Nikada

Saratoga Funding Corp (NYSE:SAR) is a enterprise improvement firm or BDC with a fairly standard focus – i.e., investing and issuing loans to the decrease finish of the center market firms which are already money movement constructive with annual gross sales between $8 and $250 million, and EBITDA north of $2 million.

Whereas that is the core enterprise, SAR has additionally made allocations by way of separate subsidiaries into collateralized mortgage obligations or CLO funds. Plus, SAR has stepped right into a three way partnership with different companions in managing some further quantity of CLOs.

It’s not unusual for BDCs to hold an publicity in direction of CLOs as this fashion a component of diversification together with enhanced return prospects is captured. With that being stated, that is one thing that’s price factoring into the equation earlier than probably going lengthy SAR.

Moreover, when SAR we have now to acknowledge the truth that it is among the smallest BDCs on the market with an NAV of ~ $360 million that’s approach beneath the sector mean of ~ $1.4 billion. I’ll elaborate on this beneath, however, in essence, I’d contemplate this as an obstacle within the context of the prevailing market surroundings.

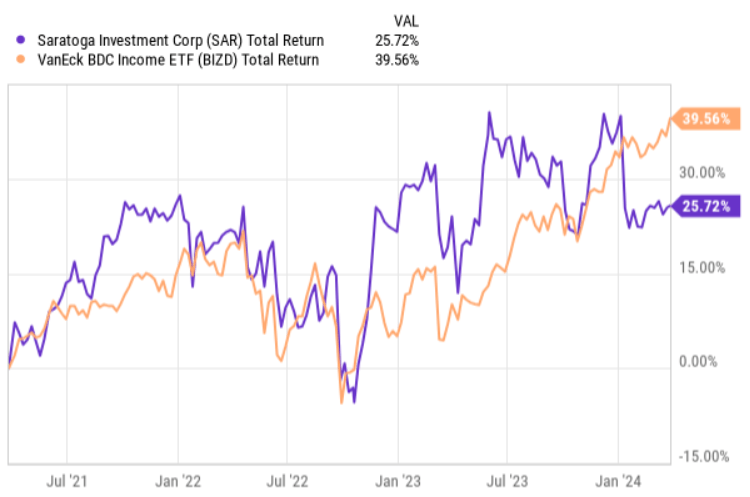

From the full return perspective, SAR has been fairly constant in outperforming the general BDC marketplace for the bigger a part of the trailing three-year interval. Nonetheless, on a YTD foundation, SAR has significantly lagged behind the index, experiencing ~10% value drop as a result of unfavorable Q3, 2024 earnings result.

Ycharts

Let’s now assess the underlying particulars of SAR and attempt to decide whether or not the latest divergence from the BDC market gives a sufficiently engaging alternative to purchase the BDC.

Thesis

Beginning with the fundamentals, there are three distinct structural points which are price highlighting.

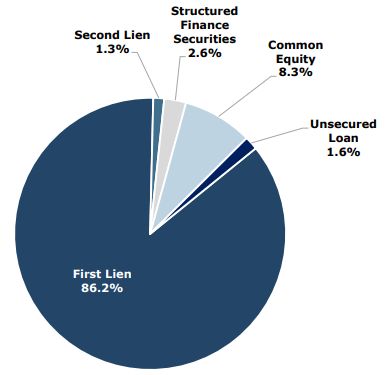

First, the core portfolio of SAR is closely skewed in direction of first-lien bucket with the remaining chunk largely being defined by the allocations into frequent fairness.

SAR Investor Presentation

What this does is it injects an essential layer of security, the place within the case of a broader company misery and even formation of non-accruals within the portfolio, SAR enjoys bigger possibilities of recovering the invested capital.

Right here it is usually price noting that the CLOs do probably not play an essential position within the context of general portfolio and yield era, which helps de-risk the state of affairs additional.

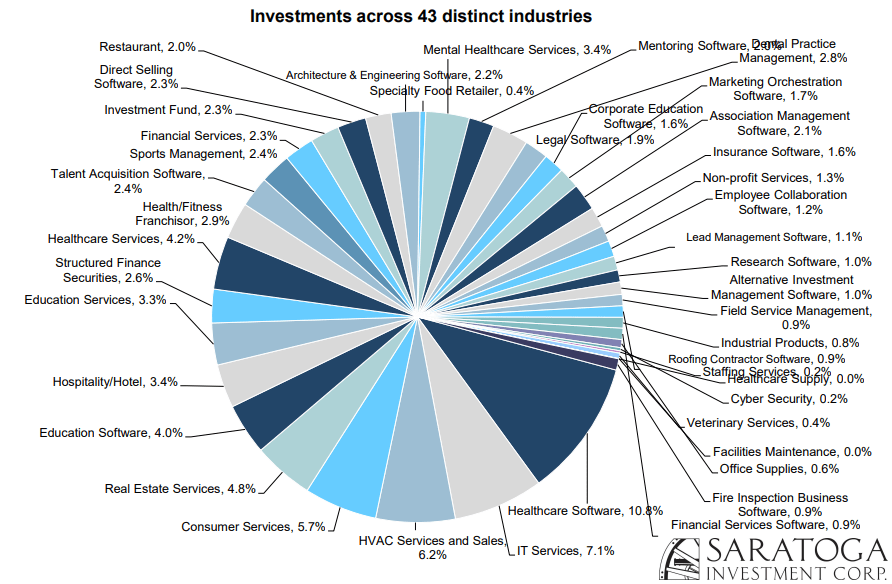

Second, portfolio diversification is robust and significantly distributed amongst many industries. Trying on the chart beneath, we will see that the most important business publicity is related to funding within the healthcare software program firms that collectively account for round 10% of the portfolio worth.

SAR Investor Presentation

Having this type of diversification along side the give attention to already cash-flowing companies is once more a stable signal of the underlying energy/resiliency within the portfolio.

Third, the borrowings or exterior leverage half takes the other way from the 2 aforementioned points. In different phrases, as of now, SAR is essentially the most indebted BDC on the market with a debt to fairness exceeding 220%, which is roughly 103% above the sector common. The second most indebted BDC has a debt-to-equity ratio of ~180%.

Apart from the clear dangers this degree of leverage brings (e.g., magnified losses within the case of non-accruals, big sensitivity to the financial downturn), the construction of underlying borrowings is one thing that positively deserves consideration.

The lion’s share of SAR’s borrowings are assumed at fastened charges that presently are beneath the market-level value of debt. The maturity dates differ relying on the instrument, however the bulk of excellent borrowings will mature within the upcoming 2-3 yr interval, thereby triggering curiosity expense convergence to the market degree charges. Granted, it could possibly be that by that point rates of interest will already be down into accommodative territory which might in flip assist SAR keep away from affected by a large surge in financing prices. But, there’s additionally an honest chance that this isn’t the case. In such an occasion, we may count on a large wave of headwinds for SAR’s NII era going ahead.

Why SAR has diverged from the index?

Now, the important thing purpose why SAR’s share value reacted because it did as soon as the earnings got here out is two-fold.

One of the vital essential metrics measuring BDC efficiency – adjusted NII – decreased in comparison with final quarter. The sequential quarterly per share lower equated to $0.07, which stemmed from the notable fairness issuance that SAR performed throughout the latest quarter. The attraction of further fairness was made with the goal of reducing the leverage profile.

The disagreeable issue on this context was that these incremental shares had been issued at a large low cost to the NAV as SAR trades roughly 20% below its fair value. For the present shareholders, this means value-destructive dilution. Additionally, if we take a step again and put ourselves in administration’s footwear, we will simply consider how important it was (and nonetheless is) to cut back the monetary threat within the system.

The second driver behind the decreased share value was the truth that throughout Q3’24, SAR originated no new portfolio investments. This sends an uncomfortable sign on SAR’s potential to navigate the present surroundings, the place there are basically depressed capital markets and M&A exercise that might gasoline the portfolio development of BDCs or no less than defend the present ranges. For BDCs, it is very important have a big asset base from which to seize spreads between low-cost value of capital and attractive portfolio yields. On this state of affairs, dimension issues, the place SAR has no benefit.

The underside line

Saratoga Funding Corp is an fascinating funding case. On the one hand, it has the required traits on the basic degree for being thought of a pretty funding play (e.g., diversification, bias to first-lien, and cash-generating companies). But, however, it carries structurally unfavorable points that improve the general threat degree dramatically. The truth that SAR has the very best leverage in the complete BDC area, whereas additionally being one of many smallest gamers (from the NAV perspective) introduces an excessive amount of threat. Specifically, it’s not the fitting time to go lengthy SAR, when a protection stance is most well-liked given the backdrop of a coordinated uptick in BDC non-accruals and extra shallow web funding volumes throughout the board.

In mild of this, my advice is to keep away from (maintain) Saratoga Funding Corp. I’d not quick it because the inherent leverage in SAR may, with any constructive dynamic on the sector degree, trigger a significant leap within the inventory value.