JazzIRT/E+ by way of Getty Photos

Shockwave Medical (NASDAQ:SWAV) is a pioneer in intravascular lithotripsy, with a just lately reset valuation attributable to momentary components. The corporate has continued 2023 with robust income progress however some coming hiccups. The inventory has dipped attributable to ongoing concern round GLP-1 medicine and impression on the medical tools market in the long run. Compounding issues, Shockwave is navigating weak point in its present peripheral enterprise and coming 2024 uncertainty within the second half. Mix these components collectively and the inventory is down 29% over the previous yr whilst income ramps with GAAP profitability. Shockwave now trades at simply 10x gross sales and 38x forward earnings for 2024. Let’s study the present points which can be hurting SWAV shares and why it is a purchase right here.

Q3 outcomes strong however steerage disappointment

Shockwave confirmed continued excellence in Q3 outcomes with $186 million income for 42% income progress. As the corporate scales, the expansion charges are declining, however profitability is robust, with working revenue rising to $43.6 million earlier than taxes. Above 23% working margin is sort of good as the corporate continues to be solidly in an funding section and 30+% working margins long run are anticipated. The corporate is slowly constructing out presence in worldwide markets like Germany, Japan and China, which can take effort and time to assist future progress. SWAV has a robust money place from a 1.0% convertible notice providing of $650 million in August 2023 of $917.3 million. At a market cap of simply $6.36 Billion as we speak, Shockwave is now priced very fairly in comparison with its latest previous. The timing of that notice providing was poor for shareholders, and sure contributed considerably to latest draw back within the inventory. Just one% curiosity on the notes have been favorable phrases for Shockwave, making it an inexpensive transfer from administration coming right into a extra unsure 2024 interval. On the constructive information entrance, the corporate has added 20-30% further fee for physicians performing IVL beginning January 1, 2024. The class 1 CPT code provides $140 in fee, additional benefitting docs performing efficient lithotripsy procedures.

One huge motive for the drawdown after the earnings was the reiterated steerage by administration at $727.5m income for the yr. That is the primary time Shockwave hasn’t elevated their steerage in latest historical past. The weak point in information is said to the preauthorization subject, which I dive into under.

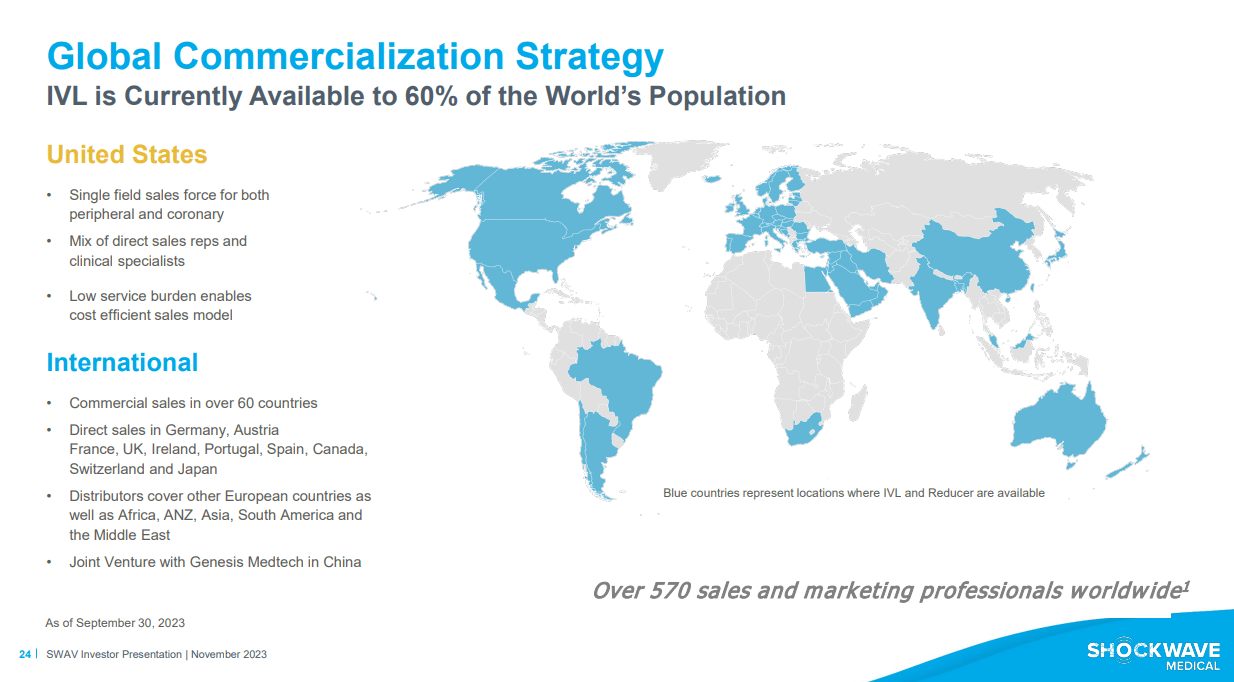

SWAV Worldwide Publicity (SWAV IR)

Preauthorization Strain

The second main subject that started in September, in response to administration, is strain on preauthorization processes. This was seen largely in peripheral limb procedures, on this case from these with leg ache. Peripheral revenues in Q3 solely grew 30%, versus 50% for coronary procedures, displaying the sizable impression that is having on progress. Primarily, non-public insurance coverage payers like Aetna are wanting potential sufferers to bear train or different remedy previous to permitting Shockwave procedures. It is a price saving measure and follows an article within the Wall Road Journal in the summertime outlining overuse. Whereas I have never been in a position to find that article, it is a phenomenon outlined by different medical expertise friends on Q3 earnings calls. Encourage Medical (INSP) additionally known as out points on this space in Q3, displaying a possible space the place insurance coverage suppliers assume they’ll enhance financials by slowing these expensive newer procedures. This subject has much less readability on when it can resolve and is prone to be a big headwind in 2024. Nonetheless, the inventory dropped considerably on the Q3 outcomes, from over $215 to beneath $178 as we speak.

Whereas present analyst consensus for 2024 is for $926m in income or 26% progress for the yr, it’s doubtless the market expects revenues beneath that giving upside if revenues can shock to the upside. 26% income progress continues to be distinctive, and you’ll see under working margin is holding up within the low 20% vary even with growth internationally. Worldwide ought to improve in significance in 2024 and new product launches like C2+ in the US will assist increase gross sales. This gadget for coronary procedures is in full launch in worldwide markets and has boosted progress there with its further energy for tough lesions.

Second half 2024 ‘air pocket’

Administration has spoken for round a yr a couple of potential subject in 2024 referring to Medicare process funds for coronary IVL. Shockwave has pushed for its present transitional passthrough code to be made everlasting for the beginning of 2024. Nonetheless, it was not included within the guidelines for 2024, so the everlasting code is prone to begin at first of 2025. That is largely a problem as a result of the present code expires June 30, 2024 which means the second half of 2024 could have diminished fee for hospital outpatient procedures. It is a progress space for SWAV and sure will harm income for Q3 and This fall of 2024. This can be partially mitigated by some procedures being pulled ahead, and a possible giant rebound in volumes with Q1 of 2025. It is a giant motive for SWAV weak point this summer season, because the market hates uncertainty. The code wasn’t on the docket in August, inflicting the inventory fell $30 in a brief interval on elevated quantity, displaying its impression on investor sentiment. United States coronary income has been the strongest space for SWAV because the code was granted, making it a brief time period fear for buyers. Excellent news on this entrance is it is a momentary subject, which is now properly understood by the market and needs to be priced in solely. Whereas administration would not really feel it can considerably impression volumes because of the quick interval, the market is reflecting this weak point within the share worth already. If something, this might show a blessing in disguise for buyers that imagine within the expertise long run.

Compelling Danger/Reward – Purchase rated

Whereas the inventory is at a yearly low like it’s now, I so as to add to long run positions. Whereas 2024 is prone to be a yr stuffed with potential for volatility and worth swings, the inventory is used to this sort of motion. These with a excessive threat urge for food on the lookout for outsized positive aspects can be clever to take a look at SWAV, simply figuring out it can transfer closely on reimbursement and earnings information. The corporate sells an modern excessive margin product with a robust future forward of it. These sorts of merchandise are going to beat any quick time period weak point associated to payer associated dynamics, as the advantages of Shockwave IVL remedy far outweigh the prices. Progress will proceed over the following 5 years, with a big money hoard which means no important dilution for present shareholders from right here.