SHansche/iStock through Getty Pictures

Introduction

Secure Bulkers (NYSE:SB) is one other mid-size bulk provider firm. It’s an thrilling proposition with its fleet of 46 vessels at a mean age of ten years. Twenty-two ships are geared up with scrubbers, and 100% have a ballast water remedy system. SB has a strong stability sheet with 57% whole debt to fairness and 68.4% whole liabilities to whole belongings. The corporate has high margins and returns in comparison with similar-sized firms. It pays dividends with 4.77% yields and, in November 2023, introduced its inventory buyback program. The corporate is undervalued, given its previous multiples and in comparison with its friends. SB is considered one of my high picks within the bulker carries phase, and I give it a powerful purchase score.

SB overview

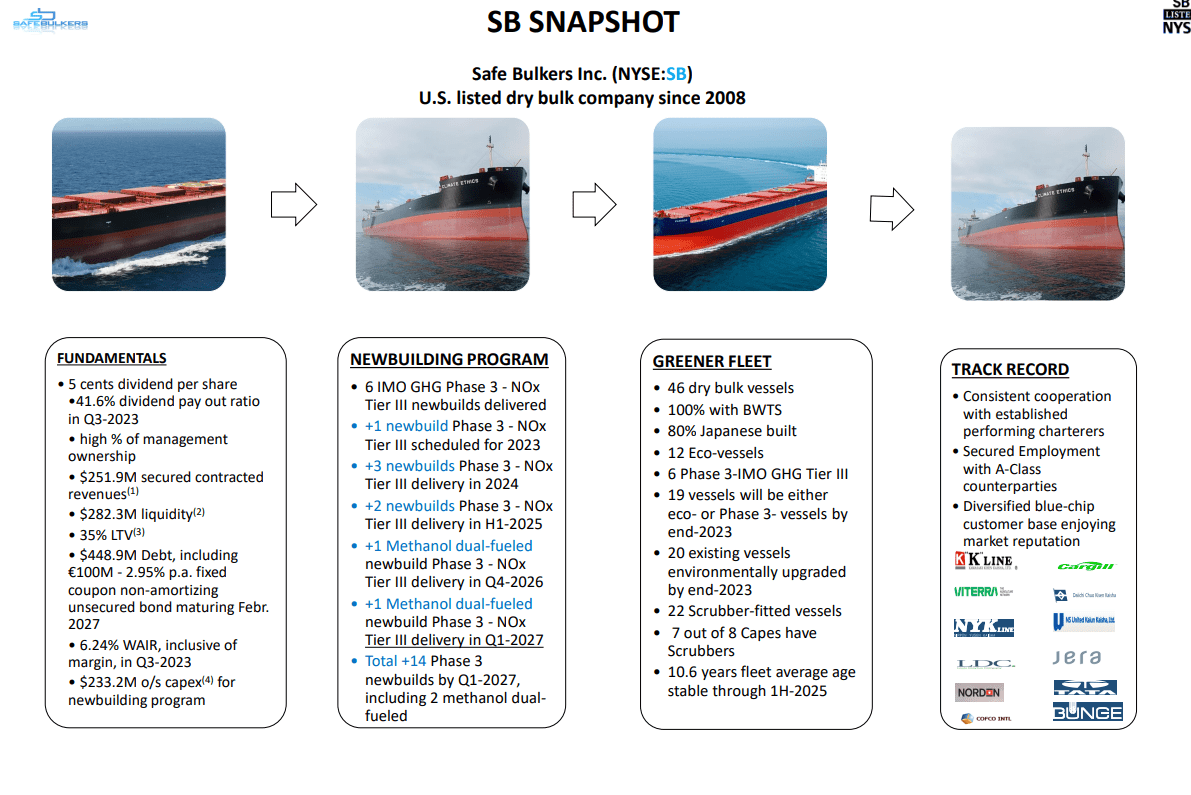

In my view, SB is among the finest bulker firms to play the present bull cycle. Let`s take a look at firm particulars to see why. The chart beneath from the final presentation exhibits SB at a look.

SB presentation

SB has a extra intensive fleet, proudly owning 46 ships, than similar-sized firms. They’re properly scattered throughout numerous sizes: 10 Panamax, 10 Kamsarmax, 18 Put up Panamax, and eight Capesize.

SB is targeted on time charters as an alternative of voyage or bareboat charters. In 3Q23, 15 of its ships had been operated beneath spot time charters for as much as three months. The remaining vessels had been contracted beneath interval time charters longer than three months. Eleven of the ships have chartered for greater than two years. Nonetheless, the typical TC period throughout the fleet is 0.7 years.

In a earlier article on Pangaea Logistics (PANL), I mentioned the professionals and cons of voyage and time charters. Within the case of PANL, voyage charters work completely as a consequence of their distinct fleet of ice-class vessels. They serve particular commerce routes exterior of the usual bulker voyages. Nonetheless, SB owns standard-type ships touring throughout the globe. Which means there may be extra publicity to geopolitical dangers, and, as we all know, the delivery enterprise advantages from rising world tensions.

We now have a looming disaster within the Purple Sea and a drought within the Panama Canal. The latter is extra essential for bulkers. SB fleet is completely positioned to profit from these disruptions within the provide chain. Working approx 30% of its ships beneath spot time charters exposes the corporate to day charges of parabolic progress.

The corporate has made vital progress in NOX and SOX emissions, having 22 vessels geared up with scrubbers. This represents 47% of the corporate`s fleet. For reference, solely Genco Shipping (GNK) has an identical share (37%), though decrease.

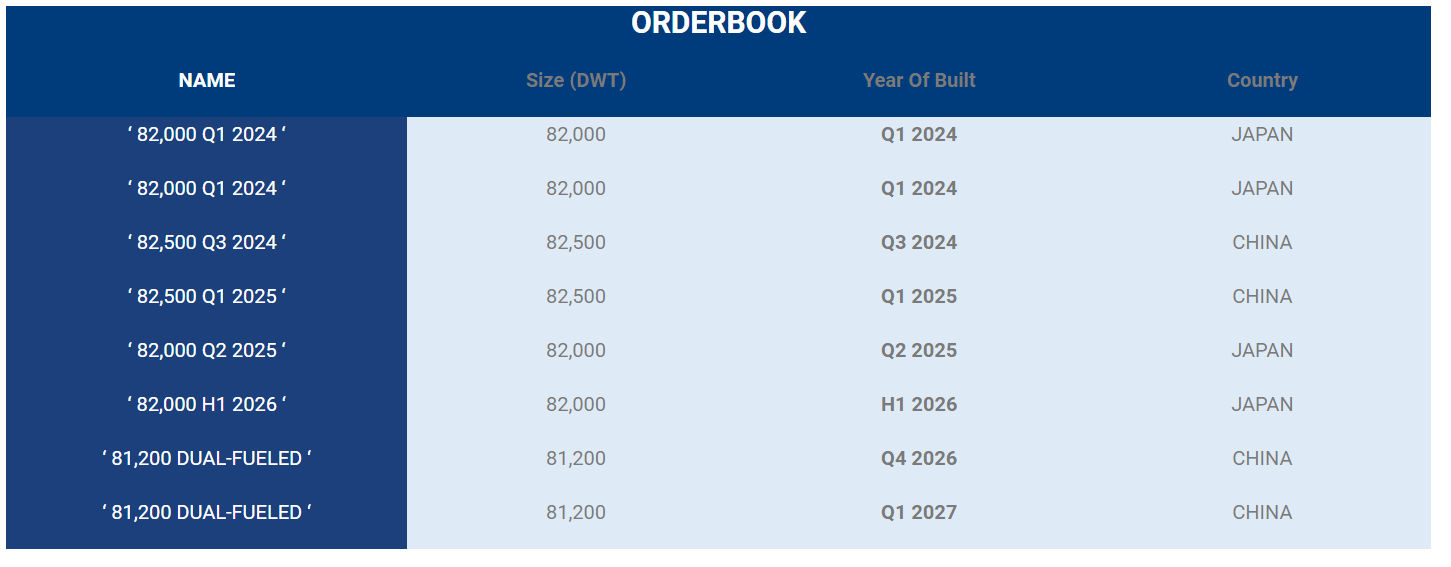

SB expects the supply of 8 new vessels within the coming years.

SB presentation

Three are anticipated to be delivered in 2024, two in 2025, one in 2026, and one in 2027. Two of the ordered ships are methanol twin gas. 3Q23, the corporate received two new Kamsarmax ships: MV Pedhoulas and MV Morphou. Each vessels cowl the IMO Regulation 13 for nitrogen oxide emissions (NOx).

SB stability sheet

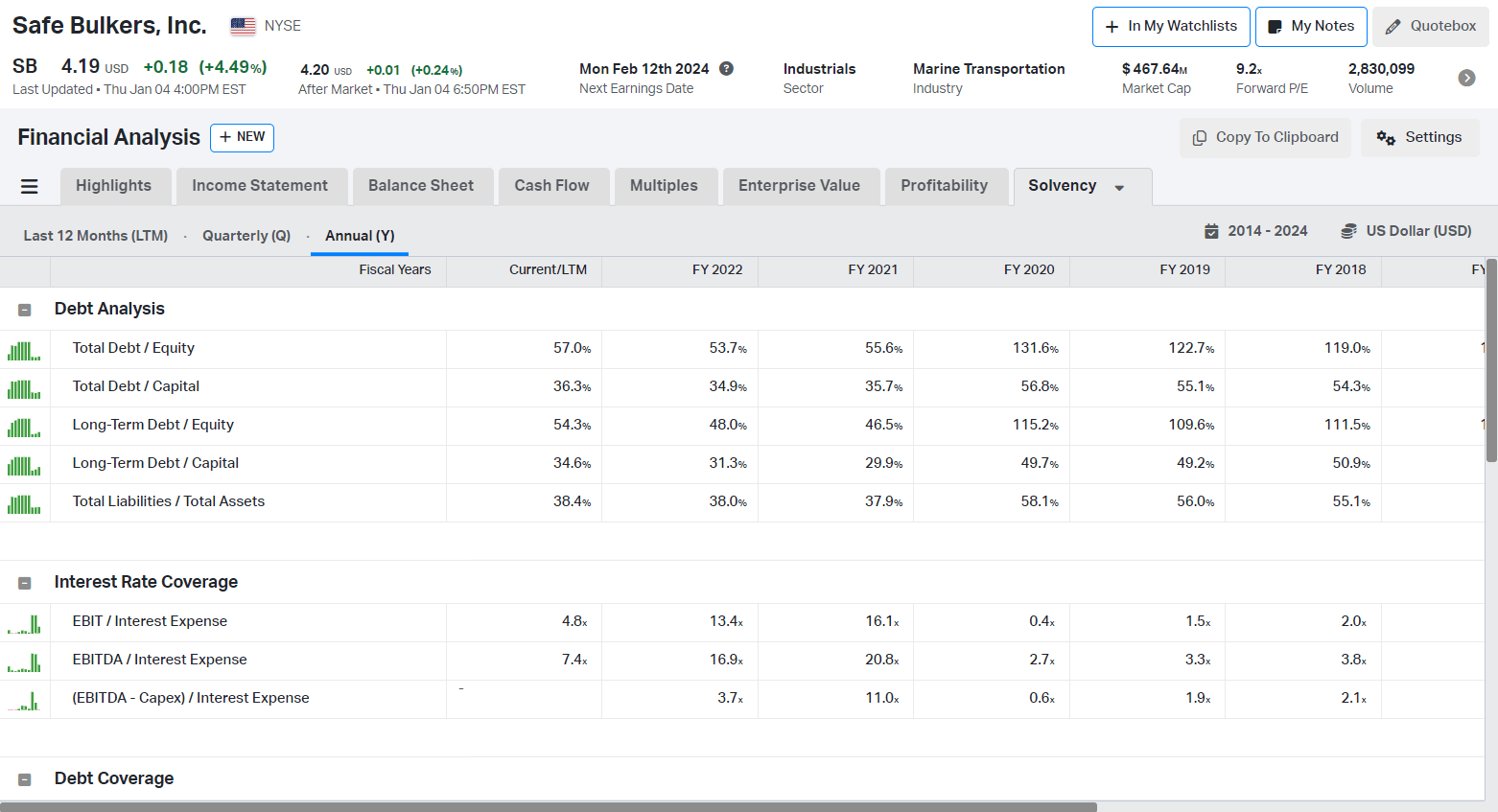

Regardless of the fixed capital funding in updating its fleet, SB maintains a wholesome stability sheet with 57% whole debt to fairness and 37.4% whole liabilities to whole belongings. The desk beneath exhibits SB’s capital construction and curiosity protection.

Koyfin

The progress through the years is important. The corporate decreased its leverage by greater than 100%. In 2020, SB had 131 whole money owed to fairness and 58% whole liabilities to whole belongings. Even on the backside of the cycle in 2020, SB curiosity protection was 2.7.

Let`s evaluate just a few similar-sized firms with SB:

- Secure Bulkers (SB) $74 million money; $440 million whole debt; 0.17 money to whole debt ratio, whole debt to fairness 57%

- Pangaea Logistics (PANL) $87 million money; $275 million whole debt; 0.31 money to whole debt ratio, whole debt to fairness 73%

- Diana Delivery (DSX) $173 million money; $657 million whole debt; 0.26 money to whole debt ratio, whole debt to fairness 135%

- Grindrod Delivery (GRIN) $71 million money; $168 million whole debt; 0.42 money to whole debt ratio, whole debt to fairness 60%

- Genco Delivery (GNK) $48 million money; $141 million whole debt; 0.33 money to whole debt ratio, whole debt to fairness 15%

SB has the bottom cash-to-total debt ratio. However, the debt-to-equity ratio is the second lowest within the peer group.

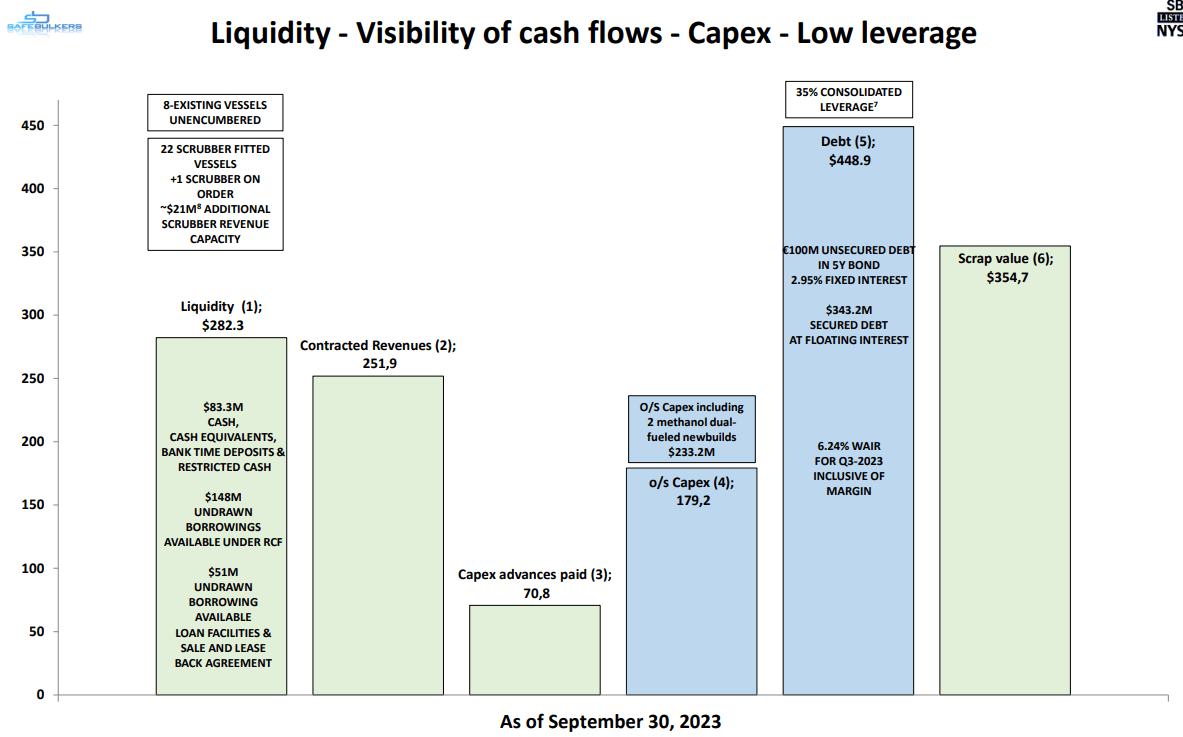

The next desk exhibits the SB liquidity place:

SB presentation

SB has $83 million money, $148 million undrawn borrowings from the revolving credit score facility, and $51 million undrawn from mortgage services and Sale and lease again agreements. In different phrases, the corporate has sufficient liquidity to cowl its operations and capital prices.

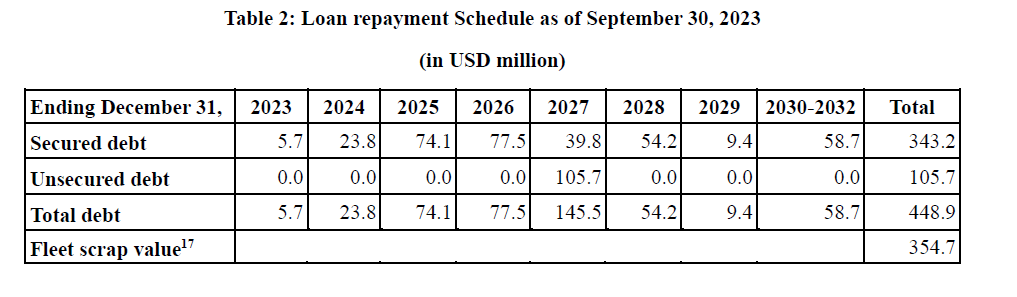

SB has a $448 million debt. The debt is distributed between $100 million 5Y bonds and $343 million secured debt. The previous will mature in February 2027, and the rate of interest is 2.95%. The debt reimbursement schedule is proven beneath:

3Q23 assertion

In 2023, SB should cowl $23.8 million of its secured debt. 2025 SB should pay $77.5 million; in 2026, $74.5 million; and in 2027, $145.5 million. SB has sufficient liquidity and has proven its capacity to generate money flows through the cycle. The corporate generated $217 million in operational money circulate in 2021, $218 million in 2022, and $193 million in 2023 (for 9 months).

SB profitability

Within the record beneath, I evaluate SB’s profitability metrics towards its friends:

- Secure Bulkers (SB) 62% gross margin, 52% EBITDA margin, 11.1% ROE, 5.1% ROTC

- Pangaea Logistics (PANL) 21% gross margin, 17% EBITDA margin, 11.4% ROE, 5.2% ROTC

- Diana Delivery (DSX) 65% gross margin, 49% EBITDA margin, 14.4% ROE, 6.0% ROTC

- Grindrod Delivery (GRIN) 29% gross margin, 7.8% EBITDA margin, (3.5)% ROE, 1.0% ROTC

- Genco Delivery (GNK) 36.5% gross margin, 26.3% EBITDA margin, 1.2% ROE, 3.71% ROTC

SB and DSX have the very best revenue margins and returns. Because the figures above present, working at a spot-time constitution market in a bull cycle is a dangerous however helpful endeavor.

The desk beneath exhibits how SB’s profitability developed during the last 5 years.

Koyfin

SB had detrimental returns solely in 2020 on the backside of the cycle. For the reason that firm has realized respectable margins and returns. In 2021 and 2022, when the day charges recovered, SB had strong returns and margins.

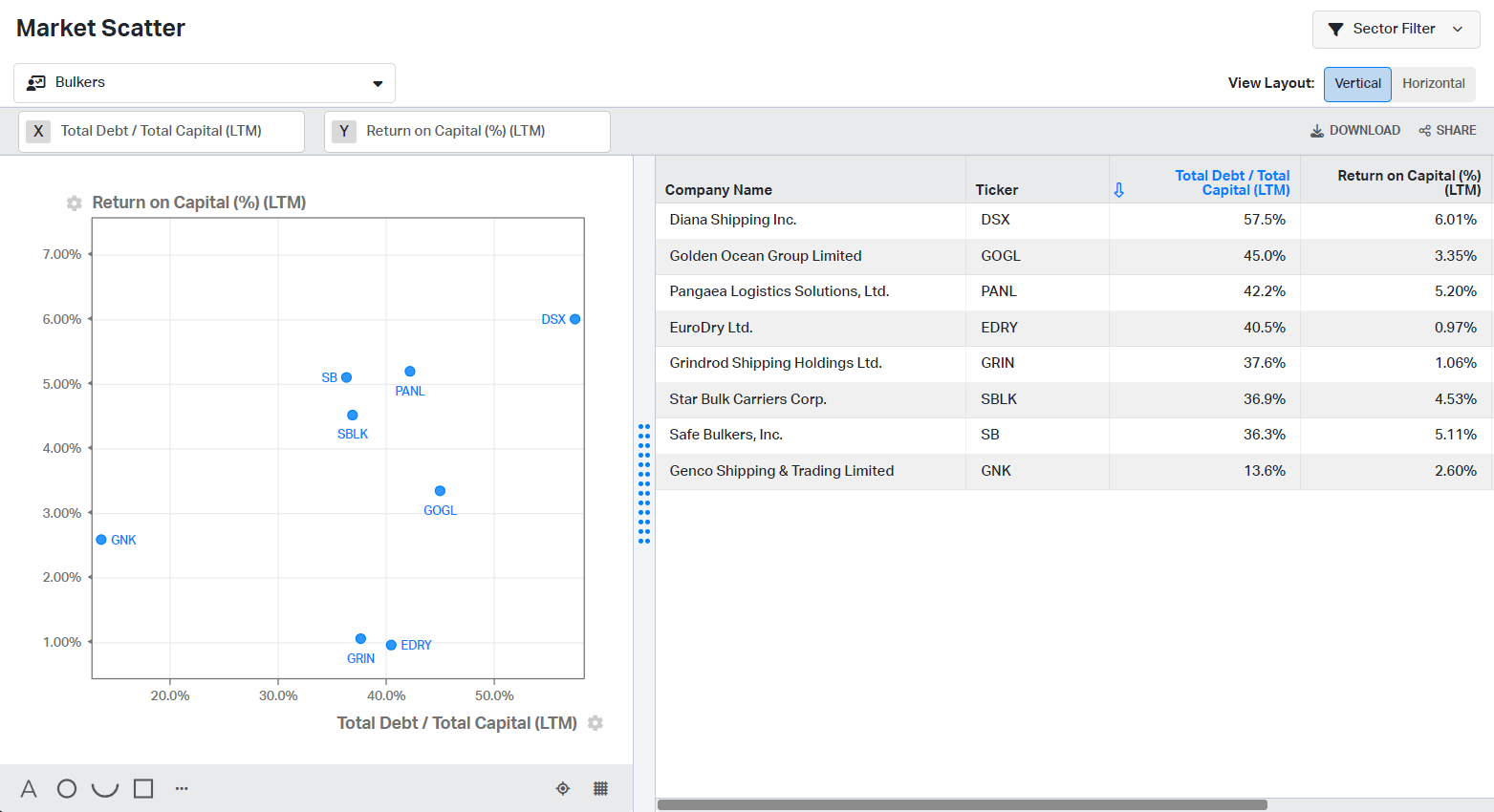

I evaluate SB with similar-sized firms and one of many majors within the enterprise, Star Bulk (SBLK), within the chart beneath primarily based on whole debt/whole capital and ROTC. The purpose is to evaluate SB administration’s capacity to allocate capital.

Koyfin

Dividing ROTC by TD/TC measures how prudently the managers make investments the corporate`s capital. The upper, the higher. SB holds the respectable second place with 14%, subsequent to GNK with 20%. DSX, PANL, and SBLK scored 11%-13% on the ROTC vs. TD/TC ratio.

SB administration is eager so as to add worth for firm shareholders.

Koyfin

The corporate distributes dividends with an excellent yield at 4.77% and frequently repurchases firm shares. On November 30, 2023, SB announced its approved program to repurchase 5 million shares. That is 4.5% of the full SB widespread shares and eight.1% of the general public float.

SB Valuation

First, I’ll evaluate SB towards the identical firms from earlier chapters:

- Secure Bulkers (SB) 2.8 EV/Gross sales, 5.38 EV/EBITDA, 0.57 P/BV

- Pangaea Logistics (PANL) 1.22 Ev/Gross sales, 7.15 EV/EBITDA, 1.12 P/BV

- Diana Delivery (DSX) 2.83 EV/Gross sales, 5.72 EV/EBITDA, 0.62 P/BV

- Grindrod Delivery (GRIN) 0.73 EV/Gross sales, 9.34 EV/EBITDA, 0.57 P/BV

- Genco Delivery (GNK) 1.99 EV/Gross sales, 7.56 EV/EBITDA, 1.02 P/BV

SB and DSX commerce on the highest EV/Gross sales. SB has the bottom EV/EBITDA and P/TBV.

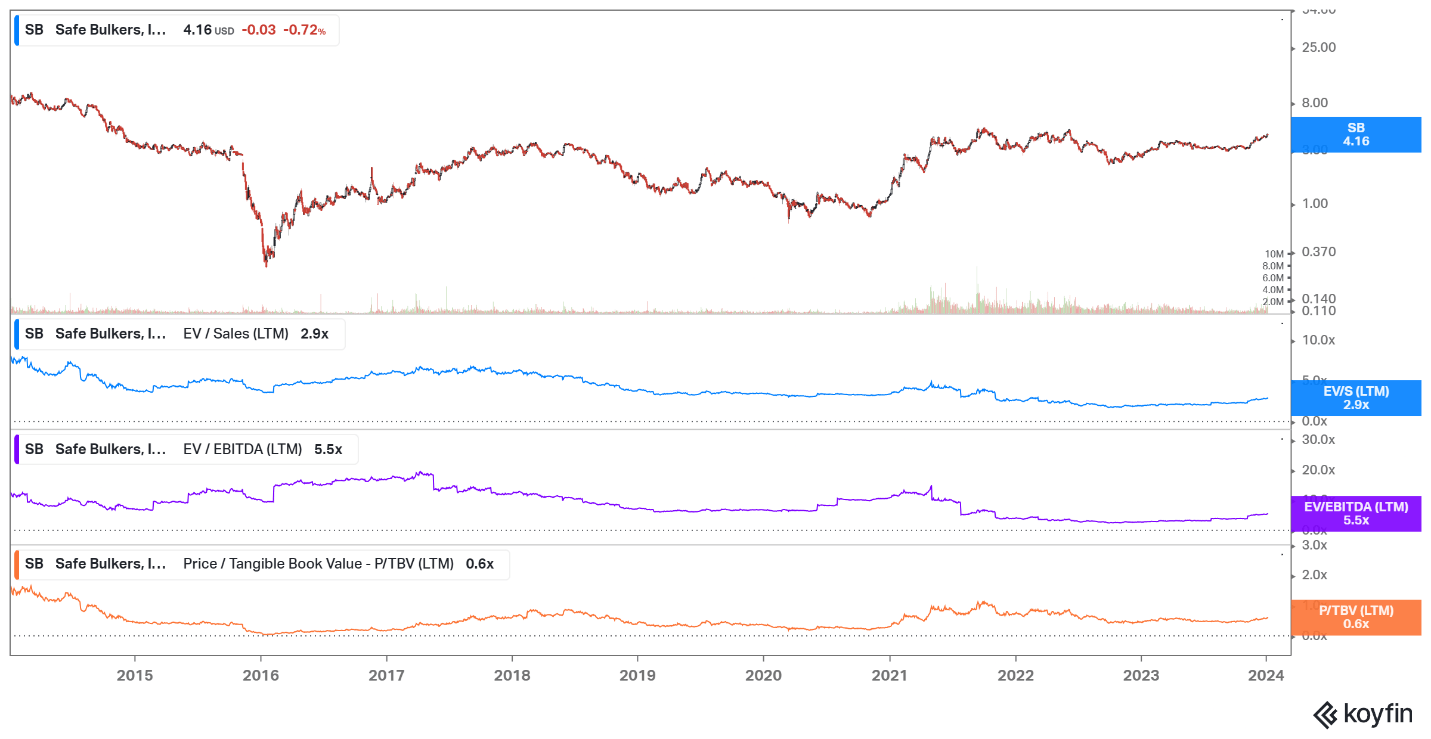

The desk beneath exhibits SB multiples during the last ten years.

Koyfin

SB is deeply undervalued in comparison with its 10Y peaks (6.9 EV/Gross sales, 20 EV/EBITDA, 1.7 P/BV). Conversely, the corporate trades near its 5Y common multiples (2.97 EV/Gross sales, 6.21 EV/EBITDA, 0.58 P/BV).

The corporate is undervalued, given its previous multiples and in comparison with its friends. And within the coming months, its inventory will reprice. In my view, we are going to attain greater highs within the present delivery cycle as a consequence of a number of catalysts just like the Purple Sea disaster and the Panama Canal drought. The delivery trade just isn’t homogeneous, and the assorted lessons of ships will probably be affected distinctly. The bulkers will profit considerably from Panama Canal points, whereas the containers and tankers will reap earnings from the Purple Sea disaster. SB is completely positioned to revenue from these circumstances.

Dangers

For the delivery firms, the monetary danger is essentially the most pronounced. They often are closely leveraged. The important thing to survival and success for each shipowner is figuring out how one can play the delivery cycle. Being overleveraged across the backside of the cycle often means the demise penalty for the enterprise.

SB has a sturdy stability sheet with $83 million money and $199 million undrawn borrowings. The debt maturities are concentrated in 2025-2027, leading to a $300 million debt to be repaid. Even on the present charges, SB can pay its money owed. As I discussed, I anticipate the charges to be greater for longer, enhancing the corporate’s profitability. With extra cash at hand, SB will enhance its liquidity positions additional.

Buyers takeaway

SB is considered one of my favourite shares within the bulk provider phase. 47% of its fleet consists of scrubber-fitted vessels, eight new ships are coming within the subsequent few years, and the corporate`s focus is spot and interval time charters. The corporate has a sturdy stability with sufficient liquidity to cowl its debt obligations and capital investments. SB has high margins and returns in comparison with similar-sized firms; aside from that, its administration excels at capital allocation. SB distributes dividends with an excellent yield at 4.77% and frequently repurchases firm shares. The corporate is undervalued, given its previous multiples, in comparison with its friends. I give SB a powerful purchase score.