Monty Rakusen/DigitalVision through Getty Pictures

Introduction

Within the high-stakes enviornment of aerospace manufacturing, Spirit AeroSystems (NYSE:SPR) stands as a case examine in navigating complicated monetary and operational challenges. As we dissect Spirit AeroSystems’ monetary statements, an image of an organization at a crossroads emerges. The erosion of gross revenue margins, a stability sheet reflecting a precarious mix of liquidity and substantial debt, and a inventory efficiency echoing investor skepticism, all paint an image of an organization in dire want of strategic recalibration. This evaluation goals to unpack the layers of Spirit AeroSystems’ monetary scenario, offering perception into the challenges it faces and the potential pathways it’d discover to navigate by this turbulent part. In doing so, we will even supply a perspective on funding methods within the context of Spirit AeroSystems’ present market place, evaluating the potential dangers and alternatives that lie forward for this key participant within the aerospace sector. We consider that SPR wants a big operational revamp and because of that we don’t see any risk-adjusted upside for fairness holders within the subsequent 12-24 months. We place a score of ‘Promote’ and a Value Goal of $18.

Navigating Monetary Turbulence: A Nearer Look

Spirit AeroSystems’ monetary journey is akin to navigating a storm. The income of $1.43 billion, whereas substantial, is overshadowed by an excellent increased price of income at $1.49 billion. This imbalance has led to a notable web lack of $204 million, portray an image of operational and monetary inefficiency. The damaging EPS of -$1.94, albeit a slight enchancment from the earlier quarter’s -$1.96, is a stark reminder of the corporate’s struggles with profitability. This steady development of losses raises crimson flags in regards to the firm’s operational mannequin, price administration, and market adaptability.

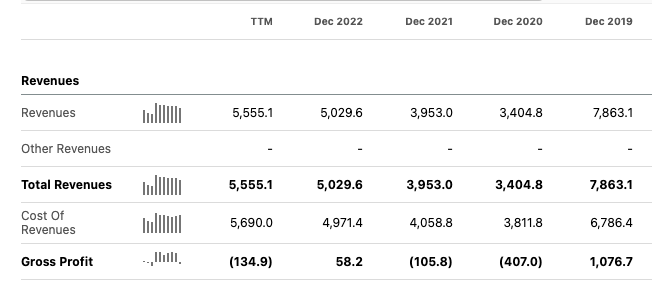

Gross Revenue SPR (In search of Alpha)

SPR’s earnings statements reveals that the corporate is grappling with a narrowing gross revenue margin. This challenge stems primarily from the escalating prices of products bought (COGS), that are outpacing income progress. In a sector like aerospace, the place manufacturing and materials prices might be excessive, such a development is especially regarding. This imbalance between revenues and COGS suggests inefficiencies in SPR’s manufacturing course of or maybe rising prices of supplies and labor that the corporate has been unable to offset by its pricing methods. Add in labor issues and quality issues the operational challenges that SPR at the moment faces are certainly formidable. Consequently, this erosion of gross revenue margin places further strain on the corporate’s general monetary well being, limiting its potential to put money into progress alternatives or handle its present debt load successfully. Addressing these gross revenue challenges is essential for SPR, because it seeks to stabilize its monetary place and reassure traders of its potential for sustainable profitability within the extremely aggressive and capital-intensive aerospace trade.

The Dichotomy of the Steadiness Sheet: Delving Deeper

The stability sheet of Spirit AeroSystems is a juxtaposition of energy and vulnerability. On one hand, the corporate’s liquidity, marked by its $374 million in money and equivalents, offers a cushion in opposition to short-term monetary pressures. This liquidity is essential in enabling the corporate to handle its day-to-day operations with out the quick menace of money move insolvency.

Nonetheless, the opposite facet of the ledger presents a worrying situation. The corporate’s complete debt stands at an alarming $3.97 billion, with web debt of $3.59 billion. This excessive stage of indebtedness not solely places strain on the corporate’s future money flows but in addition raises questions on its long-term monetary sustainability. The damaging complete fairness of -$855 million is an additional indicator of previous struggles and accrued losses. This damaging fairness means that the corporate has been eroding its worth, doubtlessly diluting shareholder confidence and making it difficult to draw new funding.

This dichotomy within the stability sheet displays a crucial balancing act for the administration. On one hand, there’s a want to keep up enough liquidity to make sure operational continuity. On the opposite, the corporate should handle its substantial debt and damaging fairness to revive monetary well being and investor confidence.

To handle its monetary wants, Spirit AeroSystems intends to generate $200 million through the sale of its Class A common stock and an additional $200 million via convertible debt, set to mature on November 1, 2028. This choice underscores the corporate’s reliance on fairness financing within the wake of its current struggles.

Increasing on Inventory Efficiency and Investor Sentiment

Google

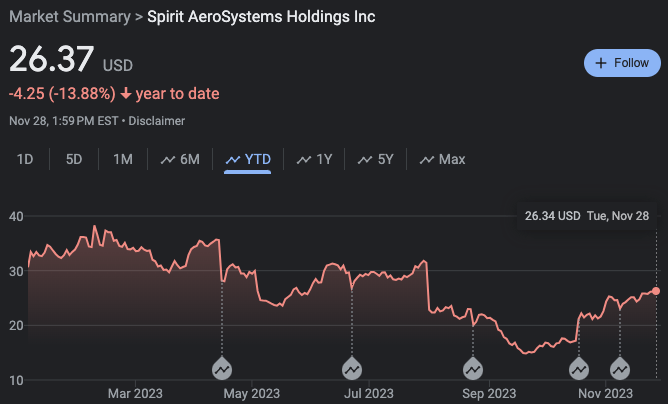

The inventory efficiency of Spirit AeroSystems serves as a direct reflection of investor sentiment and market confidence within the firm’s future. The numerous decline in its share worth to $26.35, a 14% drop YTD, is a transparent indicator of the market’s apprehension. With a low of ~$15 vary the information of a brand new Boeing contract is the one that has propelled them out of their 50% drop earlier within the yr. This decline is not only a response to the corporate’s monetary struggles, as outlined in its earnings experiences, but in addition a broader reflection of uncertainties inside the aerospace trade. Buyers are seemingly cautious of SPR’s potential to successfully handle its operational and monetary challenges, comparable to excessive prices and substantial debt, in an trade recognized for its volatility and cyclicality.

This skepticism is additional fueled by broader market tendencies and exterior financial components that affect the aerospace sector, together with fluctuating demand for air journey, shifts in protection spending, and the affect of worldwide financial circumstances.

Conclusion

Spirit AeroSystems’ journey by its present monetary and operational storm is one which calls for cautious scrutiny from traders. The corporate’s struggles to realize profitability, alongside its reliance on fairness dilution and exterior fundraising to remain afloat, are crimson flags. These points are compounded by administration instability, additional clouding the corporate’s future. Spirit’s important position within the U.S. aerospace trade suggests it may not fail outright, however this alone doesn’t assure a optimistic outlook for potential traders.

The corporate’s monetary statements reveal deep-rooted challenges. The constant incapability to generate a considerable gross revenue since 2019, which can’t be completely attributed to the COVID-19 pandemic, signifies systemic points in its operational mannequin. Even with new contracts, the shortage of serious gross revenue factors to inefficiencies that want addressing for any significant monetary turnaround.

Transferring ahead, Spirit AeroSystems would want to embark on a rigorous path of restructuring and strategic realignment to regain investor confidence and monetary stability. This might doubtless contain an intensive overhaul of its operational processes to handle inefficiencies, a strategic method to debt administration, and probably a reshaping of its administration staff to herald contemporary views and stability.

We assign a ‘Promote’ score to Spirit AeroSystems inventory with a goal worth of $18. At present, a number of potential catalysts may affect SPR’s market efficiency. These embrace securing new contracts, shifts in administration, the affect of fairness dilution, enhancements in gross margins, and a path to profitability. Nonetheless, given the corporate’s ongoing challenges, we anticipate that Spirit’s inventory will doubtless expertise lateral motion out there for the foreseeable future.

Our technique includes promoting cash-covered Places at roughly the $18 stage over the subsequent few quarters. This method displays a cautious stance, permitting us to capitalize on the corporate’s present market place whereas ready for indicators of considerable enchancment. We consider this methodology is prudent till SPR demonstrates a concrete restoration, each financially and operationally. Solely with clear proof of Spirit AeroSystems regaining a secure basis in these areas would we rethink our place and outlook on the inventory.