onurdongel

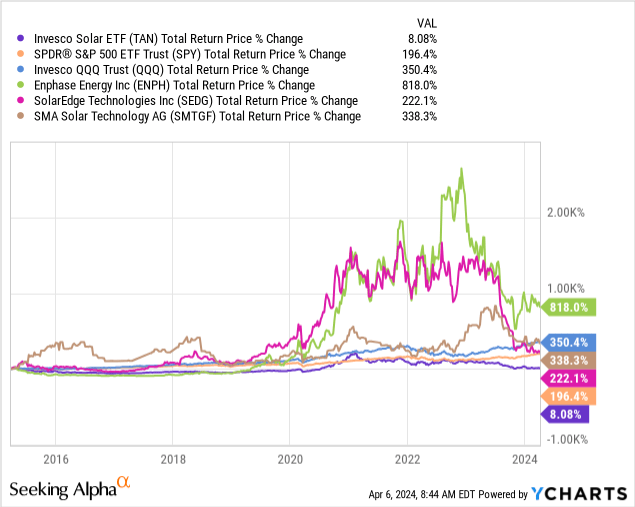

Regardless of delivering huge progress as an trade, the photo voltaic sector has not been significantly variety to buyers. For instance, Invesco’s (IVZ) Photo voltaic ETF (TAN) has massively underperformed the S&P 500 index (SPY) and the very talked-about Invesco expertise belief ETF (QQQ). Nonetheless, buyers which have solely centered on firms specializing in photo voltaic inverters have skilled glorious returns. Corporations like Enphase Power (ENPH) and SolarEdge Applied sciences (SEDG) have been among the finest performing firms the previous few years. This is the reason we consider buyers that need publicity to the expansion within the photo voltaic sector ought to in all probability concentrate on this a part of the trade, and keep away from the largely commoditized photo voltaic panel producers.

We previously in contrast SMA Photo voltaic Expertise (OTCPK:SMTGF) to Enphase Power, and we at the moment are updating our protection after the corporate reported fiscal yr 2023 earnings outcomes and supplied steerage for 2024.

There may be numerous debate on which inverters are one of the best, and after spending a lot time doing analysis on the topic, the reply appears to be “it depends”. Basically, it seems SMA Photo voltaic inverters are fairly dependable and normally less expensive in comparison with opponents specializing in micro-inverters. Nonetheless, micro-inverters have benefits when there’s partial shading or among the panels malfunction, they usually allow higher monitoring. Nonetheless, there’s clearly demand for SMA Photo voltaic inverters, as the corporate continues to extend its gross sales. They look like significantly properly suited to giant scale installations, as that is their largest section, and the one that’s rising the quickest.

FY2023 Outcomes

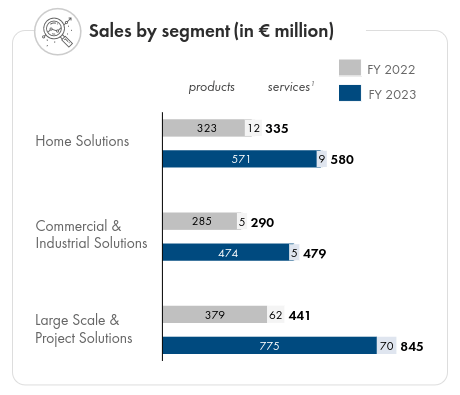

The corporate delivered very sturdy monetary outcomes for fiscal yr 2023, with group gross sales rising 79% to €1,904 million, and the EBITDA margin widening to 16%. The corporate delivered stable working efficiency in all its segments, with the Massive Scale & Mission Options section rising a formidable 91.8% to €845.0 million.

SMA Photo voltaic Investor Presentation

Web revenue roughly quadrupled to €225.7 million, whereas inverters bought in 2023 reached 20.5 GW, a lot increased than the 12.2 GW bought in 2022. SMA Photo voltaic additionally ended the yr with a big internet money place of €283.3 million, giving the corporate assets to spend money on future progress.

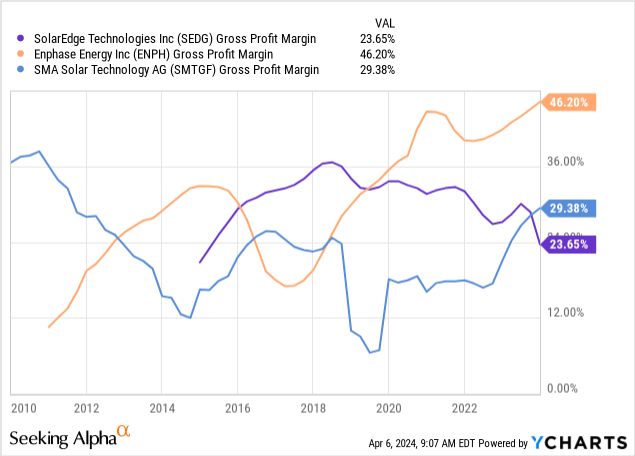

The gross margin was up considerably yr over yr to 29.4%, pushed particularly by elevated profitability within the Dwelling Options section. Nonetheless, Enphase Power nonetheless has a lot better gross revenue margins.

Order Backlog

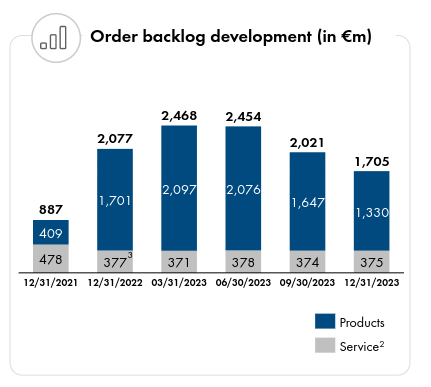

The backlog has come down, however stays at a wholesome degree. The corporate reported ending the yr with a complete backlog of €1,705.0 million.

Notably, the backlog for the Massive Scale & Mission Options section rose to €914 million, giving sturdy indications that that is an space the place the corporate has a powerful providing and is competing very efficiently.

SMA Photo voltaic Investor Presentation

Development

Whereas the corporate didn’t take part to the identical extent as Enphase Power and Photo voltaic Edge Applied sciences within the sturdy progress in rooftop photo voltaic, it’s now benefiting from very vital progress in giant scale initiatives.

Consequently, its income progress is anticipated to outperform by a big margin in 2024. The corporate is making ready for future progress by investing within the SMA Gigawatt manufacturing facility in Germany, it’s increasing its manufacturing capability in Poland, and it’s contemplating a brand new manufacturing web site within the U.S.

In search of Alpha

Future Outlook

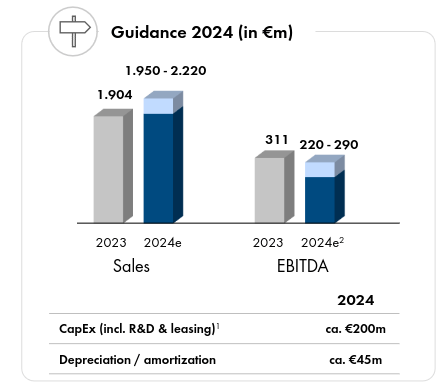

Steering for fiscal yr 2024 is for gross sales to be between €1,950 million and €2,220 million, and EBITDA of between €220 million and €290 million. Gross sales progress in 2024 is generally anticipated to be pushed by the Massive Scale & Mission Options section. SMA’s Dwelling and Industrial & Industrial segments are anticipated to face headwinds within the first half of 2024 because of excessive stock ranges with their prospects. Regardless of increased anticipated gross sales, and a one-time €19 optimistic impression from the sale of shares in elexon GmbH, the corporate expects a slight lower in EBITDA for FY24.

Longer-term, the outlook could be very optimistic for the corporate, with some analysts forecasting huge progress in utility scale photo voltaic. For instance, Morningstar is predicting that renewable vitality will triple by 2032, with photo voltaic projected to be the fastest-growing expertise. Specifically, they count on utility-scale photo voltaic initiatives to develop a number of fold.

SMA Photo voltaic Investor Presentation

Valuation

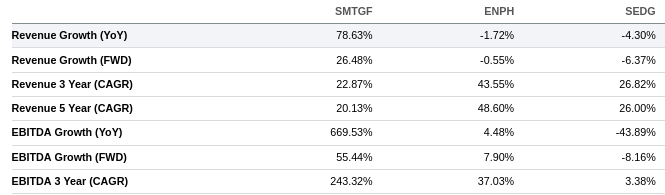

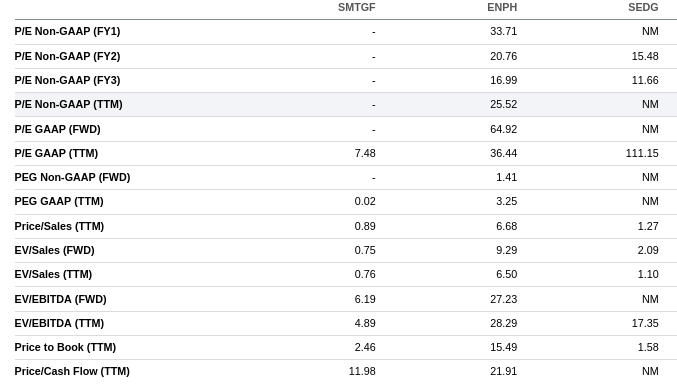

Regardless of the optimistic medium-term and long-term outlooks, the corporate is buying and selling with very low valuation multiples. We attribute this partially to the truth that the corporate relies in Europe, the place valuations are presently decrease generally. The corporate is anticipated to ship increased income progress this yr in comparison with Enphase Power and SolarEdge Applied sciences, however trades at a fraction of their valuation multiples.

For instance, SMA Photo voltaic’s trailing twelve months EV/EBITDA a number of is lower than 5x, whereas Enphase’s is round 28x, and SolarEdge’s near 17x. Because of this we see SMA Photo voltaic as considerably undervalued, and one of the engaging choices within the photo voltaic vitality sector.

In search of Alpha

Dangers

We see just a few dangers price contemplating, together with uncertainty relating to future authorities and company assist for renewable vitality applied sciences. There may be danger that competitors may intensify, with opponents probably growing higher expertise or discovering methods to fabricate comparable merchandise at a decrease price.

To this point inverter firms have been capable of ship a lot better revenue margins than photo voltaic panel producers, however there isn’t any assure this can proceed. Nonetheless, dangers are mitigated by sturdy mental property and know-how inverter producers have, and powerful manufacturers and industrial relationships.

Conclusion

SMA Photo voltaic delivered spectacular outcomes for its 2023 fiscal yr, with sturdy income and earnings progress. The corporate trades at a a lot decrease valuation in comparison with friends, and we consider it’s an attention-grabbing possibility to contemplate to get publicity to the large anticipated progress in photo voltaic installations within the coming years. The corporate is displaying explicit energy within the giant scale initiatives section. We view shares as considerably undervalued contemplating the very optimistic outlook and the engaging valuation multiples, particularly when in comparison with its friends.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. trade. Please pay attention to the dangers related to these shares.