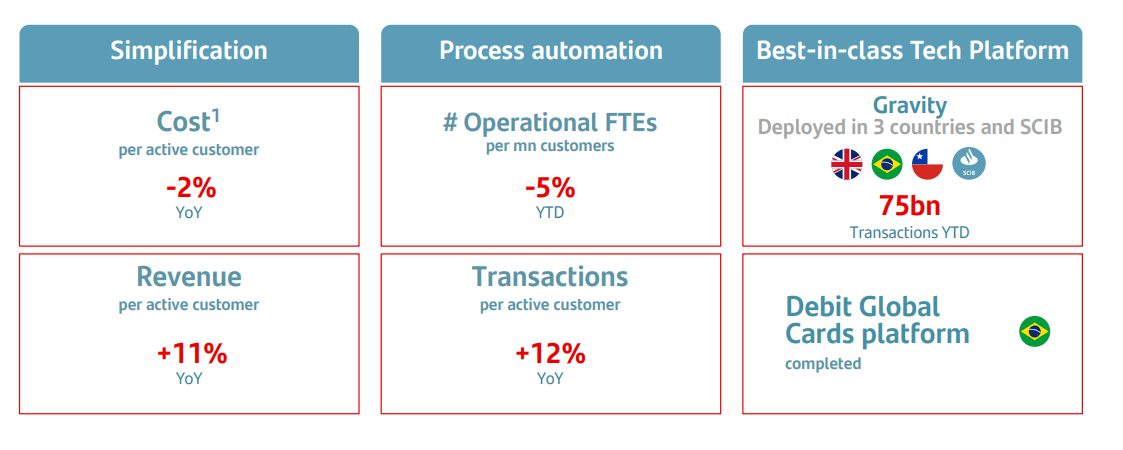

The financial institution is seeing underlying effectivity enhancements with its so-called “one transformation” (a lot of what I see by way of enhancements), which is the core methodology of the corporate driving down prices and driving up different indicators. And that is working wonders on a world scale. This program is what most different banks are doing to enhance their operational effectivity, and it entails a mixture of streamlining inefficient bureaucratic processes, growing digital adoption for sure components of the operations, and as we will see beneath, general ensuring that much less are doing extra, including to the financial institution’s backside line. That is the essence of its “One Transformation”, one other title for what many corporations have been doing for years at this level.

Santander IR (Santander IR)

So long as these enhancements proceed alongside this kind of trajectory, and there aren’t any danger additions for the corporate, I do not see any purpose why this firm ought to see an enormous drop in its valuation – and even when it did, I would not see it as justified right here.

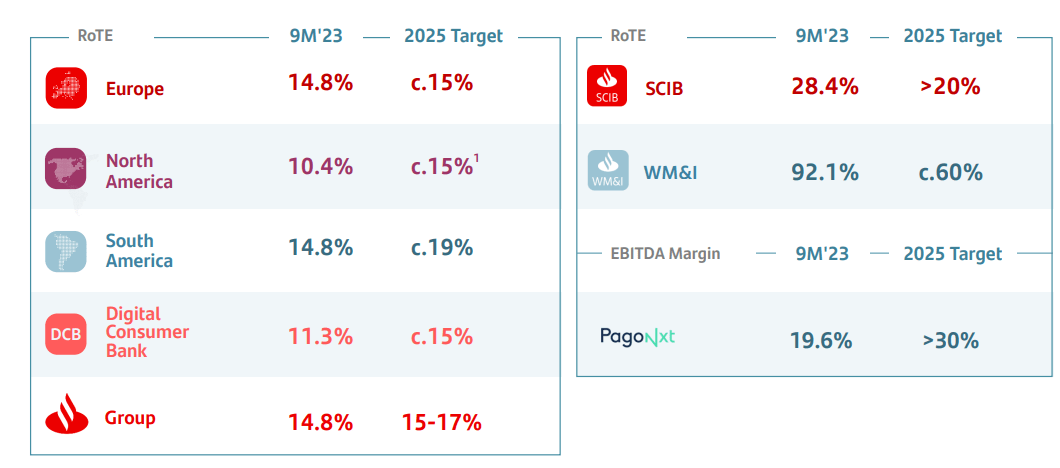

The tempo of income development in lots of of those segments that the corporate is focusing on, reminiscent of the worldwide and community companies, is rising quicker than the group general.

Whereas nonetheless very small in comparison with a section like Auto leases, the place the corporate has over €179B and which is barely falling, the expansion in one thing like WM&I remains to be 22%, rising to €52B.

South America stays one of many firm’s core targets for profitability, with a 19% goal in 2025E, the best in your complete group, and carrying a big a part of that group’s 15-17% goal for the 2025E.

Santander IR (Santander IR)

Total, I don’t see a number of danger on this firm’s most up-to-date outcomes. With each NII and NIM up YoY supported by each volumes and price will increase, South American traits transferring to the constructive sector, constructive jaws from the transformation program (because of this the corporate’s revenues are rising quicker than its prices), and a continued bettering general credit score high quality for the corporate’s loans and portfolios, there are a number of issues to love right here.

Sure, in comparison with different European, and particularly Scandinavian banks, this firm’s NPLs and CoR ratios are at shockingly excessive ranges. NPL for September 2023 was 3.13%, with over €35B at stage 3 and over €1,000B at stage 1. Evaluate this to one thing like Swedish banks, which hardly ever, if ever, rise above 0.5%.

Nevertheless, protection ratios stay strong at over 65%, and that is nonetheless one thing to anticipate on this specific credit score setting. Unemployment stays very low within the firm’s goal geographies, and many of the group’s provisions are associated to retail. Mainly amongst its impacted geographies are Poland, with Brazil bettering, Mexico really at good ranges, and the US according to general expectations.

As I mentioned, this has been an extended journey for Santander going again not less than 5 years – and a troublesome one. Santander popping out of the GFC was in dangerous form, with 2011 earnings happening 31% and at absolute lows. The financial institution then went by way of basically from 2013/2014 to 2020, virtually 6 years with none kind of earnings enchancment, which noticed the share value collapse to the underside of COVID-19 lows, and as soon as once more low EPS. Since then, the corporate has recovered – however the share value, whereas we have seen the start of a journey right here, will not be reflecting these enhancements but.

Santander IR (Santander IR)

I grew to become snug investing in that journey just a few years again when the worth justified it. I have not regretted it since that first funding.

It is essential to contextualize these newest set of ends in the larger and longer image. What I wish to see right here, each quarter, isn’t any indicators of fear within the underlying fundamentals or development prospects. I do not wish to see any of what I think about an important KPIs “fizzle”. If that was the case, I’d revisit my elementary thesis and expectations for this financial institution. For example we had been to see, abruptly, a decline in profitability in among the firm’s main markets, reminiscent of South America or the house market Spain. Given the significance of those markets, this could warrant a far deeper survey of what is driving this deterioration, and if we must always anticipate this to proceed. However to place this quarter within the context of the larger image, it was yet one more affirmation for me that Santander is certainly transferring in the precise course, and to my thesis that the upside is not materialized sufficient within the valuation.

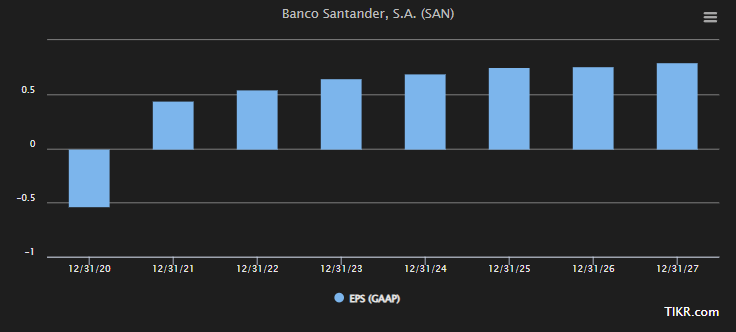

My expectations for FY23, and for 4Q23, which goes to be reported in about 2 weeks, is a robust end to the fiscal. I anticipate additional Internet payment earnings and improved profitability numbers not solely within the European however within the South American markets as effectively. I imagine the corporate will ship on the 2023E targets – because it has communicated that it’s on trajectory to take action. I imagine, moreover, that we’re solely at the start of a cloth EPS enchancment for this financial institution – and I am removed from the one analyst seeing the indicators of underlying enhancements, as most forecasts name for a ~€0.4/share native EPS or thereabout, however one which’s possible to enhance as a lot as to double that inside 4 fiscal years, because the enhancements the corporate is at present executing on mature (Supply: S&P International).

Let us take a look at the dangers and upsides for this specific financial institution.

Dangers & Upside for Santander

The corporate’s long-term traits are far inferior to the shorter-term ones. In truth, my funding in Santander is up greater than 24% in a single yr. I’d categorize the first dangers to Santander as follows.

The apparent danger to the corporate is the heavy LATAM and South America publicity. Irrespective of how even somebody constructive on the area reminiscent of me desires to slice it, it is one of the politically unstable areas in your complete world, maybe aside from sure areas in Africa and the Center East. One other level in that area unfavourable is that these areas aren’t any strangers to large-scale banking collapses – and whereas Santander stays considerably insulated because of its European domicile, it nonetheless has its ft and fingers deep in these geographies. In the event you don’t love LATAM and Southern-American danger, you in all probability ought to rethink Santander.

Santander experiences its outcomes and presents largely in Euro – however the truth that round 70% come not from the eurozone however from overseas forex is one other danger. The corporate stays, regardless of enhancements, very uncovered to rising market forex danger. One more reason I stay solely a relatively smaller place within the firm.

Nevertheless, on the upside, if you happen to’re like me, then this firm operates in high-prospect areas and manages spectacular profitability in comparison with virtually all European friends. Its diversification and deal with retail banking additionally give it an unimaginable quantity of danger spreading, which is a necessity for a participant reminiscent of this one, and when this firm’s portfolio is totally unlocked, then this financial institution may definitely go locations. What I imply by that is that Santander has the potential to basically 1.5-2x its earnings on a GAAP/IFRS foundation if it had been to be as environment friendly a financial institution by way of C/I, credit score high quality, and operations as a few of its European friends. Check out RoTE, Effectivity, and mixed working ratios of the insurance coverage operations, additionally a part of Santander. There is not any doubt to me that that is nonetheless years off, however it’s a possible – and it is on this potential enchancment that I’m investing.

That is how I see this firm’s dangers and upsides.

Santander Valuation

The valuation is in fact a considerably completely different story – as a result of it stays very enticing right here. For example that we forecast the financial institution on the decrease finish of its latest 5-year common, which might come to round 8x P/E, which I imagine to be the bottom we must always enable right here. That is even with the comparatively excessive miss ratio that the financial institution does have below its belt.

Such an estimate goes to 21% per yr, or 76% till 2026, which stays a really strong and market-beating kind of potential RoR. Once more, that is the decrease short-term estimate.

If we had been to make use of 20-year averages, which I’d think about as really being extra correct, then we may see an upside to an 11.2x P/E of 33% per yr, or 137% complete RoR. And this isn’t a wierd or outlandish expectation in any approach, on condition that the corporate traded effectively above this throughout worse development prospects previously.

The explanation why I think about historic averages related right here, so long as they’re in the long run, is that the longer-term 20-year averages embrace each coverage durations with low, and excessive rate of interest durations. Whereas I view it as harmful to take a look at solely a 5-year or perhaps a 10-year common for a financial institution (as an example, Sweden has not seen rates of interest this excessive in extra than 10 years), a 20-year common takes under consideration a wider vary of rate of interest environments, which makes it extra related.

Santander is unstable, and it has the potential to go each up and down in comparatively vital methods. Little question about that. Nevertheless, as issues stand proper now, I view the traits for the bullish view as extraordinarily favorable.

Banco Santander FAST Graphs (FAST Graphs)

That’s the reason, even with the comparatively low yield that Santander nonetheless affords right here of three.66%, I’d not view it as one of the best funding doable by way of security – however definitely secure sufficient with its mixture of fundamentals to weigh up for the dangers from the geographies whereby the corporate is energetic.

S&P International analysts give the corporate a set of targets beginning at $3.6 and going as much as $5.8 with a median of $5.2. The corporate at present trades at $4.12. I give the corporate a value of $4.2, not less than in my final article. Unpacking this value goal, in the case of banks, I am just a few multiples. E-book worth multiples are extra helpful than with different corporations, particularly given the insurance coverage operations as a result of it helps us decide how a lot we’re paying for the financial institution’s property relative to historical past and relative to the sector. EBITDA multiples are ineffective – P/E nonetheless has some worth, however e-book multiples are increased on the record right here (although, ideally, we use a mixture of them). Santander, for the native, trades at a 15-year P/B common of 1.6x, with a excessive of 6x, and a low of 0.4x. It is at present at round 0.8x. Even if you happen to restrict the comparability to the post-GFC period, the financial institution remains to be undervalued in comparison with a 1.25x – particularly given the financial institution’s vastly improved credit score high quality since that point, in addition to the operational security. However the unpacking of the e-book worth additionally explains why, whereas I say the financial institution can double in P/E, my value goal doesn’t indicate a “doubling”, however quite a extra modest upside – as a result of I work extra with P/B in the case of these corporations.

Whereas I do see additional upside to this financial institution and will improve my goal given the newest set of positives, I am not doing that till I see the 4Q outcomes – so for now, I am retaining my goal “steady” right here, with a strong “BUY” however with a low upside to my present PT. I am ready to bump my goal right here if I see additional upside, however in the intervening time, I give the corporate round 1-1.1x P/B within the goal vary, and upwards of not less than 8-9x P/E, in comparison with the present native P/E of round 6x. This takes into consideration as effectively, what I think about to be an enormous outperformance potential based mostly on earnings – check out what S&P International analysts expect over the following few years, which is a part of what I base my upside on.

Santader EPS Estimates (S&P International/TIKR.com)

Right here is my up to date thesis for 2024.

Thesis

- Santander is among the higher banks discovered within the Southern European space and geography. It has vital rising market publicity, which provides it a heightened danger profile in context to different banks – however it’s additionally immensely qualitative, as evidenced by the way it has survived earlier downturns.

- I think about Santander a “Buy” at low-cost valuations, and I imagine this financial institution can ship vital upside over time – and now’s a kind of occasions.

- I imagine the corporate’s thesis and potential have improved since my final article, and I proceed so as to add shares, albeit at a decrease price than another banks.

- I stay for Santander at a PT of $4.2/share, a share value improve, and provides it a “Buy”.

- This thesis has been up to date for 2024, and I stay constructive right here.

Bear in mind, I am all about:

-

Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – corporations at a reduction, permitting them to normalize over time and harvesting capital good points and dividends within the meantime.

-

If the corporate goes effectively past normalization and goes into overvaluation, I harvest good points and rotate my place into different undervalued shares, repeating #1.

-

If the corporate would not go into overvaluation, however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

-

I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

- This firm is general qualitative.

- This firm is essentially secure/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is at present low-cost.

- This firm has a practical upside based mostly on earnings development or a number of expansions/reversions.

Regardless of a 7% RoR since my final article, I think about the corporate fulfilling all of my standards – it is enticing right here.

![[BREAKING] 20-year veteran reportedly performed with AEW after Worlds Finish, may return…](https://whizbuddy.com/wp-content/uploads/2024/01/7eecd-17039828746000-1920-600x600.jpg)