Presley Ann/Getty Photographs Leisure

The market was so targeted on whether or not SoFi Applied sciences, Inc. (NASDAQ:SOFI) was GAAP worthwhile within the December quarter, most individuals missed that the fintech was already a cash machine. The corporate guided to huge tangible e-book worth progress in 2024 with adjusted earnings set to soar. My investment thesis stays extremely Bullish on the inventory, nonetheless struggling to breakout above the unique SPAC worth of $10 introduced all the best way again in 2020.

Supply: Finviz

Revenue Machine

The inventory has been very risky because the SPAC deal, however the firm continues to report blockbuster numbers. SoFi simply reported Q4 ’23 revenues of $594.3 million, up an unbelievable 34% from final This fall.

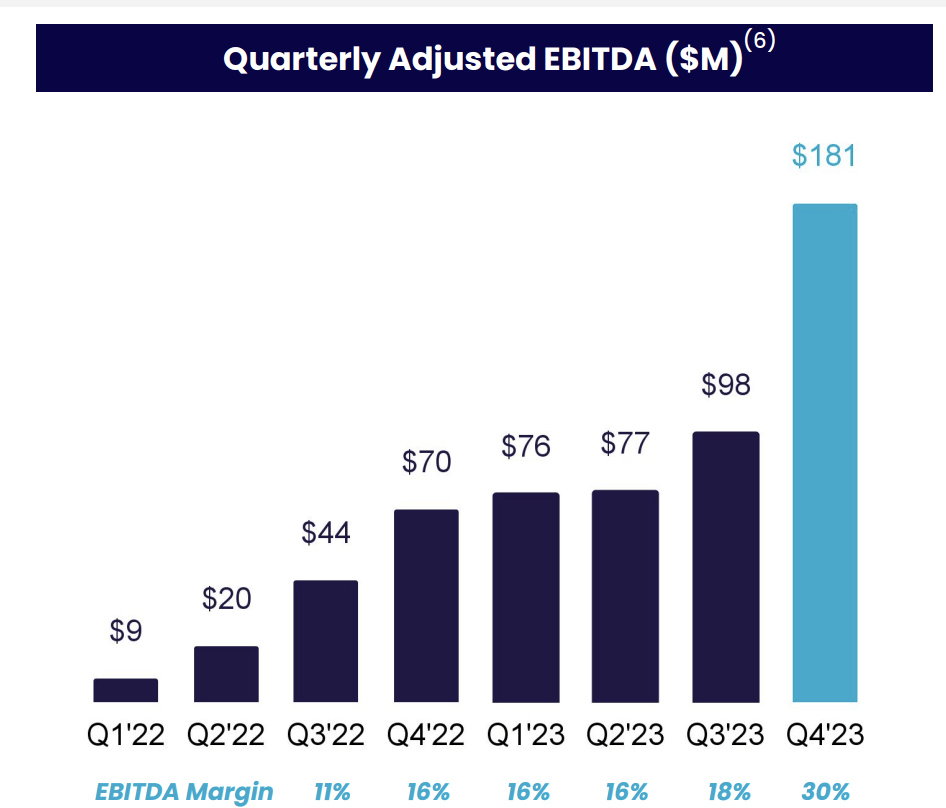

Whereas the highest line income progress was outstanding contemplating the robust financial surroundings and restricted demand for loans, the larger increase got here from the backside line. SoFi reported This fall’23 adjusted EBITDA practically doubled sequentially from Q3 to $181 million.

Supply: SoFi This fall’23 presentation

The fintech reported growing quantities of adjusted EBITDA over the past yr, however the market principally ignored this progress. The prime motive was the concentrate on GAAP earnings, with SoFi reaching this milestone throughout This fall’23 with an EPS of $0.02.

Naturally, a minimal EPS is not spectacular, however for quite a few causes, traders ought to focus extra on the adjusted earnings. The prime motive adjusted EBITDA is definitely an adjusted revenue metric is that the first bills excluded are non-cash expenses.

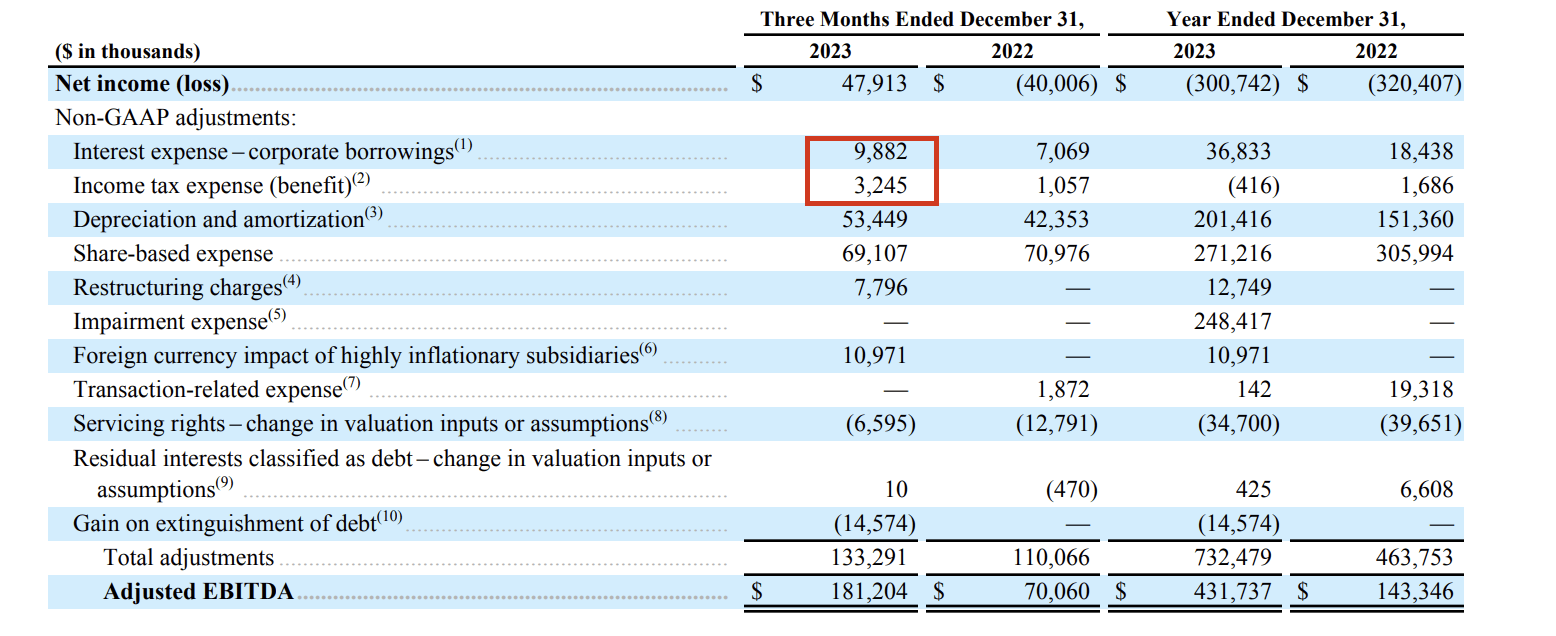

Outdoors of curiosity bills and earnings taxes highlighted within the beneath EBITDA desk, the opposite expenses are usually non-charge. Of the $181 million in adjusted EBITDA, SoFi solely had $13.2 million in regular bills not excluded from an adjusted revenue metric.

Supply: SoFi This fall’23 earnings launch

As highlighted earlier than, the first changes are for amortization expenses and stock-based expense. The two expenses mixed for $122.6 million in reversible expenses.

The amortization expenses don’t have anything to do with the continuing enterprise and all the things to do with writing off the extreme buy worth of acquisitions. The fintech even took a big goodwill impairment expense final quarter. The stock-based expense is factored into the EPS calculation with the diluted share counts.

With SoFi now reporting earnings, the corporate now lists a diluted share depend of 1.03 billion. The inventory now has a $9 billion market cap, with the inventory leaping to $9 following the sturdy This fall outcomes.

A major instance of the revenue machine arrange for SoFi is the steerage for tangible e-book worth to develop by $300 to $500 million within the present yr. The GAAP EPS goal for the corporate is just $0.06, which quantities to simply $60 million in web earnings for the yr.

Huge Steering

SoFi enters 2024 as a sudden revenue machine. The corporate guided to the next numbers for the yr:

- Tech Platform and Monetary Companies progress of fifty% or extra versus 2023 ranges

- Lending phase at 92-95% of 2023 income ranges

- GAAP Web Earnings of $95 – $105 million

- Adj. EBITDA of $580 – 590 million

- EPS of $0.07 – $0.08 cents

- $300 – 500 million of Tangible E book Worth progress.

The massive secret’s that concentrate on for adjusted EBITDA to succeed in practically $600 million in 2024, up from $432 million in 2023. SoFi continues to develop earnings at a quick clip as the brand new banking merchandise launched within the final couple of years are turning into revenue machines after reaching scale.

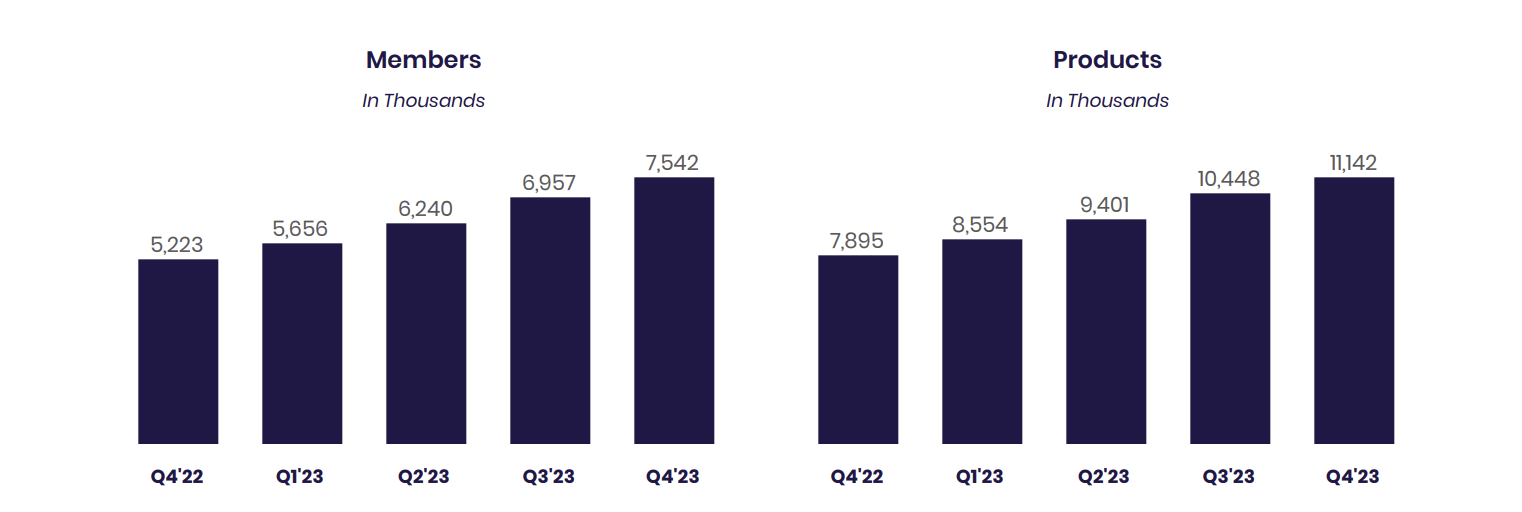

The corporate continues so as to add a considerable quantity of latest members, driving extra merchandise’ progress. These new members and the growth of the merchandise utilized by present members will drive progress for years forward.

Supply: SoFi This fall’23 earnings launch

SoFi added 585K new members through the quarter for 44% progress. These members added 695K new merchandise for 41% progress. The corporate grew merchandise by 110K greater than members in an indication of how members are including greater than the unique product.

The corporate does not even information to a robust lending phase push on account of dire financial steerage. SoFi set forth these weak financial metrics for 2024:

- Contraction in GDP in 2024

- Improve in unemployment to greater than 5%

- Continuation of unsure capital markets exercise and continued normalization of client credit score

- Assuming 4 fee cuts with Fed funds fee reaching ~4.5% by This fall 2024.

The lending phase is just forecast to generate as much as 95% of the revenues produced in 2023 on account of a company need to carry again lending actions beneath demand with the expectation for a recession. The entire progress is tied to the Monetary Companies enterprise and Tech platform targets at rising a mixed 50% throughout 2024 resulting in ~$400 million in income progress in comparison with practically $800 million price of revenues in 2023.

The truth is probably going that SoFi exceeds the steerage. Whereas the corporate is barely detrimental on the lending phase, the corporate is just now ramping up mortgage lending and the coed mortgage lending market is not absolutely again to pre-Covid ranges but.

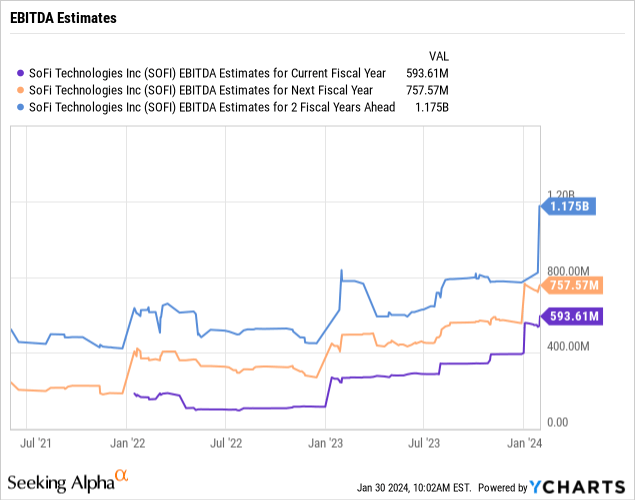

As talked about above, the inventory has a market cap of solely $9 billion, whereas SoFi guided to just about $600 million of adjusted EBITDA (earnings) in 2024. The consensus analyst estimates are up at $756 million in 2025 suggesting extra upside subsequent yr.

Assuming a brand new 2025 adjusted EBITDA goal of $750 million, the inventory solely trades at 12x ahead estimates. As soon as going again to the unique 2023 EBITDA target of $270 million, SoFi probably smashes the 2024 estimates, once more offering substantial upside to the 2025 estimates.

The fintech had initially guided to EBITDA numbers hitting nearly $1.5 billion by 2025 earlier than among the pupil mortgage moratoriums and the additional spending on Monetary Companies. In essence, the massive hole in EBITDA numbers are prone to be closed over the following few years, all whereas an investor can truly get the inventory no less than $1 cheaper now than when the SPAC deal was agreed to with these monetary targets.

Solely final July, SoFi soared to just about $12 following the large Q2’23 beat. Sarcastically, the inventory ended up falling beneath $7 by mid-November regardless of the fintech guiding to a 2023 adjusted EBITDA on the time of $338 million and really hitting $432 million, or 28% greater.

The inventory market is oddly not buying and selling shares primarily based on precise outcomes, as usually an organization beating targets by 28% over the course of 6 months would truly commerce vastly greater. SoFi beats numbers and traders promote the inventory off.

The widespread fears over the following few months might be enamel gnashing over the shortage of Lending Section progress. The market will try to persuade traders the expansion story is over right here. In actuality, decrease rates of interest will compress revenues, however SoFi might be much more worthwhile going ahead. SoFi guided to annualized progress charges of 20% to 25% by means of 2026 and the market is not valuing the inventory for any progress forward.

Takeaway

The important thing investor takeaway is that the market stays too detrimental, with SoFi buying and selling with a restricted market cap compared to the company progress over the previous couple of years as a public firm. Much more superb, SoFi seems far too detrimental with forecasts for GDP declines and unemployment surging to five% offering potential upside with a lift in lending when the detrimental financial view modifications.

Both means, SoFi Applied sciences, Inc. inventory trades at solely 12x adjusted EBITDA earnings for 2025. Contemplating the fintech has always beat inside monetary targets and the constant sturdy progress charges, SoFi should not commerce at a a number of far beneath the probably conservative progress charges.