onurdongel

Funding Rundown

There was a notable transfer from extra conventional funding areas like utilities and industrials into tech firms, not solely in the previous few quarters however over the past decade, one thing that I feel each investor can agree on. I wish to spotlight with this text on Spire Inc. (NYSE:SR) that there are a whole lot of alternatives that open up when this pattern occurs. An organization like SR, which has a really giant asset base and trades at a few of its lowest ranges in recent times, makes it an awesome shopping for alternative. A yield of 5% and constant bottom-line progress make SR in my eyes the spine of an organization for a portfolio.

Utility firms typically accumulate a whole lot of debt throughout their years of operations, however I do not suppose they need to be confused with a major quantity of danger. An organization like SR is in an awesome place to proceed driving larger and better money flows and earnings to pay down debt, they usually are typically fairly dependable as nicely.

Firm Segments

SR works with the acquisition, distribution, and sale of pure gasoline to a various vary of shoppers throughout the USA. The corporate operates by means of three key segments: Fuel Utility, Fuel Advertising and marketing, and Midstream. SR is devoted to offering pure gasoline to residential, industrial, and industrial customers. Furthermore, it performs a task in advertising pure gasoline companies, together with taking part within the transportation and storage of pure gasoline. Moreover, SR is engaged in propane operations, together with propane pipeline actions, danger administration, and numerous associated ventures.

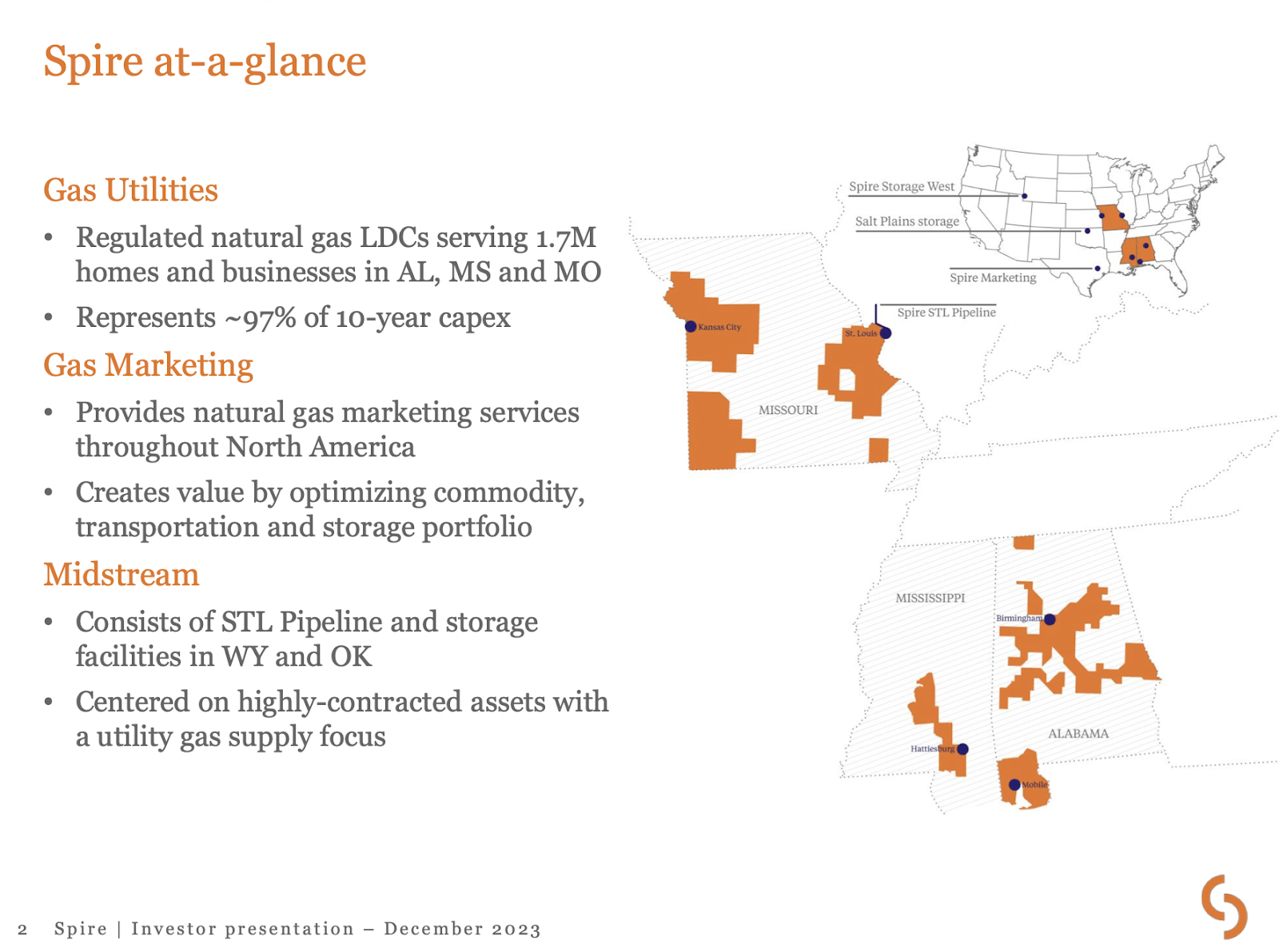

Firm Overview (Investor Presentation)

Throughout its years of operation which spans again to 1857, SR has diversified its operations and operates nowadays in a number of states, like Alabama, Mississippi, and Missouri. Most prospects are positioned in Missouri with over 1.2 million making up a majority of the full 1.7 million whole prospects. The corporate is working pipelines which means that a lot of the worth the corporate generates comes from current infrastructure then from manufacturing one thing after which promoting it. The pipelines span 61.200 miles in whole. 90% of the revenues come from the regulated gasoline utilities section of the enterprise while the remainder is made up of selling and a few midstream operations. One other gasoline firm that I’ve covered is Southwest Fuel Holdings (SWX) which has seen comparable buying and selling patterns as SR, which means missing progress as funding corporations appear to lean extra in the direction of progress firms now as a substitute after news of fee cuts this yr got here out.

Earnings Highlights

Revenue Assertion (Earnings Report)

Wanting on the last report by the corporate there have been noticeable enhancements within the revenues YoY, maybe not the final quarter, however for the complete fiscal yr of 2023, it rose by over 20%. This places the corporate at an FWD p/s of simply 1.25, a virtually 30% low cost to its 5-year historic a number of of 1.74. Wanting additional on the earnings assertion, see that the underside line fell barely YoY. The first trigger for this appears to have been larger curiosity bills and a slight dilution YoY of about 1%. I feel this will probably be brief lived although and for margins to stabilise within the later a part of 2024 and starting of 2025 as we see the rates of interest develop additional. The final report was launched on November 16 and the inventory value rose steadily after for a couple of weeks however is all the way down to the identical stage. The 52-week excessive for SR is at $75 and it seems the next report will come on January 30. I feel that if SR posts sturdy numbers then and raises outlooks for the yr, the inventory value will rally. It has been in such a gradual decline and reversing that may solely be attainable if the corporate posts sturdy outcomes.

Valuation (Searching for Alpha)

The first approach that SR drives revenues is from its pipeline which is its asset base to a majority. Revenues are typically considerably secure over the long run with some fluctuations quarter to quarter relying on how costs develop and asset depreciation appears. Regardless of the property rising practically 8% YoY since 2021 the corporate trades at a few of its lowest multiples, a 37% low cost based mostly on p/s to the utilities sector. Although there are some dangers going through the corporate I feel a good a number of right here can be round 1.7 no less than. I argue that that is justified due to the soundness of the income technology that SR and the way dependable they’ve been the previous decade, compounding at 10.12%. With a 1.7 a number of, we get a value goal of $91 proper now with a income per share estimate of $51 per share for 2024. I feel that for 2024 SR might very realistically put up comparable income as to 2023, with maybe extra progress to the underside line, relying on how the rates of interest lower. However with that stated, I feel 2024 will see SR posting simply shy of $2.7 billion in revenues.

Let’s examine SR a bit extra to a detailed peer as nicely which might be ONE Fuel, Inc. (OGS). These firms are very comparable on a market cap foundation, each between $3 – $3.3 billion. The inventory value has, nonetheless, carried out worse for GGS within the final 12 months, down over 22%, with SR down solely 17%. Yield-wise sensible SR is the winner right here with 5.1% in comparison with 4.4% for GGS. The place I favor SR and suppose it is the higher possibility is the valuation firstly, right here SR trades at decrease multiples than GGS, the p/e for instance 13.4 in comparison with 14.2 for GGS. Traditionally SR has additionally been the superior firm, rising the highest line at a CAGR of 10.12 within the final decade and GGS at simply 4.91%. I feel SR has the higher basis for higher and superior progress within the subsequent decade which is why it is my most popular selection of the 2.

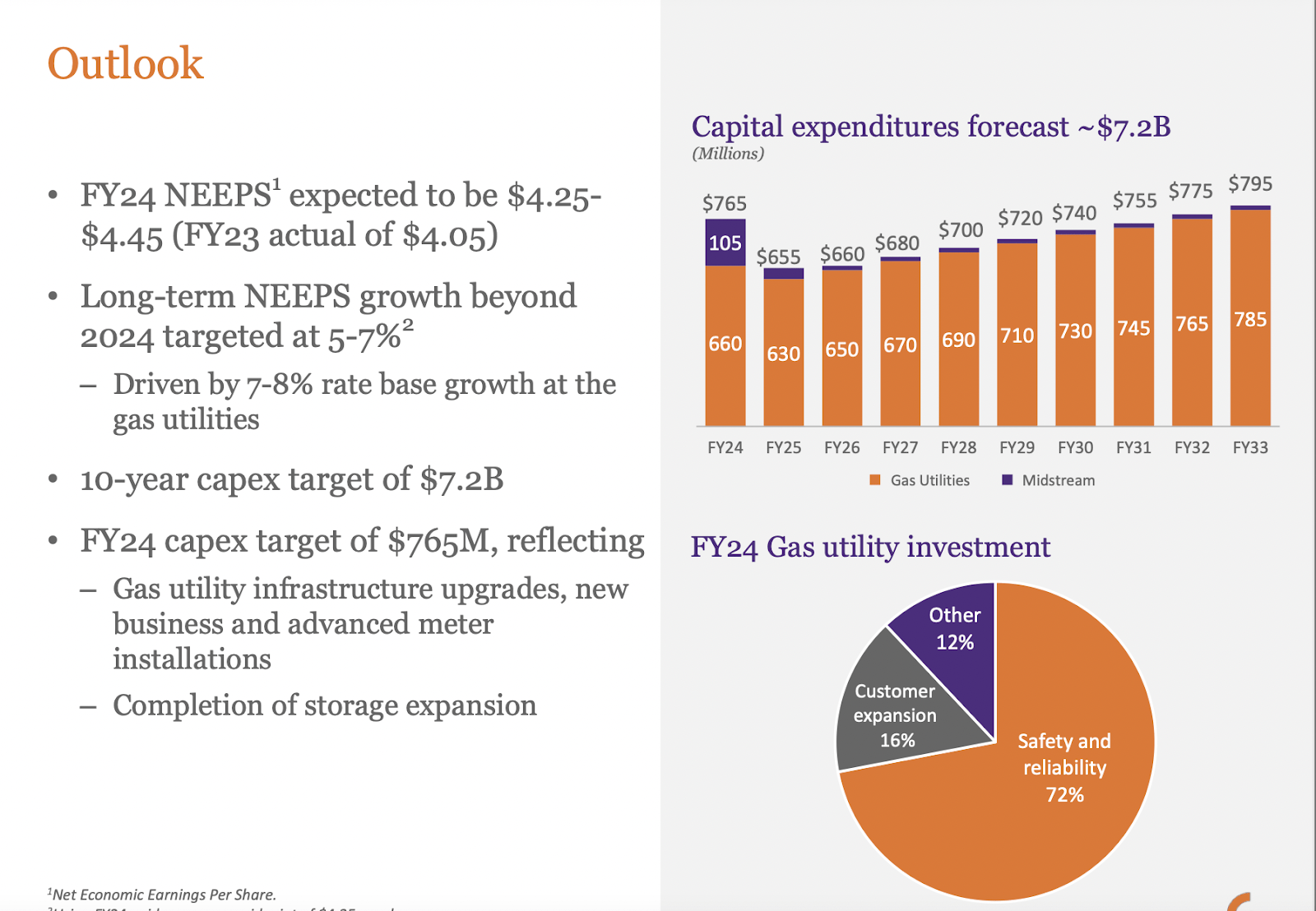

Firm Outlook (Investor Presentation)

The corporate does forecast a reasonably sturdy 5 – 7% long-term NEEPS progress fee which is pushed by a 7 – 8% fee base progress for the gasoline utilities, the biggest section of the enterprise. This outlook goes in step with the estimated revenues I’ve for 2024 for SR. With that value goal of $91, we additionally obtain an upside of roughly 50% proper now and the 5% divine yields get us to 55% within the subsequent 12 months. I feel it isn’t unreasonable that we get fairly excessive up on that forecast, however a dependable 55% return in 12 months would get each single funding agency on the market to put money into SR proper now. I feel the case will be made although that SR presents a really compelling likelihood that it might outperform the broader markets within the subsequent 12 months, which implies I’m additionally ranking it a purchase now.

Dangers

A notable danger going through SR stems from environmental variability, each by way of local weather and pure gasoline prices. The hotter climate contributes to elevated depreciation on property, consequently elevating capital expenditures and upkeep prices. This extended affect on earnings might necessitate a discount in shareholder-friendly initiatives, similar to buybacks and dividends, to make sure continued operational effectivity. The US continues to see shifting climate patterns and I feel is affordable to imagine that within the subsequent decade, the depreciation for SR property will speed up because of this.

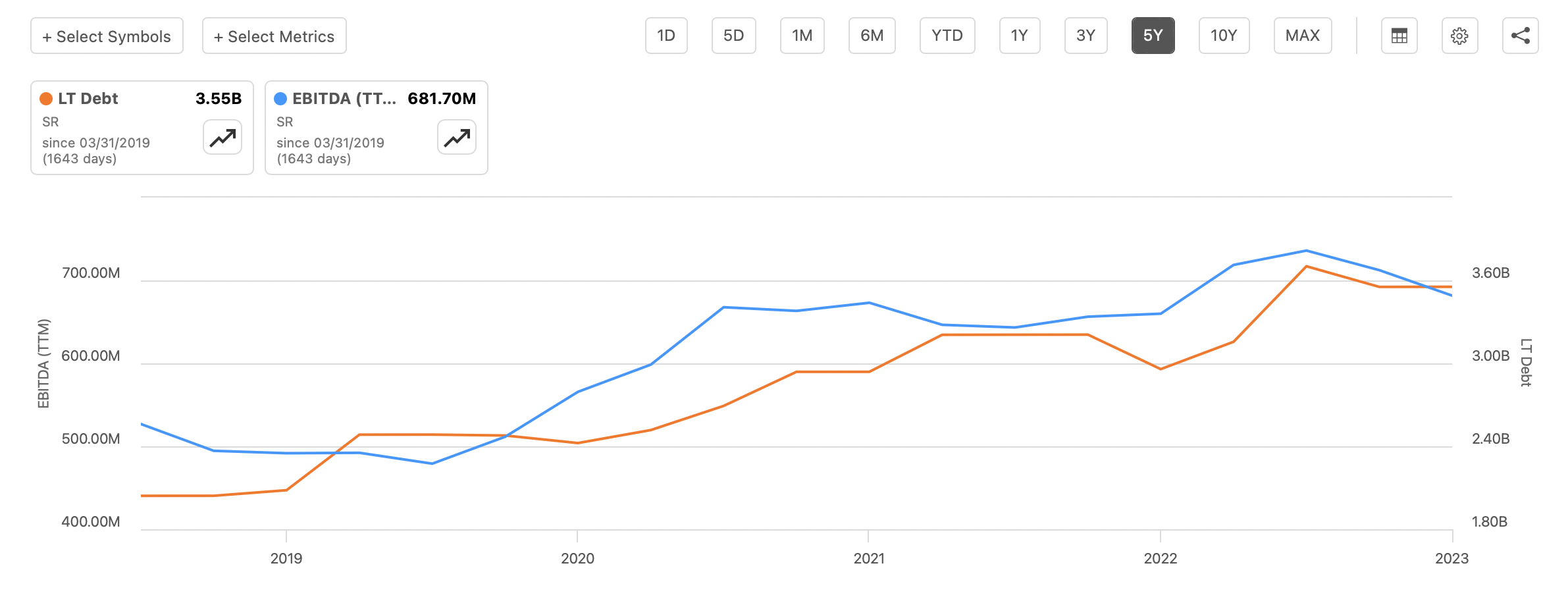

Debt and EBITDA (Searching for Alpha)

Extra of a brief to medium danger is the rising rates of interest within the US which is placing stress on the earnings of SR. The corporate has at all times had a whole lot of debt on its steadiness sheet, and I do not suppose it is a main danger for traders. The leverage between EBITDA and long-term debt is roughly 5, and with such constant EBITDA technology, I feel larger leverage isn’t any problem right here. The debt ranges are at slightly below $3 billion proper now however with the chart clearly showcasing the EBITDA having the ability to sustain it stays a low danger to me. The TTM EBITDA is $681 million however has grown rapidly from the $448 million it was again in 2018. That is a 52% enhance in simply 5 years. The issue arises extra in that for the brief time period SR won’t have the ability to make as aggressive acquisitions and expansions as earlier than, which could justify a decrease valuation like now we have seen for the final 12 months for the inventory. This danger additionally ties into the primary one I discussed with shifting climate circumstances, doubtlessly resulting in larger depreciation on property. If SR is already sitting with a whole lot of debt and now faces excessive upkeep bills it would result in a maintain on elevating the dividend as capital is required elsewhere.

Last Phrases

Utilities firms have struggled the previous 12 months and SR isn’t any totally different, down practically 20% the previous 12 months. When digging deeper into the corporate although it is revealed that the asset base and areas of operations showcase a sturdy enterprise mannequin that leaves loads of worth for traders proper now. The valuation has crept all the way down to historic lows and with a yield previous 5%, it is onerous to withstand shopping for into SR at these value factors. My value goal signifies {that a} important outperformance may be attainable within the subsequent 12 months and that leads me to fee the corporate a purchase proper now.