ArtistGNDphotography/E+ via Getty Images

Intro

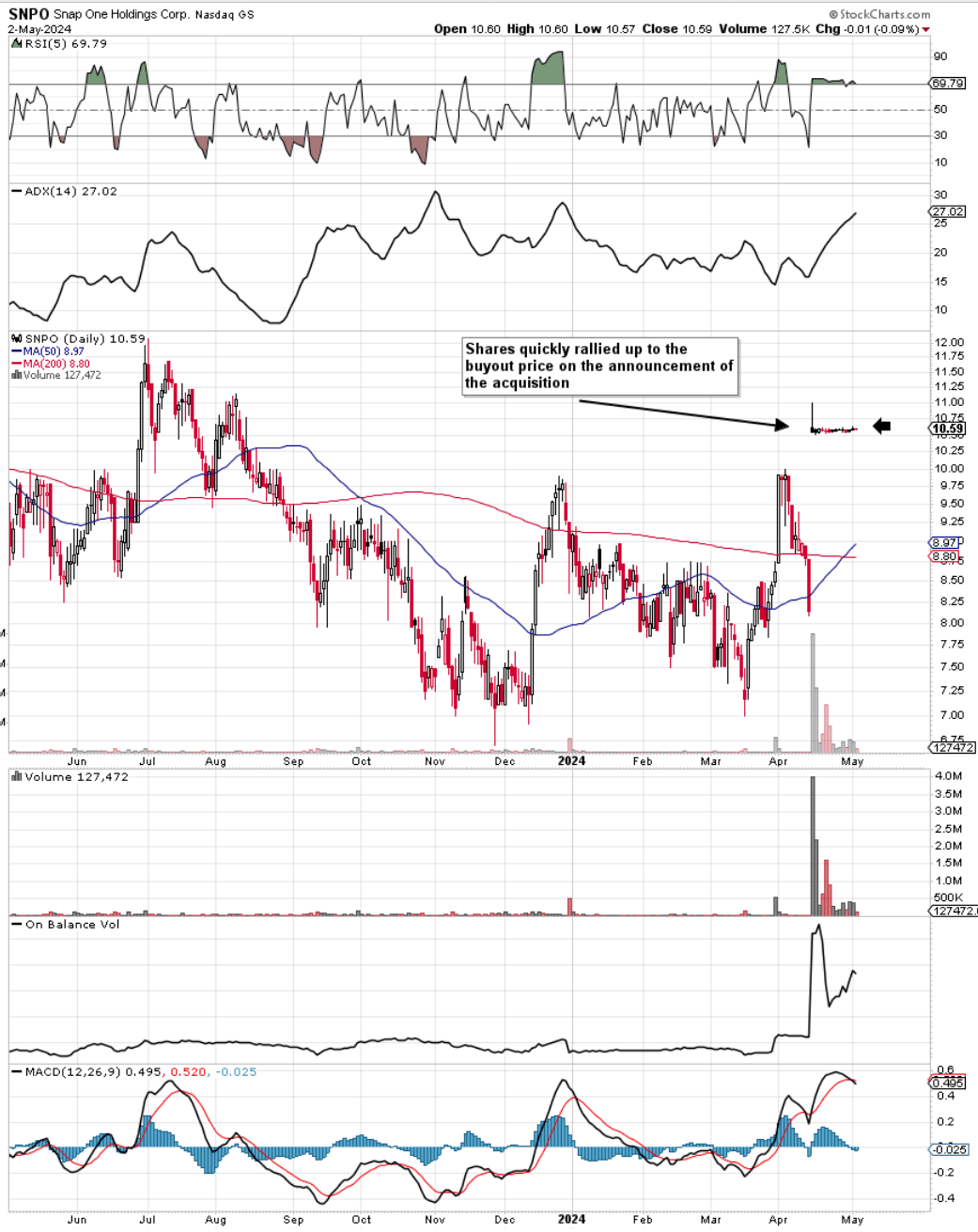

If we pull up a technical chart of Snap One Holdings Corp. (NASDAQ:SNPO) (US-based commercial & residential smart-living solutions outfit), we see that shares quickly (on the announcement of the pending acquisition by Resideo) moved up toward the buyout price of $10.75 a share. Astute shareholders would have sold their SNPO shares promptly on the news on the expectation of limited upside in Snap One Holdings until the acquisition finally goes through (expected in the second half of calendar 2023). Suffice it to say, the only risk now to current Snap One investors (who did not sell on the acquisition announcement) is that the acquisition is held up for some antitrust or regulatory issue over the upcoming months. In the absence of any forward-looking roadblocks, we expect shares to continue to trade for at least the buyout price just below $11 a share.

Therefore, as the present fundamentals stand, we believe SNPO remains a strong ‘Hold’ at this juncture. Bullish trends were already in motion in Snap One before the acquisition which we go through below.

SNPO Technical Chart (Stockcharts.com)

Forward-Looking Earnings Revisions Remain Bullish

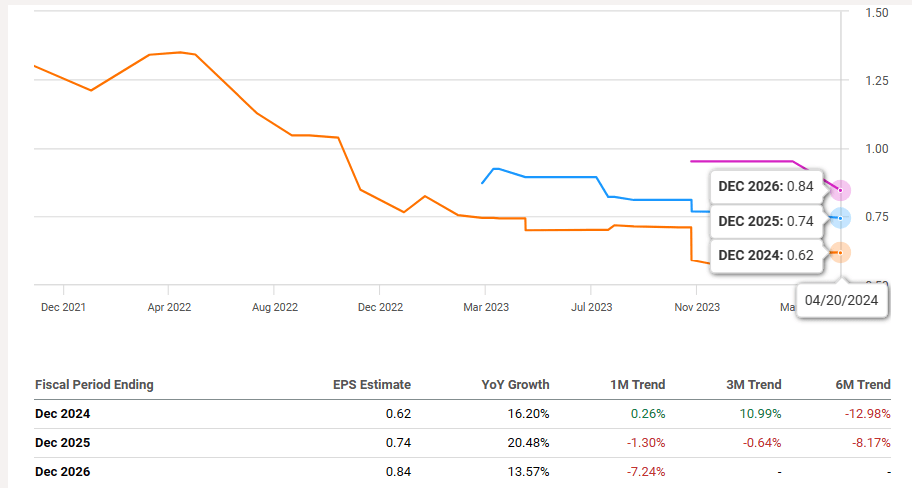

As we can see from the graphic below, the consensus EPS target for fiscal 2024 in Snap has increased by more than 10% over the past three months alone. This means (at present), expected bottom-line growth for fiscal 2024 now surpasses 16% due to five upward revisions over the past three months alone. Bullish forward EPS revisions positively impact the valuation in that recent trends now mean Snap trades with a forward earnings multiple of 17.18 & a fiscal 2025 multiple of 14.26.

Suffice it to say, It was evident as we see below that Snap was undervalued from both a sales & assets standpoint. Still, recent bullish earnings revisions have now brought the valuation of the company’s earnings back down into undervalued territory. Growth is driven by the expectation that the company’s share of wallet with integrators on average should automatically increase going forward as we discuss below. Furthermore, the likes of Snap One’s Control4 Connect technology will also drive demand from the end customer going forward.

Snap One Consensus Earnings Revisions (Seeking Alpha)

| Sector Median | Snap One | |

| P/E Non-GAAP (FWD) (2024) | 14.96 | 17.18 |

| P/E Non-GAAP (FWD) (2025) | – | 14.26 |

| Price / Sales (FWD) | 0.86 | 0.74 |

| Price / Book (FWD) | 2.13 | 1.03 |

Value Continues To Be Added

Snap One works with more than 20,000 professional integrators to install its products & services so the ‘stickiness’ of these relationships remains paramount from a forward-looking basis. At Snap One’s core, connectivity, product integration & ecosystem adoption are fundamental where technology both for residential & commercial purposes continues to change at breakneck speeds. This means as long as Snap One can remain competitive with its offerings in this rapidly evolving technology environment, you feel that there will continue to be an outlet for its products, and even more so if housing starts can begin to accelerate.

To this point, to stay ahead of the competition, Snap One continues to stay at the forefront concerning ongoing product launches (which were sizable in fiscal 2023) in their respective niches. Furthermore, notwithstanding technological improvements, Snap One continues to improve its omnichannel presence through local branch increases & the unifying of portals (Control 4 & Snap One). The above initiatives as mentioned should help in improving the stickiness of the relationships between integrators & Snap One over time, consequently leading to dividends over time.

Margins Continue To Rise As Momentum Builds

To gauge operating performance from a non-GAAP standpoint, management uses the ‘contribution margin’ metric which rose 4.3% (Hitting 41.7%) in the company’s most recent reported fourth quarter. This means the fourth quarter increase outpaced the full-year average (Contribution margin rose by 1.4% in fiscal 2023) demonstrating momentum on two fronts in the company.

The biggest reason for the company’s margin expansion is down to how the supply-chain has improved in recent times. Post-COVID, management has been able to consistently bring down costs in this area which is positively impacting margins. Furthermore, upward price adjustments also benefited the company’s margins in fiscal 2023.

Given how SG&A costs made up close to 34% in fiscal 2023, it is imperative that management can keep scaling the business (By turning over product at an above-average clip) to protect the income statement going forward. A strong economy of scale can be achieved by continuing to invest in value-adding products and ensuring the absolute maximum synergies are being realized from acquisitions & mergers to date.

On the partner side, management is confident that inventory levels have now dropped to levels that should spur aggressive buying going forward. This, as mentioned is important as the numbers (product) must be run through the income statement at speed due to the elevated SG&A costs mentioned earlier.

Conclusion

To sum up, present shareholders received a nice boost in their unrealized gains from the buy-out offer from Resideo in April of this year. Shares spiked up toward the buyout price of $10.75 a share on the news and have maintained this level since then. Change was afoot however before the buyout as announced synergies were beginning to come off past acquisitions resulting in margin gains for the company. Supply chain-related headwinds have also eased off resulting in management being able to eke more costs out of the system.

Once the acquisition gains final approval, long holders of Snap One at the time will receive $10.75 a share in cash for their shares. It must be acknowledged that a further bidder is always possible (which could push the price up) in the interim period. Still, given how close shares are currently trading ($10.60) from the buy-out price, the potential reward doesn’t seem justified. Therefore, bullish investors on Snap One should now be looking to the purchaser (Resideo Technologies) to see if this company is in a position to scale the combined ‘entity’ earnings in earnest.

Let’s see how Snap One’s Q2 earnings for fiscal 2023 (due to be released shortly) fare out. We look forward to continued coverage.