Funtap/iStock by way of Getty Pictures

US massive cap fairness valuations have moved again to their most excessive ranges on document barring the 1990-2000 and the 2021 peaks. Primarily based on a median of probably the most dependable valuation measures going again to 1991, the S&P500 trades at multiples constant with 10-year actual returns of round zero. With actual annual progress in fundamentals prone to be at the very least a proportion level slower than they’ve been traditionally on account of slower actual GDP progress, buyers ought to anticipate actual whole returns of -2.8% to -6.4%.

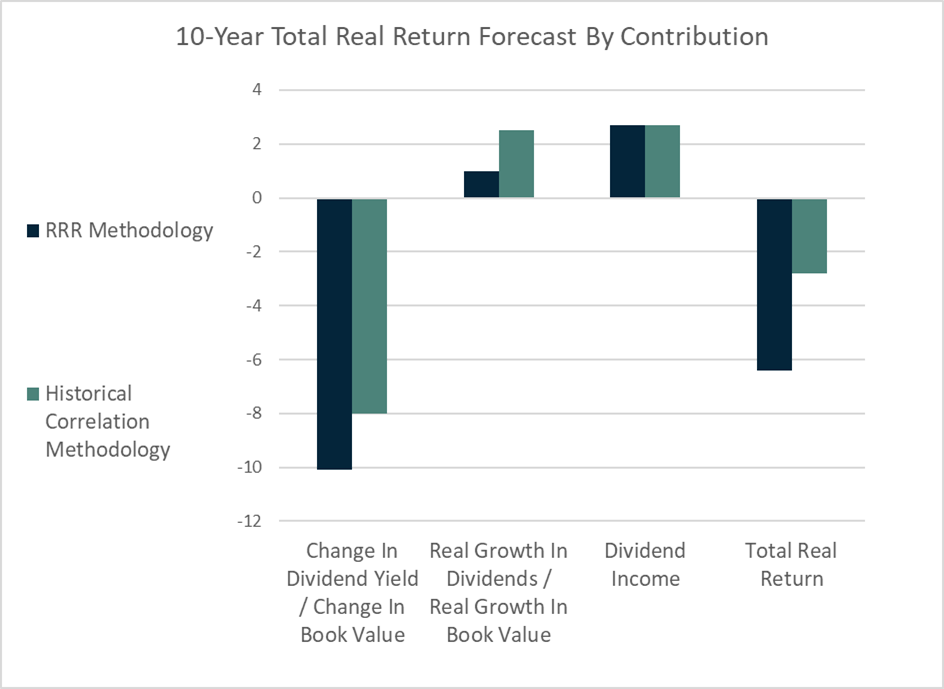

The -2.8% determine is predicated on John Hussman’s methodology of trying on the historic correlation between a selected valuation metric and subsequent returns. I’ve used the worth to guide ratio primarily based on knowledge since 1991 because it has proven the strongest correlation. The -6.4% determine is predicated on the decline required to revive traditionally regular future returns. On this case I have used the dividend yield and assumed a 5.0% required fee of return of 5.0% and actual dividend progress of 1.0%.

Writer’s calculations

Historic Valuation-Return Correlation (Hussman Methodology): -2.8%

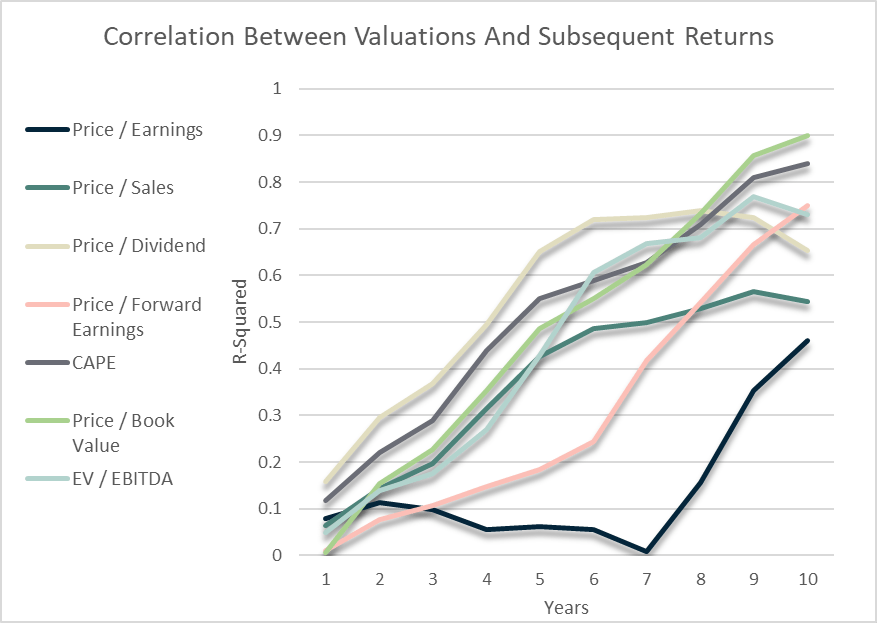

The chart beneath reveals the energy of the correlation between varied valuation metrics and subsequent S&P500 returns over totally different time durations. The very first thing to notice is that fairness index valuations have little or no affect on quick time period returns however are by far a very powerful issue figuring out long run returns. Because the time horizon rises to round 4-5 years a few of the extra dependable valuation metrics are in a position to clarify nearly half of the S&P500’s whole actual subsequent returns. On the 10-year horizon the r-squared rises to round 0.9.

Bloomberg, Robert Shiller, Writer’s calculations

The second factor to notice is that there’s a massive diploma of variability within the predictive energy of various valuation metrics. Though the worth/earnings ratio is probably the most extensively used, it’s among the many least dependable indicators when it comes to its means to foretell returns. The reason being that earnings are extremely delicate to the enterprise cycle. The market has appeared artificially low cost on a PE foundation previously on account of unsustainably excessive income throughout growth occasions and appeared artificially costly on a PE foundation when income have been briefly depressed throughout recessions. The worth to ahead earnings ratio does a significantly better job of predicting returns however the cyclically adjusted PE ratio has a more in-depth correlation because it smooths out these earnings over 10 years.

The desk beneath reveals the correlation between valuations and 10-year subsequent whole actual returns for the primary valuation metrics, together with 10-year implied future returns.

| Implied Ahead Annual Actual Returns | R-Squared Log Scale | |

| Worth / Earnings | 3.1 | 0.46 |

| CAPE | 1.0 | 0.84 |

| Worth / Dividend | 0.9 | 0.65 |

| Worth / Ahead Earnings | 0.0 | 0.75 |

| EV / EBITDA | -2.5 | 0.73 |

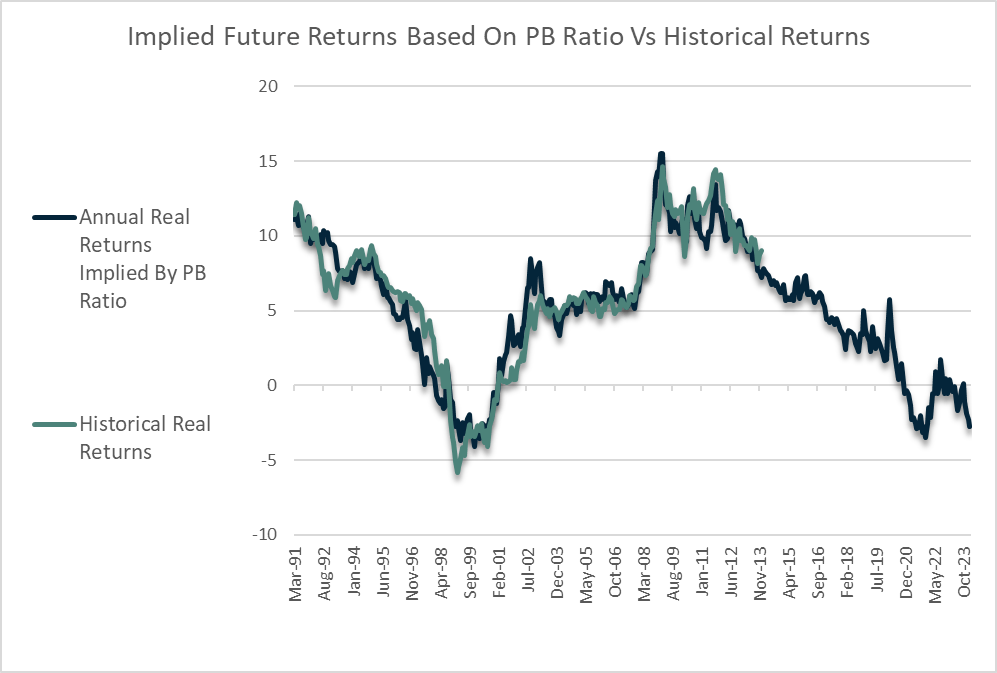

| Worth / Guide Worth | -2.8 | 0.90 |

| Worth / Gross sales | -3.2 | 0.54 |

Actual return estimates vary from 3.1% within the case of the PE ratio to -3.2% within the case of the PS ratio. The PE ratio’s weak historic reliability suggests warning is warranted, and once we clean out the affect of revenue margins utilizing the cyclically adjusted PE ratio anticipated returns fall to 1.0% and the correlation considerably improves. The worth to guide worth ratio has the closest correlation on a 10-year horizon, with an r-squared of 0.9, and the present determine implies annual actual whole returns of -2.8%.

Bloomberg, Writer’s calculations

The worth to guide worth estimate looks as if probably the most dependable indictor to make use of not solely as a result of it has the strongest correlation but additionally as a result of it’s the most steady indictor. The three.1% annual actual return determine implied by the PE ratio implicitly assumes that income proceed to develop quicker than guide values over the subsequent decade even with returns on fairness at document highs, which is extraordinarily unlikely.

Imply Reversion In Required Price Of Return: -6.4%

The second methodology seeks to calculate the returns that may consequence over the subsequent decade if valuations had been to imply revert to the degrees that implied historic common subsequent returns of 6.5%. For this, we have to take the dividend yield and estimate its probably future progress fee in dividends per share. Over the long run dividends are likely to develop on the tempo of earnings, which develop in step with gross sales, guide values, and GDP. This technique due to this fact components within the ongoing slowdown in pattern actual GDP progress into returns.

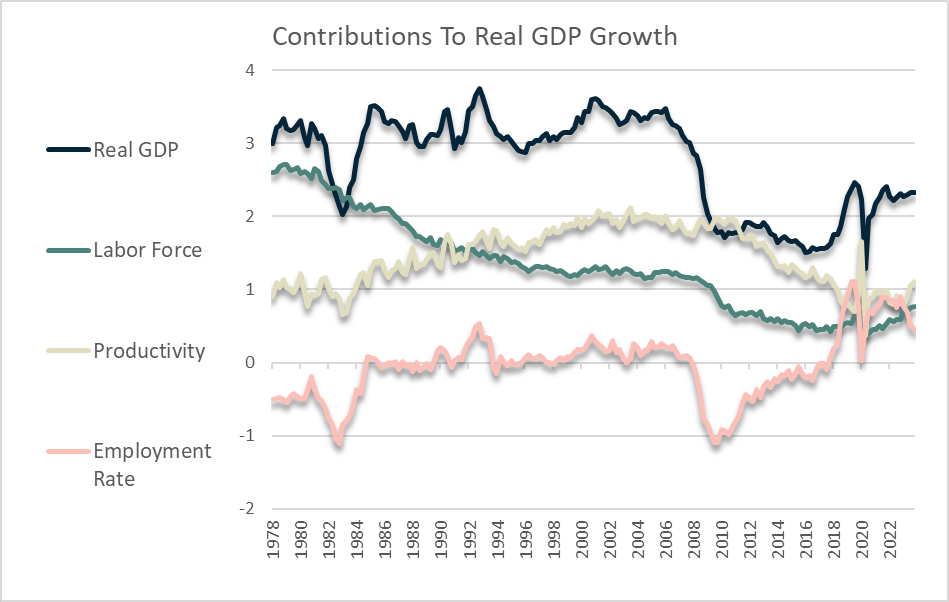

My core view is that actual GDP progress will common round 1% over the subsequent decade in step with the pattern progress charges seen in the remainder of the developed world over the previous twenty years. To see why, we will break down actual GDP progress into three fundamental parts; productiveness progress which is captured by output per employee, progress within the labour pressure reflecting inhabitants progress and internet immigration, and modifications within the unemployment fee. The chart beneath reveals the 10-year transferring common of the three parts. The two.3% annual progress fee loved over the previous decade could be damaged down roughly into 0.8% from progress within the labour pressure, 0.5% from a decline within the unemployment fee, and 1% progress in output per employee.

Bloomberg

Going ahead, the CBO tasks the US whole inhabitants to develop by round 0.4% yearly over the subsequent decade whereas the Convention Board tasks the working age inhabitants to develop by round 0.2% yearly, pushed fully by internet immigration. Which means that even when the downtrend in productiveness progress is halted and stays at 1%, it might solely take a transfer within the unemployment fee again to round 5% for actual GDP progress to common beneath 1%.

Assuming 1.0% actual GDP and dividend progress, the dividend yield must rise to five.5% for returns to satisfy the required fee of 6.5%. With the dividend yield at the moment at simply 1.4%, which means if this rise had been to happen step by step over the ten yr forecast interval it might end in actual whole returns of -8.5% yearly as proven beneath.

(1+g)(Unique Yield/Terminal Yield)1/N – 1 + (Unique + Terminal)/2

(1.01)(.014/.055)1/10 – 1 + (0.014 + 0.055)/2 = -0.085 = -8.5%

The -8.5% return determine above assumes that buyers will finally worth shares to return 6.5% yearly sooner or later at the same time as progress is assumed to be slower. Slower progress sooner or later implies that buyers could also be prepared to just accept decrease future returns, which can stop a full imply reversion in valuations. Assuming the required fee of return falls to five.0% on account of 1.5pp slower actual GDP progress relative to the previous, the return figures rises barely to -6.4%.

(1.01)(.014/.04)1/10 – 1 + (0.014 + 0.04)/2 = -0.064 = -6.4%

Taking a median of the 2 strategies offers an anticipated annual whole actual return forecast of -4.6%. That is broadly in step with the returns noticed from 1999 to 2009 and 1964 to 1982.

Price Cuts Have By no means Prevented Valuation Imply Reversion

There’s a widespread perception that if rates of interest fall then the required fee of return on shares would additionally fall, maintaining valuations from imply reverting decrease. Nevertheless, even when actual bond yields had been to fall again to zero it might not essentially stop a big decline in inventory valuations within the occasion of a reversal within the present optimism surrounding market returns. The fairness danger premium has moved independently of actual bond yields all through historical past. Even amid deeply unfavorable actual yields shares have usually traded at ranges implying robust long-term returns. As we’re seeing proper now, and as noticed on the 2000 peak and the 2007 peak, excessive fairness valuations can exist alongside excessive yields for a protracted time frame, however ultimately financial actuality units in and buyers start to require larger fairness returns. This normally happens in a self fulfilling method as such excessive optimism means even small losses trigger buyers to hunt the security of money.

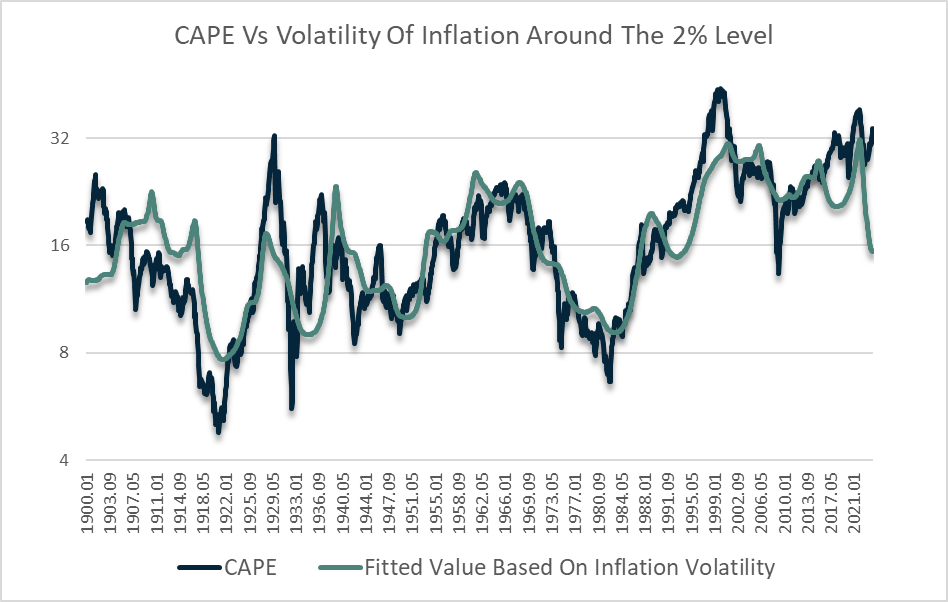

Over the long run a key issue driving swings in fairness valuations has been financial uncertainty associated to inflation. Falling valuations have tended to happen when inflation has deviated considerably from its long run common, both to the draw back like through the Nice Melancholy or to the upside like within the Nineteen Seventies, valuations have fallen considerably. This makes present market valuations notably troubling. As we noticed in 1929 and the late-Nineties, valuations aren’t solely excessive however are now not justified by a steady macro backdrop.

Robert Shiller, Writer’s calculations

Conclusion

The mixture of maximum valuations and slowing pattern actual GDP progress suggests actual S&P500 returns are prone to be deeply unfavorable over the subsequent decade, with my baseline assumption sitting at -4.6%. That is broadly in step with the returns noticed from 1999 to 2009 and 1964 to 1982 which occurred regardless of falling actual bond yields. Macroeconomic uncertainty as mirrored in inflation volatility is at ranges which have triggered draw back strikes in valuations previously.