JHVEPhoto

Expensive readers/followers,

I have been protecting the corporate Securitas AB (OTCPK:SCTBF) (OTCPK:SCTBY) for a variety of years, and preserve as of immediately a continued place within the enterprise that I consider might generate a strong type of return – at some level. The corporate’s profitability has been affected, however gross and working margins are slowly bettering. That is been the development at the least for the previous few quarters – and we’ve some tendencies and updates which the corporate reported lately, has seen this enhance even additional.

On this article, I search to deconstruct the newest set of reports and tendencies and take a look at what might be seen from Securitas over the interval of the following 3-4 or so years.

The fabric and information we’re digesting immediately is the progress because the final investor day – which was again in August of 2022. And whereas Securitas nonetheless has some methods to go, there’s an upside available right here with the corporate transferring ahead.

So with out additional ado, let’s examine what we’ve right here.

Securitas – What upside can we see going into 2024E?

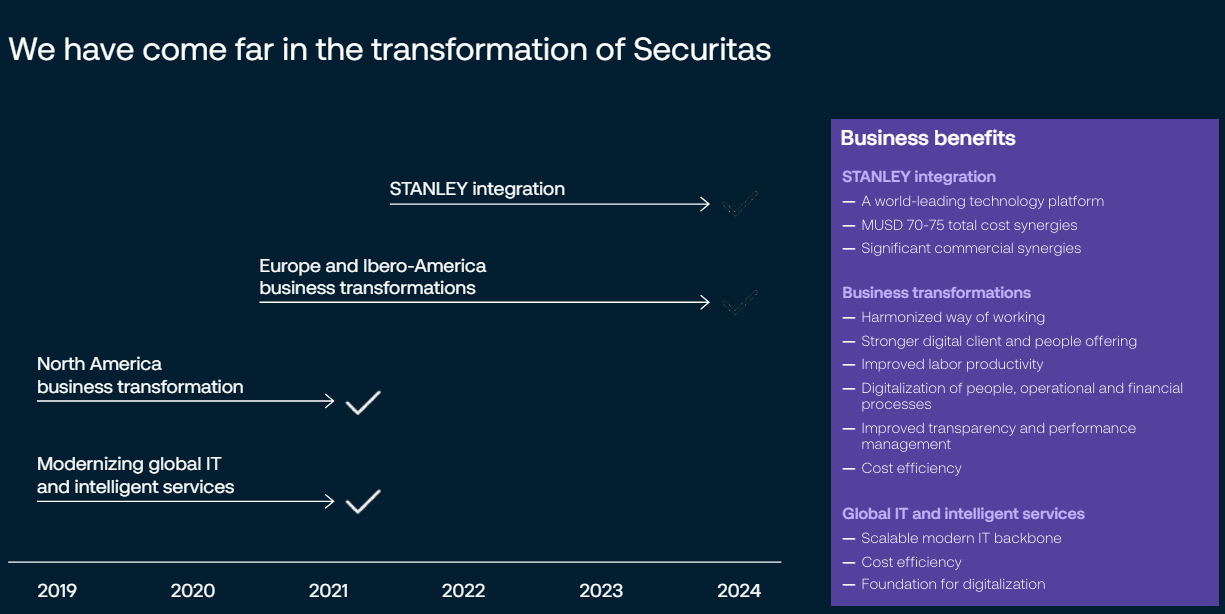

Securitas does require persistence from you for investing. Whereas we’ll present some important progress that the corporate has remodeled the previous few months and the final 12 months, there’s nonetheless lots left for the corporate to do. The creation of the Securitas Expertise section, with the combination of STANLEY, is the largest set of reports for traders at the moment.

Additionally, Securitas is, maybe additionally necessary, seeing enhancements throughout each single section. That is one other good factor. The corporate is seeing important progress in expertise and options and can report some very significant client wins. If doable, I might, after all, elaborate extra on what important shoppers the corporate is referring to right here, however the truth is that the corporate has, as of this text, not but shared the specifics of those shoppers, past their characterization as “significant”. Nonetheless, among the firm’s important shoppers embody offering options to Linkedin, Microsoft (MSFT), CVS (CVS), and others – so different shoppers theoretically be in that realm of measurement and relevance.

The expansion in tech pertains to the ever-increasing relevance of applied sciences in safety contexts. Verticals corresponding to industrials, manufacturing, aviation, crucial infrastructure, workplace, retail, and others undergo excessive losses because of important threats – and Securitas supplies these shoppers with new and modernized safety programs to fight this. The expansion the corporate is seeing might be seen in areas like Video analytics, distant safety, extra superior on-site safety in building websites, MobileCams, and the like. All of those markets appear to expertise progress, or at the least progress with respect to the usage of expertise versus bodily safety guards.

Additionally, the corporate has made progress on the digitalization entrance – over 130 000 consumer websites and, 60 000 officers are actually concerned. The corporate is optimizing your complete worth chain and is exiting non-core low-performing and off markets, which I view as a optimistic.

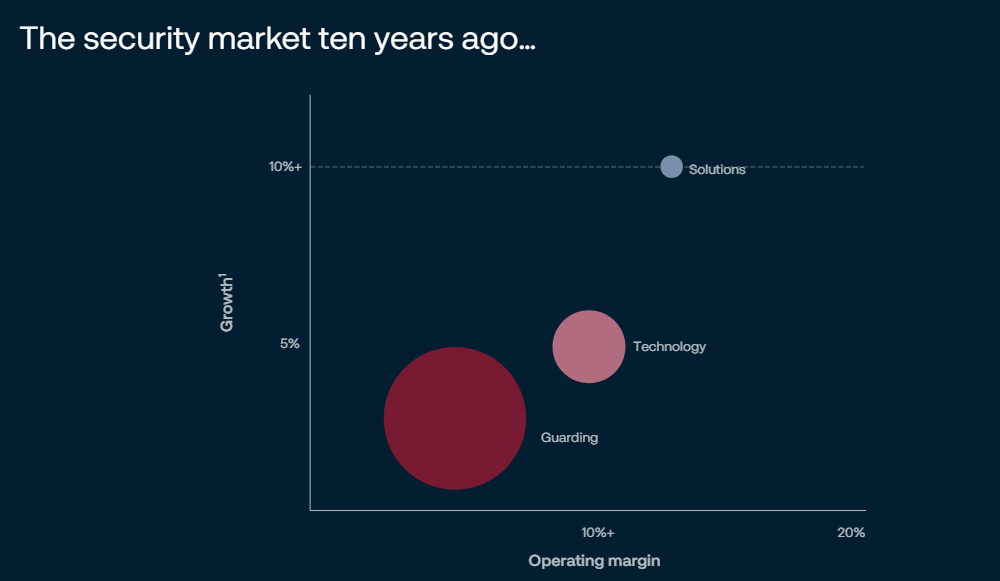

This must also be seen from a historic context. A few decade in the past, the safety market was a spot that was primarily about bodily guarding. It was very low progress, and comparatively low margins, however secure, and an enormous a part of the income. That is how issues regarded on the time.

Securitas AB IR (Securitas AB IR)

This has now developed to guarding slowly shrinking, expertise virtually doubling, Options greater than tripling, and the Information-Pushed SaaS section showing as effectively, in in regards to the measurement of the options section or barely bigger. So in lower than 15 years, your complete marketplace for the corporate has shifted barely.

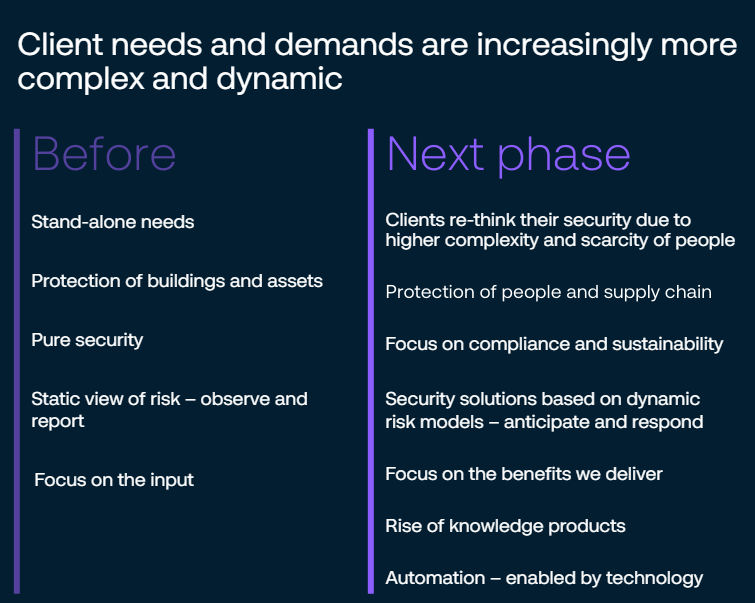

Consumer wants are very totally different immediately than they had been a decade in the past.

Securitas IR (Securitas IR)

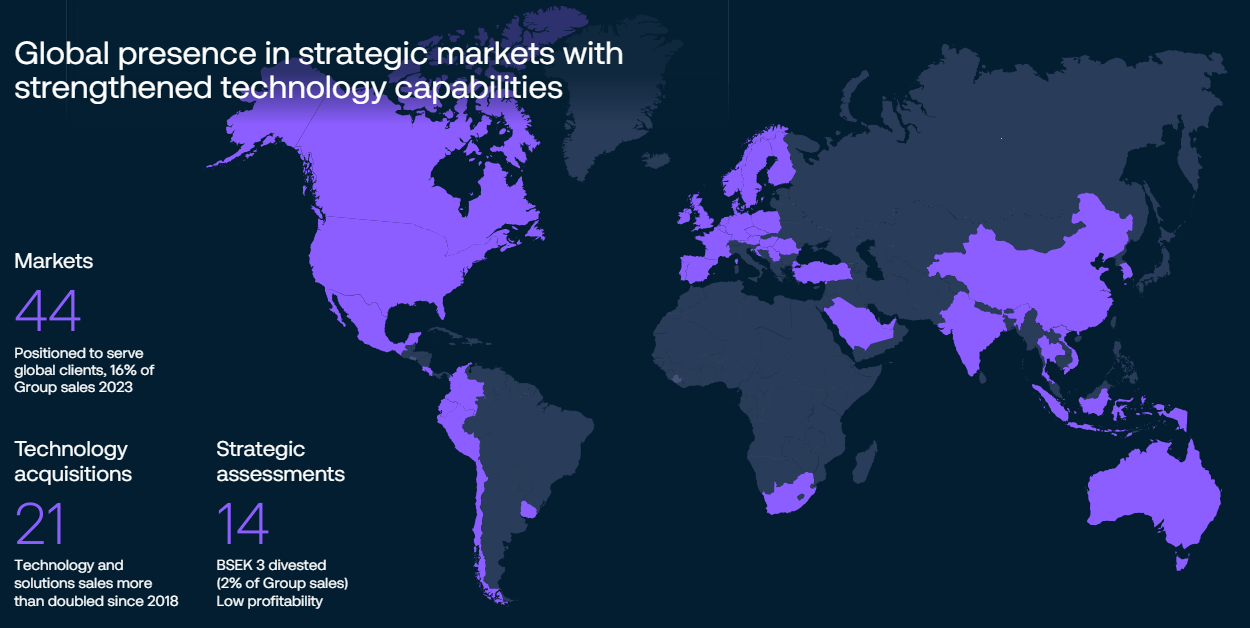

The plan is to show Securitas right into a world-leading safety powerhouse – much more than the corporate already is immediately. The corporate has now left over 10 markets, and lower its workers by virtually 30,000 individuals. The corporate has moved to a digital mannequin whereas sustaining its excessive consumer retention numbers.

Securitas IR (Securitas IR)

So, what’s going to Securitas be doing?

The corporate is prone to concentrate on expertise management. 21% of group gross sales in 2023 are aimed toward this – with a goal of finalizing the combination with lots of of hundreds of thousands of SEK price of price synergies and extra cross-selling upside.

The corporate’s core safety companies – the staffed ones, I am referring to right here – are prone to stay the largest sector, and so they proceed to symbolize over or round two-thirds of what the corporate manages right here. Securitas wants to search out methods to maintain labor prices in examine to make sure that price effectivity right here is in an excellent place, in a world the place inflation and elevated costs and prices for issues appear to be commonplace.

The Firm’s concentrate on options can also be one thing to be bigger and bigger – it is presently 11% of group gross sales, and set to develop considerably on a ahead foundation. Once more, cross-selling is an enormous factor right here, and the truth that Securitas has effectively over 90% consumer retention is one thing that can be a significant benefit right here.

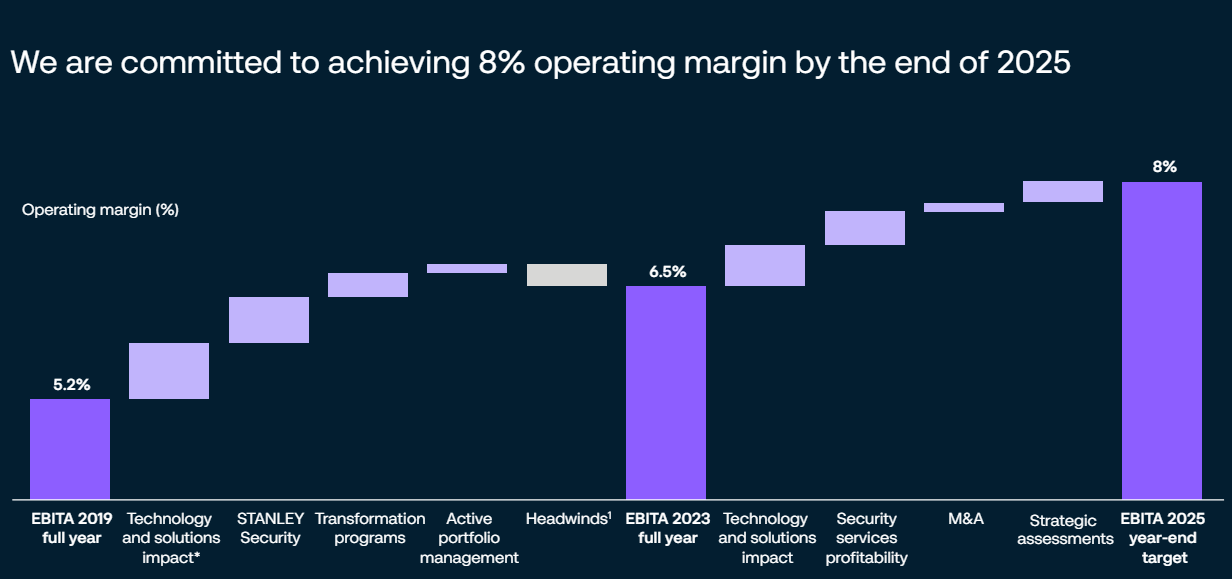

An enormous catalyst for the corporate is reaching a greater EBIT margin. Securitas targets that double-digit EBIT margin, and calls this “strategically important” for the enterprise – and this improvement in margin is predicted to return from two areas. SaaS and Digital merchandise. The standard safety companies alone, or as well as, can’t obtain this, as a result of margins in these legacy companies are decrease than for the brand new sectors and companies. Even with digital launched and dealing, it should take time to achieve that double-digit margin although – as appears clear by the corporate’s personal messaging.

Securitas IR (Securitas IR)

That being mentioned, I do need to liken this firm’s progress to that of a House Shuttle, given its working parameters and market. Discovering this type of margin progress, and seeing a path to eight% in a number of years, is just not one thing simple right here.

So what precisely goes to occur to Securitas that permits this progress?

Effectively, it is a combine – unsurprisingly. The corporate goes to see margin restoration and profitability in Safety Companies Europe. That is an enormous one – coupled with Ibero-America and NA margin restoration as effectively.

Nonetheless, the massive enhancements are coming from the aforementioned digital and SaaS segments. It is going to, as issues are wanting proper now, turn out to be a considerably totally different combine than we have seen with the corporate earlier than.

And this transformation is presently ongoing.

Securitas IR (Securitas IR)

All that being mentioned, Securitas doesn’t have the best monitor document on the market. Given this (sure, I will name it considerably poor right here), I would not take any such estimates with greater than a teaspoon of salt – however we will at the least verify that the corporate has some type of upside right here if the value is low sufficient. I’ll say although that when it comes to fundamentals and precise enterprise tendencies, Securitas is in a really strong place and in a spot the place important upside might be loved by this enterprise. In my final article, I wrote clearly that we’ve the investor day in March of 2024. That is the day we’re reviewing on this article, and what I’m basing this text upon.

Dangers & Upside

As I’ve clarified earlier than, the dangers for Securitas are totally on the operational aspect. That the corporate has been in a decline for a while when it comes to valuation is just not one thing we will argue about – you want solely take a look at the share worth improvement. Nonetheless, I do consider {that a} turnaround appears to be occurring, however on the similar time, I see the visibility right here as decrease than I would like for the timing particularly. The timing portion is likely one of the main dangers right here.

My total danger/reward evaluation continues to be that on the proper worth, Securitas supplies outperformance potential – and I’ll defend this assertion in my valuation portion as effectively to information you to what I consider is an effective valuation for the enterprise.

Securitas – Good valuation, good upside

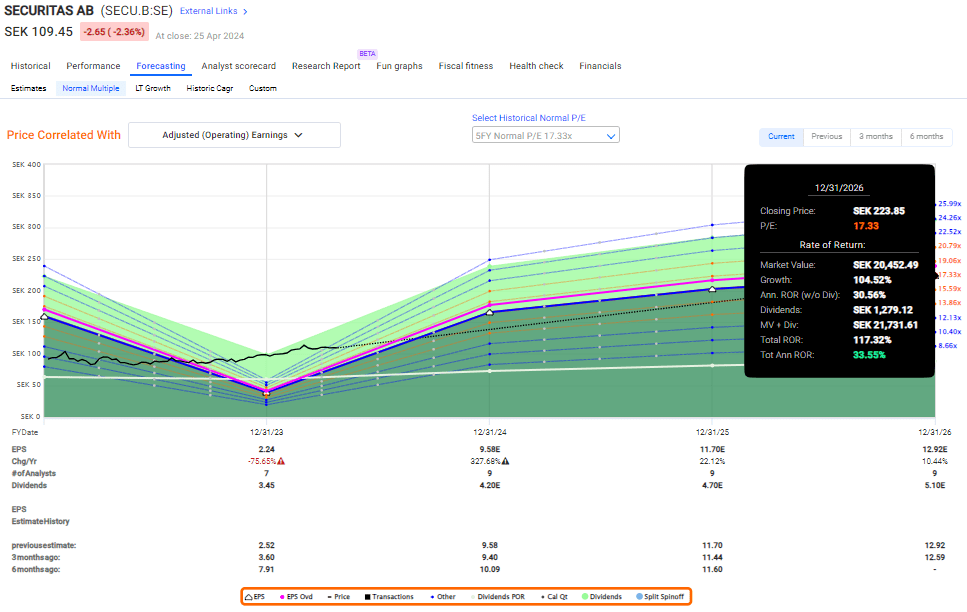

So, what I’ve been speaking about goes to occur within the coming years – should you’re to consider forecasts. By this I imply the reversion in earnings, and a strong total upside for the corporate each from a dividend and from a capital appreciation perspective. The present dividend is just not spectacular. 3.5% simply is not that good when even a primary financial savings account offers you 3.8%. However the upside is important as soon as Securitas begins rising, and present EPS progress estimates put the corporate’s progress at a median of 47% for the next 3 years, with the largest reversal this year.

So let me be clear: I’ve already purchased my Securitas shares. I personal the place I need to personal. Now I am just about “waiting” right here for the upside to materialize whereas making a really first rate 4%+ yield on my price foundation.

That is what I consider will occur within the subsequent few years.

Securitas Upside (Securitas Upside )

Or one thing near it. Securitas is nowhere close to as engaging as after I analyzed it final. In my final article, I spoke of the attraction of beneath 90 SEK, now we’re at virtually 210. My price foundation is near 88 SEK. You may see why I’m a contented investor right here.

The corporate is slightly below my PT of 110, and I’m not elevating it as of this specific time. I may increase it to 115 SEK or 120 SEK with out elevating any eyebrows or overextending what I anticipate from the enterprise right here. However earlier than I do this, I need extra readability on the corporate’s worth/combine evolution – and we have not gotten that but.

However I’m satisfied that we’ll begin seeing the true upside right here at this juncture, and for that purpose, I am sustaining my “BUY” right here regardless of the value goal being so very near being realized.

Timing of the upside right here is the necessary factor – I’ve little doubt it is coming, however when is the query – and if we return right down to double digits once more, then this firm would turn out to be extraordinarily interesting.

As of this time, analysts contemplate Securitas to be a “BUY”, echoing my very own sentiments with conviction. 11 analysts comply with the corporate, and their targets vary from a low of 80 to a high of 160 SEK, with an average of 115 SEK – close to my own heart here. Nonetheless, it additionally represents a major enhance in share worth targets from the early 2023 degree, when the common was virtually at 95 SEK – and since then, I might not say that a lot has occurred.

As a result of not a lot has occurred, the next is my continued thesis for Securitas AB.

Thesis

- There’s rather a lot to love in regards to the safety firm Securitas, which is a worldwide recognized model and enterprise. The corporate’s present challenges however, I consider long-term funding is smart at a pretty entry worth.

- I’ve been shopping for the corporate at interesting funding costs/ranges for over a 12 months, that being beneath the 95 SEK/share degree.

- For the following 12-18 months, the stress in earnings, inflation, prices, and integration name for this to be a riskier funding. My technique dictates that I work this otherwise, and I’ve accomplished so with buy-writes, annualizing over 16% RoR. I preserve this stance in my 2024E article replace.

- The corporate is a “BUY”. I give it a long-term PT of 110 SEK/share, however there could also be a very long time earlier than that is realized.

Bear in mind, I am all about :

1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly huge – corporations at a reduction, permitting them to normalize over time and harvesting capital good points and dividends in the interim.

2. If the corporate goes effectively past normalization and goes into overvaluation, I harvest good points and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is total qualitative.

- This firm is essentially secure/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is presently low cost.

- This firm has a sensible upside primarily based on earnings progress or a number of growth/reversion.

Whereas not essentially low cost any longer, I nonetheless view the corporate as a “BUY” given the general elementary tendencies and quarterly enhancements that we have been seeing. I due to this fact say “BUY” right here.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please concentrate on the dangers related to these shares.