Kajdi Szabolcs/E+ by way of Getty Pictures

We consider SEGRO Plc (OTCPK:SEGXF) deserves extra consideration than it’s getting from traders. This firm is in a number of methods the British model of Prologis (PLD), a really effectively managed industrial and logistics REIT with sturdy aggressive benefits.

Much like Prologis, it has vital embedded development that ought to propel earnings greater within the coming years. First, market rents are considerably greater than its present in-place common rents, which ought to push working revenue greater as these contracts expire and get renegotiated. Second, the corporate develops properties itself and has a horny land financial institution that ought to permit it to maintain creating new belongings at nice places and with good charges of return. Third, trade dynamics and e-commerce development proceed creating vital demand for good logistics places, additional growing common market rents and occupancy. Lastly, just like Prologis, the corporate has a really sturdy stability sheet too.

SEGRO Plc Investor Presentation

Placing every thing collectively, the corporate believes it could possibly ship roughly 53% rental development over the approaching three years. In 2023, regardless of going through greater financing prices, the corporate was in a position to ship a 5.5% adjusted earnings development, and determined to extend its dividend by 5.7%. Comparable to what’s taking place in North American actual property, the economic asset class continues to be pushed by enticing fundamentals and it’s outperforming a lot of the different actual property courses. Regardless of this, greater rates of interest have additionally affected its share worth, but when charges begin coming down quickly, sentiment in direction of the corporate might see a fast enchancment.

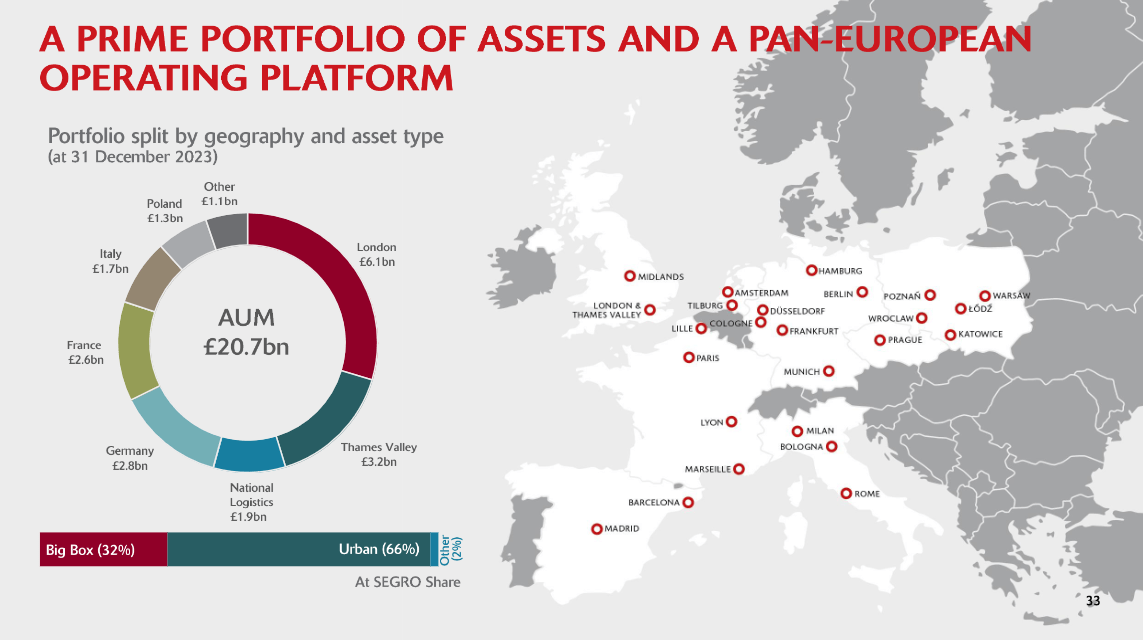

Firm Overview

Whereas the corporate could be very centered on the UK, it does have a big presence in a number of different European international locations, as illustrated within the slide under. E-commerce penetration in Europe has to date been decrease, nevertheless it has been growing, which ought to present a big tailwind for the corporate for the subsequent few years.

SEGRO Plc Investor Presentation

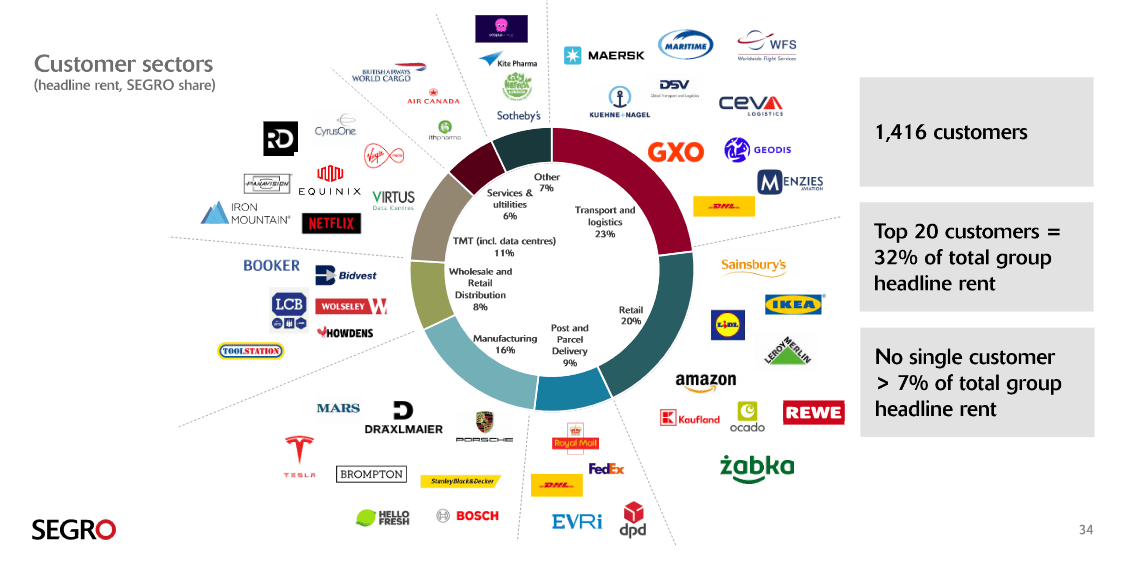

Along with e-commerce gamers like Amazon (AMZN), the corporate additionally serves prospects within the logistics trade like FedEx (FDX), DHL (OTCPK:DHLGY) and Maersk (OTCPK:AMKBY), grocery chains like Sainsbury’s (OTCQX:JSNSF), knowledge middle operators like Equinix (EQIX) and Netflix (NFLX), and auto makers like Tesla (TSLA) and Porsche (OTCPK:DRPRY). In different phrases, essential companies, lots of that are rising in a short time. On the similar time, the corporate has good diversification, which reduces danger and places the corporate in an excellent negotiating place.

SEGRO Plc Investor Presentation

FY23 Outcomes

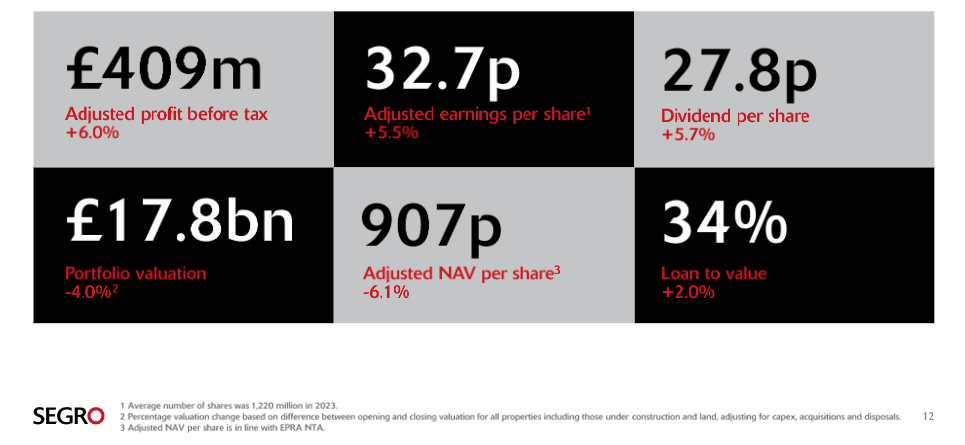

Regardless of a +12.1% enhance in internet rental revenue, greater financing prices diminished adjusted revenue development to +6%. A barely greater share depend diminished adjusted EPS to +5.5%. Nonetheless, given the curiosity price headwinds we view the outcome as passable. Ebook worth was diminished regardless of hire will increase, principally because of adjusting valuations to the upper rate of interest atmosphere. The corporate retains an affordable loan-to-value of 34%.

SEGRO Plc Investor Presentation

Occupancy

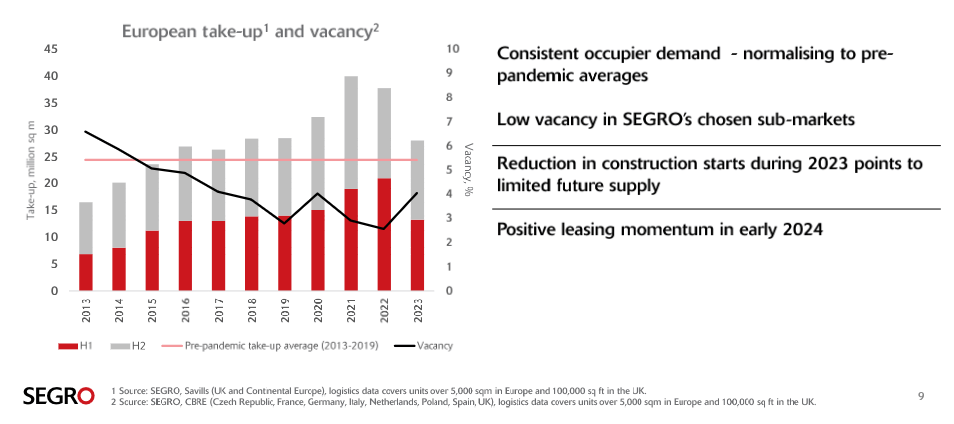

Whereas emptiness ticked-up in 2023, occupancy stays very excessive for the corporate, and development begins have been falling on account of elevated prices and normalizing demand. SEGRO shared that emptiness stays significantly low in its chosen sub-markets, and that it has seen constructive releasing in early 2024.

SEGRO Plc Investor Presentation

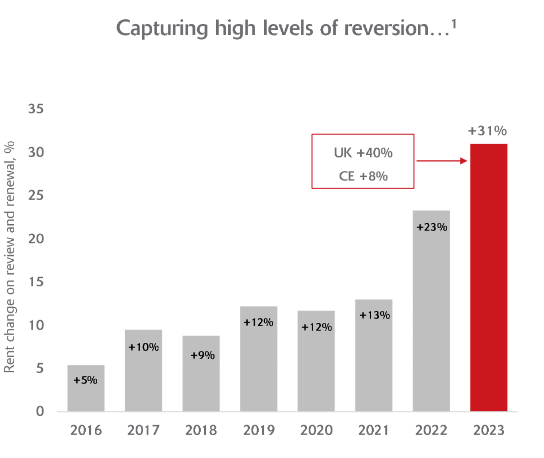

These dynamics are offering vital potential for greater rents to be captured in coming years. The corporate at present estimates embedded development potential of roughly £137 million, and that is mirrored in excessive elevated hire modifications on overview and renewals.

SEGRO Plc Investor Presentation

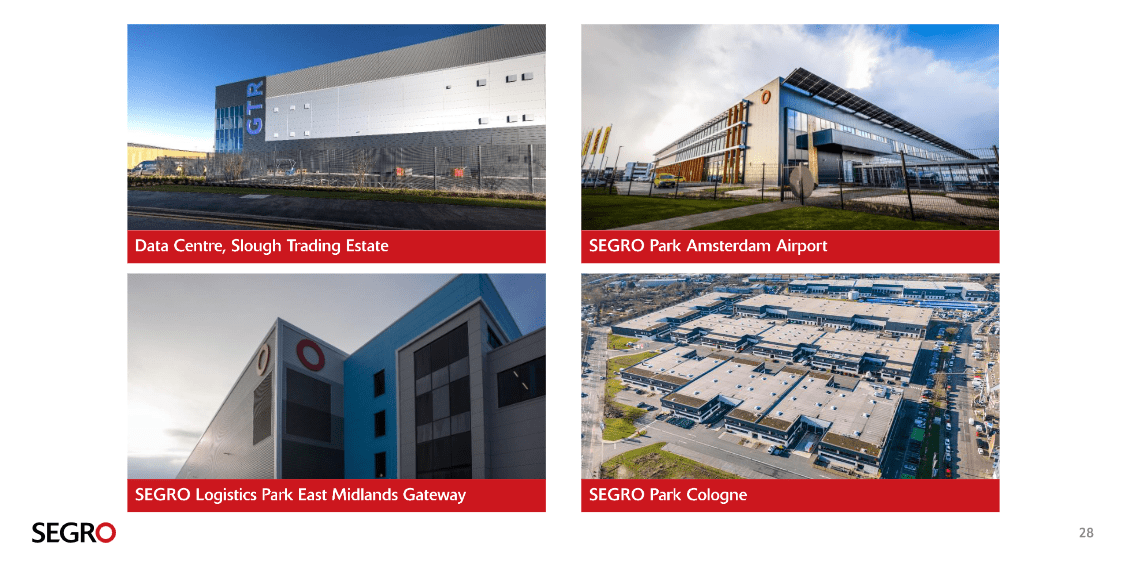

Developments

In addition to hire will increase, the corporate has an extra development vector with new developments. Under are some examples of 2023 growth completions which had been carried out with a yield on price of roughly 7%.

SEGRO Plc Investor Presentation

The corporate has a big growth pipeline of £575m internet investments, which incorporates some selective disposals and extra prime land acquisition. The corporate is prioritizing pre-let developments, and developments on land the corporate already owns might ship yield on new funding cash of near 10%.

SEGRO Plc Investor Presentation

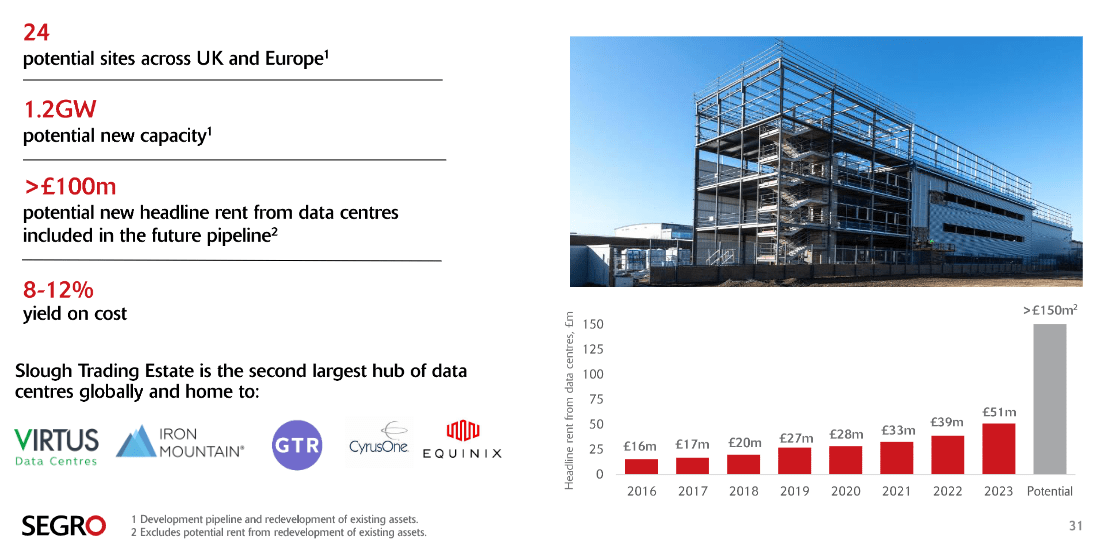

Maybe some of the promising enlargement areas is new knowledge facilities, the place yield on price averages between 8% and 12%. The corporate has recognized 24 potential websites throughout Europe and the UK, for roughly 1.2 GW of recent capability.

SEGRO Plc Investor Presentation

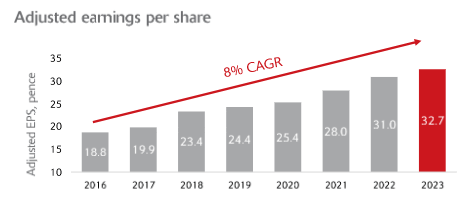

Development

Contemplating that the corporate usually pays out round 85% to 95% of its full yr adjusted earnings as dividends, leaving comparatively little for reinvestment, it’s spectacular that it nonetheless has managed to develop adjusted earnings per share at a charge considerably above inflation. This has been partially due to rents renewing at considerably greater charges, new developments with excessive yields on price, and stable price controls and operational effectivity. Assuming valuation multiples stay unchanged, this degree of development can doubtlessly supply traders double digit returns when mixed with the three%+ dividend yield.

SEGRO Plc Investor Presentation

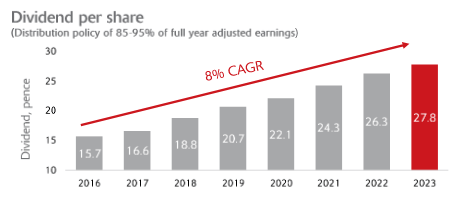

Dividends have been growing at the same charge to adjusted earnings, roughly 8% CAGR the previous couple of years. This has resulted within the dividend virtually doubling when in comparison with 2016. Given the numerous structural tailwinds we see for industrial and logistics actual property, and the corporate’s land financial institution benefit, we see a path for future development for at the very least just a few extra years.

SEGRO Plc Investor Presentation

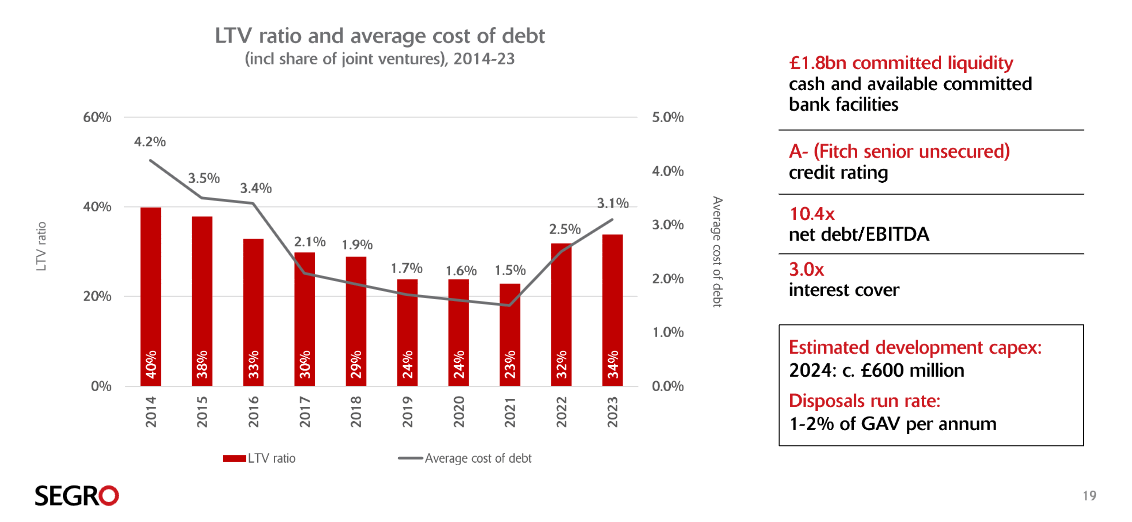

Steadiness Sheet

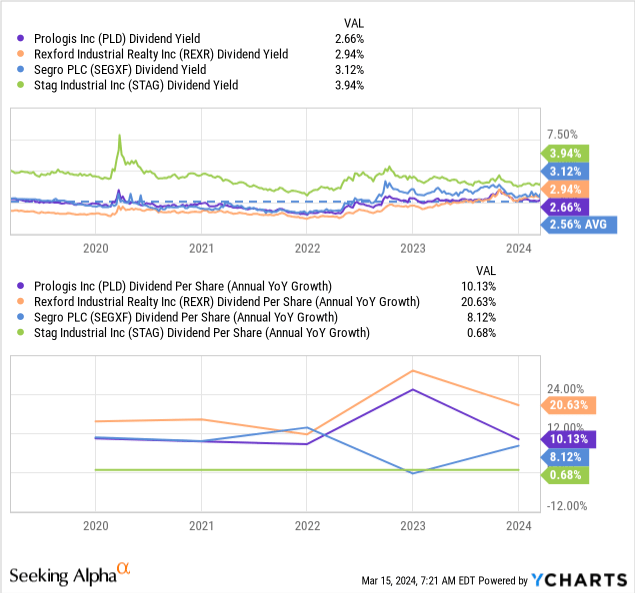

Whereas not as excessive as Prologis’ ‘A’ ranking from S&P World (SPGI) and ‘A3’ from Moody’s (MCO), SEGRO has an funding grade credit standing of ‘BBB+’ from Fitch, with a adverse outlook. That is nonetheless a stable funding grade credit standing, and just like Rexford Industrial Realty’s ‘BBB+’ with outlook stable from Fitch too. For its half, STAG Industrial (STAG) has a decrease credit standing of ‘BBB’, however with a stable outlook. In any case, Prologis does have a barely stronger credit score profile, however SEGRO could be very near the remainder of its U.S. friends.

Its stability sheet is kind of sturdy, with a median debt maturity of 6.9 years, however down year-over-year from 8.6 years previously. Its price of debt at a median of three.1% stays fairly affordable, though it too has considerably deteriorated in comparison with the earlier yr’s 2.5% common curiosity price. Its loan-to-value (LTV) ratio is a nonetheless wholesome 34%, nevertheless it too noticed a small deterioration in comparison with the 32% from the earlier yr. Round 95% of its debt is both mounted, or has a capped rate of interest publicity. Total we aren’t too apprehensive concerning the monetary power of the corporate, however do consider within the quick to medium time period greater rates of interest will proceed to show a headwind.

SEGRO Plc Investor Presentation

Valuation

Not like its U.S. friends, SEGRO follows IFRS accounting, which suggests it has to regulate the worth of its belongings relying on market values. Which means its Value/Ebook Worth is normally a greater proxy for honest worth, even when it could possibly nonetheless underestimate or overestimate it. Its present IFRS internet asset worth (NAV) per share is 886 pence, whereas the native shares are buying and selling at 853 pence, for a roughly 3% low cost to internet asset worth.

We see shares as very near honest worth, even when the present dividend yield is barely greater in comparison with the common of the final 5 years. In comparison with its U.S. friends, solely STAG Industrial is exhibiting a better dividend yield, however its dividend development has been decrease. Conversely, Prologis and Rexford Industrial have decrease dividend yields, however have been rising their dividends at a sooner charge. We’re due to this fact ranking SEGRO as a “Hold”, however consider it’s a high quality firm value being adopted.

Dangers

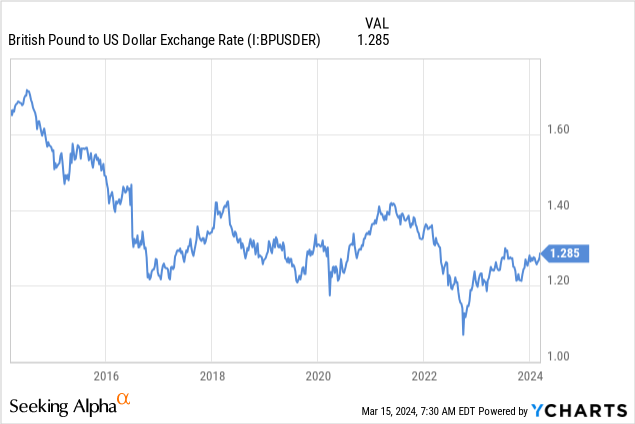

Along with among the similar dangers its U.S. friends have, resembling a possible recession affecting demand for industrial and logistics house, SEGRO has an added danger with international trade fluctuations. Being UK-based means dividends will fluctuate with the worth of the British Pound. This could transfer in both course, however the previous decade it has misplaced floor to the greenback, particularly after their resolution to exit the European Union. There may be additionally some refinancing danger, though that is mitigated by a stability sheet that is still in good condition, and backed by what continues to be thought-about a really enticing actual property asset class.

Conclusion

We consider actual property traders ought to put SEGRO on their watch lists, as that is an fascinating firm working in one of many healthiest actual property sectors, however with a UK and Europe focus. This could add diversification for traders, and we consider the corporate will profit from growing e-commerce penetration in Europe.

Primarily based on the corporate’s vital growth pipeline, together with enticing knowledge middle alternatives, we consider it could possibly proceed delivering stable earnings development for the foreseeable future. It has been rising adjusted earnings at a roughly 8% CAGR, which suggests the corporate might ship returns of round 11% if it continues development on the similar charge and the valuation stays steady. At near their internet asset worth per share, we charge the corporate a “Hold”, and can proceed to observe it in case a market dislocation creates a horny investing alternative.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please pay attention to the dangers related to these shares.