ArtistGNDphotography

Synopsis

Simpson Manufacturing (NYSE:SSD) is an organization that designs and manufactures high-quality wooden and concrete development merchandise. SSD’s 2023 income development was considerably decrease than the earlier years. Nevertheless, regardless of income development fluctuations, its margins remained strong over time. Trying forward, SSD has positioned itself effectively to develop its market share within the fastener market. As well as, the opposite two key core addressable markets have sufficient room for SSD to develop into, thus offering it with the tailwind wanted to develop its enterprise within the foreseeable future. Nevertheless, its present share value lacks a ample margin of security. On prime of that, SSD additionally confronted difficult macroenvironment in each the US and Europe. On these notes, I’m recommending a maintain ranking for SSD.

Historic Monetary Evaluation

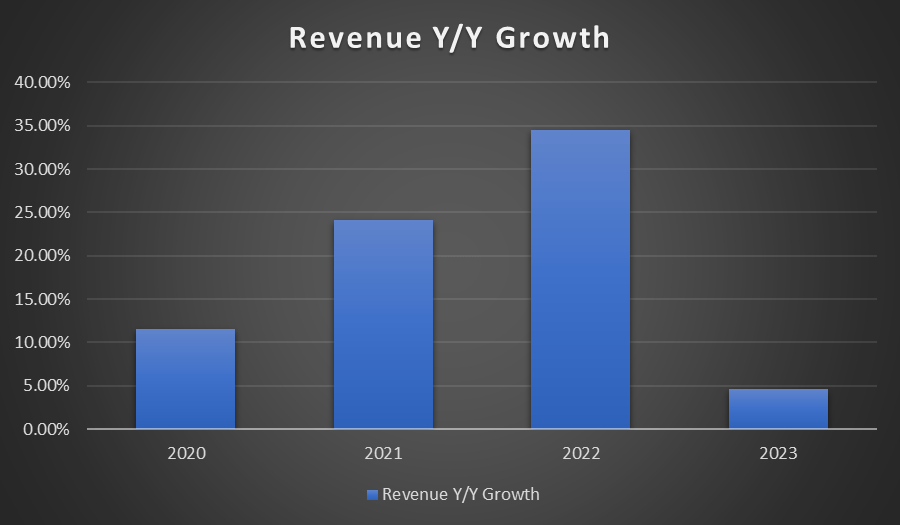

Primarily based on the next chart, it’s clear that 2023’s revenue development has decelerated drastically in comparison with the earlier years. The decrease development charge was pushed by difficult environments such because the decrease US housing begins. In Europe, it was additionally dealing with difficult financial headwinds and decrease development exercise.

Writer’s Chart

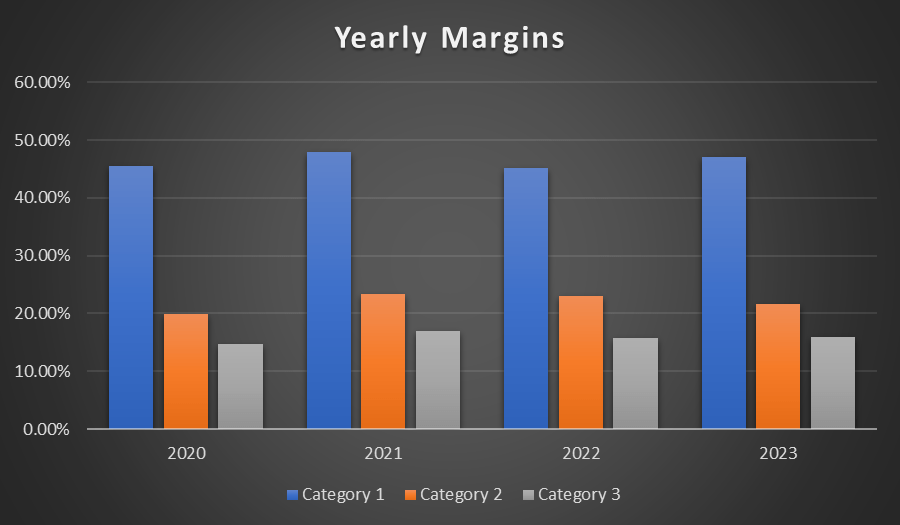

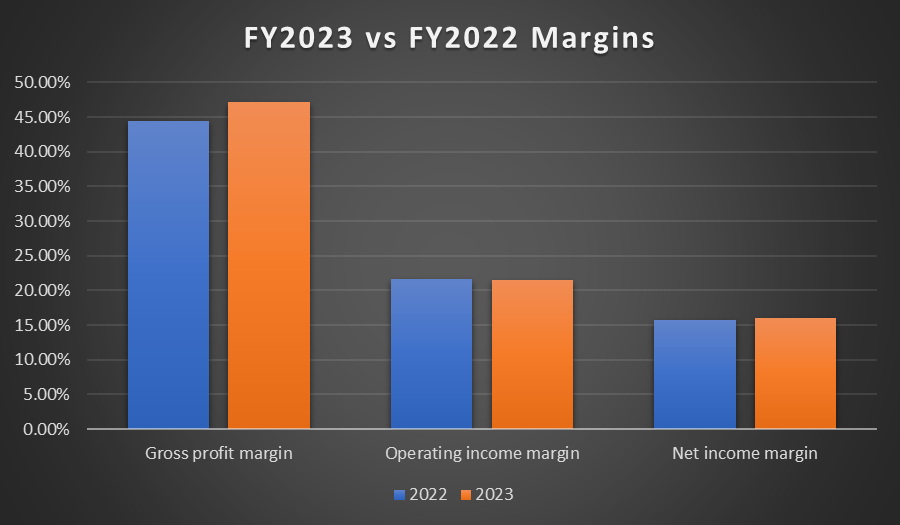

Regardless of fluctuating income development charges, SSD’s margins have expanded barely over time. In 2023, it reported a gross revenue margin of 47.1% vs. 2020s 45.5%, an working earnings margin of 21.46% vs. 2020s 19.88%, and a web earnings margin of 15.9% vs. 2020s 14.75%.

When trying on the chart, 2021 was the 12 months that SSD’s margin expanded. From then on, it remained comparatively flat year-over-year. The margin enlargement seen in 2021 was pushed by product value will increase and decrease labor and manufacturing facility bills.

Writer’s Chart

FY2023 Earnings Evaluation

For FY2023, SSD’s web gross sales grew low-single digit of 4.6% year-over-year to $2.2 billion, up from 2022’s $2.1 billion. The expansion was primarily pushed by its acquisition of ETANCO, a $12.7 million profit from overseas foreign money translation as Europe’s currencies strengthened in opposition to USD, and share positive aspects in SSD’s finish markets and product traces.

When it comes to profitability margins, I can be analyzing its gross revenue margin [GPM], working earnings margin [OIM], and web earnings margin [NIM]. In FY2023, SSD’s GPM expanded from 44.5% to 47.1%, and the enlargement was pushed by the acquisition of ETANCO and likewise by decrease uncooked materials prices. Regardless of the expansion in GPM, its OIM and NIM had been nearly flat year-over-year.

FY2023’s OIM and NIM reported had been 21.46% and 15.9%, respectively, in comparison with 2022’s 21.69% OIM and 15.78% NIM. The explanation behind that is because of the additional bills incurred which might be associated to SSD’s development enlargement plans. Nevertheless, administration is assured that these further bills are effectively value it, as they anticipate SSD’s future gross sales quantity CAGR to be above market. Lastly, FY2023 reported EPS was $8.26 vs. FY2022’s $7.76, which represents a year-over-year development of ~6.4%.

Writer’s Chart

Key Addressable Market Nonetheless Has Room for Progress

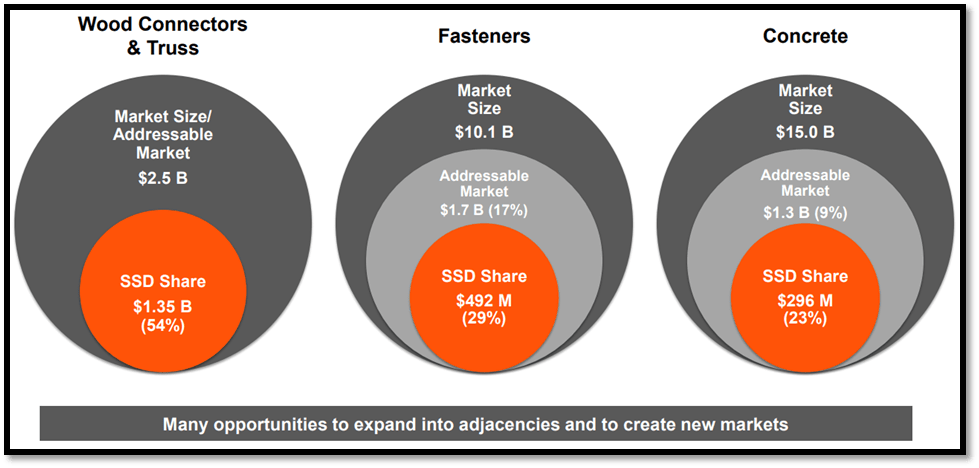

Primarily based on SSD, its web gross sales’ product teams will be segregated into wooden development, concrete development, and others. Out of those, wooden development types the biggest share of ~85% of whole web gross sales. Concrete development is available in second at 14.5%, with different segments forming the rest.

Beneath wooden development, the principle merchandise are connectors, fasteners, and lateral resistive techniques. For concrete development, the merchandise embrace anchor merchandise and development, restore, safety, and strengthening merchandise. Primarily based on the next diagram, it’s clear that SSD’s key markets are massive and nonetheless have sufficient room to permit SSD to proceed rising. For wooden connectors and trusses, SSD presently solely instructions ~54% of the market share, at ~$1.35 billion. The addressable wooden connectors and truss market dimension is estimated to be ~$2.5 billion.

For the fasteners market, SSD solely instructions round 29% of the $1.7 billion addressable market. Nevertheless, the entire market dimension for fasteners is ~$10.1 billion, which signifies that SSD’s addressable fasteners market nonetheless has the capability to develop because it presently sits at 17%. Lastly, for concrete, SSD’s market share is ~23% of the $1.3 billion addressable market. Just like the fasteners market, SSD’s addressable marketplace for concrete is barely 9% of the entire market dimension of $15 billion. Subsequently, there’s nonetheless loads of room for SSD’s concrete addressable market to develop and develop.

SSD’s Investor Relations

Effectively Positioned to Increase into the $1.7 Billion Fasteners Market

For the $1.7 billion fastener addressable market, SSD is aiming to be the worldwide market chief, given the substantial development potential this market brings to the desk for them. As well as, increasing on this section may even profit its connector and lateral merchandise, as they’re complementary to one another, thus offering a number of benefits.

SSD’s established channels and buyer bases within the constructing and development markets present a robust basis that may assist drive its development within the fastener market. Furthermore, its established manufacturing and provide chain processes place them effectively and assist their enlargement aim. Subsequently, trying forward, SSD’s drive to develop market share on this massive market, which has substantial development potential, is anticipated to bolster its development outlook.

US Annual Housing Begins And Europe Building Exercise Creating Headwind

Though consolidated web gross sales grew and margins remained comparatively strong, you will need to spotlight that the annual US housing begins declined by 9%. Regardless of that, SSD’s FY2023 North America web gross sales and quantity nonetheless managed to squeeze a modest development of 1%. Nevertheless, we can not deny the truth that it’s creating headwinds for SSD. In Europe, it would not fare effectively both, as administration said that the area can also be dealing with difficult financial challenges in addition to decrease development exercise.

On these notes, for 2024, administration expects the difficult market situation to persist into 1H24 however regularly subside when transiting into 2H24. Trying on the market estimate for SSD’s 2024 income, it’s ~$2.32 billion. When in comparison with 2022, this represents a year-over-year development of ~5.45%. Though that is an enchancment to 2022’s development, it’s nonetheless decrease than its 10-year median.

Relative Valuation Mannequin

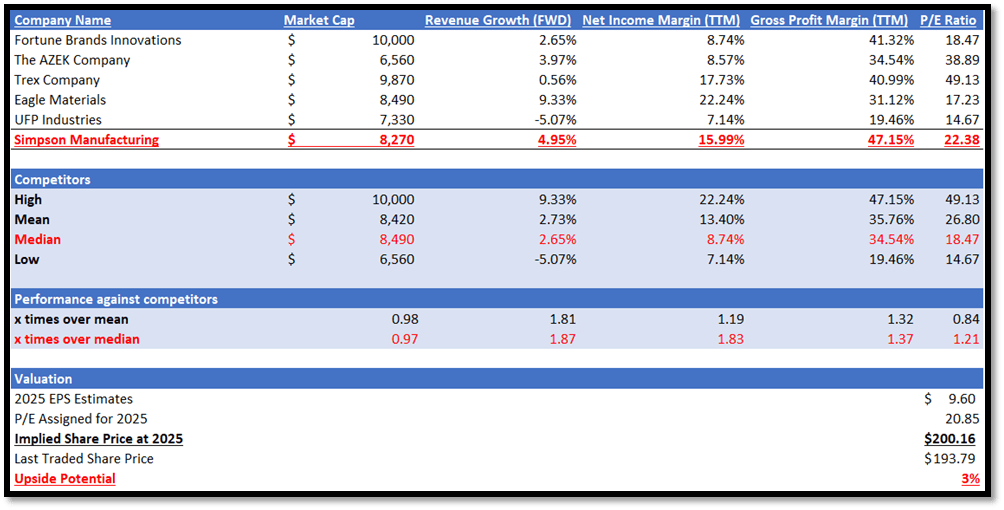

When it comes to firm dimension, SSD is equally sized in comparison with its friends. It has a market capitalization of $8.2 billion, in comparison with its friends’ median of $8.4 billion. Regardless of being equally sized, it outperformed its friends when it comes to development outlook and profitability. SSD has a ahead income development charge of 4.95% in comparison with friends’ median of two.65%. When it comes to profitability, SSD additionally has the next gross revenue margin TTM of 47.15% vs. friends’ median of 34.54%. SSD’s web earnings margin TTM of 15.99% can also be greater than friends’ median of 8.74%.

Because of its higher metrics, SSD’s P/E ratio of twenty-two.38 x is buying and selling greater than friends’ median of 18.47x, which is justified. Nevertheless, it’s buying and selling above its 5-year common of 20.85x. Provided that its 2023 income development charge and ahead development charge are decrease than its 10-year median of 9.41%, it isn’t justified to be buying and selling above its 5-year common P/E.

The market estimate for SSD’s 2024 income is $2.32 billion, whereas 2025 is $2.45 billion. For EPS, the 2023 estimate is $8.66 and for 2024 it’s $9.60. Given the expansion catalysts and headwinds relating to the housing market that had been mentioned above, the estimate is affordable and justified. By making use of a P/E of 20.85x to its 2025 EPS estimate, my goal value is $200.16, which represents a modest upside of solely 3%.

Writer’s Valuation Mannequin

Danger

The upside threat to my maintain advice is in relation to the expansion potential of SSD in its addressable markets. If the US and Europe’s macroeconomic and housing challenges had been to subside, it could present the tailwind for SSD to develop. As well as, SSD is effectively positioned to seize development within the bigger fastener market given its established channels and buyer bases, together with its strong manufacturing and provide chain processes.

Conclusion

In conclusion, SSD’s 2023 income development charge has slowed down drastically when in comparison with 2020-2022. The deceleration was attributable to decrease US housing begins and Europe’s difficult financial headwinds. On a brighter word, its margins really remained strong over the identical interval regardless of the income volatility.

Trying forward, SSD’s outlook is blended. Though its three core markets nonetheless have ample room to develop, and it’s also effectively positioned to develop into the massive fastener market, administration is anticipating the difficult market situations SSD confronted in 2023 to roll over into 1H24. Nevertheless, it’s anticipated to subside within the latter half.

Relating to valuation, though SSD outperformed its friends, its P/E is buying and selling somewhat too excessive. To be able to keep conservative, I’ve adjusted its P/E downward to its 5-year common. At this a number of, my goal value signifies modest upside potential. Given the blended outlook, the upside potential would not present sufficient margin of security. Subsequently, I’m recommending a maintain ranking.