Eoneren

Introduction and funding thesis

Final time I’ve covered Snowflake (NYSE:SNOW) following its FY24 Q3 earnings release, the place I rated the corporate’s shares as a Sturdy Purchase. Essential new product launches, a few of that are already contributing to revenues mixed with stabilizing consumption traits and a decreased valuation premium have been my primary arguments in favor of shopping for shares.

Though the share value response following the FY24 Q4 earnings release proved my earlier Sturdy Purchase advice untimely, I’m nonetheless bullish on the corporate’s prospects with much more conviction than earlier than.

First, my earlier fears of RPO deceleration and stagnation in bigger new account progress have been defied by the This autumn earnings print. Second, the FY25 steerage, which disillusioned buyers appears unusually conservative to me, organising Snowflake for beat-and-raise quarters. Third, the CEO transition is a optimistic in my eyes getting ready the corporate for the AI-era.

I imagine that the melt-up within the share value over the previous month has been overdone, and there’s a good alternative now to provoke a protracted place or add to present ones. It’s true that vital product launches may very well be typically out there for patrons for the second half of the 12 months which means that income might reaccelerate extra visibly in H2. Nonetheless, I imagine that the share value will get better most of its post-earnings losses by that point.

Comforting This autumn earnings with ultraconservative FY25 steerage

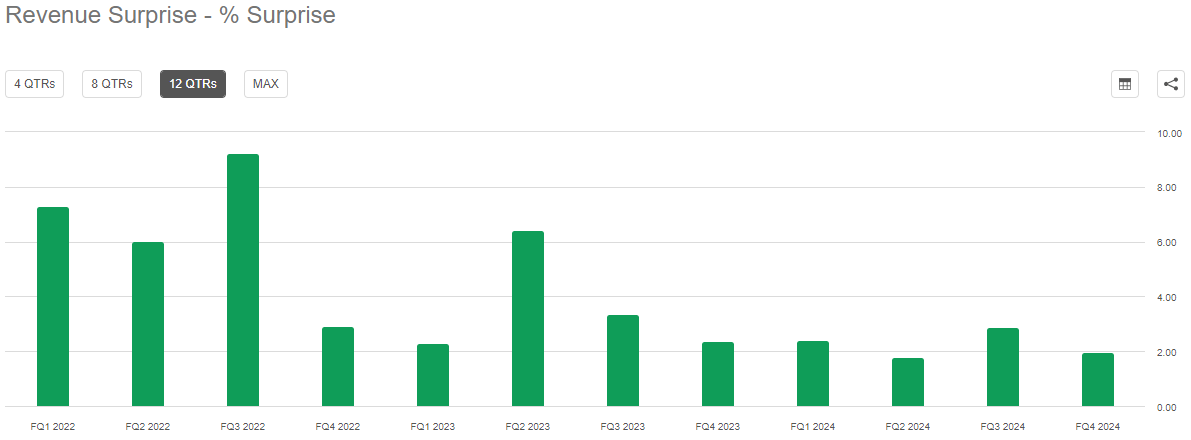

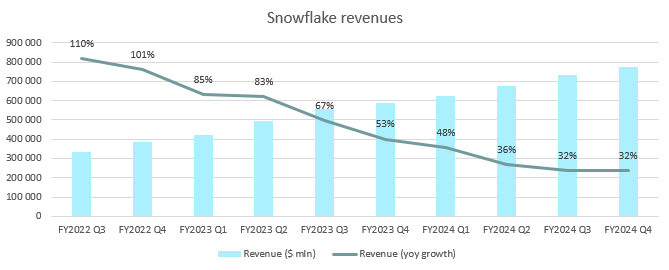

Snowflake reported revenues of $774.6 million for its just lately closed FY24 This autumn quarter beating the common analyst estimate of $760.4 million. The magnitude of the beat has been according to earlier quarters, regardless of administration feedback on the Q4 earnings call that consumption picked up slower popping out of the vacations:

Searching for Alpha

After the standard December-January slowdown consumption picked up once more to pre-holiday ranges, however nonetheless beneath the place it has been earlier than FY24 when value optimizations didn’t play such an vital function within the software program area. Revenues have grown 32% yoy within the quarter similar to 1 / 4 earlier than, which has been an encouraging signal after a number of quarters of topline progress deceleration:

Created by creator based mostly on firm fundamentals

Bettering income progress has been pushed by stabilizing consumption traits, which has been extra pronounced within the again half of FY24. In Q3, 9 out of prime 10, in This autumn, 8 out of prime 10 prospects have grown their consumption by Snowflake sequentially, displaying growing confidence to spend extra. A latest vital change on this entrance has been the restructuring of gross sales reps’ incentives, which is now extra weighted in the direction of producing consumption from prospects relatively than bookings. 55% of reps are compensated now for driving consumption at present prospects, whereas 35% are targeted on new consumer acquisition, with the remaining 10% working hybrid. I imagine directing the gross sales power with incentives into this route ought to have a significant impact on growing progress in consumption.

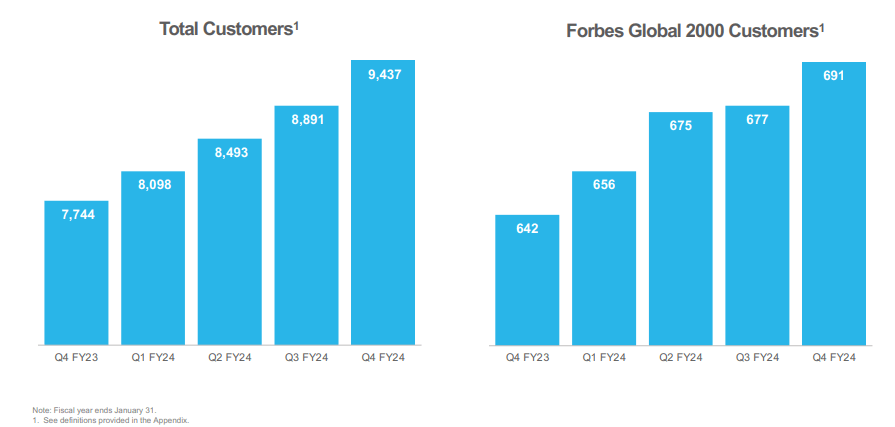

One might worry that bookings and new buyer acquisition might fall again as a consequence of considerably reducing focus, however latest outcomes present that’s not case for now. Primarily based on the corporate’s earnings presentation whole variety of prospects grew by 546 in This autumn, the very best determine in latest quarters:

Snowflake FY24Q4 earnings presentation

In the meantime, the variety of Forbes 2000 prospects elevated by 14 sequentially defying considerations from the earlier quarter that giant buyer acquisition is stagnating.

One other vital element of gross sales progress turnaround is Snowflake’s personal developer framework known as Snowpark, which allows builders writing code straight in Snowflake with out the necessity of transferring knowledge in to and out of the platform. Snowpark captures increasingly more workloads from Apache Spark, which has been the go-to software for giant knowledge workflows earlier than the announcement of Snowpark. For knowledge residing in Snowflake utilizing Snowpark ends in important value efficiencies, higher safety, sooner time-to-market and simpler arrange, which offer a wonderful incentive for patrons to shift workloads from Apache Spark.

Though Snowpark is normally availability for greater than two years, it managed to achieve important traction solely just lately. In line with administration it took time for the Snowflake gross sales group itself to get acquainted to the brand new know-how and to find with prospects how it may be utilized most effectively. Now plainly the teachings have been realized as Snowpark revenues grew nearly 50% qoq within the previous Q3 quarter. Primarily based on analysts feedback the annualized income price from Snowpark has been round $70 million in December, so it might meaningfully contribute to revenues subsequent 12 months. Formally, administration guider for 3% contribution equaling round $100 million for FY25, however within the mild of latest momentum this appears overly conservative.

Talking of conservativism, I imagine administration didn’t solely took a conservative stance when guiding for Snowpark revenues, but additionally when guiding for whole income for FY25. Beside the CEO transition this has been the primary purpose that shares started a big correction after the This autumn earnings launch, so it’s price to take a more in-depth look into this subject.

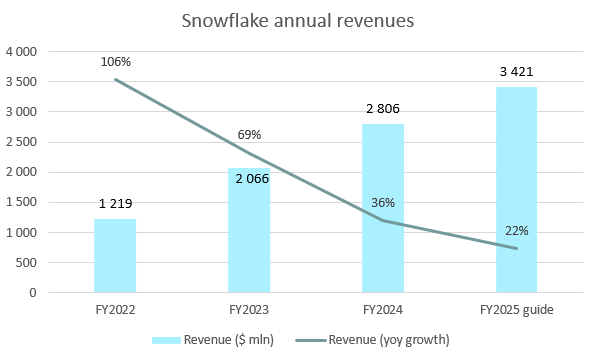

After posting revenues of $2.8 billion for FY24 Snowflake administration guided for little greater than $3.4 billion for FY25, which might equal a yoy income progress price of twenty-two%:

Created by creator based mostly on firm fundamentals

This could imply continued important slowdown from FY24 ranges simply because the yoy income progress price started to indicate indicators of stabilization within the This autumn quarter. Administration acknowledged within the This autumn earnings name that they based mostly their forecast on extra muted FY24 consumption traits, regardless that the second half has been considerably higher:

“I think we are definitely being more conservative this year given the consumption patterns we saw in ’24. And as we said at our Analyst Day last year, we needed to see consumption patterns more in line with what we saw pre-’24 to get to our longer-term goal. And as a result, we’ve decided to forecast this year based upon the consumption patterns we saw in ’24.” – Mike Scarpelli CFO on This autumn earnings name

As consumption patterns didn’t appear to deteriorate going into the FY25 Q1 quarter this equals a built-in buffer, I imagine this could setup the corporate beat-and-raise quarters all through FY25.

On the product forint I already talked about that Snowpark income steerage appears overly conservative for FY25. Nonetheless, what acts like one other buffer is the truth that potential revenues from these merchandise, which can hit normal availability this 12 months (e.g.: Snowflake Cortex, Snowpark Container Companies, Unistore) aren’t factored into the FY25 gross sales information in any respect. As most of those merchandise will hit normal availability in the course of the 12 months this ought to be a supply of additional income upside.

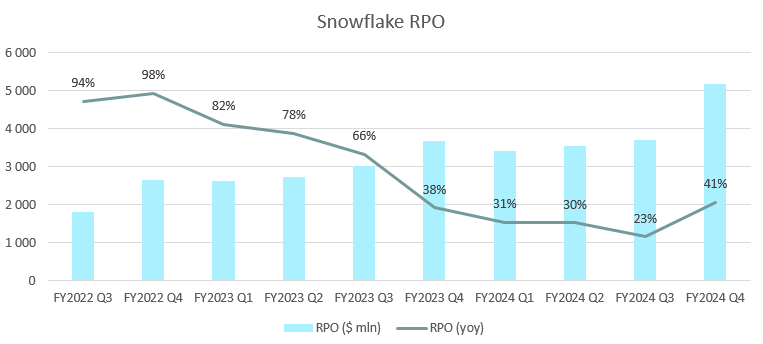

Lastly, one other signal that latest income traits are monitoring properly is the numerous improve in RPO within the This autumn quarter that reached nearly $5.2 billion rising a really robust 41% yoy:

Created by creator based mostly on firm fundamentals

Though this has been partly the results of longer than traditional commitments from prospects, just like the 5-year $250 million file deal within the quarter, it’s nonetheless an vital signal that confidence in the direction of Snowflake is growing.

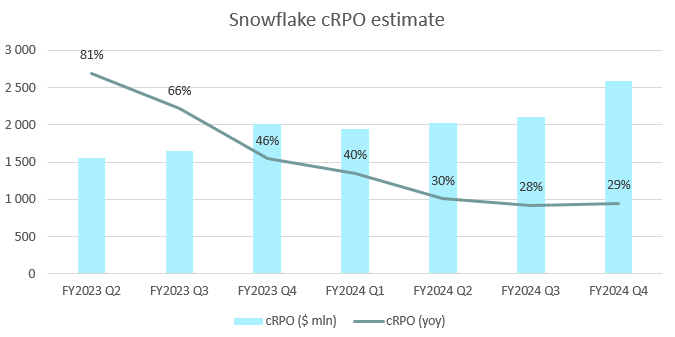

Wanting on the estimated present portion of RPO, which outstrips the results of multiyear offers we are able to see the identical development than within the case of revenues for the This autumn quarter:

Created by creator based mostly on firm fundamentals

cRPO grew ~29% yoy in This autumn roughly on the identical price than within the earlier two quarters. As bookings don’t essentially translate to consumption on Snowflake’s platform within the shut future, they aren’t an correct forecaster of revenues, however the development is encouraging.

To sum it up, the admittedly overconservative steerage from administration (not factoring in upcoming product launches into steerage, conservative estimate for Snowpark, calculating with common FY24 consumption traits as a substitute of most up-to-date traits) and the optimistic development in bookings level into the route that Snowflake might simply beat gross sales estimates over the upcoming quarters. This coupled with latest correction within the share value gives a not often occurring shopping for alternative in my view.

Dangers of falling wanting FY25 steerage

Nonetheless, let’s not overlook that there are additionally draw back dangers for reaching these targets, which I wish to talk about within the following. First, within the case of Snowflake new product launches don’t essentially imply growing revenues as generally these allow value financial savings for patrons. An vital instance for that is Iceberg tables, which might enter normal availability round June. Iceberg tables allow prospects to retailer their knowledge in an exterior cloud storage exterior of the Snowflake platform thereby avoiding storage prices. On this case the shopper is answerable for the administration and safety of the information saved in these tables. Snowflake connects by means of an exterior quantity to Iceberg tables and allows prospects to make the most of its companies even on knowledge in an exterior cloud setting.

On the one hand, this has the potential to convey new enterprise to the Snowflake platform. Alternatively, prospects may have the choice to lower their storage prices with Snowflake in the event that they assume they’ve different to handle and safe their knowledge. At the moment, 10-11% of Snowflake’s revenues are derived from storage companies, so part of these may very well be at stake with this innovation. Administration assumes prospects will make the most of this service relatively within the case of latest workloads, so it shouldn’t have a big affect on topline progress.

One other function, which has been launched to Snowflake’s largest prospects in Q3 is tiered storage pricing, which is a quantity discounting methodology for Snowflake’s largest prospects (minimal annual $1.2 million spent on the platform). Snowflake did this already earlier than asserting this function, nonetheless it is a extra clear and official means of doing it. This may negatively affect revenues in FY25 to some extent, which impact has been extra muted in FY24 because it has been solely launched just lately.

In line with Mike Scarpelli, CFO these efficiency enhancing initiatives for patrons might lead to 6.2-6.3% income progress headwind for Snowflake this 12 months. The danger issue on this case is that prospects will make the most of these value financial savings to a bigger extent within the present cautious IT spending setting pressuring topline progress to a larger extent. So, it’s vital to trace the results of those initiatives intently.

One other vital danger issue for Snowflake is competitors, which primarily consists of the big cloud suppliers’ personal companies (Amazon Redshift, Google BigQuery, Azure Synapse) and Databricks. Within the case of cloud migration workloads from on-prem options like Teradata or Hadoop Snowflake tends to compete with the hyperscalers, whereas within the case of workloads regarding knowledge scientists the competitors is Databricks. Even Snowflake admits that within the case of those workloads Databricks has a really aggressive providing, however I imagine that with the brand new tech-savvy CEO Snowflake might emerge as a powerful competitor on this area as properly.

So, at the moment Snowflake excels in creating an easy-to-use knowledge platform for knowledge engineers, which is the inspiration of an organization’s knowledge technique. This consists of managing the information, constructing pipelines and getting ready knowledge for evaluation. Utilizing this knowledge for analytical workloads, which help administration choices is the subsequent vital step. At this level Databricks is a powerful competitor, but when a buyer already has a big a part of its knowledge ecosystem construct up in Snowflake it’s a sensible resolution to make use of it for analytical workloads or for coaching ML/AI fashions as properly. Particularly that the product providing of the corporate is changing into more and more aggressive on this subject as properly.

CEO transition: Proper individual on the proper time

Along with publishing This autumn earnings Snowflake introduced that Frank Slootman, the just about legendary CEO of the corporate for the previous 5 years is stepping down and shall be changed by former Neeva Founder and CEO Sridhar Ramaswamy. After Slootman’s success at ServiceNow, which has been adopted by the same success story at Snowflake buyers might have been disillusioned about his resolution even when he continues to imagine the place of the Chairman of the Board. Nonetheless, I imagine Snowflake has made the correct step because the deep technical experience of the brand new CEO in search and AI turns out to be useful within the present setting.

Sridhar Ramaswamy and Snowflake crossed their methods when Snowflake acquired Neeva, an ad-free search engine startup final 12 months. Ramaswamy has been the top of Google’s promoting enterprise for a few years and managed to grow it along with his group from $1.5 billion to over $100 billion. Nonetheless, ha wasn’t happy with Google’s advert practices, which created a battle between the pursuits of customers and the shareholders of the corporate. He determined to stop, and created his personal firm, Neeva, the place he might do search in the way in which he imagined. Regardless of creating an ad-free, related search expertise powered by AI the corporate didn’t handle to draw sufficient subscribers to remain afloat. Nonetheless, the technical experience residing inside has been an amazing integration alternative for Snowflake, which continued with the latest appointment of Sridhar as the brand new CEO.

Initially, Sridhar has been charged with main the event of Snowflake’s absolutely managed AI/ML service, known as Cortex, which shall be typically out there to prospects round June. It took his group 7 months till Snowflake Cortex hit non-public preview just lately, which is an incredible efficiency in my view. Cortex is a core platform layer and allows prospects to make use of LLMs to carry out totally different duties (e.g.: analyzing, querying, translating, and so forth.) on their knowledge residing in Snowflake. Moreover, there are a number of ML-based capabilities out there as properly, which may be utilized by means of writing a easy code in SQL. Among the many many new product launches this may very well be the one that pulls essentially the most consideration from prospects and contributes essentially the most to gross sales progress already this 12 months.

Having Sridhar as the brand new CEO positions Snowflake strongly for the present AI are in my view, it has been the correct transfer on the proper time.

Valuation

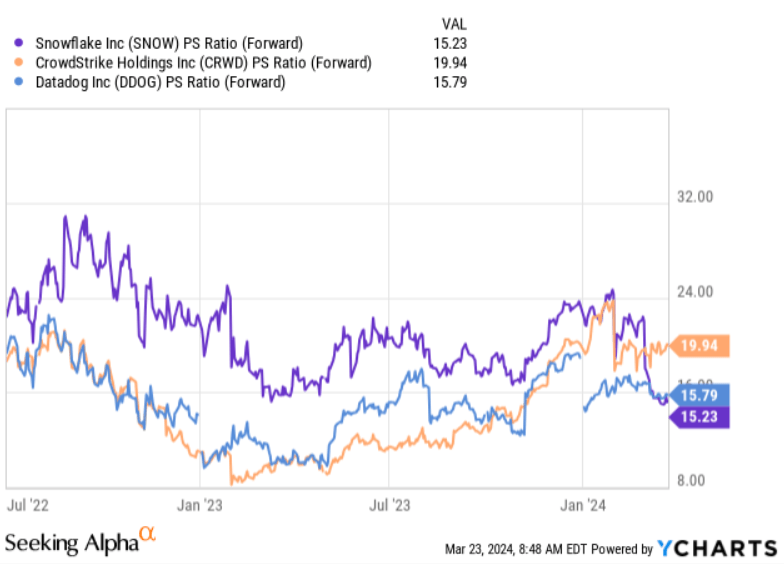

Taking a look at FY24 basic knowledge Snowflake closed the 12 months as Rule of 66 firm, when including 38% yoy product income progress and 28% FCF margin. There should not many public corporations within the SaaS area that reached these highs. For instance, there’s CrowdStrike (CRWD) closing FY24 as a Rule of 67 firm, or there’s Datadog (DDOG) coming in considerably shy as a Rule of 55 firm. What’s attention-grabbing is to match the valuation of those corporations with one another for which I’ve chosen the ahead Worth/Gross sales ratio:

YCharts

From the chart above we are able to see that over the previous two years Snowflake had the heftiest price ticket by far till the start of 2024 with a ahead P/S ratio above 16 for more often than not. Within the mild of robust long-term progress prospects this has been justified in my view. Nonetheless, after the latest This autumn earnings launch the correction of the share value introduced the P/S ratio down to fifteen.2, whereas the valuation of the 2 opponents remained secure throughout this timeframe.

As I’ve proven above the latest earnings launch didn’t level to any significant deterioration in Snowflake’s medium-/long-term progress prospects, it has been the CEO transition and the overconservative steerage of administration that might have unsettled buyers. Primarily based on this, I imagine the correction presents shopping for alternative from a valuation standpoint as properly. Buyers can purchase Snowflake’s shares at a barely decrease valuation than that of Datadog, regardless of Snowflake having considerably greater FCF margin and stronger income progress. Snowflake fundamentals are relatively similar to CrowdStrike’s, whose shares commerce 31% greater based mostly on the ahead P/S a number of.

I imagine this mispricing gained’t final lengthy as Snowflake will handle to perform consecutive beat-and-raise quarters over FY25 as upside dangers dominate draw back dangers by a big margin.