jetcityimage

Funding Thesis

In my article published September 29, 2021, I wrote,

At present share worth SpartanNash Firm (NASDAQ:SPTN) affords a gorgeous 3.79% dividend yield. The present P/E ratio of 9.29 is beneath its historic ranges of round 10.0 to 10.5. Sadly, SA analysts’ EPS estimates point out a decline in EPS via finish of 2023, so any change in P/E ratio is extra prone to be a lower than a rise. With a prospect for declining EPS and declining P/E ratio inflicting additional share worth declines, whole returns via finish of 2023 could possibly be detrimental, regardless of the dividend yield. I imagine there’ll possible be alternatives within the fourth quarter for decrease inventory costs throughout the board, together with SpartanNash, as I imagine a market correction is overdue. At a decrease share worth the dividend yield must be increased and the danger of share worth decline decrease, at which time SpartanNash would possibly come into purchase vary.

At market shut on February 23, 2024, the SpartanNash share worth was down 5.85% on the value at date of the abovementioned article, and the dividend yield had elevated from 3.79% to 4.11%. Per Looking for Alpha Premium, whole return over this era was 1.37% because of the dividend receipts exceeding the autumn within the share worth.

I got down to discover if the decrease share worth and the upper dividend yield would now justify an improve to a Purchase score. Sadly, Desk A beneath reveals some discouraging developments.

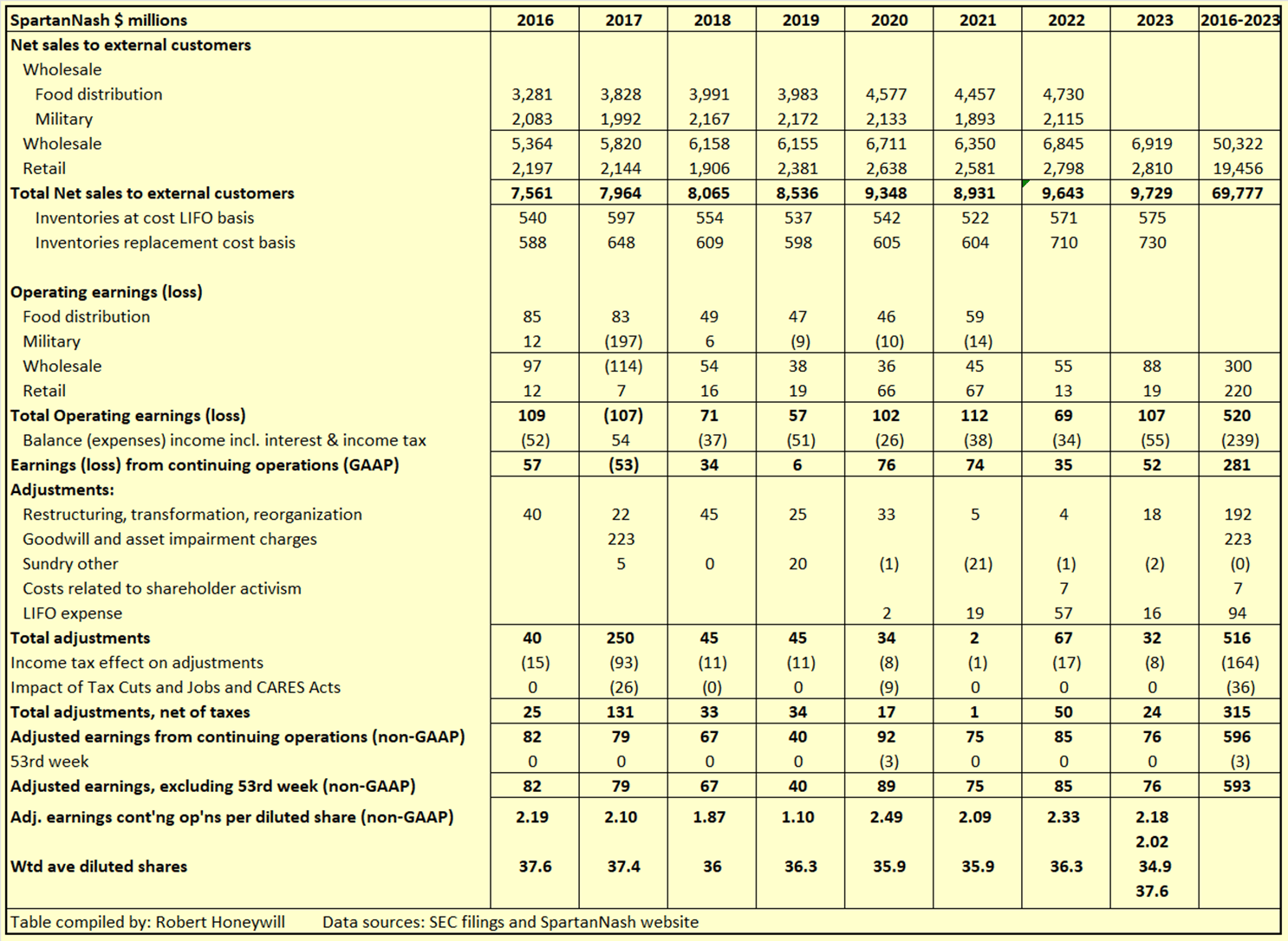

Desk A

SEC filings and SpartanNash web site

Feedback on Desk A –

- GAAP earnings of $52 million for 2023 are beneath 2016 degree of $57 million.

- GAAP earnings within the intervening years common ~$29 million per yr.

- Adjusted non-GAAP earnings of $76 million for 2023 are beneath 2016 degree of $82 million.

- Adjusted non-GAAP earnings within the intervening years common ~$73 million per yr, beneath 2016 degree.

- Expenditures of $182 million over the 8-year interval on restructuring, transformation, and reorganization ought to have resulted in enhancements in Adjusted non-GAAP earnings, however this isn’t the case.

- Recurrently recurring Restructuring, transformation, and reorganization bills seem like a traditional a part of operations, which raises the query whether or not they can legitimately be added again to normalize the outcome.

- The add again of LIFO expense within the calculation of Adjusted non-GAAP earnings is solely inappropriate. That is an try to incorporate in adjusted earnings the one off features on the worth of inventories as a consequence of worth inflation. LIFO accounting ensures the present worth of products offered is mirrored in value of products offered. Subsequently, GAAP outcomes primarily based on LIFO accounting already replicate the “true” underlying value of products offered and no adjustment is required to normalize the outcome for non-GAAP functions.

- Adjusted non-GAAP EPS of $2.18 for 2023 has the advantage of a discount of two.7 million in share depend since 2016. With out this the outcome can be an EPS of $2.02, in comparison with $2.19 for 2016. The discount in share depend is just not growing EPS, merely stopping the EPS from reducing additional.

- The discount in share depend has not been achieved by utilizing earnings in extra of dividends to repurchase shares. Stability sheet evaluation additional beneath exhibits funding of repurchases of shares is completely attributable to elevated borrowings.

- Transparency has been decreased by the choice in 2022 to now not individually report phase working earnings (losses) for Navy, at a time when Navy was exhibiting growing working losses yr by yr.

Based mostly on the foregoing overview, and my detailed evaluation beneath, I’m inclined to downgrade SpartanNash from Maintain to Promote. Alternatively, if the management enthusiasm displayed in the Q4-2023 earnings call and presentation might be translated into actual progress in gross sales and earnings, that will possible end in a rise within the P/E ratio which along with increased EPS might drive good share worth features above the present depressed share worth. Add to that the over 4% dividend yield, and a seamless Maintain suggestion, with a wait and see strategy is probably going essentially the most applicable plan of action.

My regular detailed structured monetary evaluation follows beneath.

Trying For Share Market Mispricing Of Shares

What I am primarily searching for listed here are situations of market mispricing of shares as a consequence of distortions to most of the regular statistics used for screening shares for purchase/maintain/promote choices.

I imagine the reply is to check projections, primarily based on analysts’ estimates out to the top of 2024 or later, to previous efficiency. Summarized in Tables 1 and a couple of beneath are the outcomes of compiling and analyzing the info on this foundation.

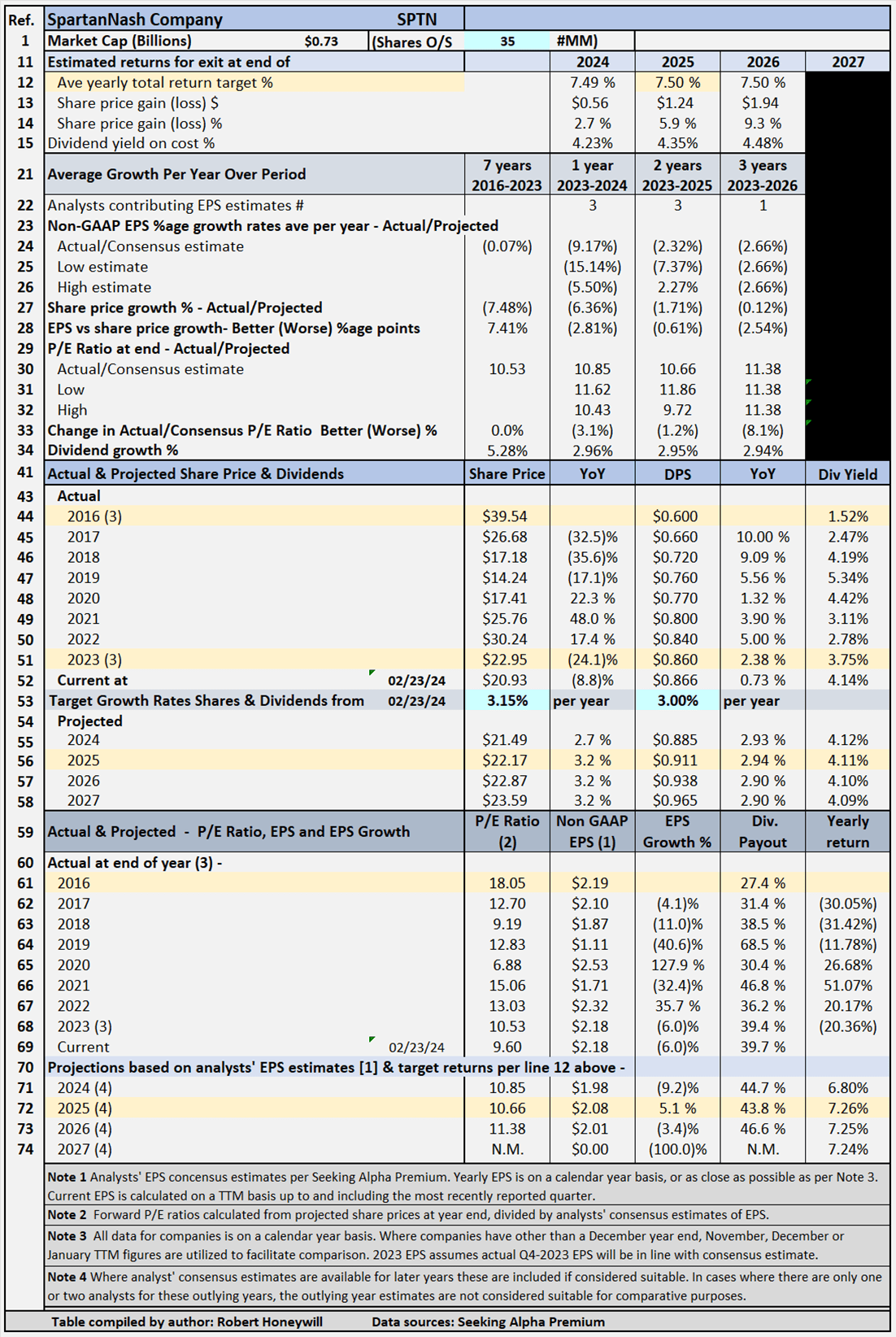

Desk 1 – Detailed Monetary Historical past And Projections

Looking for Alpha Premium

Feedback on Desk 1 –

Efficiency over previous 7 years – Desk 1 exhibits SpartanNash non-GAAP EPS has barely modified over the previous seven years, from $2.19 for 2016 to $2.18 for 2023. Over the identical interval, SpartanNash’s inventory worth declined by a median (7.48)% per yr, from $39.54 on the finish of 2016 to $22.95 on the finish of 2023. That is primarily as a consequence of a lower within the P/E a number of from 18.05 on the finish of 2016 to 10.53 on the finish of 2023. Regardless of the shortage of EPS progress, dividend per share has grown by a median yearly charge of 5.28% from $0.60 on the finish of 2016 to $0.86 on the finish of 2023. This dividend progress charge of 5.28% per yr, regardless of the absence of EPS progress, has resulted in a rise within the dividend payout ratio from 27.4% for 2016 to a nonetheless modest 39.4% on the finish of 2023. The decline within the share worth over the previous seven years has been the first cause for the dividend yield growing by round 2.5 occasions, from 1.52% on the finish of 2016 to three.75% at finish of 2023. Additional decline within the share worth via February 23, 2024 has resulted within the dividend yield additional growing to 4.11%.

Modeling for focused charges of return – Desk 1 paperwork historic information from 2016 to 2019, together with share costs, P/E ratios, EPS and DPS, and EPS and DPS progress charges. The desk additionally consists of estimates out to 2026 for share costs, P/E ratios, EPS and DPS, and EPS and DPS progress charges (word – whereas estimates are proven for analysts’ EPS estimates out to 2024, 2025 and 2026 the place accessible, estimates do are likely to develop into much less dependable, the additional out the estimates go. These estimates are solely thought of sufficiently dependable if there are at the very least three analysts’ contributing estimates for the yr in query). Desk 1 permits modeling for goal whole charges of return. Within the case proven above, the goal set for whole charge of return is 7.5% per yr via the top of 2025 (see line 12), primarily based on shopping for on the February 23, 2024 closing share worth degree. As famous above, estimates develop into much less dependable within the later years. I’ve determined to enter a goal return primarily based on 2025 yr, which has EPS estimates from three analysts. The desk exhibits to attain the 7.5% return, the required common yearly share worth progress charge from February 23, 2024 via December 31, 2025, is 3.15% (line 53). Dividends and dividend progress account for the stability of the goal 7.5% whole return.

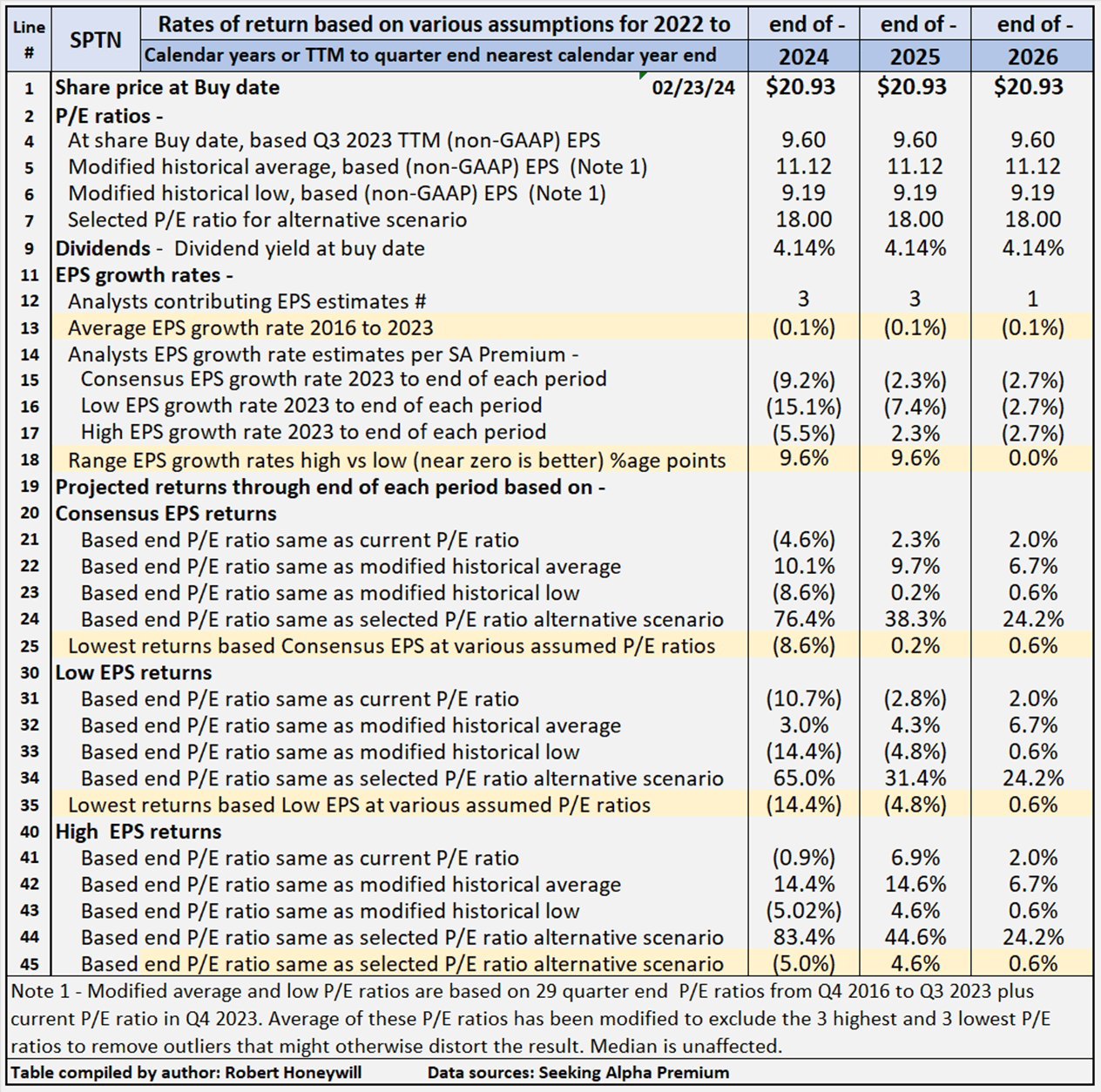

SpartanNash’s Projected Returns Based mostly On Chosen Historic P/E Ratios Via Finish Of 2025

Desk 2 beneath gives extra eventualities projecting potential returns primarily based on choose historic P/E ratios and analysts’ consensus, low, and excessive EPS estimates per Looking for Alpha Premium via finish of 2025.

Desk 2 – Abstract of related projections SpartanNash

Looking for Alpha Premium

Desk 2 gives comparative information for purchasing at closing share worth on February 23, 2024 and holding via the top of yr 2024 to 2026 (the place estimates can be found). There’s a whole of twelve valuation eventualities for annually, comprised of three EPS estimates (SA Premium analysts’ consensus, high and low) throughout 4 totally different P/E ratio estimates, primarily based on historic information, plus a fourth P/E ratio chosen to supply an alternate state of affairs. SpartanNash’s P/E ratio is presently 9.60, which is nicely beneath the historic common P/E ratio of 11.12. Desk 2 exhibits potential returns from an funding in shares of the corporate throughout the vary of P/E ratios This evaluation, from hereon, assumes an investor shopping for SpartanNash shares at this time can be ready to carry via 2025, if needed, to attain their return aims. Feedback on contents of Desk 2, for the interval to 2025 column comply with.

Consensus, high and low EPS estimates

All EPS estimates are primarily based on analysts’ consensus, high and low estimates per SA Premium. That is designed to supply a variety of valuation estimates starting from low to most certainly, to excessive primarily based on analysts’ assessments. I might generate my very own estimates, however these would possible fall inside the similar vary and wouldn’t add to the worth of the train. That is notably so in respect of well-established companies resembling SpartanNash. I imagine the “low” estimates must be thought of essential. It is prudent to handle danger by understanding the potential worst-case eventualities from no matter trigger.

Different P/E ratios utilized in eventualities

- The precise P/E ratios on the share purchase date are primarily based on precise non-GAAP EPS for FY-2023.

- A modified common P/E ratio primarily based on 30 quarter-end P/E ratios from This autumn 2016 to This autumn 2023 and present P/E ratio in Q1 2024. The common of those P/E ratios has been modified to exclude the three highest and three lowest to take away outliers which may in any other case distort the outcome.

- A modified low P/E ratio was calculated utilizing the identical information set used for calculating the modified common P/E ratio, and calculated on an analogous foundation, with the three highest and lowest P/E ratios excluded.

- A median P/E ratio is calculated utilizing the identical information set used for calculating the modified common P/E ratio. After all, the median is similar whether or not or not the three highest and lowest P/E ratios are excluded. Within the case of SpartanNash, I’ve chosen to make use of an assumed P/E ratio of 18.0 rather than the historic median of 11.01 (much like the typical). I’ve completed this to supply an concept of the affect on returns of the a number of more and more considerably above the current degree and the historic common. The chosen P/E a number of of 18.0 compares to the sector median of 18.02 for PE Non-GAAP [FWD], per Looking for Alpha Premium metrics.

Reliability of EPS estimates (line 18)

Line 18 exhibits the vary between excessive and low EPS estimates. The broader the vary, the larger disagreement there may be between essentially the most optimistic and essentially the most pessimistic analysts, which tends to recommend larger uncertainty within the estimates. There are 3 analysts masking SpartanNash via finish of 2025. In my expertise, a variety of 9.6 proportion factors distinction in EPS progress estimates amongst analysts is excessive, suggesting a substantial diploma of uncertainty, and thus elevated unreliability.

Projected Returns (strains 18 to 39)

Traces 25, 35 and 45 present, at a variety of historic P/E ratio ranges, SpartanNash is conservatively indicated to return between detrimental (4.8)% and constructive 4.6% common per yr via the top of 2025. The detrimental (4.8)% return relies on analysts’ low EPS estimates and the 4.6% on their excessive EPS estimates, with a 0.2% return primarily based on consensus estimates. These are the bottom of the returns below the consensus, high and low EPS eventualities and are primarily based on the P/E ratio remaining on the present degree. On the excessive finish of the projected returns for SpartanNash, the indicative returns vary from 31.4% to 44.6%, with consensus 38.3%. These returns would require the P/E ratio to extend from the current 9.60 to the ~18.05 at finish of 2016. Coincidentally, SpartanNash’s sector median P/E non-GAAP [FWD] ratio is eighteen.02 per SA Premium. Nevertheless, sector median proportion progress charges for Income, EBITDA, and EPS are within the mid to excessive single digits. Until SpartanNash can present progress in these areas, an 18.0 P/E ratio appears to be like like an inconceivable dream. If the P/E ratio have been to extend to the historic common of 11.12 by finish of 2025, indicative returns can be within the vary of 4.3% to 14.6%, with consensus 9.7%. The distinction between greatest and worst instances is a sign of the diploma of certainty in analysts’ estimates.

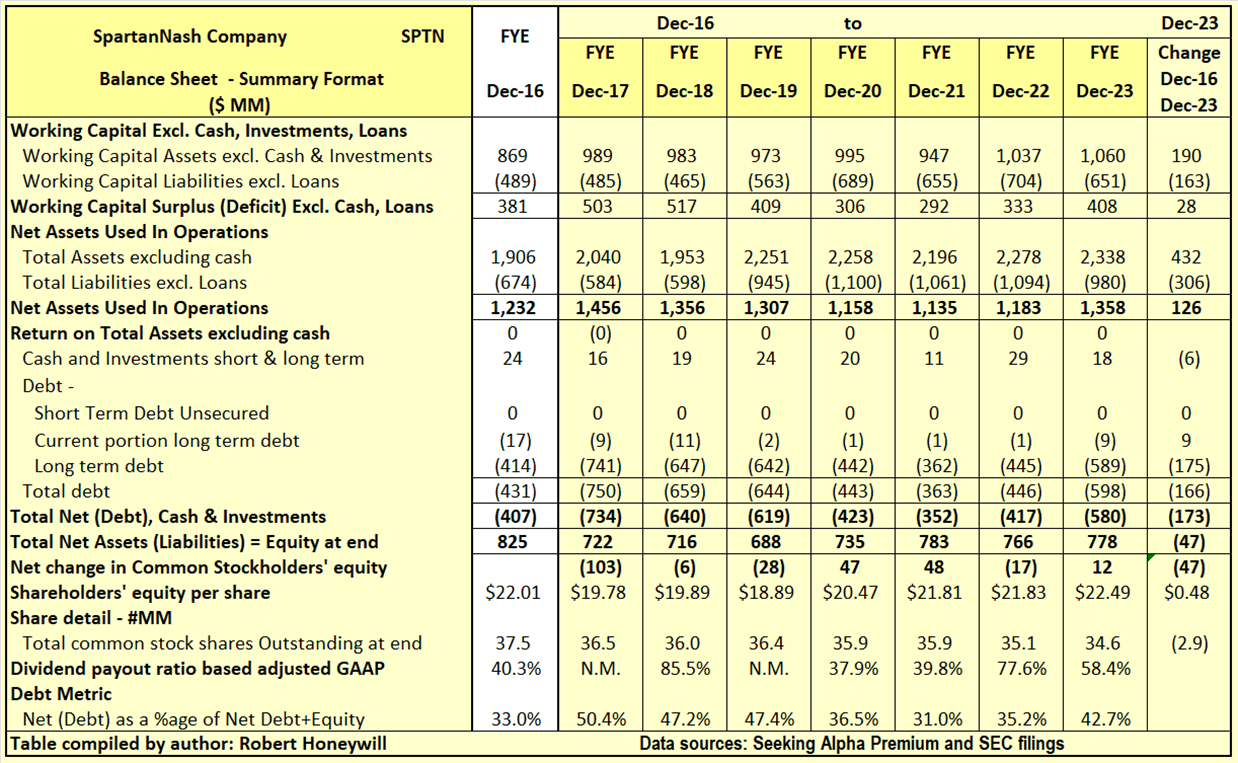

Checking SpartanNash’ “Equity Bucket”

Desk 3.1 SpartanNash Stability Sheet – Abstract Format

Looking for Alpha Premium & SEC filings

Over the seven years from yr finish 2016 to the top of 2023, SpartanNash’s shareholders’ fairness has decreased by $47 million. This discount is mirrored as a rise in debt internet of money of $173 million offset by a rise of $126 million in internet belongings utilized in operations. Excellent shares decreased by 2.9 million from 37.5 million to 34.6 million, over the interval, as a consequence of share repurchases partially offset by shares issued for inventory compensation. Internet debt as a proportion of internet debt plus fairness elevated from 33.0% on the finish of 2016 to 42.7% on the finish of 2023. The $47 million lower in shareholders’ fairness during the last seven years is analyzed in Desk 3.2 beneath.

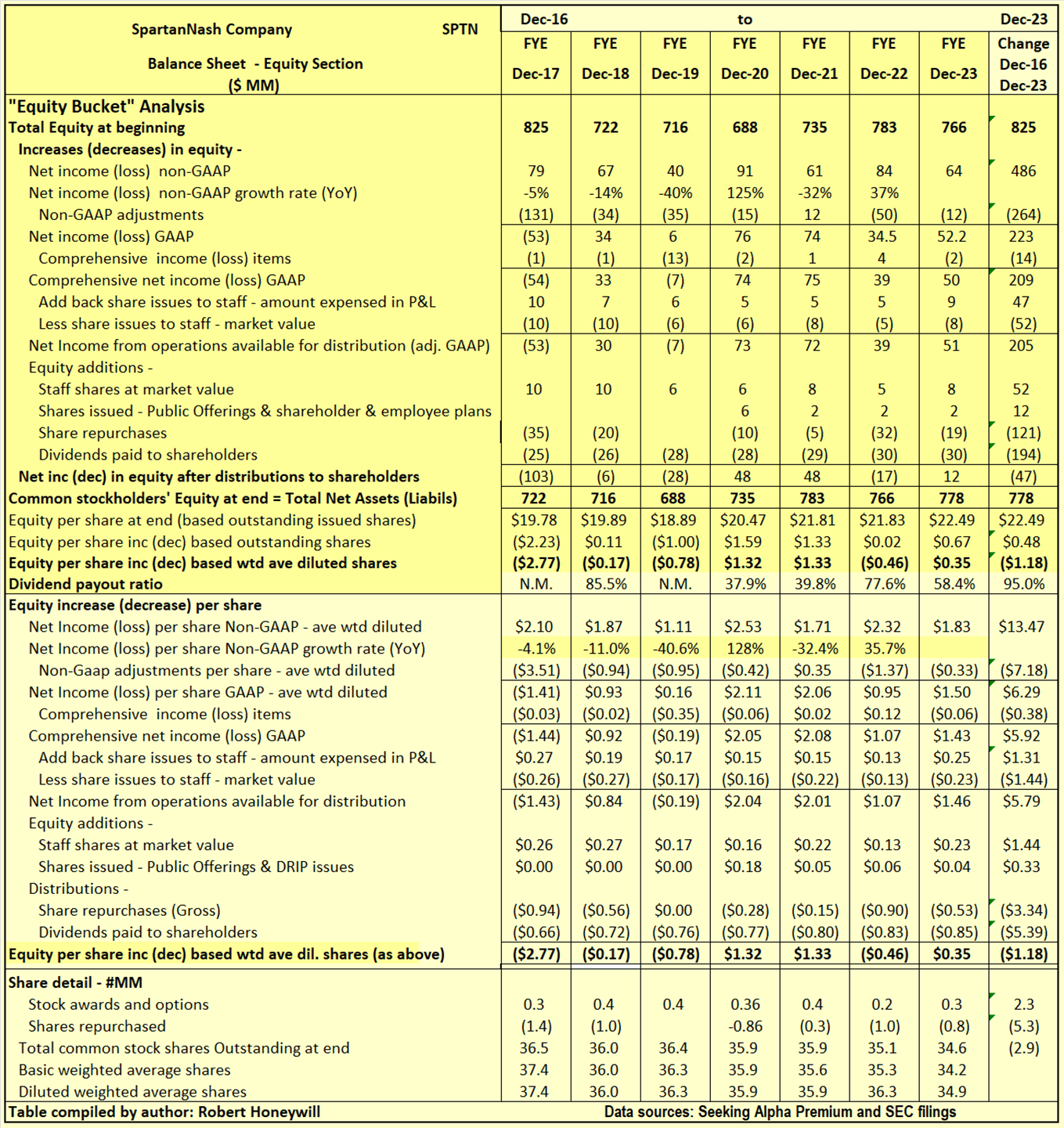

Desk 3.2 SpartanNash Stability Sheet – Fairness Part

Looking for Alpha Premium & SEC filings

I usually discover firms report earnings that ought to move into and enhance shareholders’ fairness. However usually the rise in shareholders’ fairness doesn’t materialize. Additionally, there might be distributions out of fairness that don’t profit shareholders. Therefore, the time period “leaky equity bucket.” That is occurring with SpartanNash.

Explanatory feedback on Desk 3.2 for the interval finish FY-2016 to finish FY-2023.

- Reported internet earnings (non-GAAP) over the 7-year interval totals to $486 million, equal to diluted internet earnings per share of $13.47.

- Over the 7-year interval, the non-GAAP internet earnings excludes $264 million (EPS impact $7.18) of things thought to be uncommon or of a non-recurring nature with a purpose to higher present the underlying profitability of SpartanNash.

- Different complete earnings consists of things like international alternate translation changes in respect to buildings, plant, and different services situated abroad and modifications in valuation of belongings within the pension fund – these aren’t handed via internet earnings as they fluctuate with out affecting operations and might simply reverse in a following interval. Nonetheless, they do affect on the worth of shareholders’ fairness at any time limit. For SpartanNash, this stuff totaled $14 million loss (EPS impact $0.38 loss).

- Quantity taken up in fairness in relation to shares issued to employees over the 7-years is $47 million. This compares to an estimated market worth of $52 million for these shares, leading to an overstatement of internet earnings by $5 million, which isn’t materials within the context of GAAP internet earnings of $223 million.

- By the point we take the above talked about objects into consideration, we discover, over the 7-year interval, the reported non-GAAP EPS of $13.47 ($486 million) has decreased to $5.79 ($205 million), added to funds from operations accessible for distribution to shareholders.

- Dividends of $194 million, and share repurchases of $121 million have been larger than the $205 million from operations, leading to a shortfall in internet earnings from operations after distributions of $110 million.

- The shortfall of $110 million from operations was offset by the $52 million enhance in fairness due problems with shares to employees, and $12 million from rights points, ensuing within the lower of $47 million in shareholders’ funds per Desk 3.1 above.

SpartanNash: Abstract and Conclusions

Desk 1 additional above exhibits, to ensure that SpartanNash to supply whole returns of seven.5% via finish of 2025, not solely should analysts’ consensus EPS estimates be met, however the P/E ratio should enhance from the present 9.60 to 10.66. A P/E ratio of 10.66 is beneath historic common P/E a number of ranges of round 11.12 (see Desk 2). Nevertheless, given SA analysts’ consensus EPS estimates are for EPS to additional decline via finish of 2025, a rise in P/E ratio seems unlikely. The key difficulty for SpartanNash is a scarcity of progress, and no certainty of future progress. On the similar time, the over 4% dividend yield and administration’s confidence in reaching future progress, point out a Maintain with a wait and see strategy is probably going applicable.