McKevin

Sixth Street Specialty Lending (NYSE:TSLX) has been implementing one of the most impressive portfolio strategies in the BDC industry, enabling it to generate solid risk-adjusted returns over the years. Its ability to earn one of the best portfolio yields while keeping non-accruals below the industry average is one of the promising outcomes of its business plan. With a healthy liquidity position and extensive penetration in the middle-market, Sixth Street also appears well-positioned to benefit from increasing investment opportunities in the private credit market.

BDC Market Trends are Improving

The business development industry turned into a dependable asset class for a range of buy-and-hold investors. The industry has demonstrated resilience in the face of extreme economic and credit market volatility in the past two years while generating robust cash returns for shareholders in the form of regular, special, and supplementary dividends. Their realized credit losses were significantly below the traditional lenders, averaging around 1% at fair value in 2023. Non-accruals were also significantly low, with top performing BDCs such as Sixth Street kept them around 1%.

As the Fed seeks to hold rates at a peak level for a longer time to achieve inflation and job market related targets, the improvement in deal activity in the past two quarters indicate that middle-market companies and private equity sponsors begin adjusting to the higher-for-longer interest rate environment. This is reflected in increased deal activity across the BDC industry and private credit market. For instance, Goldman Sachs BDC (GSBD) originated $359.6 million in new investment commitments compared to $166 million in the previous quarter while Blackstone’s (BXSL) $1.2 billion in new investments and more than $700 million in funding marked the most active quarter in the last three years. Carlyle Secured Lending (CGBD) reported a massive 30% increase in origination in the first quarter, thanks to improving leveraged buyout activity.

Overall, BDCs are poised to capitalize on opportunities in the emerging credit market because they offer creative financing solutions, structural flexibility, and pricing certainty. Higher portfolio yields, significant cash returns, effective portfolio management and strict underwriting policies have also been contributing to BDCs performance.

A Solid Business Plan Helped Sixth Street Gain Positive Outlook

Fitch ratings agency recently increased Sixth Street’s rating from stable to positive, attributing the rating upgrade to its credit performance, strict underwriting policies, consistent operating performance and debt to equity in the range of 0.9x-1.25x. I believe that rating upgrade is an outcome of its portfolio and business management strategies. For instance, Sixth Street’s strategy of avoiding diversification into cyclical industries, focusing more on specific sector themes, and investing only at the top of capital structure has helped it in producing solid risk-adjusted returns while lowering non-accruals and maintaining a solid liquidity position.

As Sixth Street makes a debt investment with a plan of holding it until maturity, the firm uses a bottoms-up approach, due diligence, and active portfolio management to protect the investment. The company is also benefiting from its relationship with Sixth Street Partners, a global investment firm with over $77 billion in assets under management. Sixth Street Partners has helped it participate in several cross-platform deals, including a leading role in debt financing in the acquisition of Alteryx by Clearlake Capital and Insight Partners. Moreover, the company’s strategy of gaining a voting right helps it protect its positions. As of the end of March quarter, it has effective voting control on 78% of its debt investments.

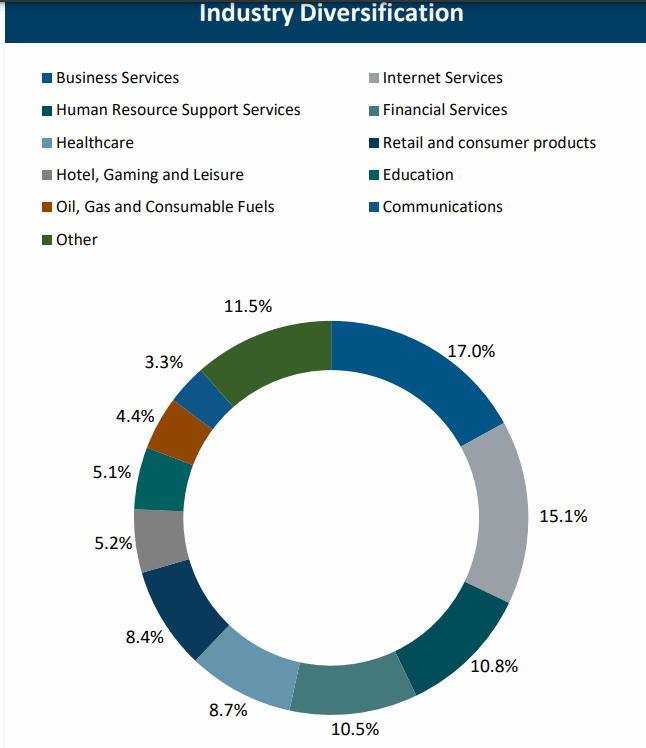

Portfolio Diversification (Q1 Presentation)

Sixth Street mainly invests in private companies in the core middle market with an EBITDA between $10 million to $250 million. Although the company avoided its portfolio exposure to cyclical industries, it has diversified investments across non-cyclical industries. Its portfolio is composed of 100 debt investments with an average investment size of $33.5 million.

Sixth Street continues to chase attractive investment opportunities due to its solid liquidity position. In the latest quarter, its total commitments were $264 million and total fundings were $163 million across the 9 new portfolio companies in eight different industries. On the positive side, despite investing in non-cyclical industries, Sixth Street’s weighted average yield on debt was 14.0% in the latest quarter, which is one of the best yields in the industry. Its peers, Goldman Sachs BDC and Blackstone Secured Lending Fund, ended the latest quarter with a weighted average yield on investment portfolio of less than 12%. Moreover, Sixth Street’s return on equity metrics are among the best in its industry, thanks to its high portfolio yield. In the first quarter, it generated return on equity of 13.6%, in line with the target return range of 13.4% to 14.2% and up significantly from cost of capital of 9%.

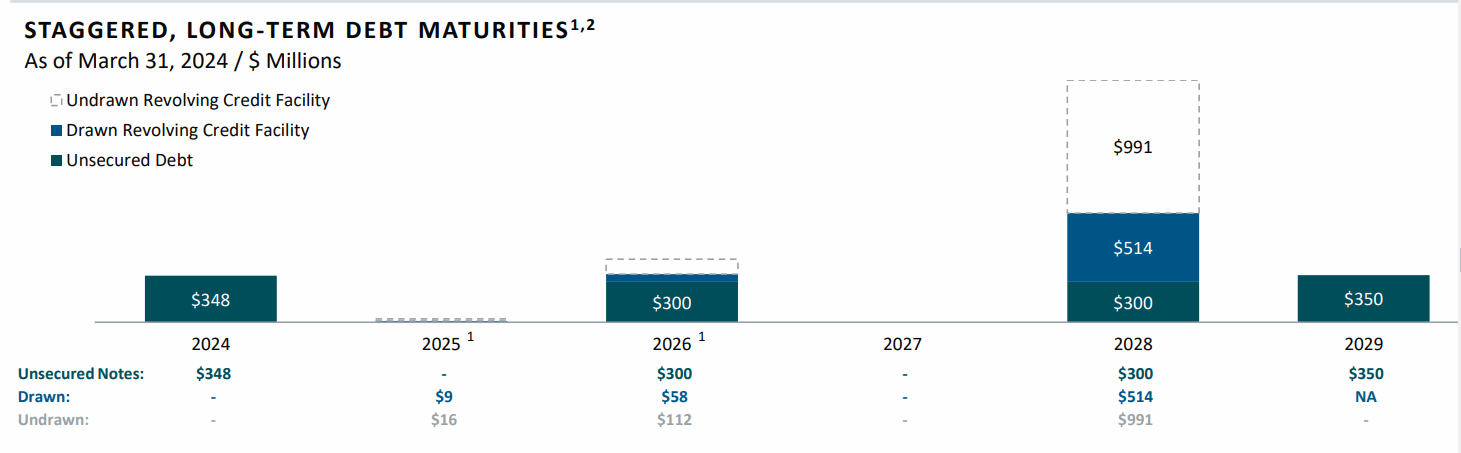

Debt Maturities (Q1 Earnings Presentation)

Besides portfolio management and underwriting strategies, Sixth Street continues to implement an impressive business plan of maintaining a liability maturity duration greater than the debt funded assets life. For instance, as of the end of the latest quarter, 78% of its debt maturities were greater than 3 years. Moreover, the extension of its revolving credit facility maturity to 2029 has enhanced its liquidity position. Furthermore, a small equity raise in early 2024 and a $350 million long 5-year bond offering has also added to its investment potential. The company also appears in a comfortable position to repay $347.5 million in late 2024 given $1.1 billion in unfunded revolver capacity. As of the end of first quarter, its debt to equity ratio was 1.14x, compared to the targeted range of 1.25x.

Dividends Are Safe As Earnings Significantly Exceed Payout

Although the spreads are declining and competition is increasing, the company continues to generate healthy net investment income, thanks to low non-accruals, higher portfolio yield and a steady growth in total portfolio value. In the latest quarter, its adjusted net investment income per share came in at $0.59, down slightly from the previous quarter’s $0.62 per share and up from $0.53 per share in the year-ago period. Its net investment income of $0.59 per share significantly exceeded its quarterly distribution of $0.46 per share. Consequently, it also announced a special dividend of $0.06 per share. The company is currently carrying a spillover income of $1.06 per share.

Apparently, there is no risk to its dividend stability. In fact, the company’s strategy of investing in growth opportunities across numerous non-cyclical industries and actively managing those investments is likely to enable it to sustain its robust net investment income. Improving market fundamentals also adds to its growth potential. Furthermore, the higher for longer forward interest rate curve continues to support Sixth Street’s net investment income because 99% of its debt investments are floating in nature.

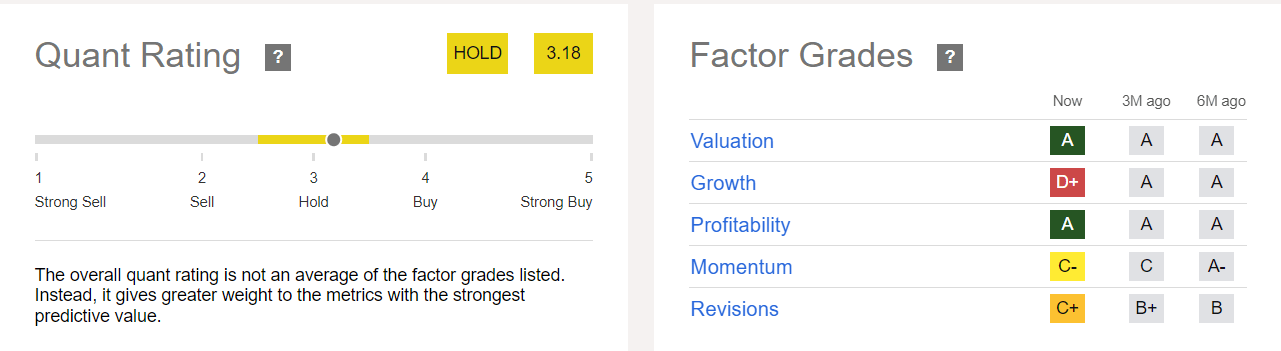

Quant Rating and Valuation

Quant Rating (Seeking Alpha)

Sixth Street Specialty Lending received a hold rating based on the SA quant system. Hold rating is mainly blamed on a poor score on the growth factor. In the latest quarter, its investment income and net investment income declined slightly from the previous period due to the impact of increased competition on spreads and portfolio yield. I expect an improvement in the growth factor given higher for longer interest rate outlook along with a steady growth in the total portfolio value. Besides that, the stock also earned a low score on momentum because its shares underperformed so far in 2024 due to investors’ concerns over the impact of rate cuts on its revenue and profitability. However, the stock began rebounding since Fed communicated the prospects of the higher for longer policy. Therefore, the momentum score is also likely to improve.

On the positive side, the company’s valuations are in line with industry average and below the sector median. The company has also been growing its net asset value year over year. Since late 2022, its net asset value grew by more than 5.5%. Its net asset value is currently around $17.11 per share, up from $17.04 per share in the previous quarter. Although its shares are trading above its net asset value, I believe paying a premium for quality dividend and future growth might not be a bad move. The company has also recently issued equity at a premium compared to its net asset value. This reflects that investors are comfortable in paying premium for quality business, higher risk adjusted cash returns and future growth prospects.

Risk Factors to Consider

Although the Fed’s strategy of holding rates at peak level supports floating nature portfolios, the strategy could also pave the way for credit deterioration. In the earnings call, the CEO of Sixth Street Specialty Lending anticipated that the tail is growing on the margin. This means that higher rates are supporting margins, but it has also been negatively impacting borrower’s ability to return the debt. The company has added one new debt investment on non-accrual status in the latest quarter due to tight conditions. If the Fed keeps rates higher for longer, there is a risk of more credit losses.

In Conclusion

BDCs turned out to be one of the safest asset classes in the past years because of their attractive business models and significant demand for direct lending. Fiscal 2024 could also be one of the best years for BDCs in terms of earnings and cash returns because their floating rate portfolios are likely to benefit from higher for longer interest rate policies. Sixth Street is one of the strong BDCs because of its impressive business and portfolio management strategies. Its healthy liquidity positions and lower non-accruals would enable it to capitalize on recovery in deal activity. Therefore, Sixth Street Specialty Lending appears like a solid option for income seeking investors with a long-term investment horizon.