All monetary numbers on this article are in Canadian {dollars} until famous in any other case.

(A Prolonged) Introduction

If there’s one factor now we have mentioned lots this 12 months, it is power. Power is a cornerstone of my long-term funding thesis, as I imagine that we’re in a brand new period the place subdued long-term provide development meets constant demand development.

Basically, since 2020, my optimism about oil and gasoline has grown considerably.

Initially fueled by the anticipation of post-pandemic demand driving up oil costs, my skepticism in direction of the renewables pattern contributed to my desire for oil and gasoline investments.

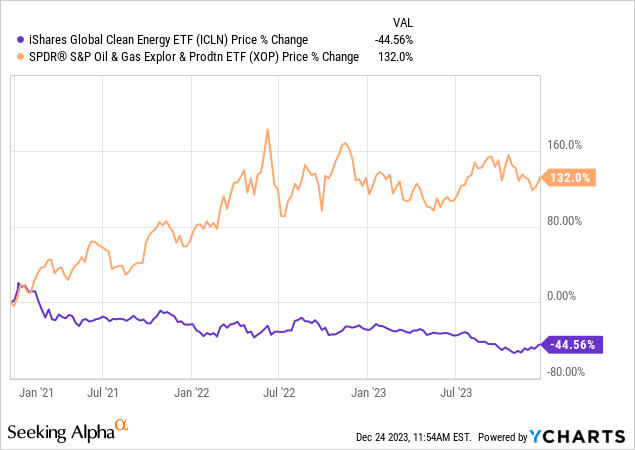

Over the previous three years, clear power shares have misplaced roughly 44% of their worth, excluding dividends, whereas oil and gasoline drillers have gained over 130%.

Do not get me incorrect, I am not towards clear power – in no way. My concern lies in the pressured international power transition, resulting in subdued investments in oil and gasoline regardless of sturdy demand.

Corporations now prioritize free money stream for stability and decreased vulnerability to grease worth crashes. Most firms, that’s.

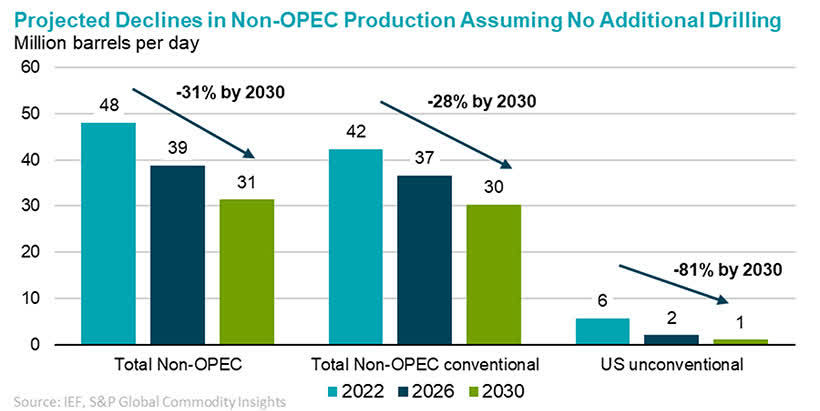

Moreover, U.S. shale manufacturing is shedding steam, and estimates counsel a possible 81% decline by 2030 with out new drilling. This shift has international implications, impacting provide development and giving OPEC, particularly Saudi Arabia, vital pricing energy, which they’ve used this 12 months by slicing output.

Worldwide Power Discussion board

Whereas it’s definitely attainable that oil costs might proceed to say no if financial development retains deteriorating, I imagine that oil costs will stay elevated for a few years to come back, with a excessive likelihood of triple-digit greenback oil costs in a state of affairs of strengthening financial development.

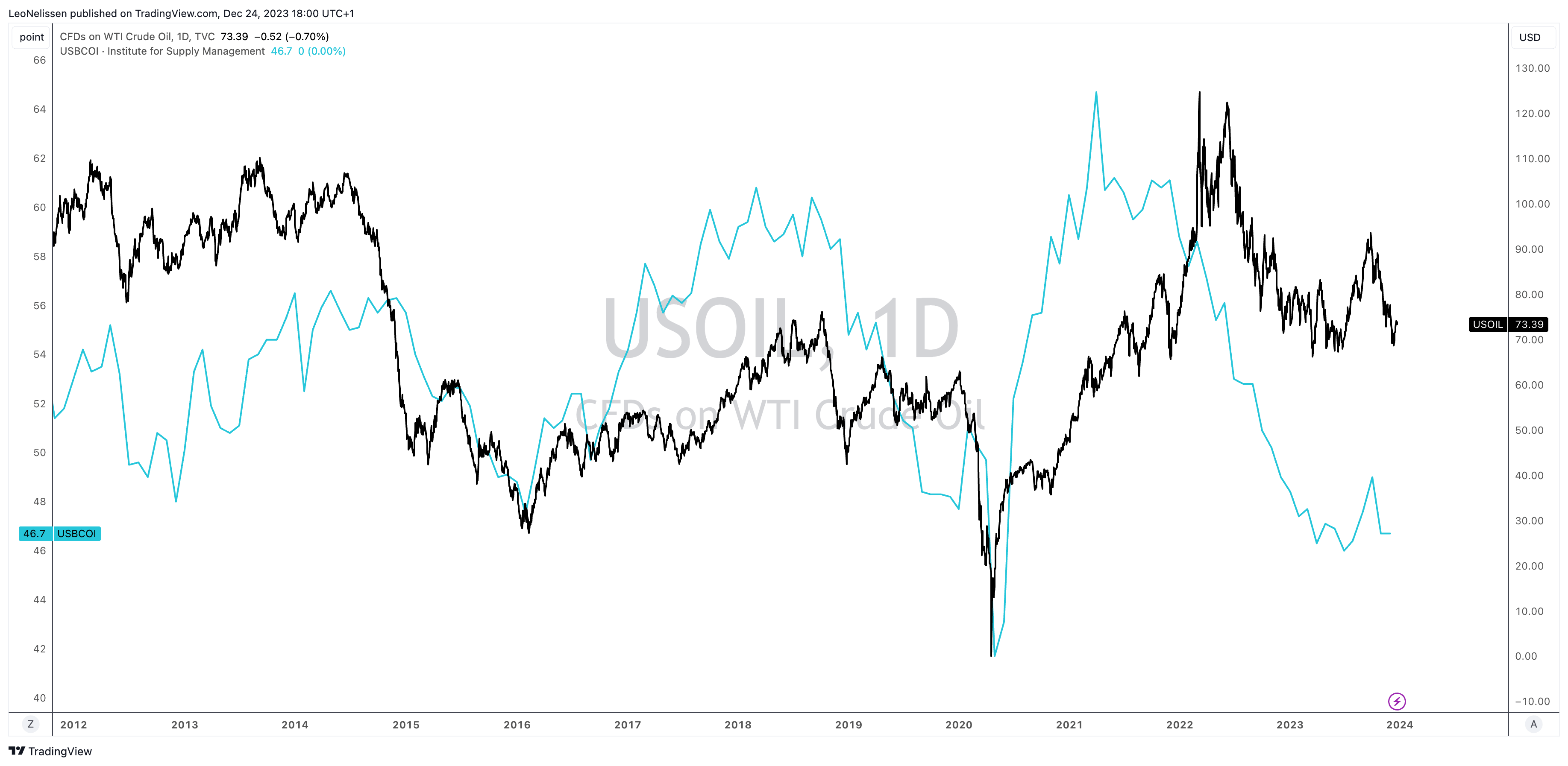

Proper now, WTI (CL1:COM) is buying and selling above $70 even though the ISM Manufacturing Index has been in contraction territory each single month this 12 months.

TradingView (WTI, ISM Index)

I imagine that if the availability scenario had been totally different, oil can be buying and selling barely above $50 proper now.

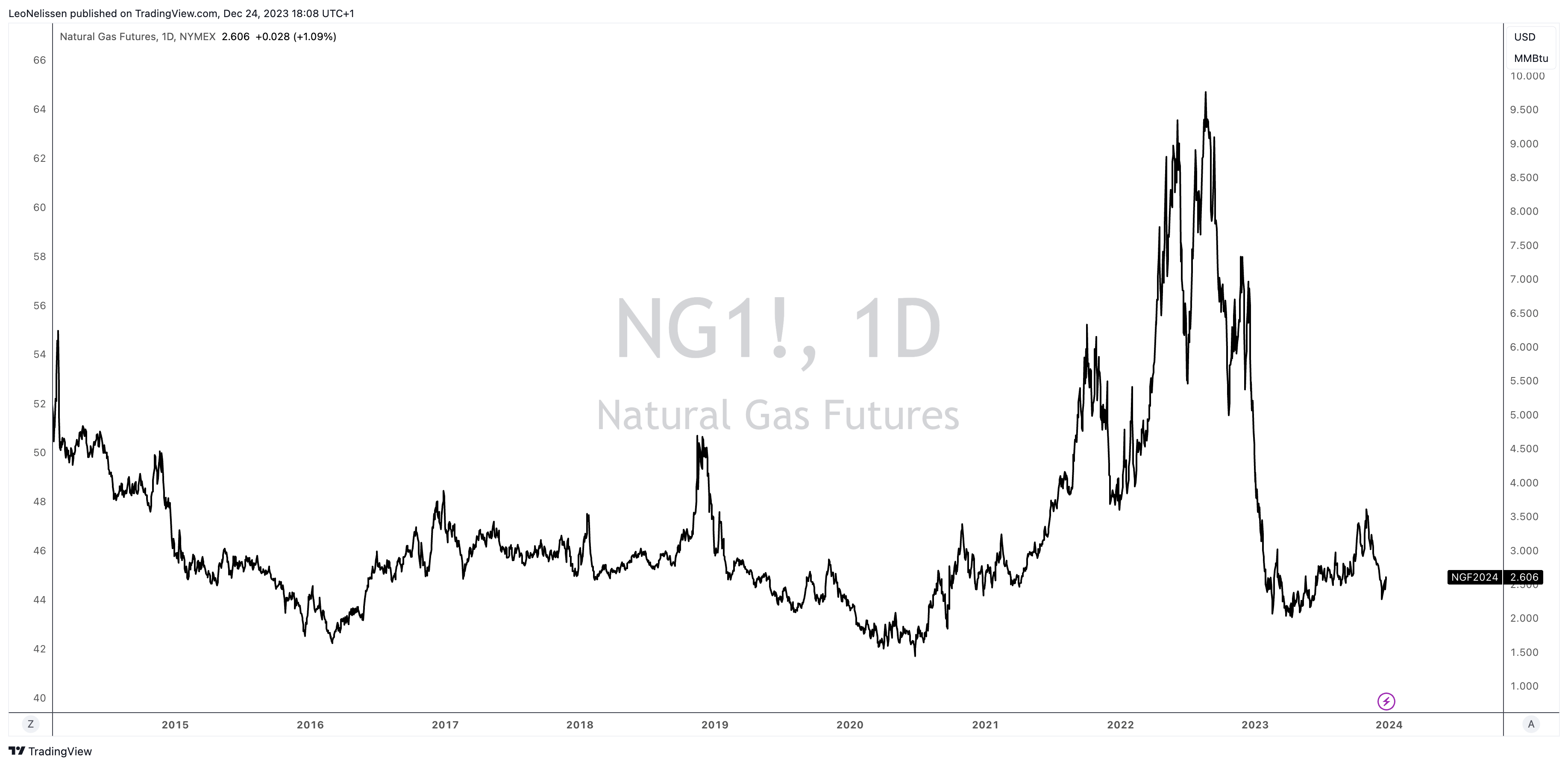

With that stated, the scenario for pure gasoline is a bit totally different, as pure gasoline provide development is quicker. This commodity is extra plentiful and far more unstable than oil.

NYMEX Henry Hub benchmark pure gasoline costs are at simply $2.60 per MMBtu resulting from weak financial development, delicate climate, and higher-than-expected inventories.

TradingView (NYMEX Henry Hub)

Nonetheless, on a long-term foundation, I’m very bullish on pure gasoline.

That is what I wrote in a latest article (emphasis added):

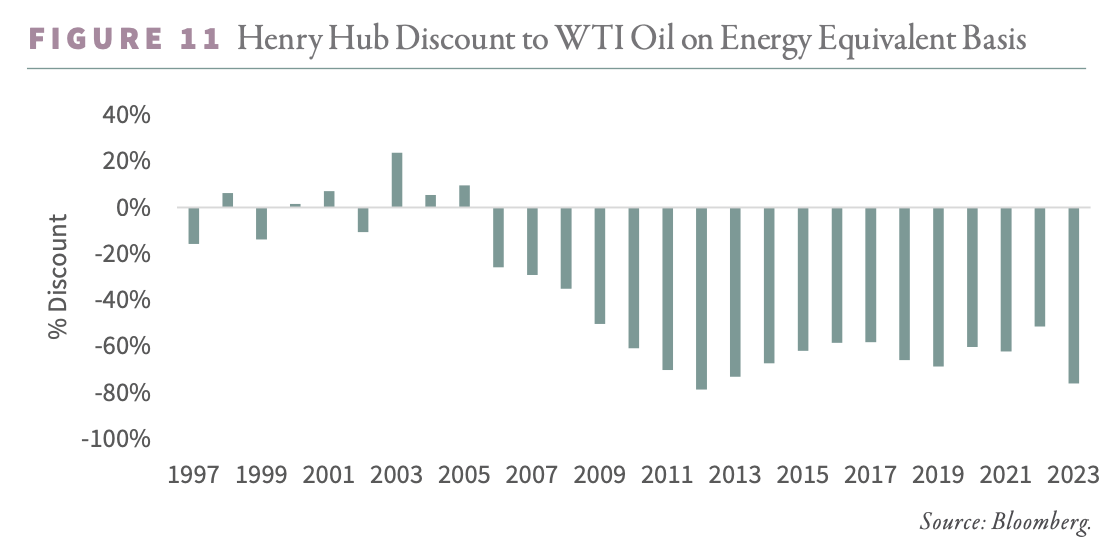

Power consultants Goehring & Rozencwajg believe that pure gasoline costs in america are method too low-cost, in accordance with international power costs.

In actual fact, G&R believes that pure gasoline costs within the U.S. are buying and selling at an 80% low cost to international power costs.

Goehring & Rozencwajg

Though a reduction is warranted resulting from America’s deep pure gasoline reserves and low-cost manufacturing strategies, it’s seemingly that this low cost will decline.

The preliminary expectation of convergence in North American pure gasoline costs with worldwide costs confronted delays resulting from a light winter and a hearth on the Freeport LNG export terminal in 2022.

These occasions, together with elevated U.S. inventories, led to an 80% decline in North American pure gasoline from the 2022 peak.

Nonetheless, these challenges are deemed non permanent, with extra inventories being addressed and operators planning so as to add six bcf/d of recent LNG export capability in 2024.

Moreover, G&R’s fashions now counsel that shale manufacturing is probably going plateauing, and the low cost to world costs will slim, probably disappearing.

The fashions predict that North American pure gasoline is on the verge of getting into a structural deficit for the primary time in 20 years, doubtlessly prompting regulatory actions to restrict exports and stabilize costs.

Based mostly on these numbers, Henry Hub pure gasoline costs of at the least $10/MMBtu might turn out to be the brand new regular.

This brings me to the star of this text, an oil and gasoline producer from Canada, which has all the pieces I am in search of in an power inventory:

Deep reserves.

Very environment friendly operations.

A wholesome steadiness sheet.

A give attention to shareholder distributions.

It is also one of many few firms centered on quick development, which bodes very effectively for future free money stream and shareholder advantages.

That firm is ARC Sources Ltd. (OTCPK:AETUF, TSX:ARX:CA), an organization I imagine most will not be conversant in.

So, let’s dive proper into it and talk about why I put this inventory on my watchlist, as I imagine it might be an amazing addition to my portfolio.

One Of The Finest In Its Trade

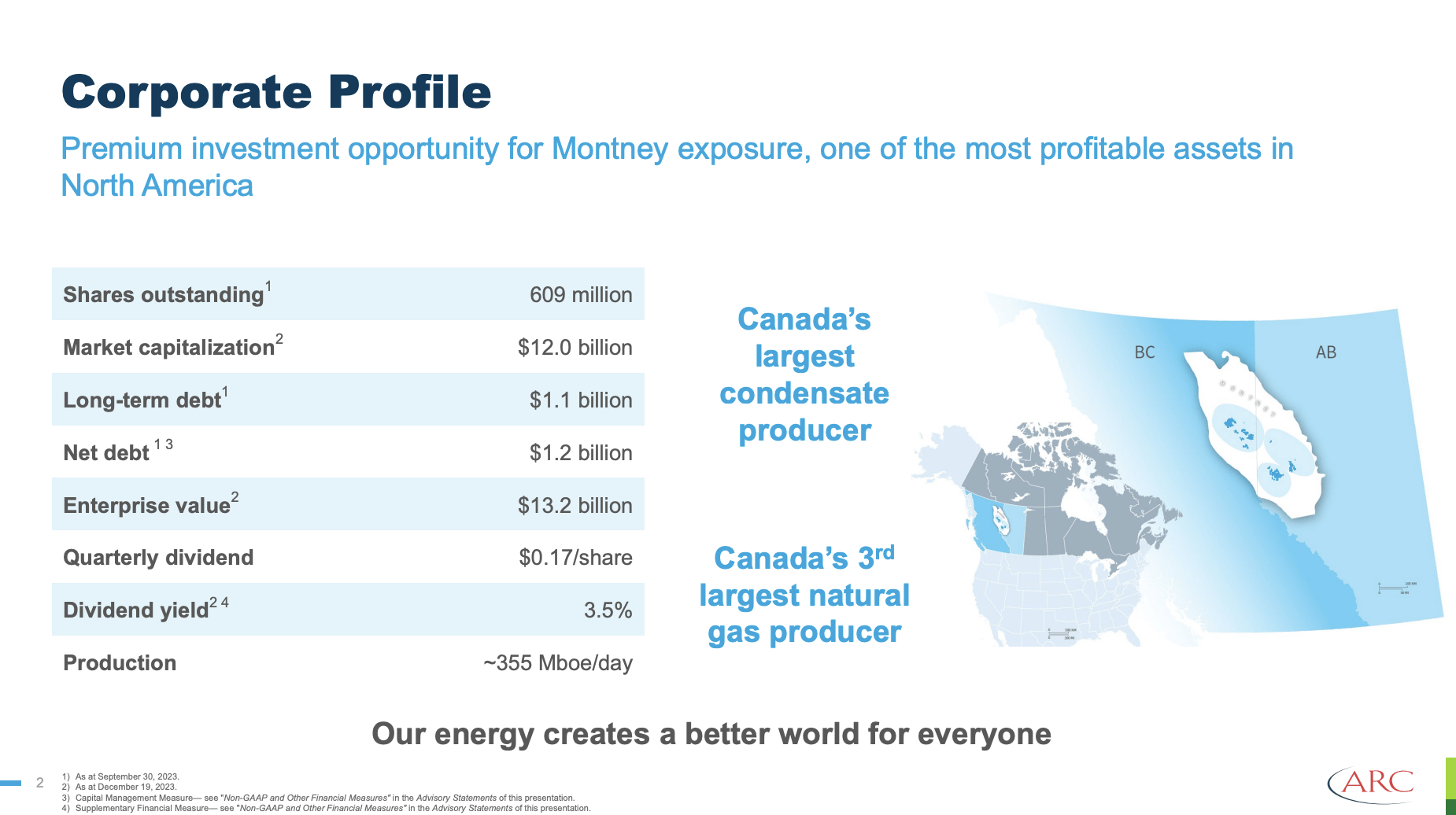

Arc Sources is considered one of Canada’s largest oil and gasoline producers, with a market cap of roughly $12 billion. That is roughly US$9 billion.

It produces near 360 thousand barrels of oil equal per day (MBOE/d), which makes it one of many greatest producers in all of North America.

The corporate produces within the Montney Formation, which is part of Canada’s well-known Western Canadian Sedimentary Basin (“WCSB”), an space with a number of the world’s greatest fossil gasoline reserves.

ARC Sources

The corporate is so giant that it’s Canada’s Third-largest pure gasoline producer.

Observe that oil accounts for only a quarter of its whole manufacturing. The remaining manufacturing comes from pure gasoline and higher-margin pure gasoline liquids (“NGL”).

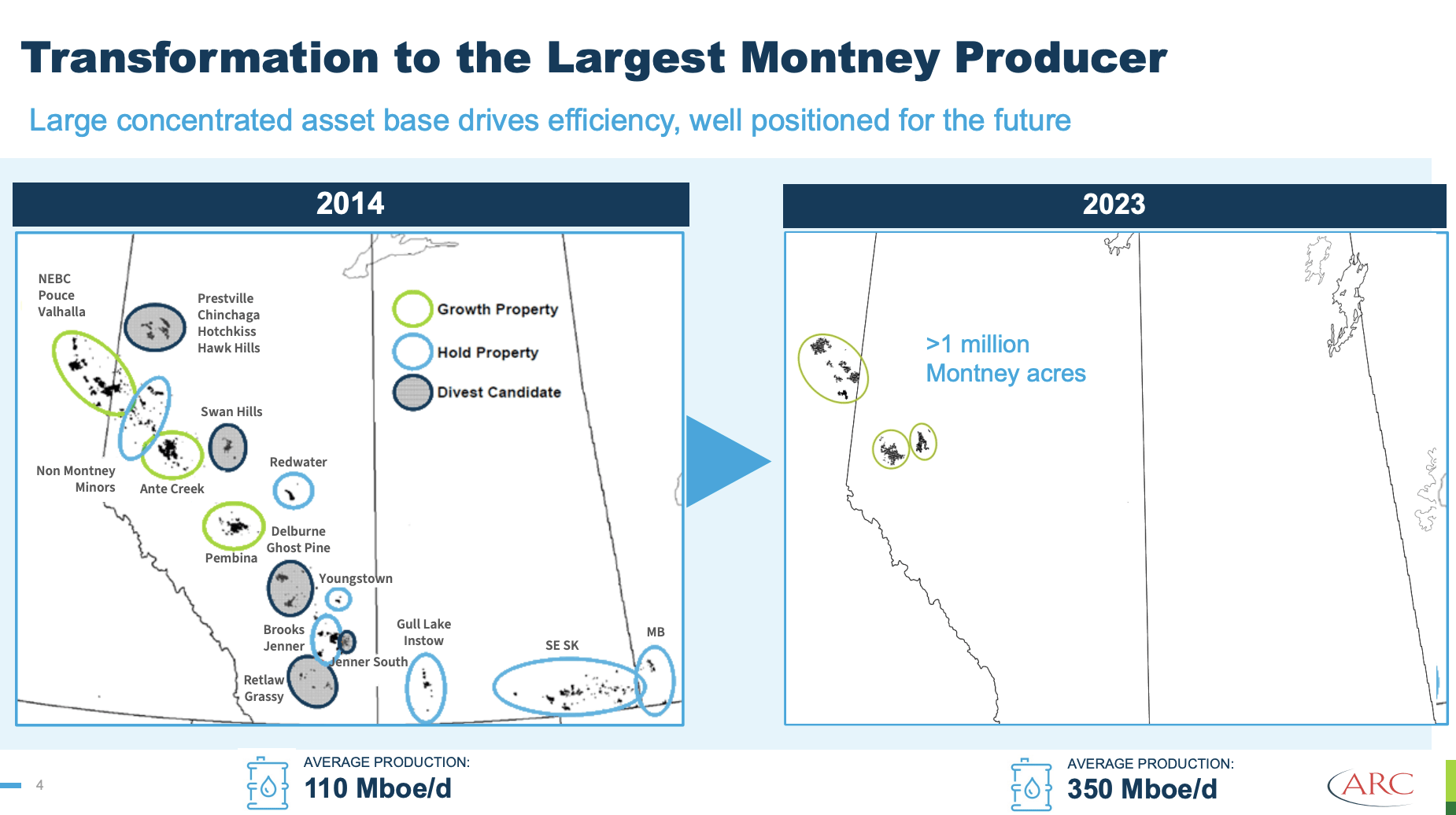

As we will see under, over the previous ten-ish years, the corporate has divested quite a lot of non-core belongings to give attention to the most effective development performs within the Montney Formation.

Because of this, with fewer performs, it nonetheless managed to spice up manufacturing from $110 MBOE/d to 350 MBOE/d.

ARC Sources

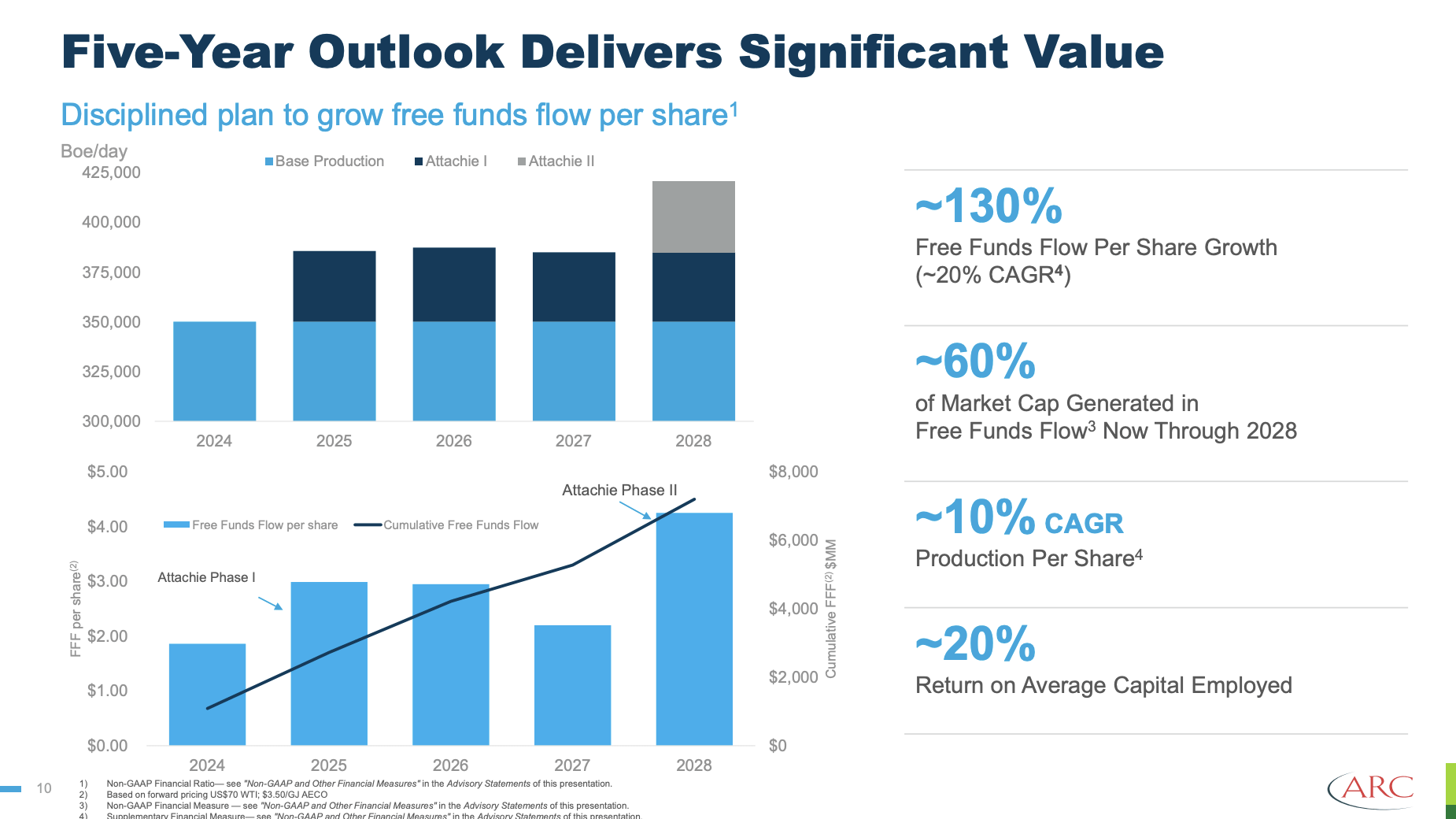

What fascinates me about ARC is its long-term plan. After divesting non-core belongings, it’s now engaged on an bold five-year plan.

ARC, in its bold five-year plan spanning from 2024 to 2028, envisions a strategic strategy that emphasizes capital effectivity, sustainable development, and substantial returns for its shareholders.

On the core of ARC’s technique is a dedication to a capital-efficient program designed to foster long-term per-share development. The corporate goals to strike a steadiness between investing in its worthwhile belongings and making certain a significant return of capital to shareholders.

ARC’s manufacturing steering for 2024 is ready between 350,000 to 360,000 BOEs per day. This projection elements within the anticipated expiry of an ethane gross sales contract within the second quarter, which is anticipated to scale back reported NGL manufacturing by roughly 5,000 barrels per day on an annualized foundation.

To counter this, ARC plans to reinject ethane into the pure gasoline stream, leading to increased income from the gross sales of upper heat-content gasoline.

With this in thoughts, as we will see under:

The corporate goals to develop per-share manufacturing by 10% per 12 months.

Free money stream per share is anticipated to develop by 20% per 12 months (depending on costs).

The corporate goals for a 20% return on common capital employed.

ARC Sources

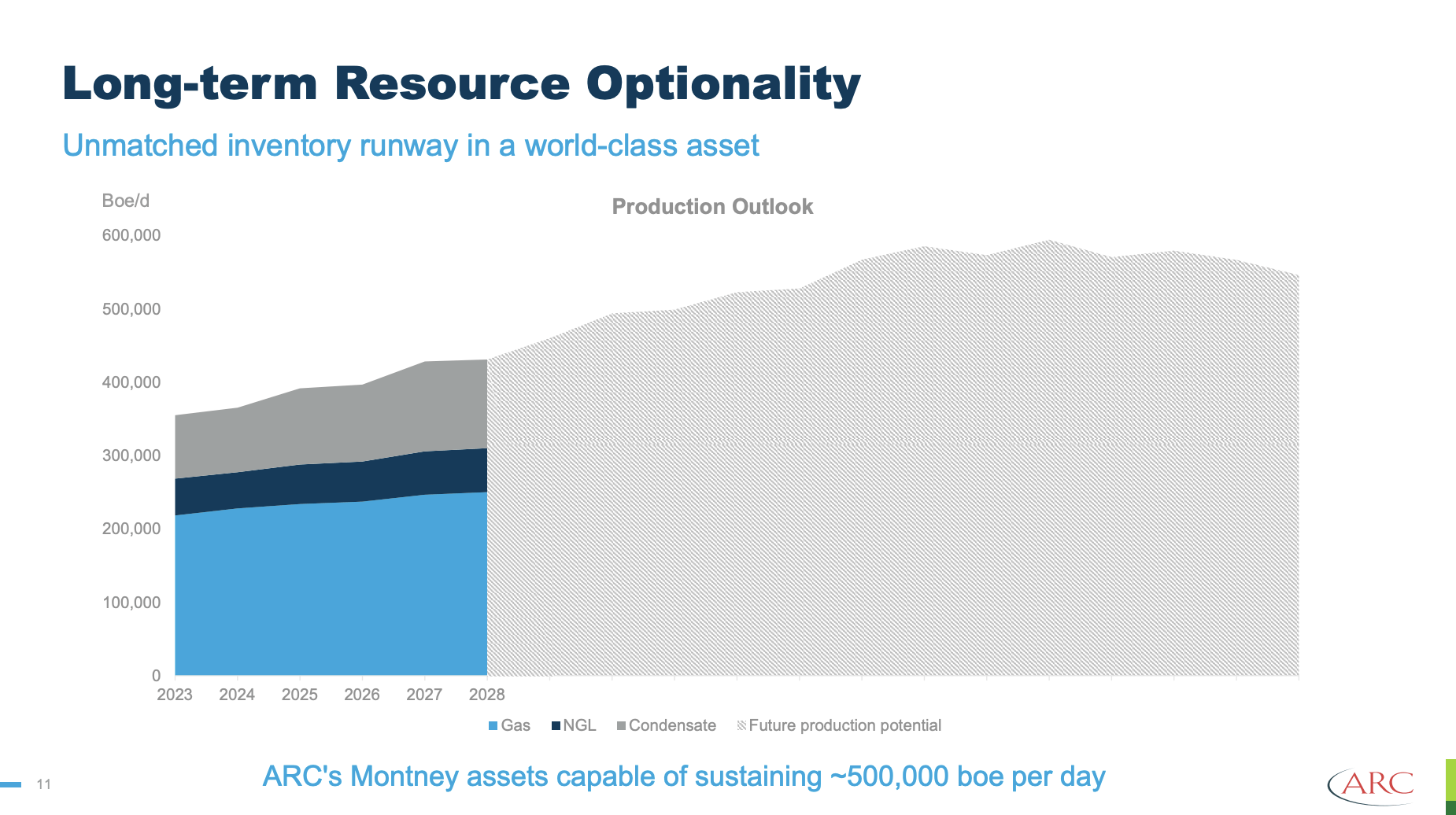

In different phrases, whereas different gamers are decreasing future development plans, ARC is raring for fast manufacturing development – even after 2028, as we will see within the chart under.

Until its friends comply with and enhance manufacturing as effectively, ARC is in a unbelievable spot to profit from increased manufacturing and higher (anticipated) pricing on a protracted foundation.

ARC Sources

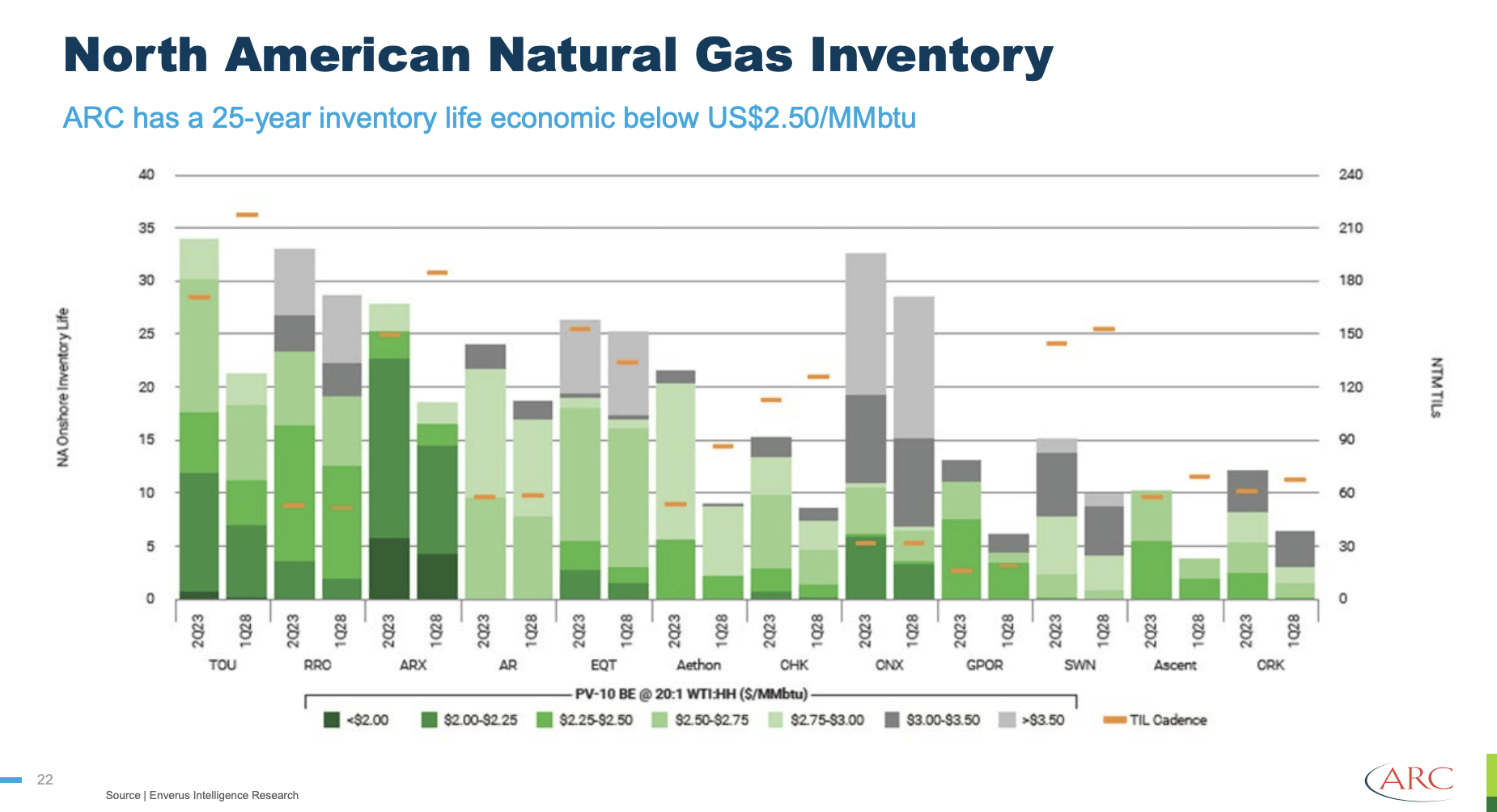

Nonetheless, not like most friends, the corporate is in a great spot to spice up manufacturing. It has huge reserves!

The corporate at present has a 25-year stock life that’s breakeven under US$2.50 Henry Hub. This makes ARC a standout participant in its trade.

ARC Sources

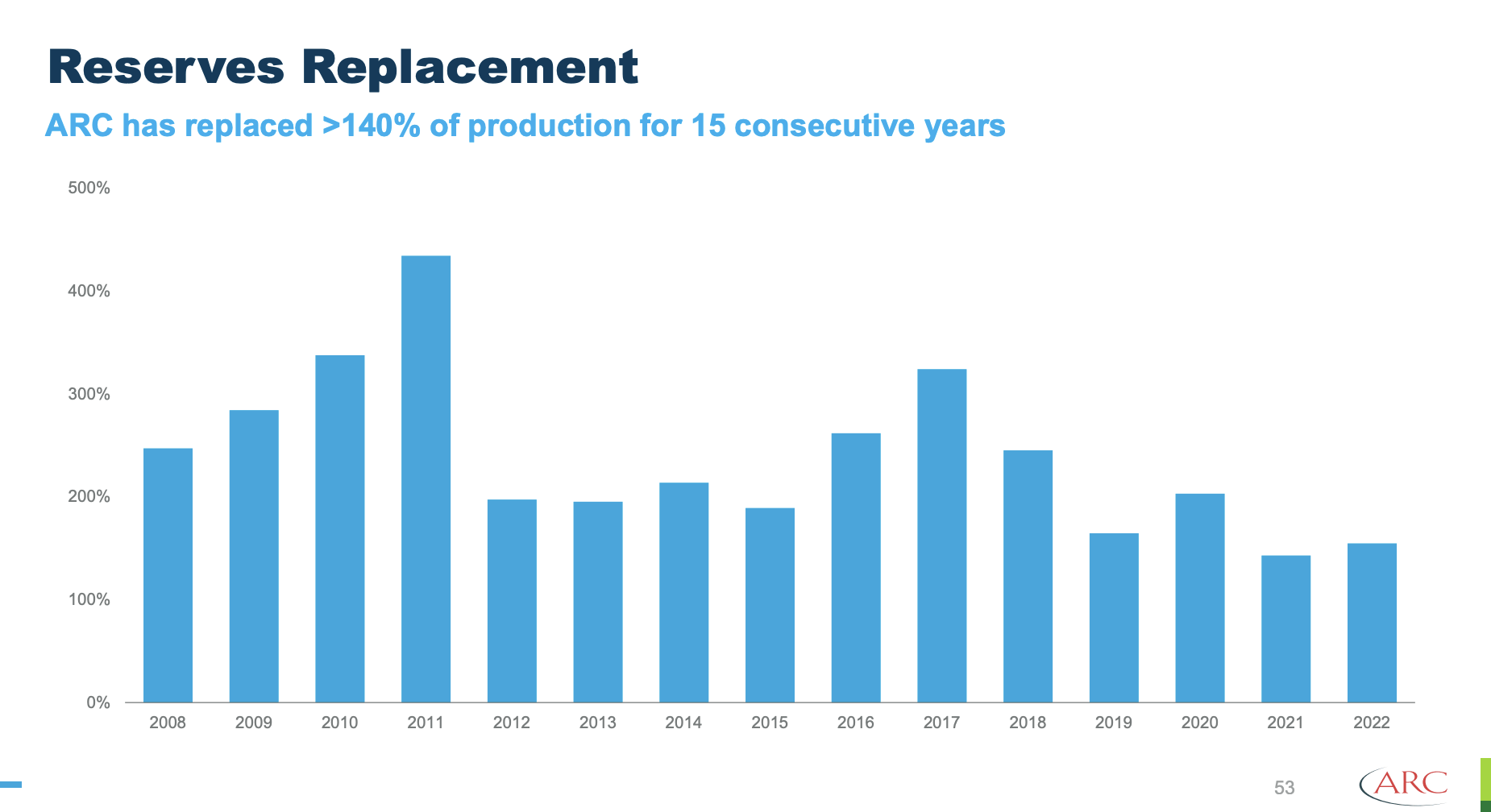

On prime of that, the corporate persistently expands its reserves. ARC has changed greater than 140% of manufacturing for 15 conservative years.

ARC Sources

Moreover, in 2024, ARC plans to take a position $1.8 billion, a discount of about $200 million in comparison with 2023, adjusting for its Attachie development capital.

The corporate attributes this effectivity to 2 key elements:

a decrease company decline in 2024, necessitating fewer wells to offset manufacturing declines and

a concerted effort to additional cut back nonproductive capital, significantly at Kakwa.

ARC forecasts little change in its value construction for 2024. Working and transportation prices are anticipated to stay comparatively unchanged year-over-year, hovering round $10 per BOE mixed.

This stability underscores the resilience of ARC’s enterprise mannequin, as the corporate asserts it could maintain manufacturing within the vary of 350,000 to 360,000 BOE per day and fund the present dividend with natural money stream even in a difficult surroundings with WTI at US$45 a barrel and $2 AECO per Mcf.

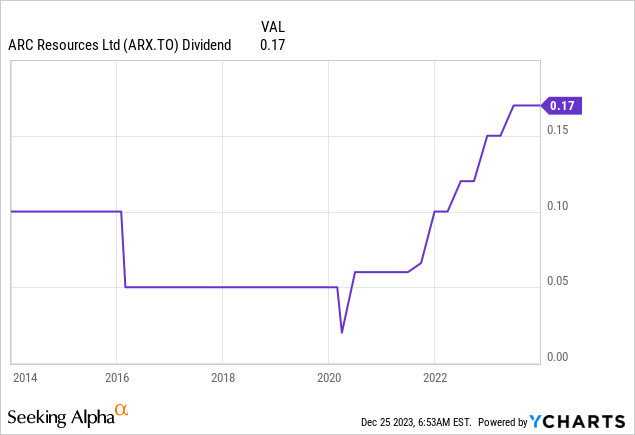

Keep in mind that the bottom dividend is $0.17 per share per quarter. This interprets to a yield of three.5%. This dividend is protected at US$45 WTI and simply CAD$2 AECO, which could be very low!

Observe that the corporate has realized a mean premium to AECO costs of 20% over the previous decade. I anticipate that to carry, as it’s utilizing liquid pure gasoline alternatives in North America, which comes with extra pricing advantages.

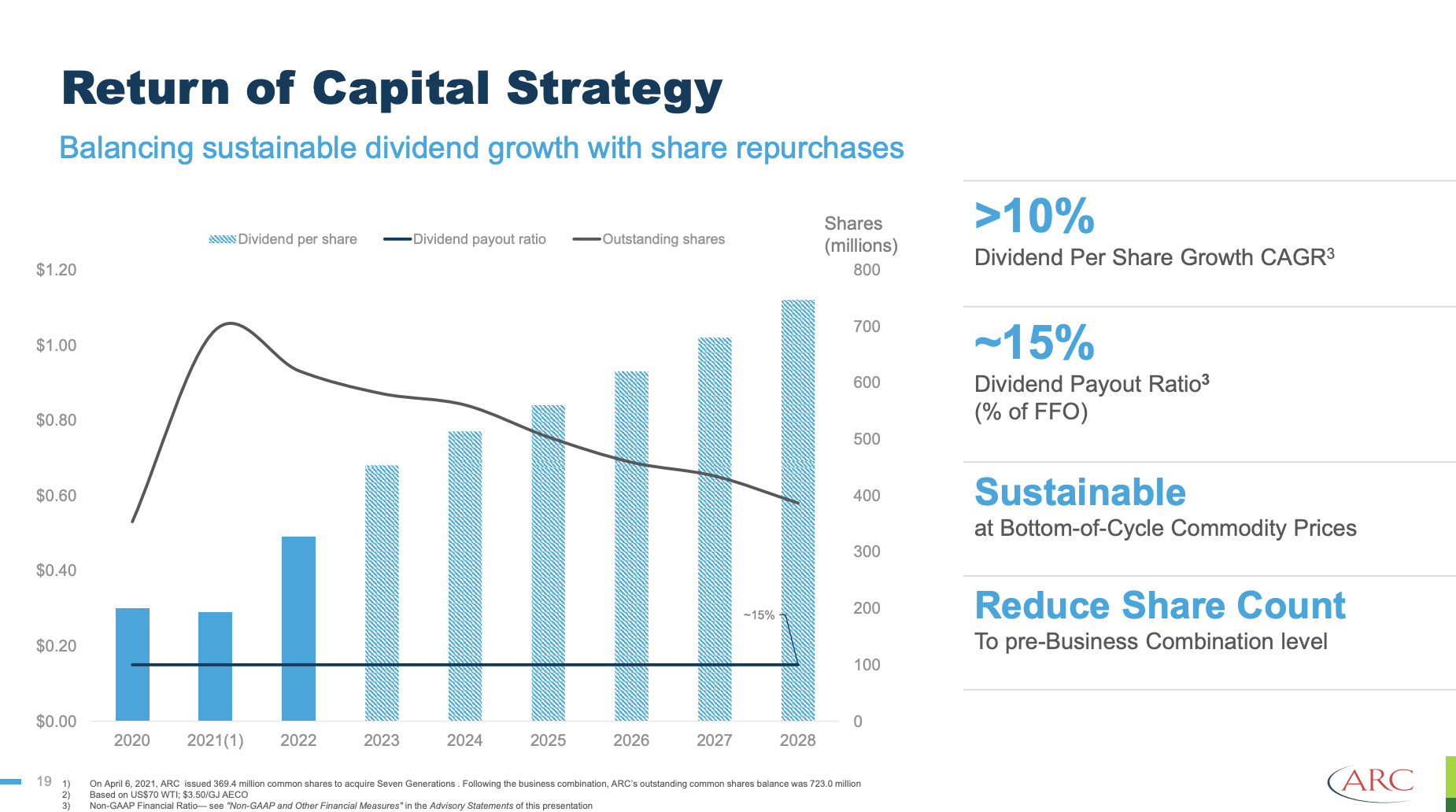

Since 2020, the corporate has persistently grown its dividend and is anticipated to maintain doing this for a lot of extra years to come back.

Additionally word that the corporate needs to develop the dividend together with its enterprise, not the value of oil.

This is essential to remember, as it’s utilizing per-share manufacturing and free money stream development to sustainably develop the dividend.

Extra free money is distributed utilizing buybacks.

ARC Sources

Since 2020, the corporate has grown its dividend by roughly 10% per 12 months. It has a dividend payout ratio of simply 15% (a lot room for dividend development and buybacks) and a big discount in its share depend.

ARC Sources

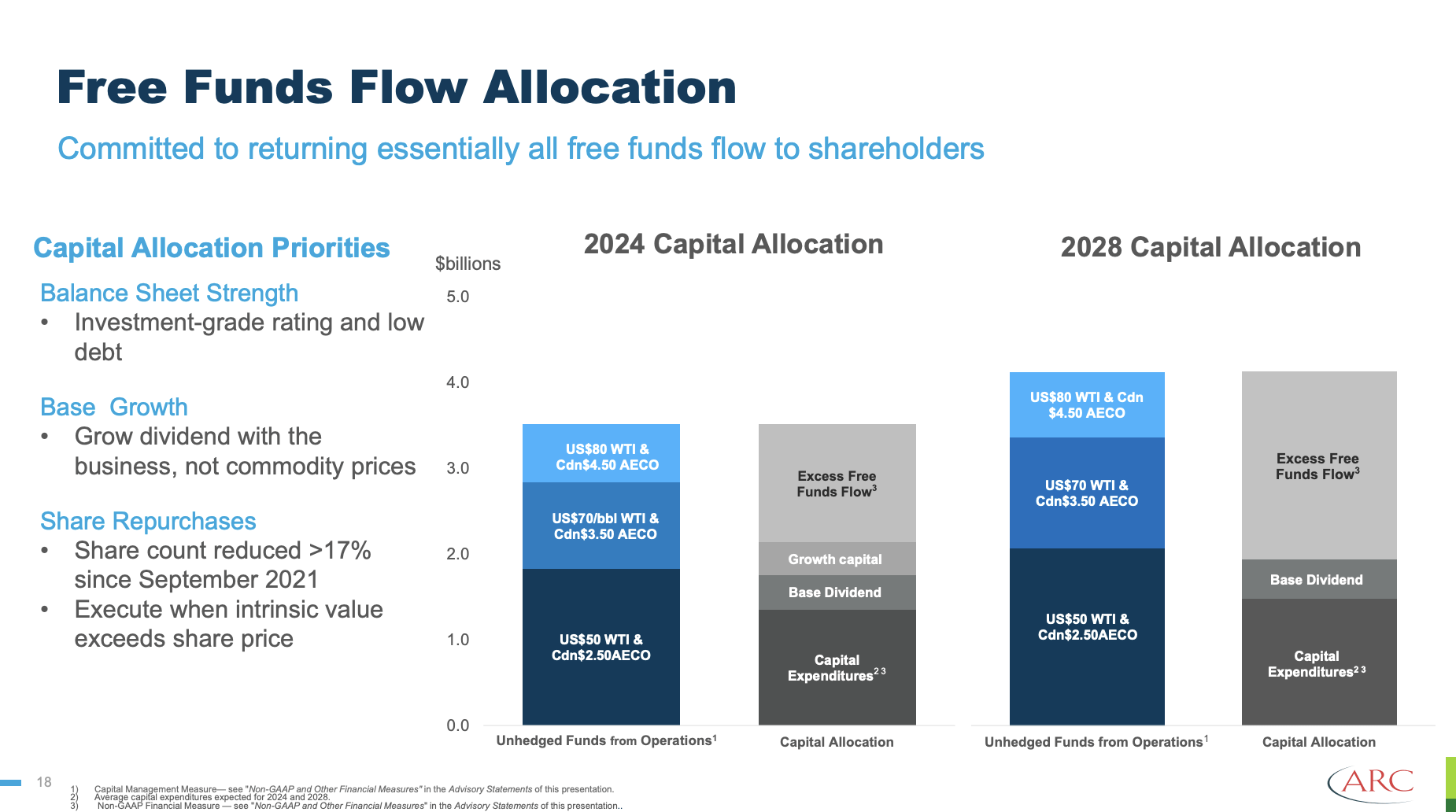

As we will see within the overview above (Free Funds Move Allocation), at US$80 WTI and $4.50 AECO, the corporate can generate near $1.5 billion in free money stream after its base dividend. That is an extra 12% in buyback potential, excluding development capital.

That’s nearly unmatched in its trade.

In 2018, that quantity might be north of $2 billion, or nearly 17% of its market cap, resulting from increased manufacturing charges.

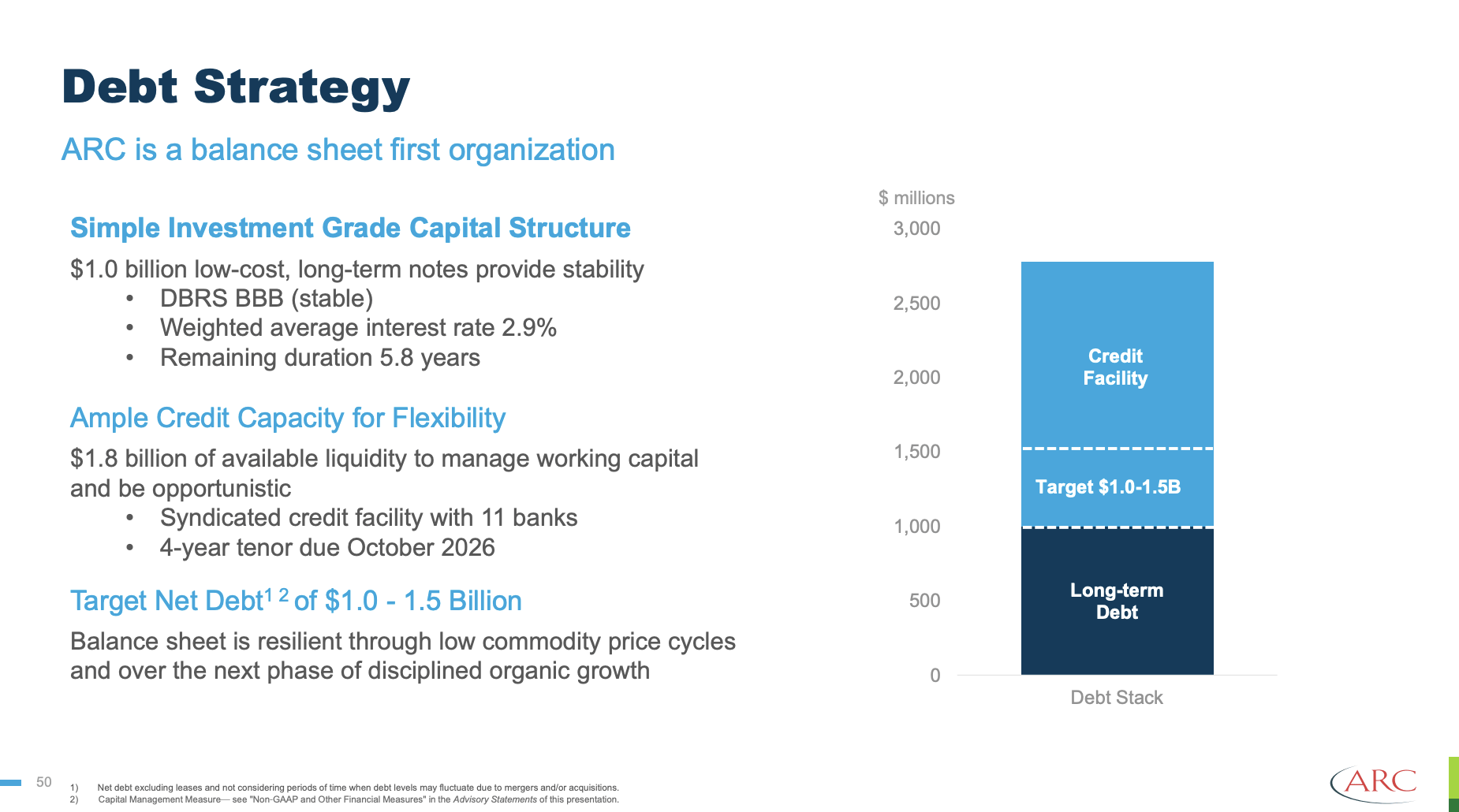

It additionally has a wholesome balance sheet, which permits the corporate to prioritize shareholders over debtholders.

The corporate has no debt maturities till 2026. It additionally has no maturities between 2026 and 2031.

Even at US$50 WTI/US$3 Henry Hub, it has a internet debt to FFO (funds from operations) ratio of lower than 1.0x.

The corporate goals to maintain internet debt between $1.0 and $1.5 billion.

ARC Sources

Now, let’s check out the valuation.

Valuation

That is the difficult half, as firms that depend on the value of the commodities they produce are liable to unstable earnings.

Nonetheless, I’m making the case that ARC is reasonable.

As I imagine that each pure gasoline and oil costs have a vibrant future, the corporate’s aforementioned free money stream potential makes it an amazing purchase at these ranges.

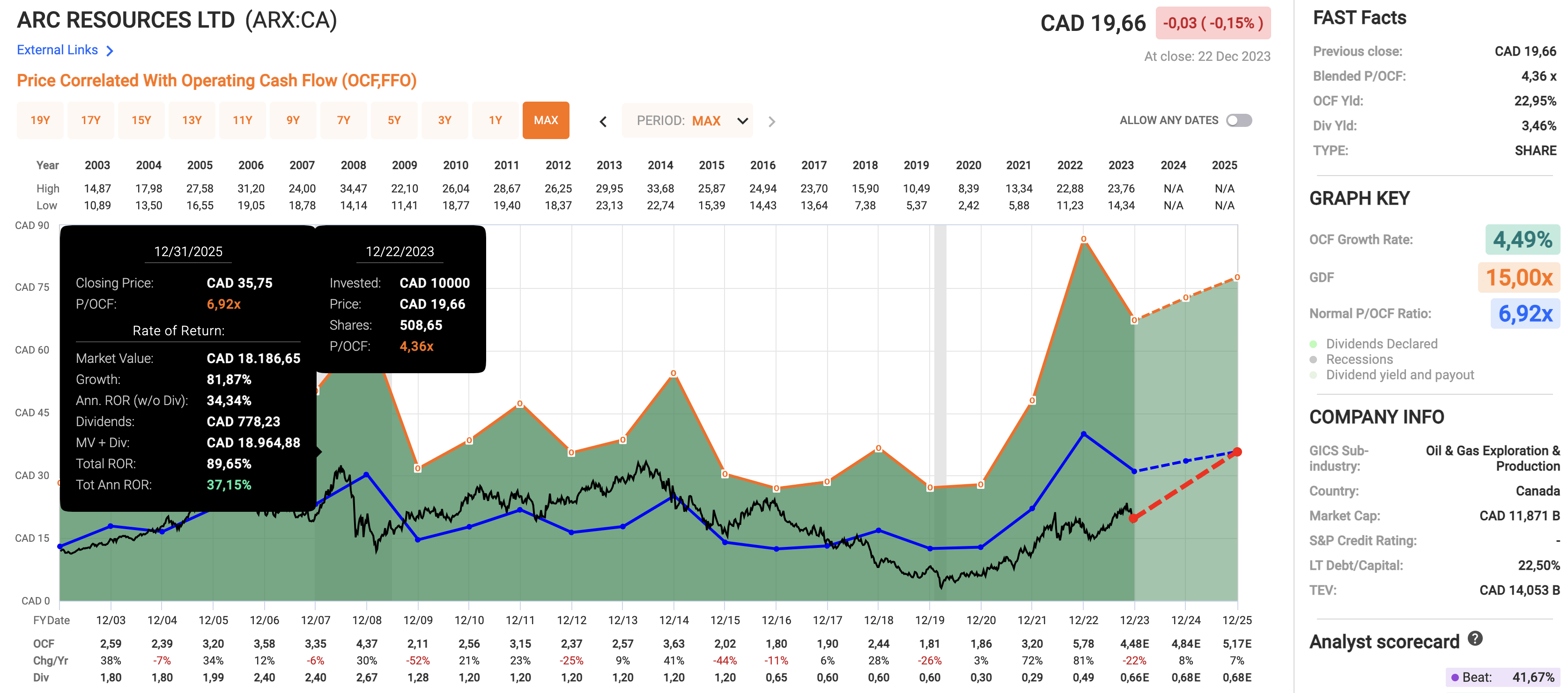

Even at these ranges and primarily based on present analyst estimates, the inventory is reasonable.

The corporate at present trades at a blended P/FFO ratio of 4.4x. That’s under its long-term normalized valuation of 6.9x. A return to that valuation primarily based on 22% anticipated FFO contraction in 2023, 7% anticipated development in 2024, and eight% anticipated development in 2025 would give the inventory a good worth goal of roughly $36 in Toronto. That’s 80% above the present worth.

FAST Graphs

Though I don’t promise something, I imagine that after power costs begin a sustainable uptrend with assist from enhancing financial development, traders will rush into undervalued power performs, inflicting ARC shares to commerce a lot increased.

Therefore, I’m utilizing $36 as a longer-term goal.

Presently, I don’t personal ARC Sources Ltd. Nonetheless, I’m determining how you can embrace it in my portfolio. I personal Canadian Pure Sources (CNQ) and Devon Power (DVN) in my dividend portfolios. I’ll seemingly promote some pure gasoline shares from my buying and selling portfolio and begin one or two significant new power positions in my long-term funding portfolio. Considered one of them is prone to be ARC Sources.

Evidently, I am going to hold readers up-to-date in 2024!

Takeaway

As international forces push for a inexperienced transition, ARC Sources Ltd. stands out as a strong participant in oil and gasoline.

Boasting a 25-year stock life and a strategic development plan, ARC combines effectivity with shareholder-friendly practices.

The corporate’s dedication to sustainable development, a 20% return on capital, and a resilient dividend, even in difficult situations, make it a standout within the trade.

With a present undervaluation and a possible honest worth goal of $36, ARC Sources is a promising addition to my watchlist, signaling a bullish outlook on the long-term prospects of pure gasoline and oil.

Editor’s Observe: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.