apomares/E+ through Getty Photographs

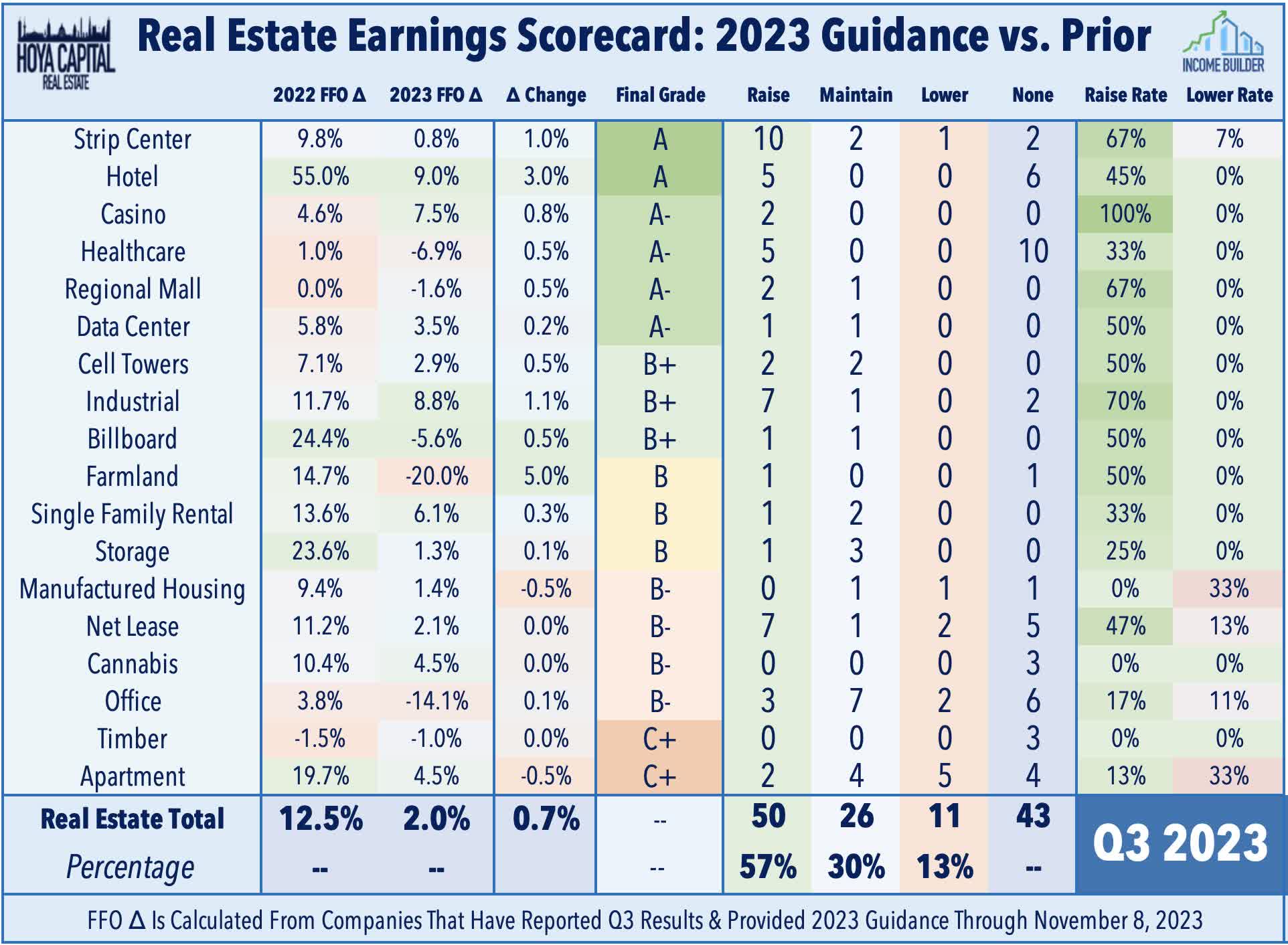

Resort REITs have been the Fifth-best REIT sector for complete return this yr, posting a achieve of 9.35%, holding tempo with the Dow (+9.23%) and outstripping the S&P 400 (+7.88%) and S&P 600 (+5.67%), whereas badly lagging the red-hot Nasdaq (+45.44%) and the S&P 500 (+19.39%).

Hoya Capital Earnings Builder

Resort REITs posted maybe the strongest exhibiting of any REIT sector during Q3 earnings season. All 5 of the Resort REITs that present FFO steering raised that steering.

Hoya Capital Earnings Builder

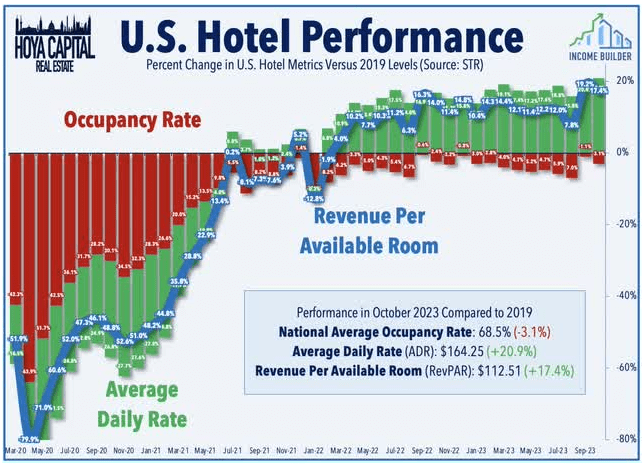

Resort demand is carefully associated to journey quantity. TSA Checkpoint data exhibits passenger quantity stays barely up from pre-pandemic ranges. In the meantime, STR reports that industry-wide, resort Income Per Accessible Room (“RevPAR”) was 17% above 2019 ranges in October. This mirrored a rise of roughly 21% in Common Day by day Room Charges (“ADR”), offset by a drag of about 3% in common occupancy charges.

Hoya Capital Earnings Builder

The uptick in journey shouldn’t be benefitting all lodges equally, nonetheless. As Hoya Capital not too long ago famous:

Distant work is altering the complexion of enterprise demand, however not essentially to the detriment of the resort {industry}. The “traveling salesman” visits are being changed by extra frequent group occasions whereas “work-from-anywhere” hybrid work-leisure journeys are skewing demand in the direction of extra “destination” segments . . . We favor the higher-margin limited-service phase and choose full-service names with a “destination” focus.

In the meantime Internet Lease REITs had been among the many poorer performers in Q3 earnings season, rating 14th out of 18 REIT sectors. However the Internet Lease sector graded out at an honest B-, as 7 of the ten corporations that present FFO steering raised that steering, in comparison with 2 that lowered. Internet Lease REITs had been hampered by cap-rate compression in acquisitions, but buoyed by strong performance from their retail clients.

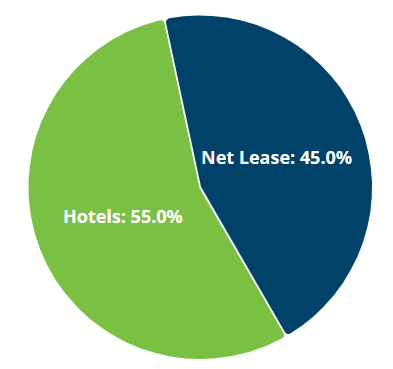

This text will look at an organization whose property are cut up nearly evenly between Resort and Internet Lease properties.

Meet the corporate

Service Properties Belief

Headquartered in Newton, Massachusetts, and externally managed by RMR Group, Service Properties Belief (NASDAQ:SVC) was based in 1995. Twenty-eight years later, it’s nonetheless a small-cap ($1.25 billion).

The corporate owns and operates 221 lodges (about 38,000 rooms), representing an funding of $6.2 billion, in addition to 761 retail websites (13.4 million rentable sq. toes), for an funding of $5.1 billion.

SVC Investor Presentation, November 2023

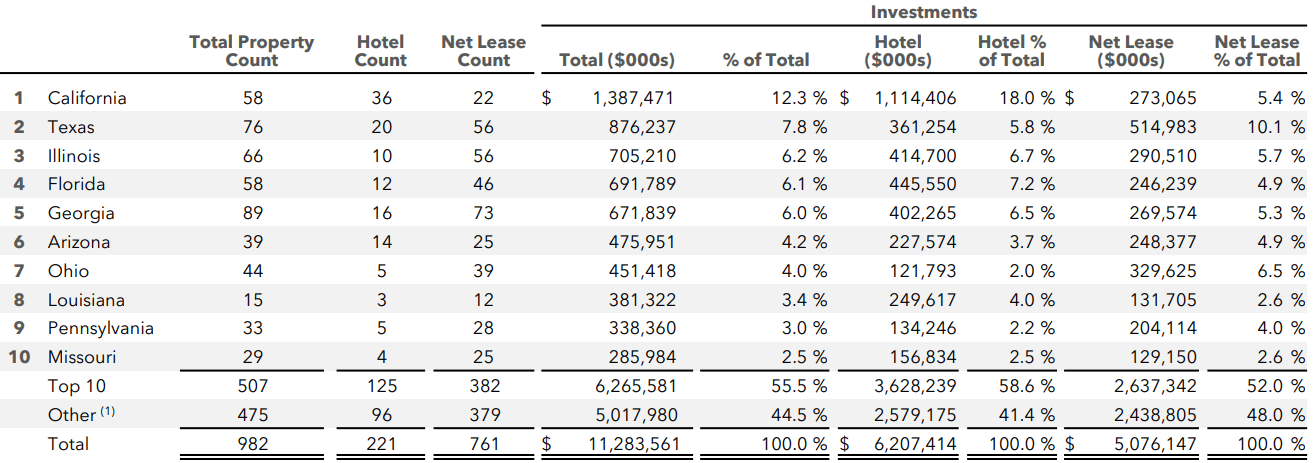

SVC property are unfold throughout 46 U.S. states, in addition to Washington, DC, Puerto Rico, and Canada. Nevertheless, greater than half of the corporate’s property, in each lodges and internet lease retail, are concentrated within the prime 10 states:

- California,

- Texas,

- Illinois,

- Florida,

- Georgia,

- Arizona,

- Ohio,

- Louisiana,

- Pennsylvania, and

- Missouri

SVC Investor presentation

Resort portfolio

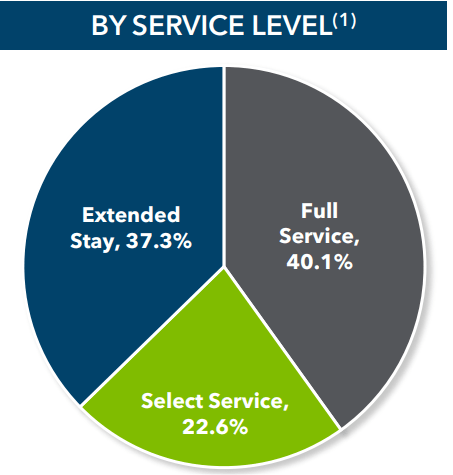

About 40% of SVC’s lodges are full service operations, and one other 37% prolonged keep, leaving solely 23% within the limited-service class that Hoya Capital favors for the close to future.

SVC Investor Presentation, November 2023

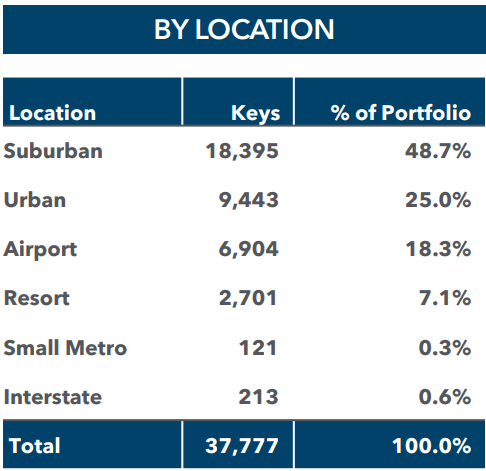

And solely 7% are clearly “destination” lodges, though a few of the city properties may additionally be thought of as such. Almost half are within the suburbs, and one other 18% are close to airports.

SVC Investor Presentation, November 2023

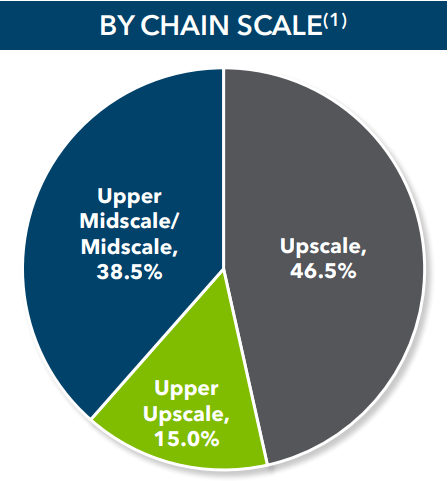

In keeping with administration, over 60% of SVC’s lodges are upscale or “upper upscale”, with solely 38.5% within the midscale vary.

SVC Investor Presentation, November 2023

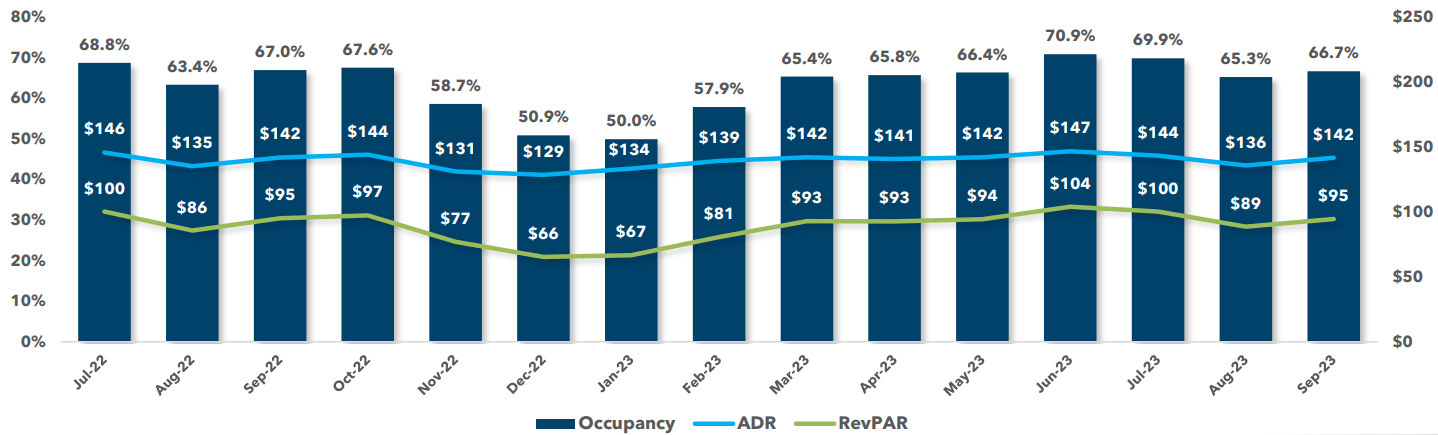

Occupancy has ranged from 50% throughout December and January to as excessive as 71% in June, averaging an unimpressive 63.6% over the previous 15 months.

SVC Investor Presentation, November 2023

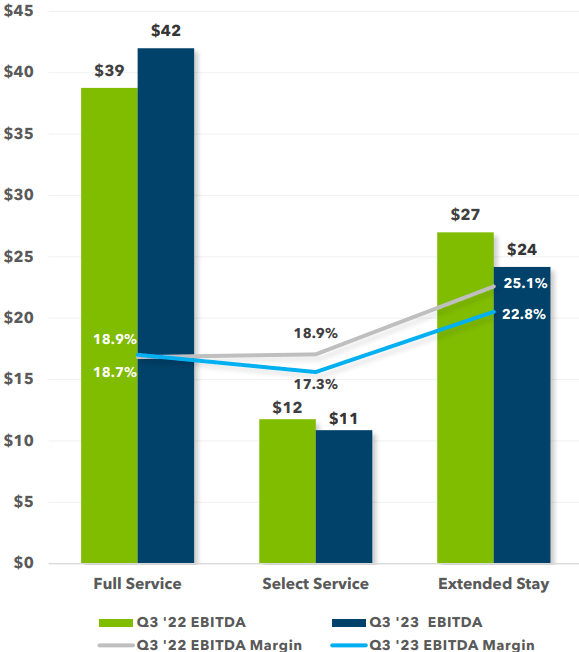

EBITDA generated by the Full-service phase rose 7.7% YoY (yr over yr) to $42 million in Q3, producing an EBITDA margin of 18.9%, barely up from 2022.

The Prolonged Keep phase EBITDA fell 11.1% to $24 million, producing EBITDA margin of twenty-two.8%, down 230 foundation factors from 2022.

In the meantime, the Choose Service phase EBITDA fell 8.3% to $11 million, producing a margin of 17.3%, down from 18.9% YoY.

SVC Investor Presentation, November 2023

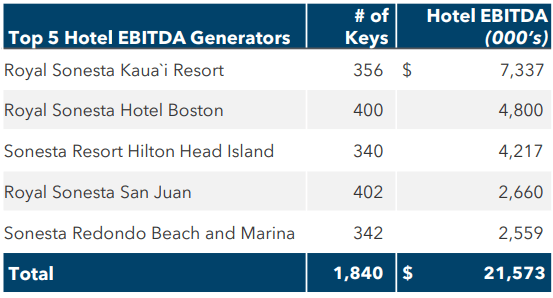

All 5 of SVC’s prime EBITDA mills on the Resort facet of the enterprise had been Sonestas.

SVC Investor Presentation, November 2023

SVC owns 34% of Sonesta, which is the Eighth-largest resort chain on the planet, and contains a number of well-known manufacturers, together with Purple Lion and America’s Greatest Worth.

SVC Investor Presentation, November 2023

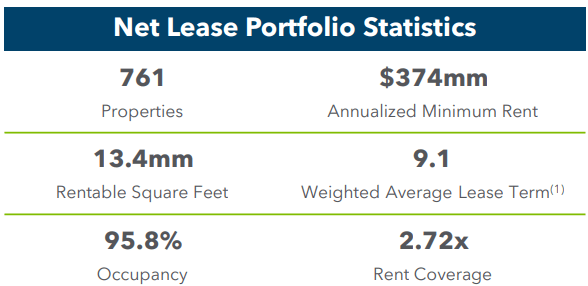

Internet Lease Portfolio

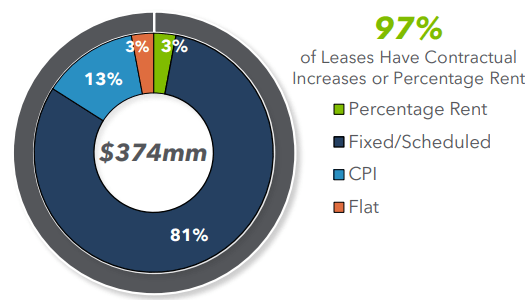

On the Internet Lease facet of the enterprise, the corporate’s 761 properties generate an ABR (annual base hire) of $374 million, with a weighted common lease time period of 9.1 years. The portfolio is 95.8% occupied, and hire protection stands at 2.72.

SVC Investor Presentation, November 2023

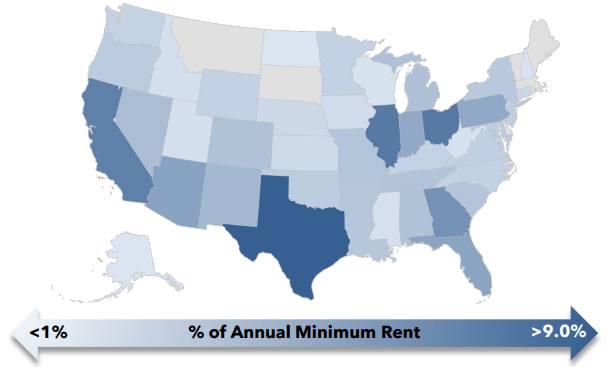

The web lease portfolio stretches throughout 43 U.S. states, leaving out solely Montana, South Dakota, Delaware, Rhode Island, Massachusetts, Vermont, and Maine. The heaviest concentrations are in:

- Texas,

- California,

- Illinois,

- Ohio, and

- Georgia

SVC Investor Presentation, November 2023

adopted by:

- Arizona, Pennsylvania

- Indiana, and

- Florida.

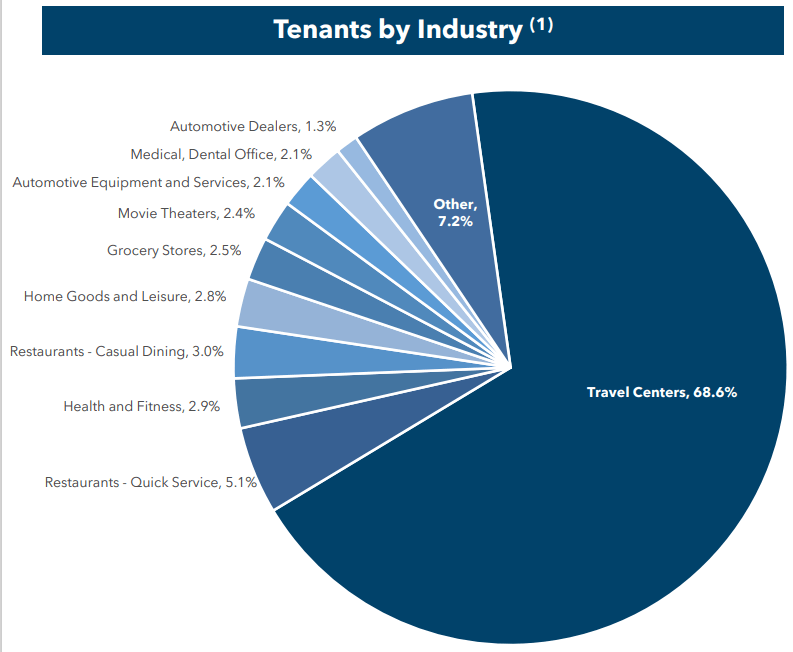

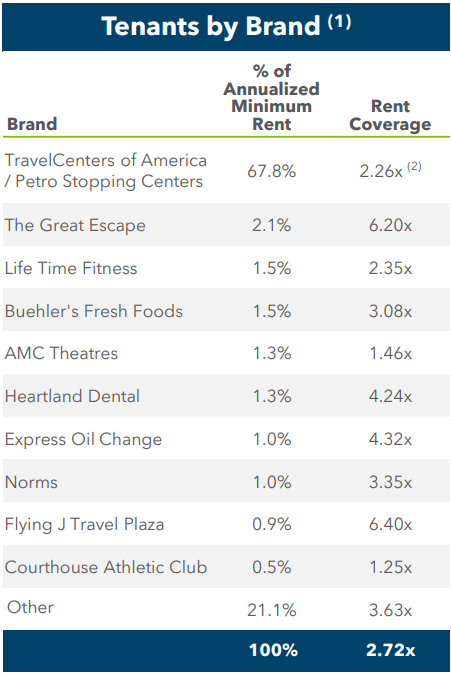

SVC’s internet lease tenants are diversified throughout 21 industries and 135 manufacturers.

SVC Investor Presentation, November 2023

That appears pretty spectacular at first blush, however by {industry}, SVC relies upon closely on journey facilities, which contribute 68.6% of ABR. All different classes are small by comparability.

SVC Investor Presentation, November 2023

Tenant diversification by firm is way from superb, with one buyer (TravelCenters of America) contributing over two-thirds of SVC’s rental income.

SVC Investor Presentation, November 2023

This important tenant operates 176 journey facilities, working beneath two manufacturers, in difficult-to-replicate areas alongside U.S. interstate highways. SVC has 5 grasp triple internet leases with Journey Facilities of America, that run via 2033, with 50 years of extension choices, and rents are assured by BP Company of North America.

A full 97% of SVC’s internet leases presently deployed have contractual will increase inbuilt, with 13% of those pegged to the patron worth index.

SVC Investor Presentation, November 2023

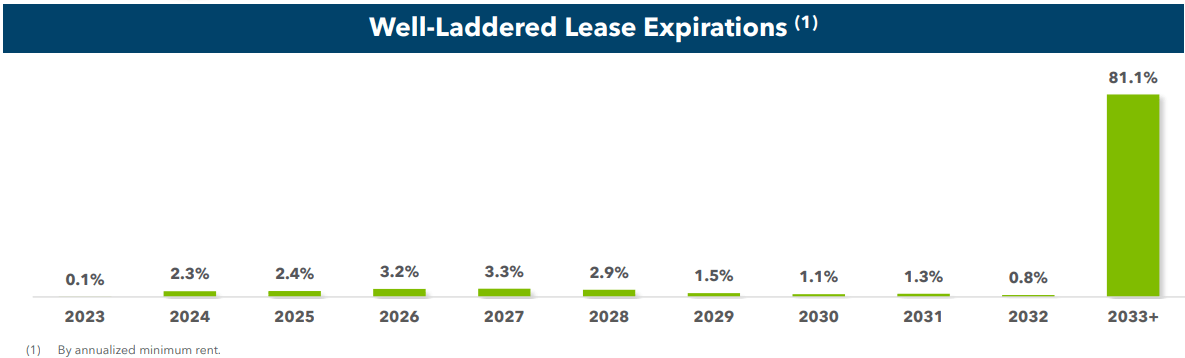

Maybe essentially the most spectacular factor in regards to the internet lease portfolio is the expiration schedule, which exhibits no more than 3.3% of ABR expiring in any single yr over the following 10.

SVC Investor Presentation, November 2023

Quarterly Outcomes

Q3 outcomes for SVC had been messy. The corporate operated at a quarterly loss, however for the primary 9 months of 2023, internet earnings was optimistic, at $10.5 million. Q3 FFO rose by 3.8% YoY, and thru the primary 9 months, confirmed a 29.8% enchancment YoY, principally due to simple comparables, following the disaster of early 2022. FFO per share confirmed an identical sample to FFO. In the meantime, the corporate’s EBITDA for Q3 was down (-12.7)% from the earlier yr, however up 17.8% for the primary 9 months. And the corporate has held share depend regular, so shouldn’t be diluting shareholder worth in an try to flee its troubles.

| Q3 | Q3 | YTD | YTD | ||||

| Metric | 2023 | 2022 | % Change | 2023 | 2022 | % Change | |

| Internet Earnings | (-$4128) | $7500 | NA | $10,544 | (-$100,972) | NA | |

| FFO | $91,731 | $88,397 | 3.8% | $221,376 | $170,597 | 29.8% | |

| FFO/share | $0.56 | $0.54 | 3.7% | $1.34 | $1.04 | 28.8% | |

| EBITDA | $170,408 | $195,267 | (-12.7)% | $520,394 | $441,663 | 17.8% | |

| Common Shares | 165,027 | 164,745 | 0.02% | 164,933 | 164,697 | 0.01% |

Supply: SVC Investor Presentation, November 2023

Progress metrics

Listed below are the 3-year progress figures for FFO (funds from operations), and TCFO (complete money from operations). Like most REITs, SVC’s revenues took a ferocious beating through the COVID disaster, however not like most, SVC’s restoration has been very sluggish. FFO ranges in the present day are lower than half the place they stood in 2019., averaging an appalling (-16.5)% slippage every year.

| Metric | 2019 | 2020 | 2021 | 2022 | 2023* | 4-year CAGR |

| FFO (hundreds of thousands) | $608 | $221 | $(-11.5) | $244 | $295 | — |

| FFO Progress % | — | (-63.7) | NA | NA | 20.9 | (-16.5)% |

| FFO per share | $3.78 | $1.23 | $1.50 | $1.72 | $1.72 | — |

| FFO / share progress % | — | (-67.5) | 22.0 | 14.7 | 0.0 | (-16.7)% |

| TCFO (hundreds of thousands) | $260 | (-$311) | (-$544) | (-$132) | (-$21) | — |

| TCFO Progress % | — | NA | NA | NA | NA | NA |

* estimate, based mostly on Q3 outcomes

Supply: Searching for Alpha Premium, Hoya Capital Earnings Builder, and creator calculations

The Bloomberg analyst consensus 2024 forecast requires FFO per share of $1.78, which might symbolize mediocre progress of three.5%.

InsiderCow.com exhibits no insider buys or sells over the previous 12 months. SVC’s return on fairness over the previous 12 months has been (-1.52)%, whereas the corporate has grown its property by a negligible 1.5%.

In the meantime, right here is how the inventory worth has carried out over the previous 3 twelve-month durations, in comparison with the REIT common as represented by the Vanguard Actual Property ETF (VNQ).

| Metric | 2020 | 2021 | 2022 | 2023 | 3-yr CAGR |

| SVC share worth Dec. 6 | $13.51 | $8.54 | $7.43 | $7.63 | — |

| SVC share worth Acquire % | — | (-36.8) | (-13.0) | 2.7 | (-13.3) |

| VNQ share worth Dec. 6 | $86.42 | $109.66 | $85.22 | $83.54 | — |

| VNQ share worth Acquire % | — | 26.9 | (-22.3) | (-2.0) | (-0.84) |

Supply: MarketWatch.com and creator calculations

Whereas the VNQ bounced again strongly from the pandemic in 2021, with a achieve of 27%, SVC shares continued to plummet, shedding one other (-37)% of their worth. The corporate outperformed the VNQ final yr, dropping solely (-13)%, in comparison with the VNQ’s (-22)%. This yr, SVC is up somewhat at +2.7%, whereas VNQ is down somewhat, at (-2.0)%. However as a 3-year funding proposition, SVC has vastly underperformed the VNQ, dropping an annual common of (-13.3)%, whereas the VNQ has been primarily flat at (-0.84)%.

Steadiness sheet metrics

SVC administration assures buyers in its November presentation that they’ve a “Strong balance sheet.” Listed below are the chilly, laborious info.

| Firm | Liquidity Ratio | Debt Ratio | Debt/EBITDA | Bond Score |

| SVC | 1.21 | 83% | 9.0 | B+ |

| Resort REIT avg | 1.81 | 42% | 6.4 | — |

| Internet Lease REIT avg | 2.12 | 34% | 6.2 | — |

| General REIT avg | 1.91 | 30% | 6.3 | — |

Supply: Hoya Capital Earnings Builder, Searching for Alpha Premium, and creator calculations

Although bond-rated, SVC’s liquidity ratio of 1.21 and debt ratio of 83% are abysmal, and the 9.0 Debt/EBITDA ratio casts doubt on the corporate’s potential to develop its method out of this gap.

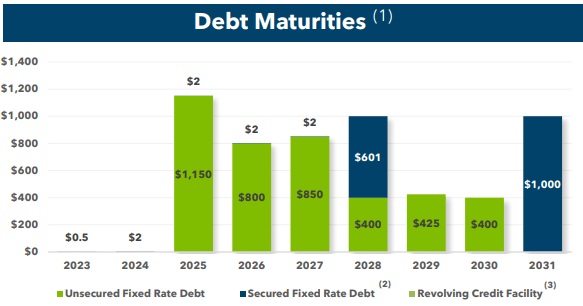

SVC has long-term money owed totaling $5.7 billion, over in opposition to $418 million in money and equivalents, and $650 million obtainable on their revolver. All of the money owed are held at rates of interest exceeding 5.0%. The WAIR (weighted common rate of interest) computes to roughly 5.95%, as follows:

| Sort of Debt | Principal | Int. Charge | Curiosity |

| Unsecured fixed-rate senior notes | $4.0 bn | 5.33% | $213.2 mn |

| Secured fixed-rate senior notes | $1.0 bn | 8.625% | $ 86.25 mn |

| Secured fixed-rate mortgage notes | $0.601 bn | 5.60% | $ 33.9 mn |

| Debt Whole and Weighted Common Curiosity | $5.6 bn | 5.95% | $333.3 mn |

That is by far the best WAIR of any firm I’ve reviewed for Searching for Alpha.

A take a look at the maturity schedule exhibits the corporate has negligible funds in 2024, however that’s principally as a result of they issued $1 billion price of senior secured notes at a blistering 8.625%, to cowl the 2024 maturities. Borrowing at larger curiosity, to repay near-term obligations is a troubling signal. Curiosity expense will reduce considerably into FFO for the foreseeable future.

Even so, a formidable 20% of their debt nonetheless comes due in 2025.

SVC Investor Presentation, November 2023

Dividend metrics

SVC’s biggest attraction to the investor is its 10.5% dividend yield. But, if you consider the truth that the corporate slashed the dividend from $0.54 to a mere penny through the pandemic, and has since restored it solely to $0.20, SVC finally ends up paying about what you’ll anticipate for a Resort/Internet Lease hybrid REIT, over the approaching 3 years.

| Firm | Div. Yield | 5-yr Div. Progress | Div. Rating | Payout | Div. Security |

| SVC | 10.5% | (-17.7)% | 5.85 | 50% | D |

| Resort REIT avg | 5.8% | (-5.4)% | 4.91 | 51% | C |

| Internet Lease avg | 6.0% | 2.6% | 6.48 | 78% | C |

| REITs total | 3.9% | 5.0% | 4.51 | 66% | C |

Supply: Hoya Capital Earnings Builder, TD Ameritrade, Searching for Alpha Premium

Dividend Rating initiatives the Yield three years from now, on shares purchased in the present day, assuming the Dividend Progress price stays unchanged.

Nevertheless, that juicy 10% yield will solely proceed to be loved so long as the corporate doesn’t reduce the dividend. Sadly, owing to SVC’s indebtedness issues and income struggles as seen above, there’s a tangible threat that the dividend could also be reduce within the coming 12 months.

Valuation metrics

SVC is grime low cost at 4.4x FFO ’23, and it trades at a really steep (-36.4)% low cost to NAV, however that does not make it a cut price. For my part, SVC is reasonable for a purpose, and research by Hoya Capital signifies that low cost REITs have a tendency to remain low cost.

| Firm | Div. Rating | Value/FFO ’23 | Premium to NAV |

| SVC | 5.85 | 4.4 | (-36.4)% |

| Resort REIT common | 4.91 | 9.4 | (-21.3)% |

| Internet Lease REIT common | 6.48 | 13.3 | (-5.0)% |

| General REIT common | 4.51 | 17.0 | (-18.0)% |

Supply: Hoya Capital Earnings Builder, TD Ameritrade, and creator calculations

What may go unsuitable?

SVC is closely depending on one tenant. As Journey Facilities of America goes, so goes SVC. If sudden reversals ought to happen for this one underlying enterprise, the results to SVC could possibly be as dangerous or worse.

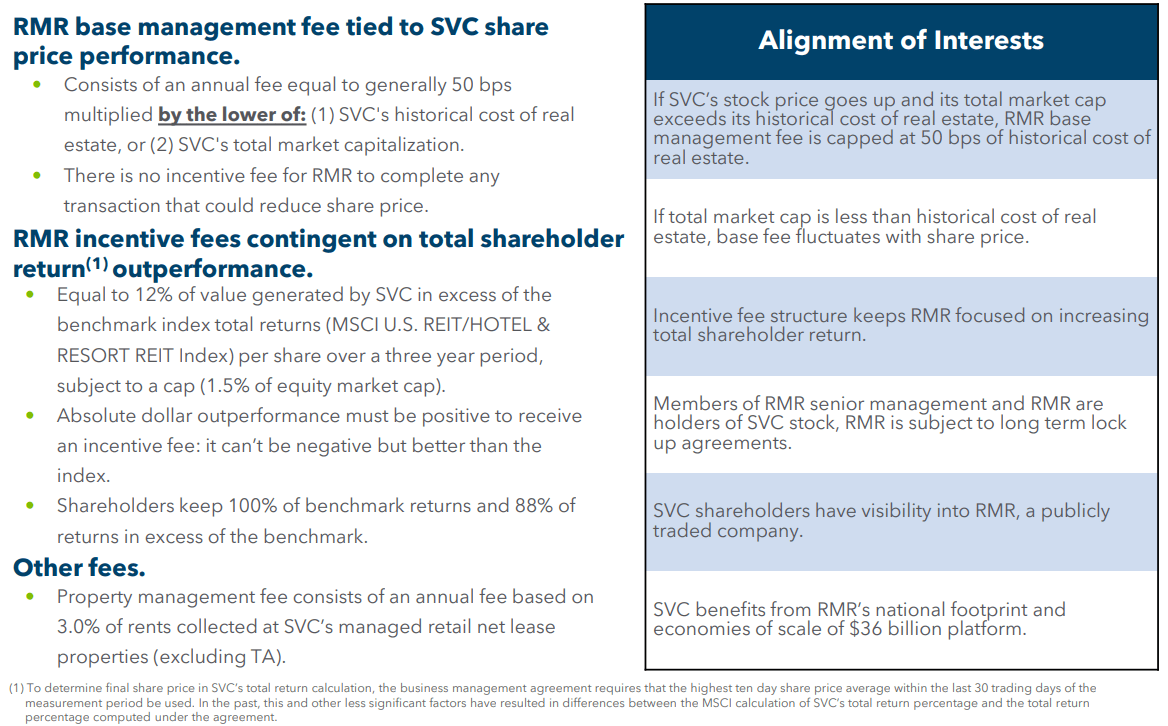

SVC is externally administration by RMR Group. The pursuits of RMR Group might at occasions battle with the pursuits of SVC and its shareholders. The graphic beneath provides extra particulars on that relationship.

SVC Investor Presentation, November 2023

There may be palpable threat of a dividend reduce, which would go away SVC buyers with the worst of each worlds: diminished money earnings and a pointy drop in share worth.

Investor’s backside line

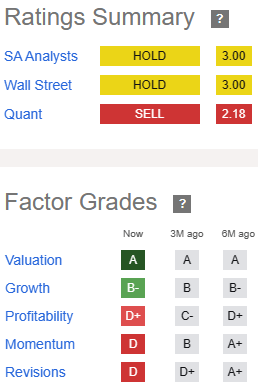

Service Properties is a possible yield entice. With excessive indebtedness and struggles on the income facet of the image, the ultra-high 10.5% yield doesn’t take a look at all protected, and thus the chance of a drop in share worth that greater than offsets the yield is unmistakable. I can not suggest shopping for shares on this firm, and if I had been holding shares, I might strongly think about reallocating that capital elsewhere. There are numerous higher investments than this firm proper now. I price SVC a Promote.

Searching for Alpha Premium

I’m not alone in that opinion. The Searching for Alpha Quant Rankings system additionally charges SVC a Promote, as does Zacks, and one of many 4 Wall Avenue analysts overlaying the agency. The typical analyst worth goal for SVC is $8.83, implying 15.7% upside.

Nevertheless, as all the time, the opinion that issues most is yours. As a result of it is your cash.