Kokkai Ng/iStock Unreleased through Getty Photos

Introduction

Over two years in the past, once I heard about Seize Holdings Restricted (NASDAQ:GRAB) going public at a $40B valuation, my preliminary response was that the corporate was most likely overpriced.

Wanting again, I used to be proper about this.

With out even doing any analysis, I additionally made the uneducated conclusion that the on-demand enterprise mannequin in Southeast Asia would possibly simply be unsustainable and would stay unprofitable for all eternity.

Because it seems, I used to be lifeless improper about this — in Q4, the corporate turned GAAP worthwhile for the primary time ever.

In search of Alpha

So after a flip to GAAP Web Revenue positivity and after an 80% decline within the inventory worth, I figured there is perhaps some worth within the inventory — so I seemed into it.

After doing a little analysis, I noticed that Seize is a tech large in hibernation.

With that being mentioned, seize (pun supposed) a cup of espresso and get cozy, as a result of this can be a deep dive into Southeast Asia’s superapp. Get pleasure from!

Firm

A bit of over a decade in the past, two Malaysian-born Harvard Enterprise College college students — Anthony Tan and Tan Hooi Ling — teamed as much as pitch a enterprise thought for the HBS New Enterprise Competitors in July 2011.

Anthony Tan, having grown up in a household that owned one of many largest car companies in Malaysia, and Tan Hooi Ling, having skilled Malaysia’s nightmare taxi trade whereas working at McKinsey, determined to duplicate Uber’s (UBER) ride-hailing service within the U.S. and produce it to their house, Malaysia.

Because it turned out, the pair completed second place within the competitors, successful $25,000. With that prize cash, they launched the taxi-hailing cell app, MyTeksi, in June 2012.

MyTeksi rapidly gained traction in Malaysia, because it gives safer and extra dependable taxi rides. Ultimately, the 2 founders realized that they might supply the identical service in neighboring international locations the place ride-hailing know-how remains to be nonexistent.

With out hesitation, they rebranded the corporate as GrabTaxi and entered different Southeast Asian markets over the subsequent few years, together with Singapore, Indonesia, Thailand, the Philippines, Vietnam, Cambodia, and Myanmar.

As well as, in 2014, GrabTaxi secured its first main funding of $65M from outdoors traders, enabling the corporate to launch extra companies and extra importantly, compete successfully towards different ride-hailing platforms which have simply launched as nicely — together with Uber, which Grab ended up acquiring in 2018.

In 2016, the corporate rebranded to Seize. Quick ahead to 2021, Seize went public within the U.S. via a SPAC merger with Altimeter Development Corp., valuing the corporate at $40B, which, at the moment, was the largest-ever U.S. fairness itemizing by a Southeast Asian firm.

App Retailer

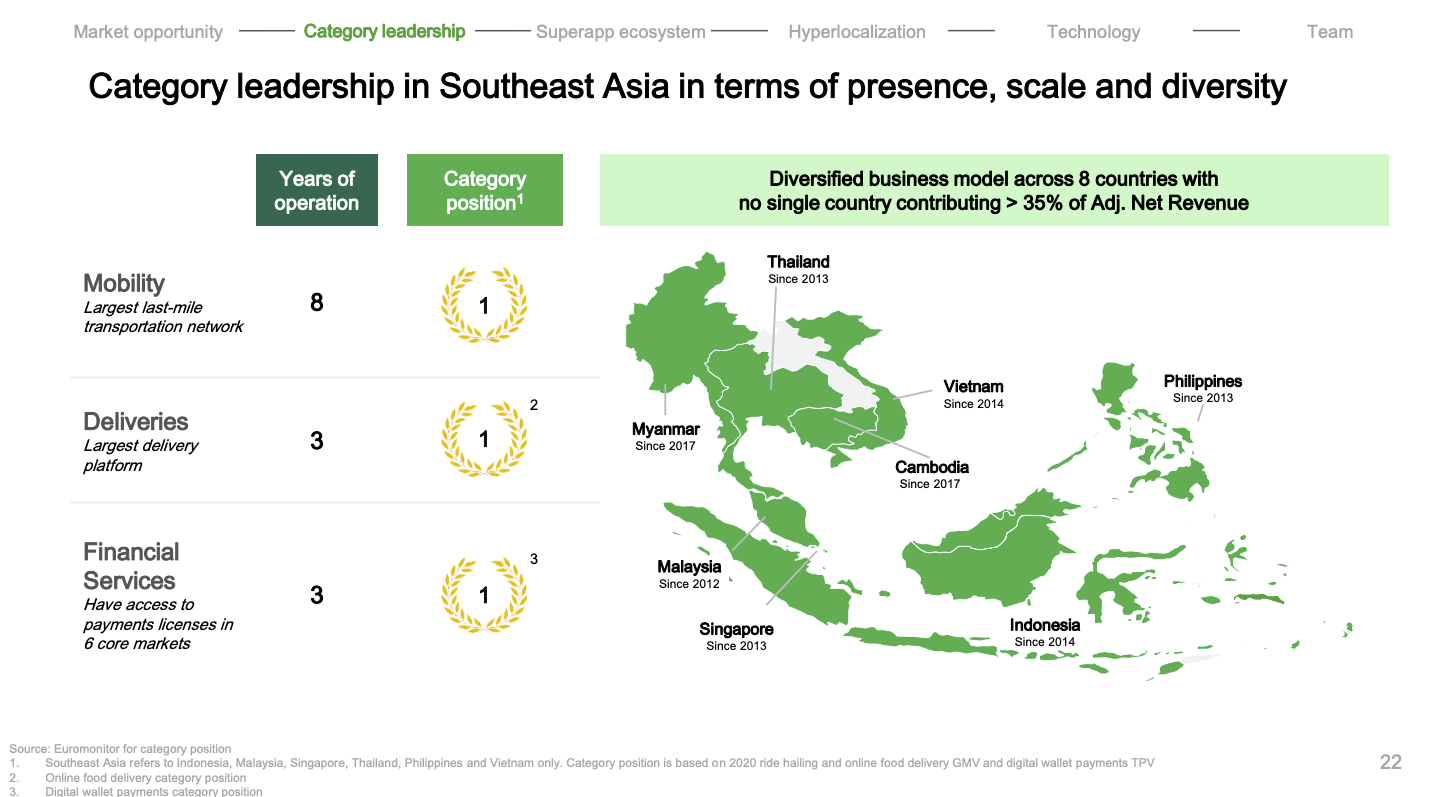

Immediately, Seize is the main superapp in Southeast Asia, providing deliveries, mobility, monetary, and enterprise companies, connecting hundreds of thousands of customers, retailers, and companions throughout 500+ cities and eight international locations — all in a single platform.

- Deliveries: In 2015, Seize received into the deliveries enterprise via the launch of its package deal supply service, GrabExpress. Just a few years later, Seize expanded to meals (GrabFood) and grocery (GrabMart) deliveries as nicely. In 2022, Grab acquired Jaya Grocer, a number one grocery store chain in Malaysia, which enormously expanded its GrabMart providing.

- Mobility: That is Seize’s flagship providing. Similar to Uber, Seize gives ride-hailing companies throughout a wide range of choices together with personal automobiles (GrabCar), taxis (GrabTaxi), and bikes (GrabBike). Talking of which, Seize acquired Uber’s Southeast Asia operations in 2018, additional increasing Seize’s ride-hailing and meals supply companies. In trade, Uber took a 27.5% stake in Seize with Uber CEO Dara Khosrowshahi becoming a member of the board.

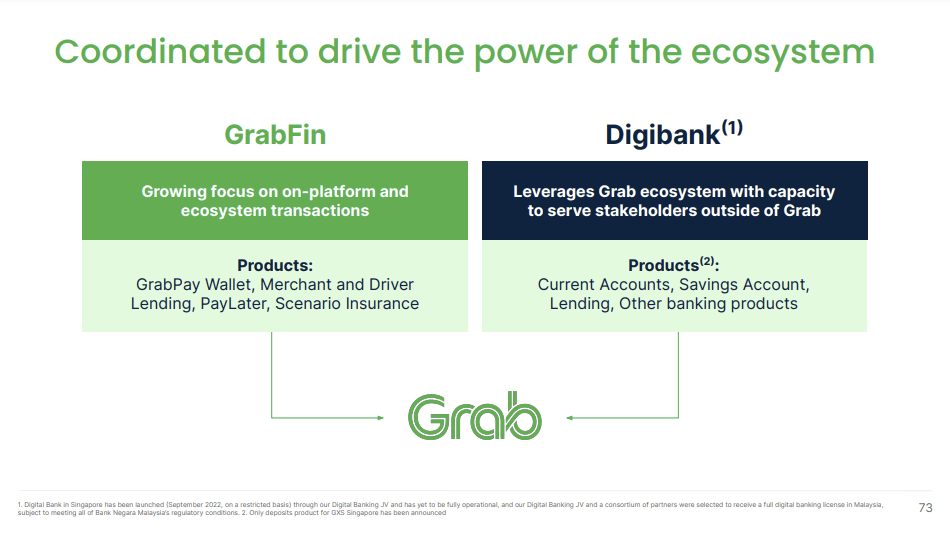

- Monetary Companies: In 2017, Seize expanded to the monetary sector by launching GrabPay, its cell pockets providing. To expedite its market presence, in 2021, Seize acquired a 90% stake in OVO, one of many largest cell wallets in Indonesia. Inside the Seize platform, Seize additionally gives lending (GrabFinance), purchase now pay later (PayLater), and insurance coverage (GrabInsure) companies. Outdoors of the Seize platform, Seize additionally gives digital banking options.

Seize 2022 Investor Day Presentation

- Enterprise: Seize additionally offers value-added companies for companies. This contains its promoting companies via GrabAds, which permits offline and internet marketing through Seize’s fleet and cell app. As well as, Seize gives mapping and location-based companies via GrabMaps, which permits enterprises to embed Seize’s map, routing, search, site visitors, and navigation options.

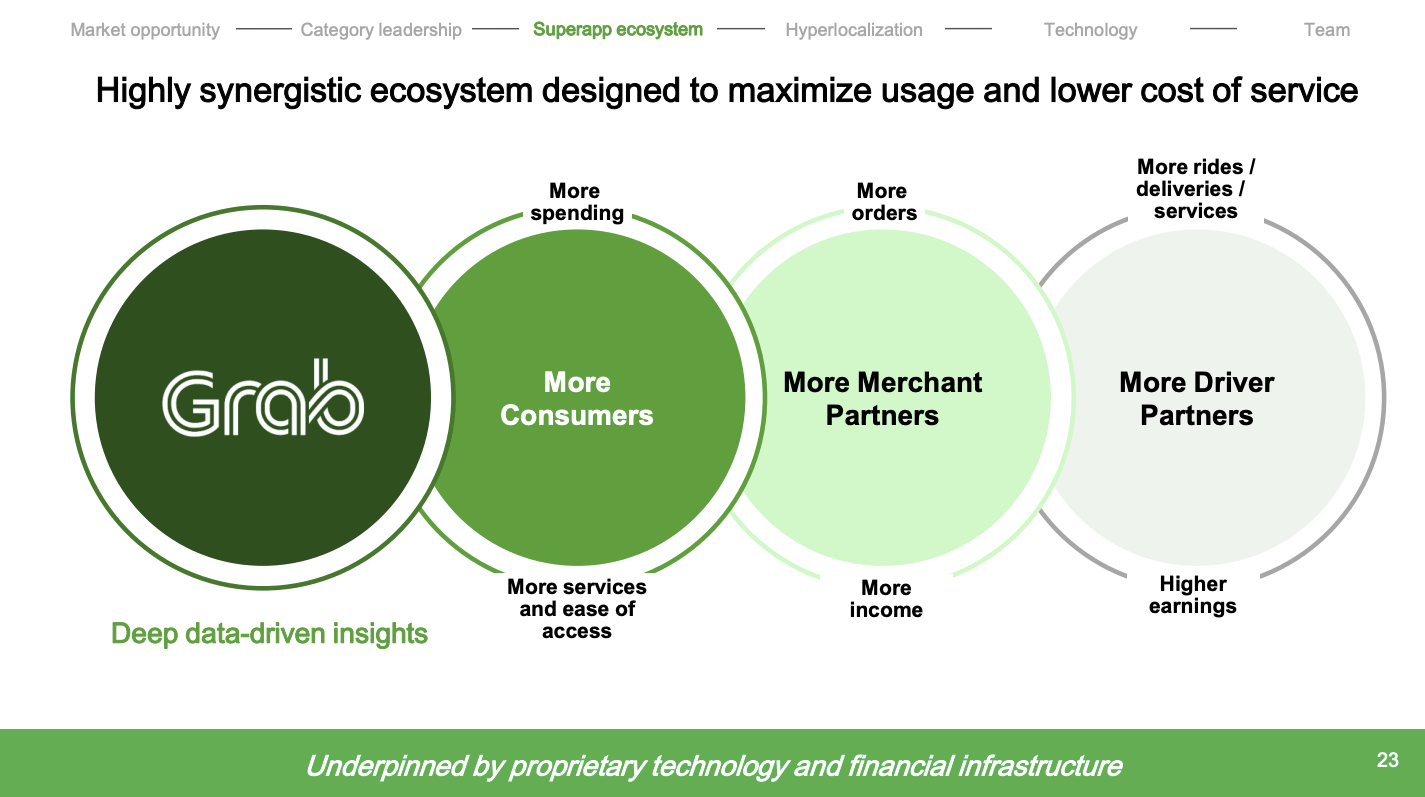

In essence, Seize is the on a regular basis app for on a regular basis customers — the corporate focuses on on a regular basis transactions reminiscent of transportation, consuming, paying, and extra.

Seize needs customers to stay and breathe throughout the Seize ecosystem.

Extra importantly, via these transactions and interactions throughout the ecosystem, Seize goals to drive Southeast Asia ahead by creating financial empowerment for everybody — that features customers, drivers, and retailers.

That is what a superapp is all about — and Seize would possibly simply be the one firm that has an opportunity of attaining and sustaining “superapp” standing in Southeast Asia.

Why?

As a result of Seize has a number of the most impenetrable moats I’ve ever seen in a enterprise.

Moats

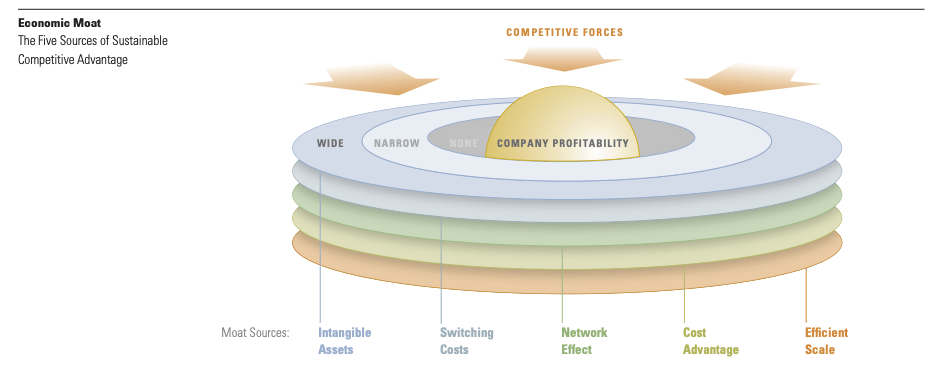

In keeping with Morningstar, there are 5 sources of sustainable aggressive benefits.

I imagine Seize has all 5.

Morningstar

Intangible Property

Per Morningstar:

Intangible belongings are issues reminiscent of patents, authorities licenses, and model id that preserve an organization forward and opponents at bay.

Surely, Seize is likely one of the strongest manufacturers in Southeast Asia. Similar to Uber, it’s a family title — a verb.

“I don’t have a car but I can just Grab later on.”

“I’m hungry. You wanna Grab some food?”

“I can’t meet you tonight. I’ll just Grab the documents to you”.

It is very tough for corporations to turn into a verb — solely the perfect do.

And Seize is the perfect.

In every single place you go in Southeast Asia, you see Seize’s inexperienced brand embossed on its fleet of automobiles, on the jackets of its riders, and on the checkout level of its retailers.

I can say this confidently as a result of I am a consumer myself who lives in Indonesia and travels ceaselessly to Singapore — two of Seize’s largest and most essential markets.

Southeast Asia is actually turning greener by the day due to Seize.

That speaks volumes about its model id and energy.

Switching Prices

In keeping with Morningstar:

Switching prices are obstacles that preserve clients from altering between merchandise, like from one firm’s product to a competitor’s.

Think about having a state-of-the-art on a regular basis app with all of the options and companies that fulfill your each day wants — all at your fingertips. Moreover, you get probably the most full catalog of transportation varieties, service provider suppliers, and meals objects. Service high quality — together with velocity of execution, ease of use, customer support, and many others. — can also be top-notch.

Now why would you employ a distinct app that provides fewer companies or decrease high quality?

Value is one cause, however apart from that, I do not see some other cause why you’d swap out of the platform.

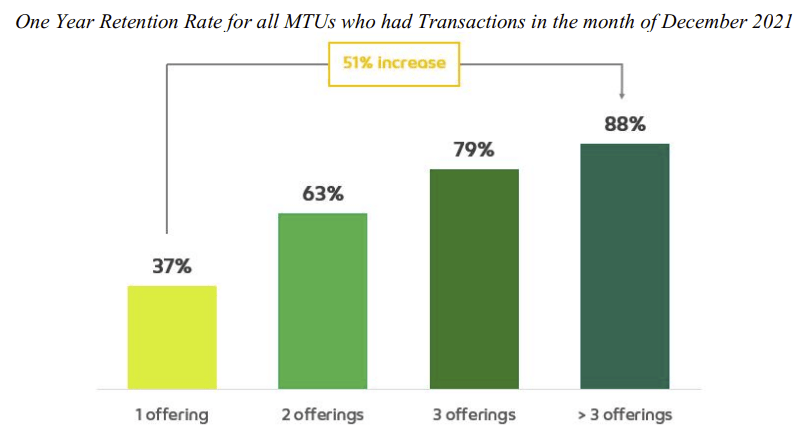

Furthermore, as Seize introduces extra services and products on its platform, the extra choices customers use. And the extra choices customers use, the extra loyal they turn into.

As you may see, retention charges enhance meaningfully as customers use extra choices, from as little as 37% for one providing, to as excessive as 88% once they use greater than three choices.

Seize FY2022 Annual Report

Moreover, subscription companies reminiscent of GrabUnlimited and rewards applications reminiscent of GrabRewards are driving even increased engagement throughout the platform, additional amplifying Seize’s switching value moats.

As an illustration, GrabUnlimited subscribers now account for one-third of Deliveries Gross Merchandise Quantity (GMV) with subscribers spending 4.2x extra on meals deliveries than non-subscribers.

Not solely that, Seize sees comparable tendencies in its monetary companies section (emphasis added):

We proceed to see sturdy ecosystem uplifts from our funds and lending enterprise, with customers from GrabPay spending 4 occasions extra and having 1.5 occasions increased retention charges than money customers. Our driver companions who tackle a mortgage with us additionally recorded 1.5 occasions increased retention in comparison with drivers and not using a mortgage.

(COO Alex Hungate — Grab FY2023 Q3 Earnings Call)

Extra choices drive increased cross-sell charges. Larger cross-sale charges drive increased retention charges. Larger retention charges drive increased spending, which in the end results in increased high quality, extra steady Income era.

That, my buddy, is excessive switching value moats at play.

Community Impact

As described by Morningstar:

Community results happen when the worth of a superb or service will increase for each new and current customers as extra individuals use it.

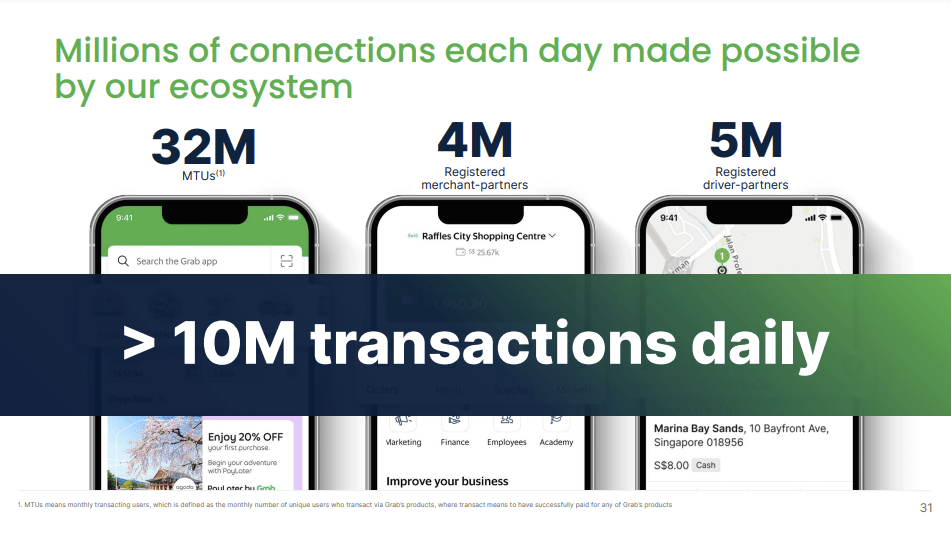

In Seize’s case, the extra customers be part of the platform, the extra invaluable the platform turns into. Suffice it to say, the Seize ecosystem is very large:

- 37.7M Month-to-month Transacting Customers (MTUs).

- 4M+ retailers.

- 5M+ drivers.

- Processing 10M+ transactions each day.

Seize 2022 Investor Day Presentation

On the similar time, Seize’s huge community additionally makes cross-selling extremely environment friendly. For instance, following the launch of GXBank in Malaysia in November 2023, GXBank was capable of entice 100K+ depositors inside two weeks, with 79% of GXBank depositors being current Seize customers.

In keeping with ASEAN, there are 680M people in Southeast Asia, which implies Seize has a market penetration price of about 5.5%. This additionally implies that Seize has a lot extra room for development.

As Seize provides extra choices, extra customers ought to be part of the platform. This could enhance total platform engagement, which is able to ultimately result in extra revenue alternatives for drivers and retailers. Consequently, extra drivers and retailers may even be part of the platform, which in the end results in much more customers.

That is the Seize ecosystem flywheel in movement which creates highly effective community results for the enterprise.

Seize Investor Presentation April 2021

Price Benefit

Morningstar’s definition:

An organization with a value benefit can produce items or companies at a decrease value, permitting it to undercut its opponents or obtain increased profitability.

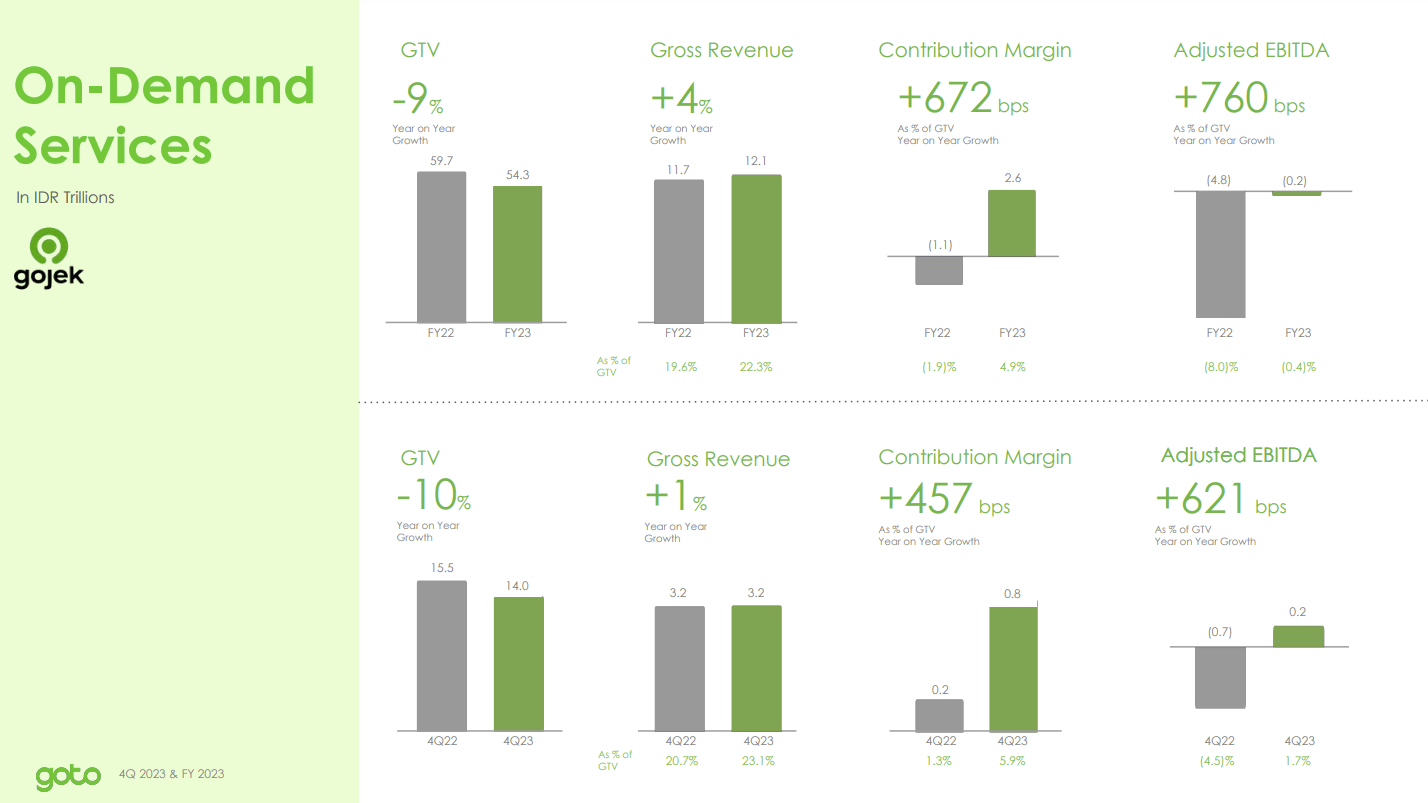

GoTo — the mother or father firm of GoJek and Tokopedia, Indonesia’s largest mobility and e-commerce corporations — is the closest competitor to Seize.

If we check out GoTo’s On-Demand Companies section, we are able to see that GoTo has an Adjusted EBITDA Margin of 1.7% (as a % of Gross Merchandise Quantity) in This autumn of 2023.

GoTo FY2023 This autumn Investor Presentation

In distinction, Seize’s On-Demand section produced $278M of Adjusted EBITDA in This autumn final yr, at an Adjusted EBITDA Margin of 6.7% (as a % of GMV).

In different phrases, Seize has an enormous value benefit over GoTo — I am not even going to check it with smaller opponents since they most definitely have a lot worse unit economics.

Why?

As a result of Southeast Asia is a extremely aggressive market and the one method to obtain profitability is to have a big sufficient scale to achieve working leverage — Seize has the size, and subsequently, the fee benefit to defeat its competitors.

This brings us to the final moat…

Environment friendly Scale

… which is crucial of all:

Environment friendly scale advantages corporations working in a market that solely helps one or a number of opponents, limiting rivalry.

Very similar to how the US ride-hailing and meals supply industries are dominated by a number of gamers like Uber and DoorDash (DASH), the Southeast Asian market can also be a winner-takes-most market.

Because it stands, Seize is the most important participant in Mobility, Deliveries, and Monetary Companies in Southeast Asia.

Seize Investor Presentation April 2021

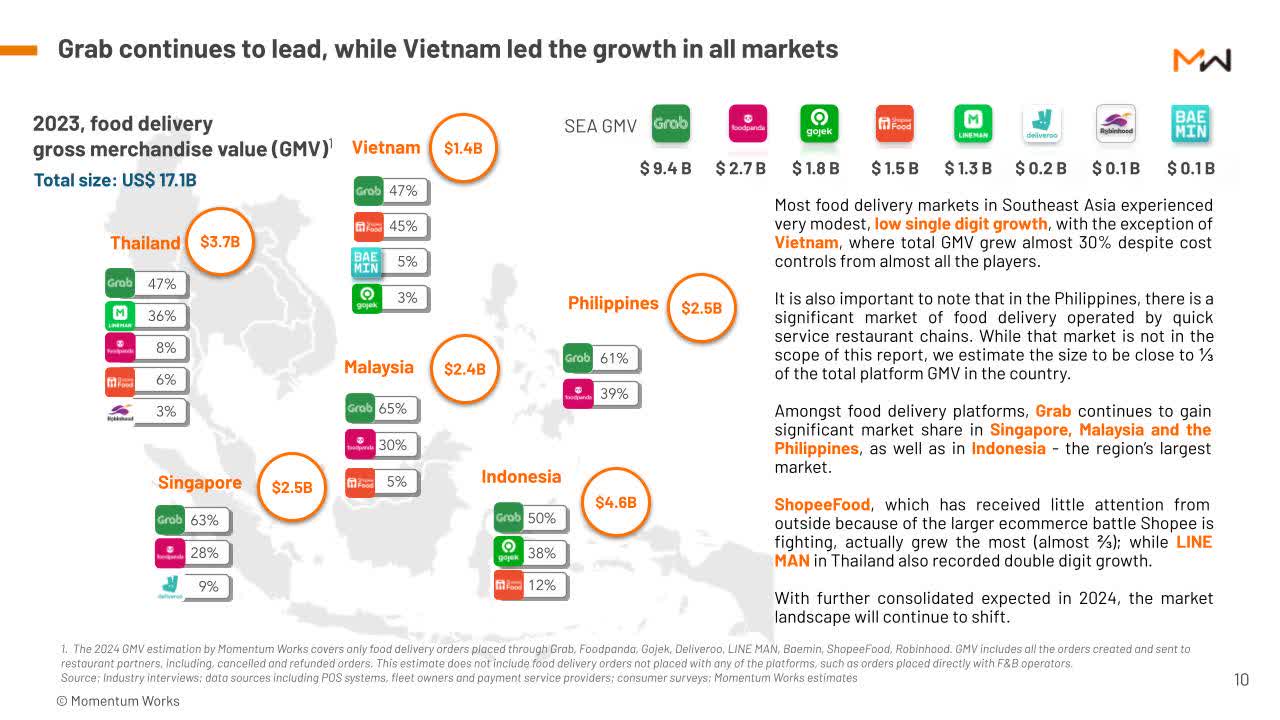

Beneath, we are able to see that Seize has the lion’s share within the meals supply market in every of the Southeast Asian international locations. In 2023, Seize processed $9.4B of meals deliveries GMV, which is many occasions bigger than its closest competitor, Meals Panda, which has an estimated GMV of solely $2.3B.

Southeast Asia is a fertile floor for us. We’re now the most important on-demand platform within the area at a scale that’s over thrice bigger than our subsequent closest competitor and but, there’s nonetheless quite a bit for us to realize for our companions on this area.

(CEO Anthony Tan — Grab FY2023 Q4 Earnings Call.)

Momentum Works

So far as I do know, Seize can also be probably the most capitalized participant in Southeast Asia. Being probably the most funded enterprise allows Seize to take market share and increase much more aggressively than opponents. This is likely one of the main the explanation why Uber failed in Southeast Asia.

In keeping with INSEAD, Grab overtook Uber because the chief in Southeast Asia on account of its large funding of $4B. Uber, alternatively, solely spent $700M within the area.

Mainly, scale is crucial aggressive moat as a result of it reinforces the opposite 4 moats:

- With scale, the model strengthens

- With scale, the fee to modify will increase

- With scale, the community impact turns into extra highly effective

- With scale, the fee construction improves.

That being mentioned, I imagine Seize has all 5 of Morningstar’s moats, which makes it one of the vital sturdy companies in fashionable occasions — its moats will in the end permit Seize to not solely crush competitors but in addition maintain profitability and seize development alternatives.

Development

Earlier than we dive into the financials, let’s speak about how Seize generates and acknowledges Income.

Seize operates 4 enterprise segments, specifically: Deliveries, Mobility, Monetary Companies, and Enterprise.

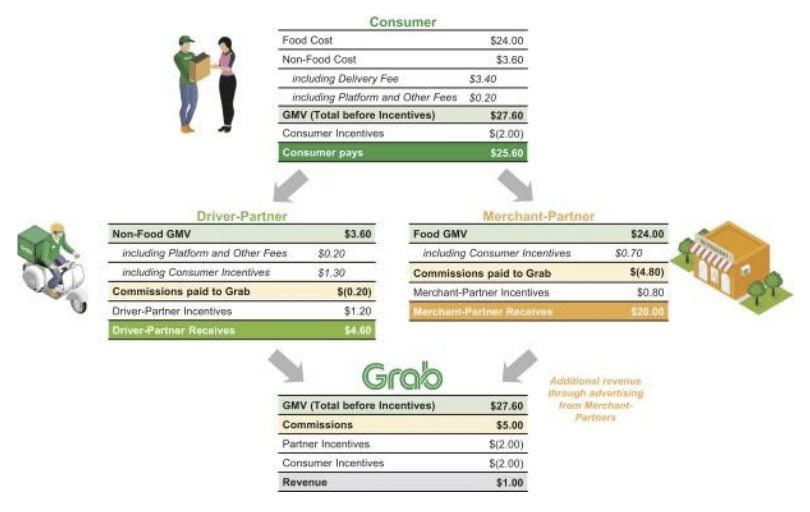

Beneath, you may see what a typical meals Supply transaction appears to be like like.

Seize FY2022 Annual Report

As you may see, Seize acts because the intermediary that connects three totally different events: customers, drivers, and retailers.

- Customers pay meals prices and non-food prices, minus client incentives.

- Drivers earn non-food GMV, plus driver incentives.

- Retailers earn meals GMV, plus service provider incentives.

- In trade for utilizing Seize’s platform, drivers and retailers pay commissions to Seize.

- Seize generates Income by taking these commissions and subtracting any incentives that it provides out to drivers and retailers.

Seize additionally generates Mobility Income in a similar way, simply that retailers are usually not concerned within the transaction.

So, Deliveries and Mobility make up the On-Demand segments of the corporate.

As well as, Seize additionally generates Monetary Companies income via transaction charges. The section additionally earns non-transaction charges via companies reminiscent of lending and insurance coverage.

Lastly, Seize generates Enterprise Income primarily via promoting companies.

With that out of the best way, let’s check out Seize’s development trajectory.

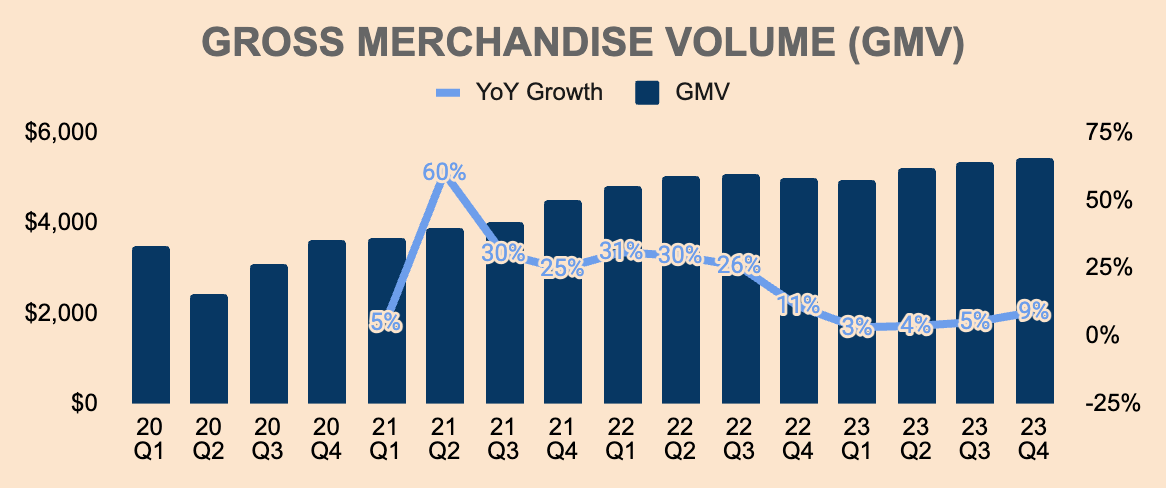

In 2023, GMV was $20.1B, up 5% YoY. In This autumn, GMV was $5.4B, up 9% YoY. Development was primarily as a result of growth of its Mobility and Deliveries section, which I am going to go into extra element in a while.

That mentioned, development has accelerated for 3 straight quarters, which is an effective signal that the corporate is gaining momentum and market share.

Writer’s Evaluation

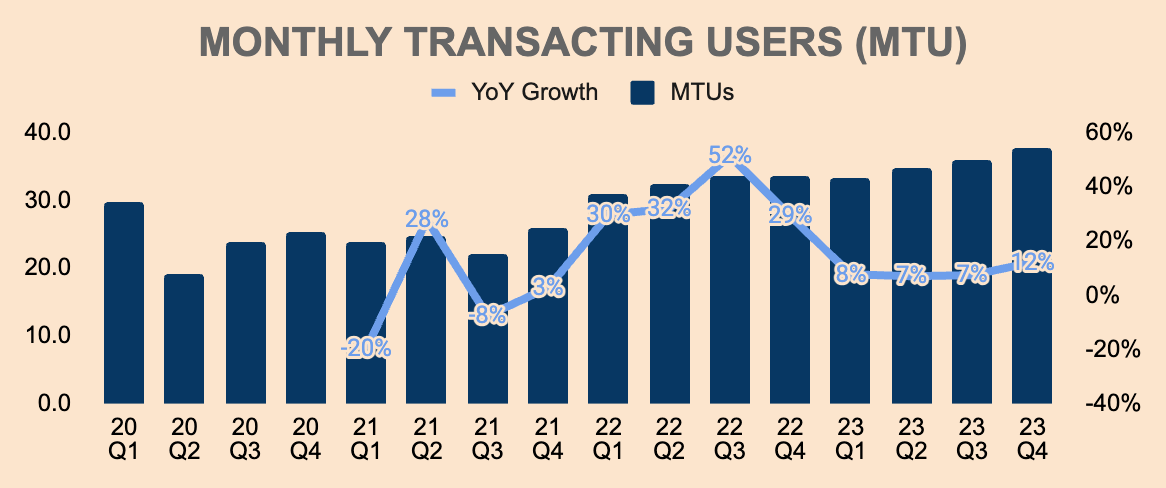

GMV was additionally pushed by rising MTUs within the platform, which was 37.7M as of This autumn, up 12% YoY. The variety of customers on a platform is likely one of the most essential metrics to trace since customers are a number one indicator of future Income development. As well as, consumer development is a sign of sturdy platform engagement and rising community impact moats.

Writer’s Evaluation

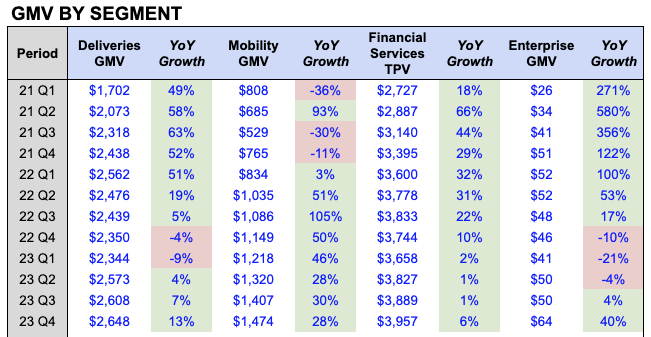

That mentioned, let us take a look at GMV by section.

As you may see, all segments are displaying strong development.

Writer’s Evaluation

This autumn Deliveries GMV was $2.6B, up 13% YoY, on account of increased spend per consumer and better Deliveries MTUs, which reached an all-time excessive in This autumn.

Higher affordability of Seize’s companies additionally contributed to development. As an illustration, Saver deliveries — which supply a decrease supply charge in trade for an extended supply time — elevated common order frequency by 1.6x, as in comparison with non-Saver customers. Saver was first launched in Q1 last year and has now accounted for greater than 23% of Deliveries transactions.

Shifting on, Mobility GMV grew strongly in This autumn, which was $1.5B, up 28% YoY. Of essential notice, the Mobility section was closely impacted by the pandemic however has now absolutely recovered with GMV exceeding pre-covid ranges for the primary time in This autumn. This was pushed by increased Mobility MTUs, increased common order frequency, and the rebound within the journey trade.

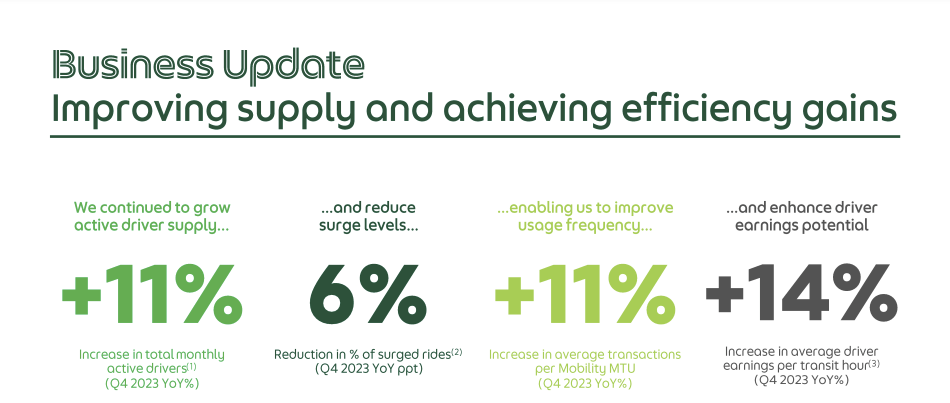

Seize is experiencing sturdy demand for its Mobility companies which is why administration is specializing in increasing its driver provide and bettering driver effectivity. As you may see, Seize managed to extend its driver provide by 11% YoY in This autumn, which consequently diminished surged rides by 6% YoY and elevated common transactions per MTU by 11%.

Seize FY2023 This autumn Investor Presentation

Subsequent, the Monetary Companies section grew Whole Fee Quantity, or TPV, by 6% YoY in This autumn, to almost $4B.

- This autumn On-Seize Quantity — consisting of transactions inside Seize’s platform like utilizing GrabPay to pay for Deliveries and Mobility companies — was $2.7B, rising 18% YoY.

- This autumn Off-Seize Quantity — consisting of transactions outdoors Seize’s platform like utilizing GrabPay in an offline restaurant — was $1.3B, declining 14% YoY.

The expansion in On-Seize Quantity and decline in Off-Seize Quantity replicate administration’s give attention to driving ecosystem transactions, because the unit economics for Off-Seize transactions weren’t as enticing:

You may bear in mind going all the best way again to September 2022 once we had the Investor Day, we talked about shifting away from the off-platform funds enterprise the place the transaction margins weren’t contributing to our path to profitability.

That is been ongoing. Off-platform transactions proceed to fall. And that implies that the margin combine improves for our funds enterprise.

(COO Alex Hungate — Seize FY2023 Q3 Earnings Name, emphasis added.)

Lastly, This autumn Enterprise GMV was $64M, up 40% YoY, as a result of development of Seize’s promoting enterprise. That is nonetheless a small section so development will seemingly be unstable within the short-to-medium time period.

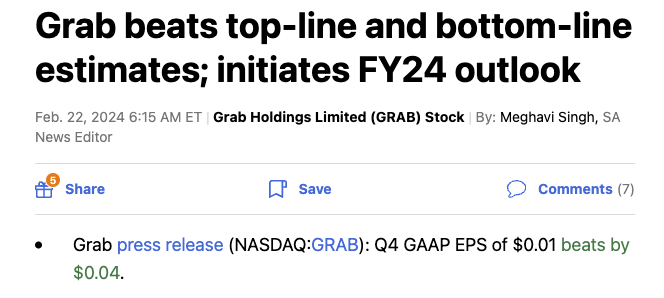

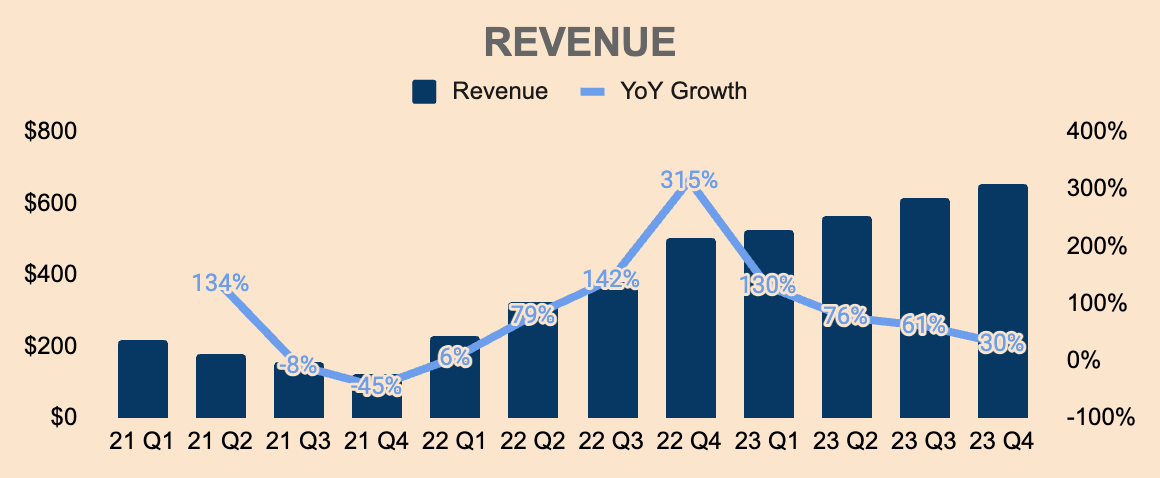

That being mentioned, Income for the complete yr was $2.4B, up 65% YoY. This beat administration’s initial guidance of $2.2B to $2.3B.

In This autumn, Income was $653M, up 30% YoY. This beat analyst estimates by $20M.

Nice to see Seize outperform expectations.

Development was primarily on account of GMV development throughout all segments, a change in enterprise mannequin for sure supply choices, and the discount in incentives.

Writer’s Evaluation

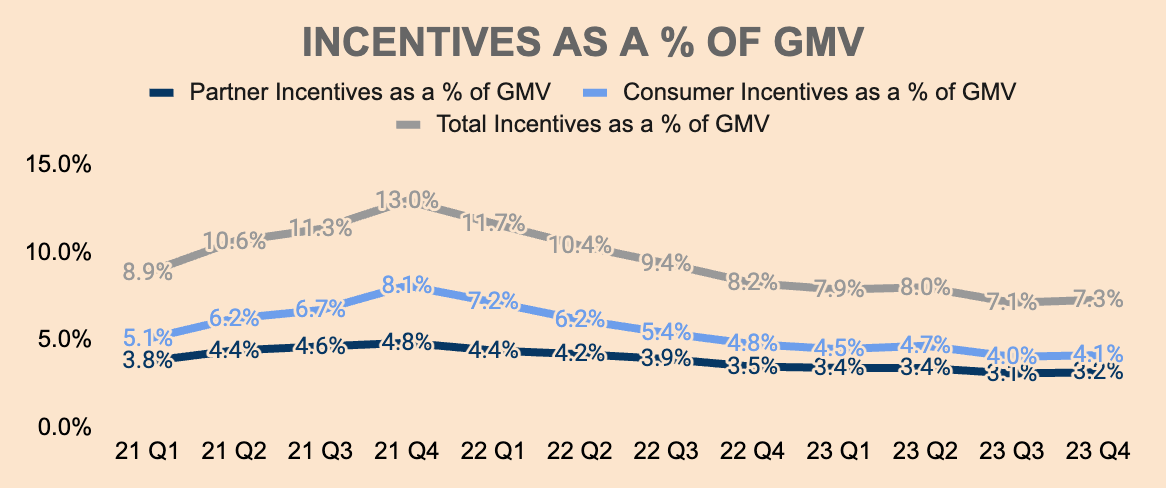

If you have not realized, Income grew a lot sooner than GMV, and that is as a result of discount of incentives.

As a reminder, Seize’s Income is the same as the commissions and costs it collects from drivers and retailers, minus any incentives it provides out to those companions and its customers.

As you may see, Seize’s Whole Incentives as a % of GMV was as excessive as 13% in This autumn of 2021. This was an effort to defend towards competitors in addition to mitigate customers and companions from churning through the pandemic.

Nonetheless, as market circumstances stabilized, Seize was capable of cut back incentives with out jeopardizing the corporate’s development. As of This autumn, Incentives as a % of GMV was 7.3%, down from 8.2% final yr, which led to strong Income development.

Ideally, we wish to see this metric proceed to say no.

Writer’s Evaluation

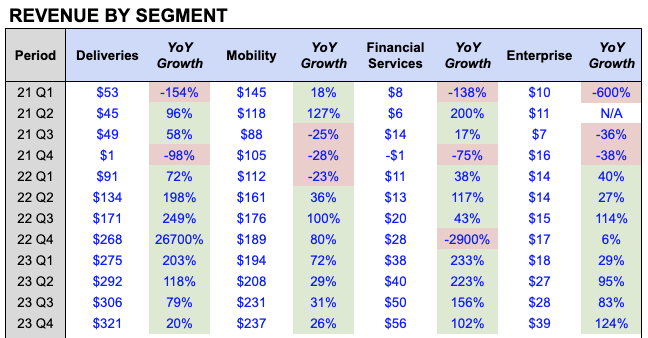

Beneath, you may see sturdy Income development for every of Seize’s segments, pushed by platform monetization and incentive discount.

- This autumn Deliveries Income was $321M, up 20% YoY.

- This autumn Mobility Income was $237M, up 26% YoY.

- This autumn Monetary Companies Income was $56M, up 102% YoY.

- This autumn Enterprise Income was $39M, up 124% YoY.

Writer’s Evaluation

Of specific notice, the Monetary Companies and Enterprise segments grew triple-digits YoY. I imagine these smaller segments might be main contributors to development within the coming years as Seize continues to monetize its consumer base.

As an illustration, Seize is ramping up investments in its Monetary Companies section.

- In October 2023, KakaoBank (South Korea’s main digital financial institution) invested a ten% stake in Seize’s Superbank in Indonesia.

- In November 2023, Seize additionally launched GXBank in Malaysia, the primary digital financial institution ever within the nation.

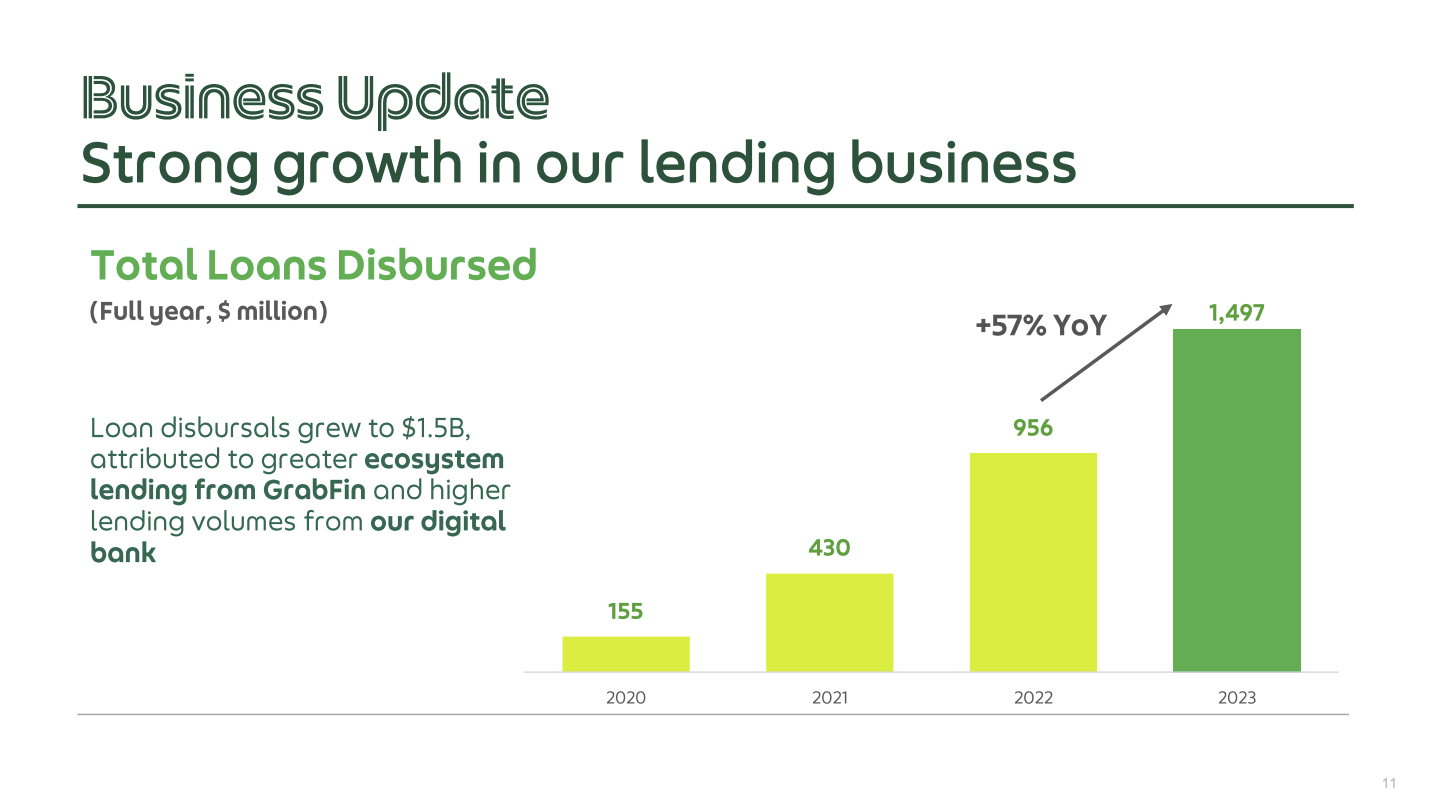

- Moreover, Seize is rising its lending enterprise quickly, with complete loans disbursed rising 57% YoY to $1.5B in 2023.

Seize FY2023 This autumn Investor Presentation

As well as, Seize’s Enterprise section — which consists primarily of promoting — remains to be in its early innings. The section is rapidly gaining traction with self-serve energetic advertisers rising 54% YoY and common spend by energetic advertisers rising 129% YoY.

All in all, Seize is displaying sturdy development because it recovers from the financial shock left by the pandemic.

All its segments are producing record-high GMV (and TPV), and I do not see any indicators of slowing down given Seize’s sturdy aggressive moats.

What’s extra, platform monetization and incentive optimization are bettering, which ought to result in strong Income and earnings development shifting ahead.

Profitability

On this part, I’ll analyze Seize’s revenue margins through the use of GMV because the denominator (as a substitute of Income). This fashion, we are able to see how margins are trending with out the volatility of Income since Income is basically affected by complete incentives paid.

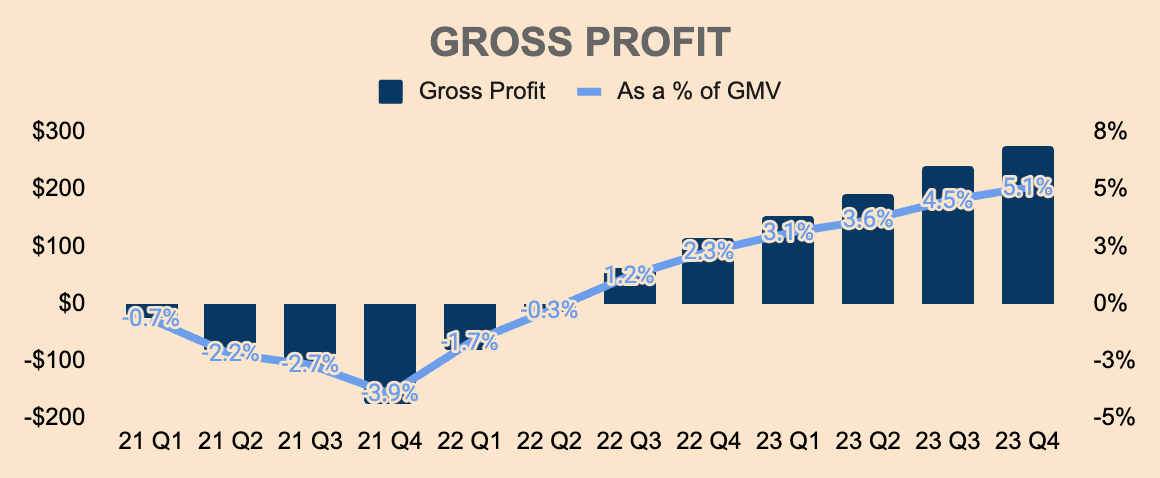

That mentioned, This autumn Gross Revenue was $276M, which was 5.1% of GMV. As you may see, Seize was Gross-Revenue-negative a few years in the past as a result of firm pumping large quantities of incentives to customers and companions. Nonetheless, Gross Revenue has turned optimistic as the corporate focuses on worthwhile development.

Writer’s Evaluation

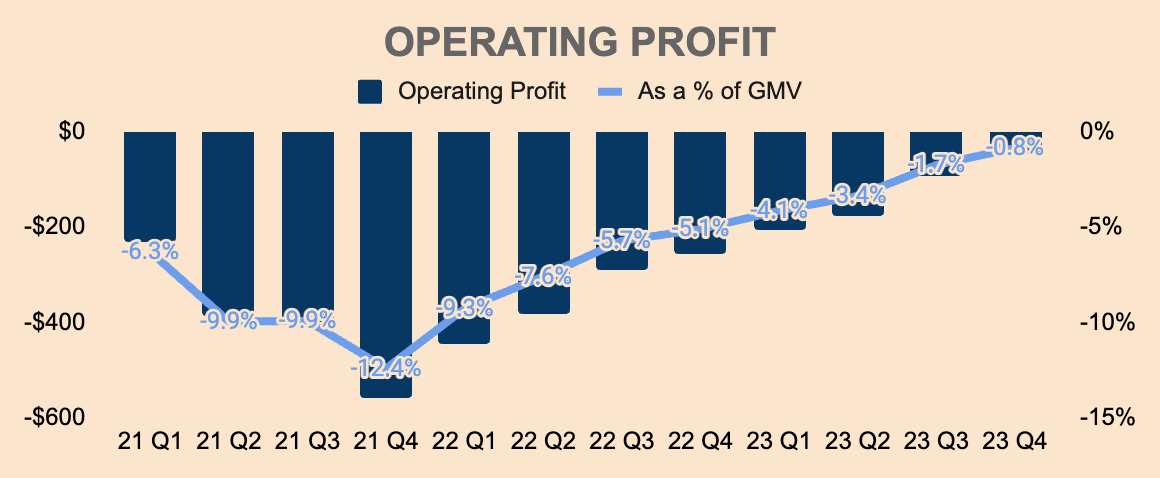

Then again, Working Revenue remains to be destructive at $(46)M in This autumn, which was (0.8)% of GMV. On the intense aspect, Seize is displaying sturdy working leverage and a transparent path in direction of profitability — Working Margin improved by 430 foundation factors YoY and 90 foundation factors QoQ, which implies that Working Revenue is on monitor to show optimistic as early as Q1 this yr.

Writer’s Evaluation

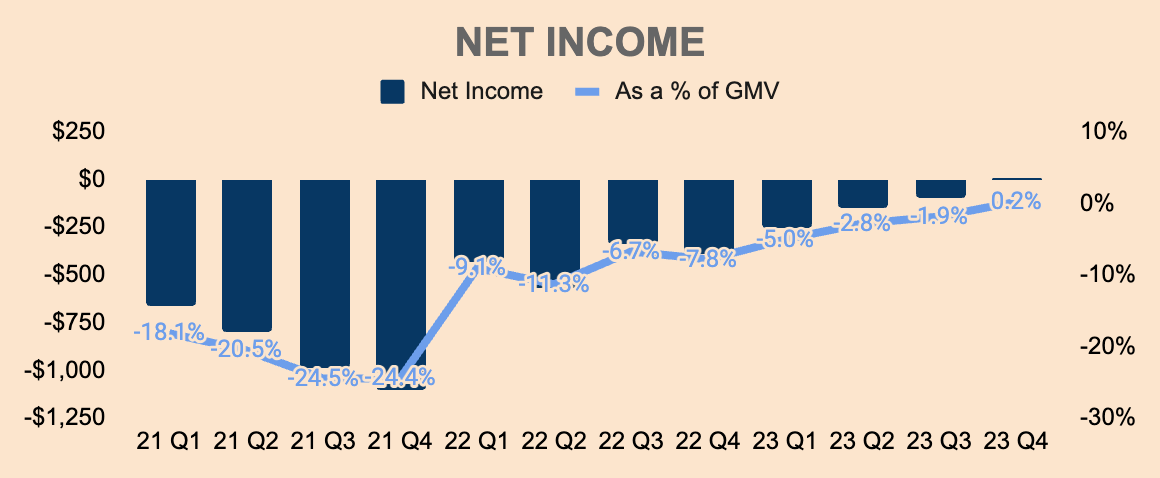

When it comes to the underside line, Seize turned worthwhile on a Web Revenue foundation for the primary time ever. In This autumn, Web Revenue was $11M, which was 0.2% as a % of GMV. Web Revenue was higher than Working Revenue on account of enchancment in truthful worth adjustments in investments in addition to increased internet curiosity revenue.

Writer’s Evaluation

Will increase in Adjusted EBITDA additionally contributed to revenue development.

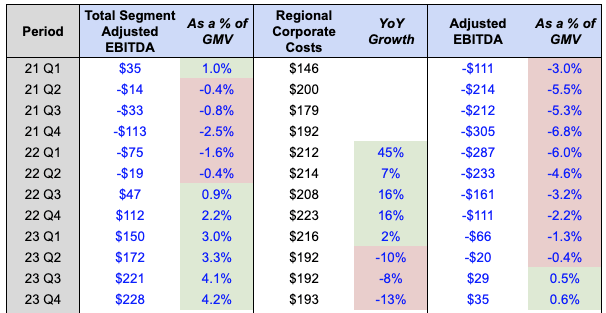

As you may see, Whole Phase Adjusted EBITDA has been rising with every passing quarter with $228M in This autumn, which is 4.2% of GMV, up 200 foundation factors YoY.

Subtracting Regional Company Prices, we get Adjusted EBITDA, which has been bettering as nicely. In This autumn, Adjusted EBITDA was $35M, which is the eight consecutive quarter of enchancment. This represents 0.6% of GMV, up 280 foundation factors YoY, on account of decrease Regional Company Prices as the corporate started layoffs in June last year.

Writer’s Evaluation

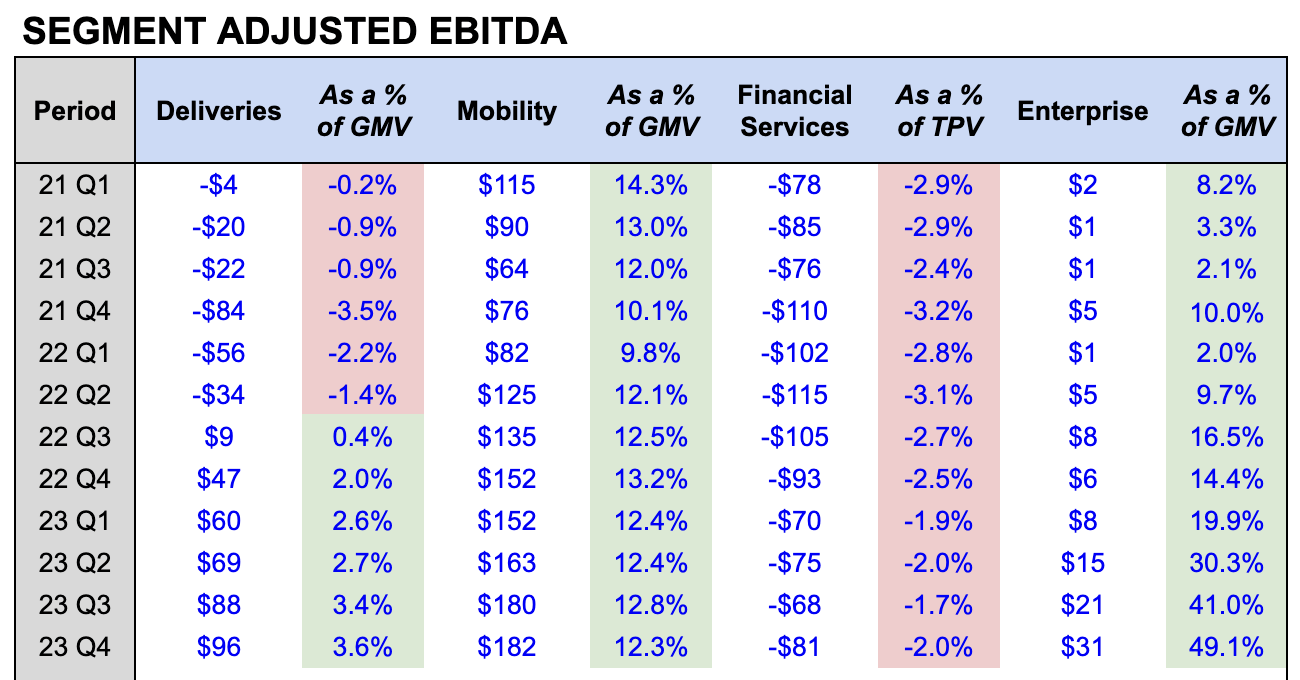

Phase Adjusted EBITDA, we are able to see the profitability of every section:

- This autumn Deliveries Adjusted EBITDA: $96M, or 3.8% of GMV. Margins proceed to enhance on account of incentive optimization, working leverage, and GMV development. Shifting ahead, administration expects Adjusted EBITDA Margin to increase by one other 100 to 200 foundation factors.

- This autumn Mobility Adjusted EBITDA: $182M, or 12.3% of GMV. Margins had been down 90 foundation factors YoY and 50 foundation factors QoQ. Nonetheless, discover how rather more worthwhile the Mobility Phase is in comparison with Deliveries. That is due to much less competitors within the Mobility area since Seize is just about a monopoly within the Mobility section — much less competitors means increased pricing energy, which ends up in increased margins.

- This autumn Monetary Companies Adjusted EBITDA: $(81)M, or (2.0)% of TPV. This section is the one unprofitable section as administration continues to spend money on the fintech market. Of essential notice, Adjusted EBITDA dropped QoQ as a result of launch of GXBank in Malaysia.

- This autumn Enterprise Adjusted EBITDA: $31M, or 49.1% of GMV. Adjusted EBITDA Margin expanded by about 35 share factors YoY and eight share factors QoQ, displaying sturdy working leverage primarily as a result of ramp in Income. The Enterprise section might be a significant money cow sooner or later, given its sturdy development and profitability profile.

Writer’s Evaluation

As you recognize, Seize has been working at large losses within the first decade of its existence, on account of heavy investments to accumulate customers, launch new merchandise, and increase geographically.

However lately, the corporate has simply turned Web Revenue worthwhile as the corporate centered on optimizing incentives, bettering its value construction, and scaling Income.

As we have seen, Seize’s profitability metrics are all trending in the appropriate path, displaying sturdy economies of scale over the previous couple of quarters.

This is not going to solely make the corporate self-sufficient but in addition strengthen its value benefit and environment friendly scale moats, resulting in an excellent stronger aggressive positioning.

All issues thought of, that is only the start of Seize’s profitability journey.

Well being

Together with bettering profitability, Seize additionally has a fortress balance sheet.

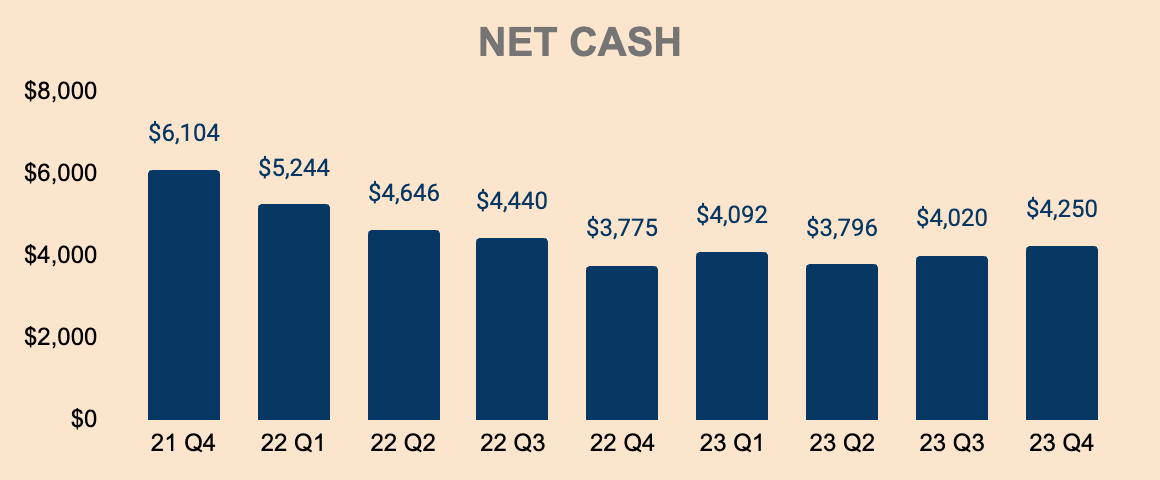

As of This autumn, Seize has a Web Money place of about $4.3B, which is over 30% of its present Market Cap of $12.4B. Web Money has been on a downfall, however that is comprehensible provided that the corporate remains to be in funding mode. Nonetheless, Web Money steadiness ought to develop over the subsequent few quarters as Seize continues to enhance profitability.

Administration additionally plans to repay their Time period Mortgage B debt facility, which is predicted to scale back annual curiosity bills by $50M, additional bettering profitability and money flows.

Writer’s Evaluation

When it comes to money move, Seize remains to be money move destructive on an annual foundation.

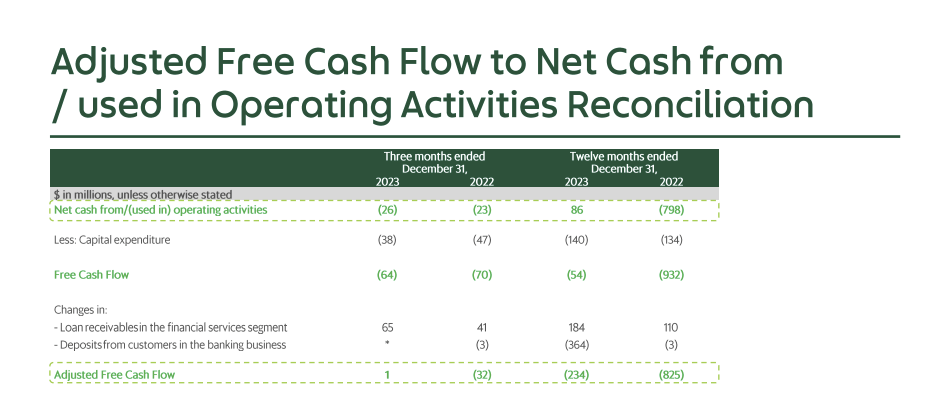

In 2023, Free Money Circulate was $(54)M, a significant enchancment from $(932)M in 2022. Nonetheless, this contains $184M of Loans Receivables and $364M of Buyer Deposits — adjusting for this, Adjusted FCF was $(234)M in 2023, nonetheless an honest enchancment from $(825)M in 2022. This was primarily pushed by increased Money Circulate from Operations, which turned optimistic in 2023 — nice to see however nonetheless lots of work to do.

Seize FY2023 This autumn Investor Presentation

Nonetheless, in gentle of Seize’s bettering profitability and robust steadiness sheet, Seize introduced a $500M share buyback program, which displays not solely administration’s confidence in regards to the monetary well being of the corporate but in addition how enticing the valuation of the corporate is at present costs.

Outlook

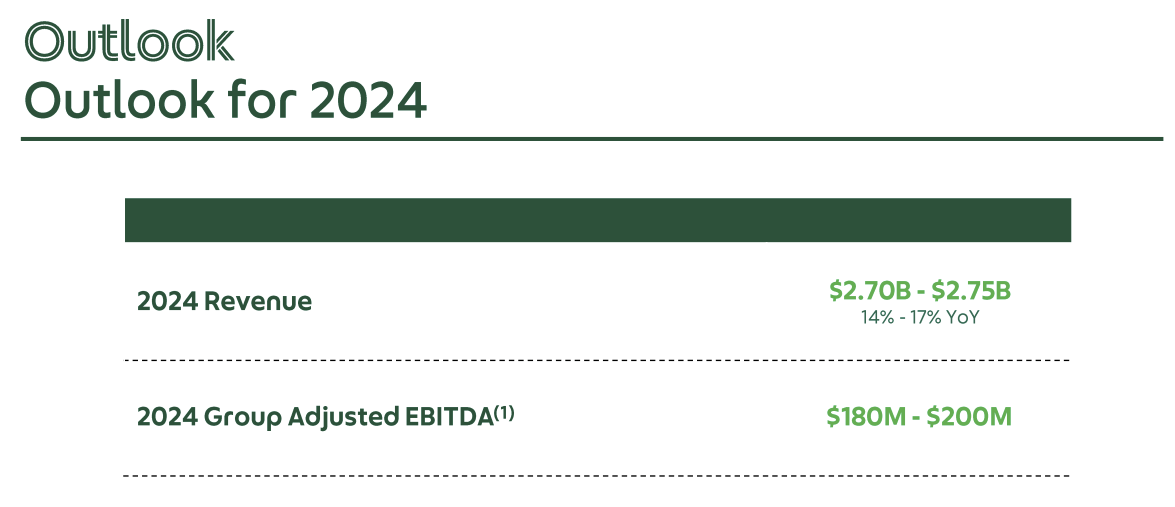

Turning to the outlook, administration offered the next steerage:

- 2024 Income of $2.725B on the midpoint, implying a 15.5% development YoY. This can be a steep deceleration from 2023’s development of 65% YoY and this fell wanting analyst estimates of $2.82B, that are two massive the explanation why the inventory bought off following This autumn earnings.

- 2024 Group Adjusted EBITDA of $190M on the midpoint, which is a big enchancment from final yr’s determine of $(22)M.

Seize FY2023 This autumn Investor Presentation

The CFO additionally gave out extra particulars about their outlook:

- Q1 On-Demand GMV is predicted to be steady QoQ. As a reference, This autumn On-Demand GMV was $4.1B, so if Q1 noticed the identical stage of GMV as This autumn, it implies a 16% YoY development in On-Demand GMV in Q1. Shifting ahead, administration expects “to see a sequential rebound of GMV in the second quarter and continued growth during the year”. In different phrases, count on sturdy On-Demand GMV development all through 2024.

- Administration expects Mobility margins to stay steady at “around 12% plus” and Deliveries margins to be “3% plus through 2024”. In different phrases, count on little to no enhancements in On-Demand margins in 2024. Nonetheless, they count on Deliveries margins to increase 100 to 200 foundation factors past 2024 as the corporate rolls out new product options that drive working leverage and platform monetization.

- For the Monetary Companies section, administration expects “losses to sequentially narrow heading into 2024”. Put merely, count on Monetary Companies margins to enhance shifting ahead.

- Subsequent, count on 2024 Adjusted FCF to “improve substantially” YoY as the corporate continues to drive working leverage.

- Past 2024, administration additionally expects Income development to speed up as the corporate scales new services and products reminiscent of GrabUnlimited, GXBank, and Household Accounts.

Briefly, development is predicted to stay strong as Seize pulls a number of development levers throughout its 4 segments. As well as, profitability is just going to get higher from right here which ought to speed up earnings development within the coming years.

No matter it’s, Seize — though greater than a decade outdated — remains to be in its early phases of development, as a result of present process digital transformation in Southeast Asia.

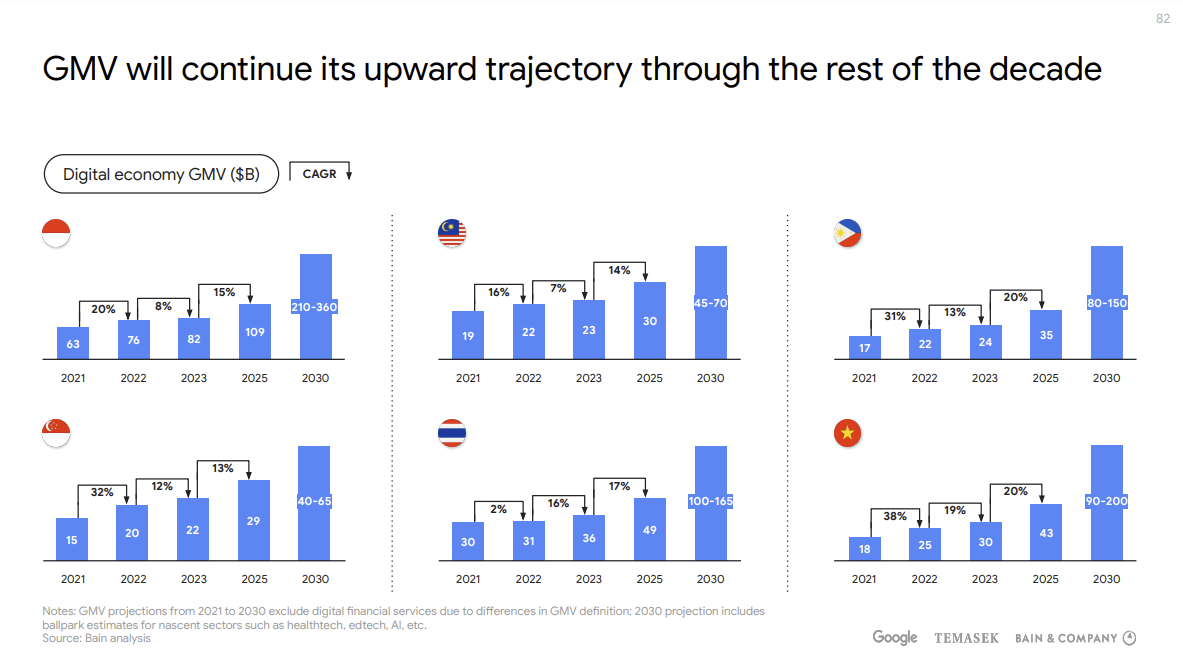

In keeping with the e-Conomy SEA 2023 report, meals supply GMV and mobility GMV in Southeast Asia are anticipated to develop at a 12% and 18% CAGR, respectively, from 2023 to 2025. As well as, digital promoting GMV is about to increase by 15% via 2025.

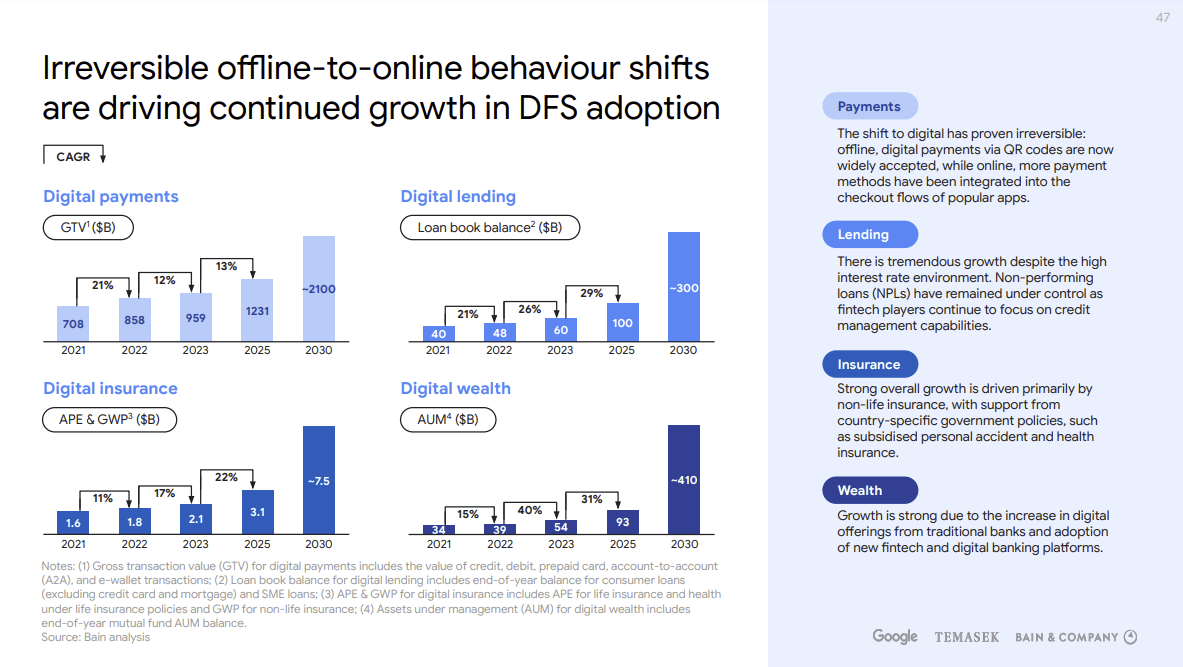

However probably the most thrilling development alternative for Seize lies within the fintech sector. In keeping with the report, digital monetary companies adoption in Southeast Asia is deemed irreversible. As you recognize, Seize gives digital funds, lending, and insurance coverage companies at present, and these subsectors are anticipated to take off within the subsequent few years as you may see beneath.

e-Conomy SEA 2023

Given the underbanked and unbanked majority in Southeast Asia, I imagine Seize’s Monetary Companies has an extended development runway forward. Scaling its monetary merchandise ought to be seamless as Seize can distribute them via its superapp — Seize has the posh to quickly cross-sell its merchandise by tapping its large scale and community.

For these causes, I imagine the complete potential of Seize’s digital Monetary Companies section has but to be realized.

That being mentioned, Seize has a large development runway forward because the regional chief in deliveries, mobility, and monetary companies — the expansion of the digital economic system in Southeast Asia shall be a large tailwind for the superapp.

e-Conomy SEA 2023

Valuation

Valuing Seize is kind of a problem for the reason that firm simply turned worthwhile and that administration has not issued long-term monetary targets.

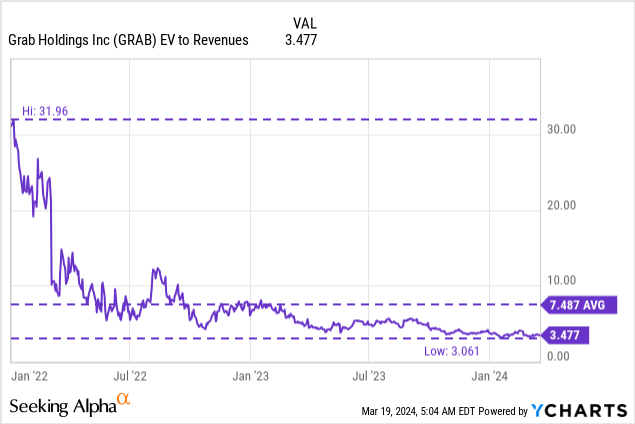

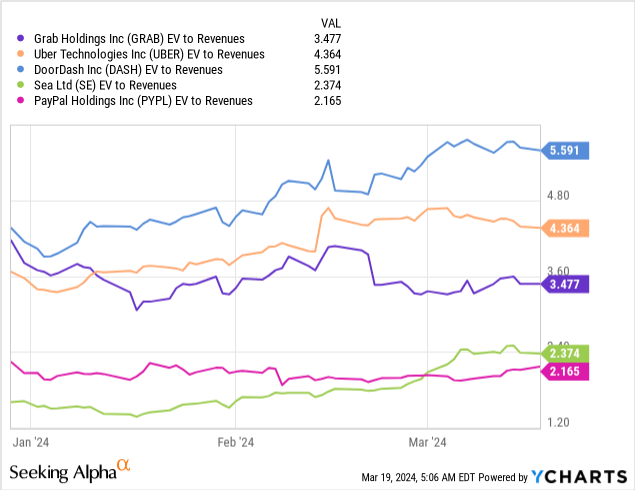

That mentioned, Seize at present trades at an EV to Income a number of of simply 3.5x, which is kind of low cost relative to its peak a number of of 32x and common a number of of seven.5x.

Given the complexity and uniqueness of Seize’s enterprise mannequin, there isn’t any direct competitor that we are able to evaluate with. Nonetheless, it is fascinating to see Seize buying and selling cheaper than its US friends Uber (4.4x) and DoorDash (5.6x) — maybe, US shares get a premium over Asian shares.

On the opposite aspect, Seize is buying and selling extra expensively than fellow Southeast Asian conglomerate Sea Restricted (SE), which is buying and selling at 2.4x. And only for enjoyable, I’ve thrown in PayPal (PYPL) as nicely, which trades at 2.2x.

In my view, Seize ought to be buying and selling at increased valuations in comparison with its peer group contemplating that Seize is actually Uber, DoorDash, and PayPal mashed collectively.

Performing a reduced money move (“DCF”) evaluation on Seize is kind of a redundant train, however I will try it anyway — utilizing very conservative assumptions, in fact.

I shall be utilizing Adjusted EBITDA as a proxy for Money Circulate from Operations, after which subtract Capital Expenditures and Revenue Tax to reach at a determine near the corporate’s Adjusted FCF.

That mentioned, listed here are my key assumptions:

- GMV development of 10% within the first 5 years and eight% within the final 5 years. I imagine these are lowball estimates given Seize’s management place and the expansion of the digital economic system in Southeast Asia.

- Adjusted EBITDA Margin as a % of GMV bettering to 7% by 2033. Once more, fairly conservative provided that:

- Deliveries margin is 3.6% in This autumn — and remains to be increasing.

- Mobility margin is 12.3% in This autumn — and has remained steady for 2 years.

- Monetary Companies margin, whereas nonetheless destructive at (2.0)% of TPV, might surpass Deliveries and Mobility margins. For context, Sea Restricted’s SeaMoney has a excessive Adjusted EBITDA Margin as a % of Income of 31% in This autumn.

- Enterprise margin is already as excessive as 49.1% in This autumn, which might drive significant margin growth for the general firm.

- Revenue Tax is about at a relentless price of 15% of Adjusted EBITDA.

- Capital Expenditures had been 0.7% of GMV within the final two years so I’ll set it at 0.7% for all of the years.

Writer’s Evaluation

Primarily based on the assumptions above, I mission a GMV of almost $50B by 2033 at a Money Circulate Margin of about 5.3% of GMV.

Writer’s Evaluation

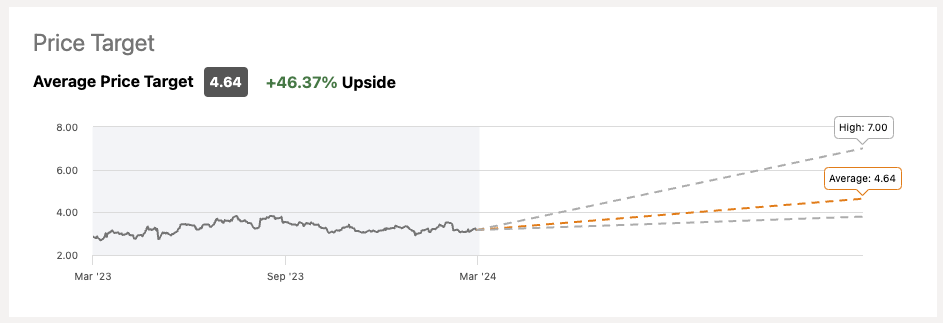

Primarily based on a perpetual development price of two.5% and a reduction price of 10%, I arrive at an intrinsic worth per share of $6.47 for Seize inventory, which represents an upside of greater than 100% at its present worth of $3.17.

As a reference, analysts have a mean price target of $4.64 for Seize inventory with a road excessive of $7.00. As of this writing, there are 21 Sturdy Purchase and 6 Purchase suggestions, with ZERO Promote scores.

In search of Alpha

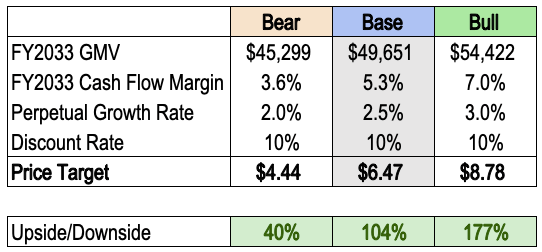

I’ve additionally included my bear and bull circumstances beneath.

Writer’s Evaluation

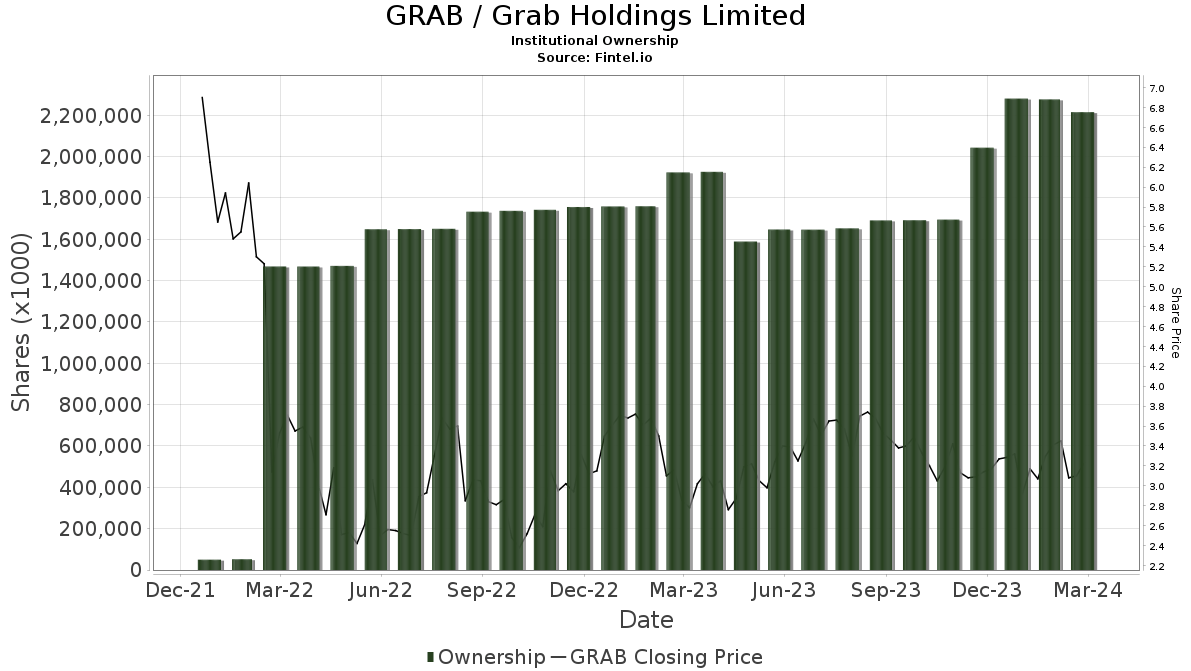

Establishments have additionally been piling on Seize inventory, which might raise the inventory increased.

Fintel

To summarize, I imagine Seize inventory is considerably undervalued.

Dangers

Whereas Seize has established itself as Southeast Asia’s most dominant on-demand companies firm, competitors stays its largest threat.

This contains GoJek, InDrive, and Bolt within the mobility area. Different worldwide gamers might also enter Southeast Asia, together with India’s Ola Cabs and China’s Didi World.

Within the deliveries section, Seize faces competitors from GoJek, ShopeeFood, Foodpanda, Deliveroo, Line Man Wongnai, and extra. Different massive supply corporations might also enter Southeast Asia, together with San Francisco’s DoorDash and India’s Zomato.

Within the fintech area, Seize is already coping with sturdy opposition, together with GoPay, ShopeePay, Dana, Google Pay, and so forth.

All this competitors might result in a worth conflict, forcing Seize to deploy extra incentives to take care of market share. As well as, the companies that Seize gives have the danger of being commoditized, which might imply decrease revenue margins and money flows for the corporate.

Nonetheless, I imagine competitors is extra of a brief subject than a everlasting one. For my part, competitors is unlikely to have the capital assets to compete with Seize on worth. They can undercut Seize for some time, however as I’ve mentioned earlier, they’re incapable of doing so for an extended time period given Seize’s value benefit, community results, and environment friendly scale moats. To not neglect, Seize has $4.3B of Web Money at its disposal.

I feel it is silly to undercut Seize — it is like digging your personal graves.

Different dangers embrace rules that might enhance compliance prices in addition to gig employee unions which might result in decrease fee charges for Seize.

Thesis

In a nutshell, Seize is the baddest superapp in Southeast Asia — its sturdy model, excessive switching prices, highly effective community results, low-cost benefit, and environment friendly scale moats solidify its standing because the undisputed king within the area.

As the corporate turns worthwhile and focuses on worthwhile development, Seize is in a primary place to capitalize on the rising digital economic system in Southeast Asia.

Regardless of being a basically stronger firm as we speak than it has ever been, Seize inventory remains to be down 80%+ from its all-time highs. Furthermore, Seize inventory has been buying and selling sideways for nearly two years — it is primarily in hibernation.

With enterprise momentum again in full power and with fundamentals bettering with every passing quarter, it will not be lengthy earlier than the sleeping large awakens.

With all this in thoughts, I’ve began a place in Seize inventory.