abadonian

STAG Industrial, Inc. (NYSE:STAG) is a pure-play industrial REIT with a market cap of near $7 billion. It carries over 560 industrial buildings, that are primarily positioned within the CBRE Tier 1 markets throughout 41 states.

Lately, I determined to allocate a part of my portfolio into STAG to seize comparatively enticing dividend with notable upside potential (each from the yield and value appreciation perspective).

Within the article under, I’ll elaborate on three key points which have motivated me to open a protracted publicity towards STAG Industrial, Inc.

#1 Favorable timing and attractive entry level

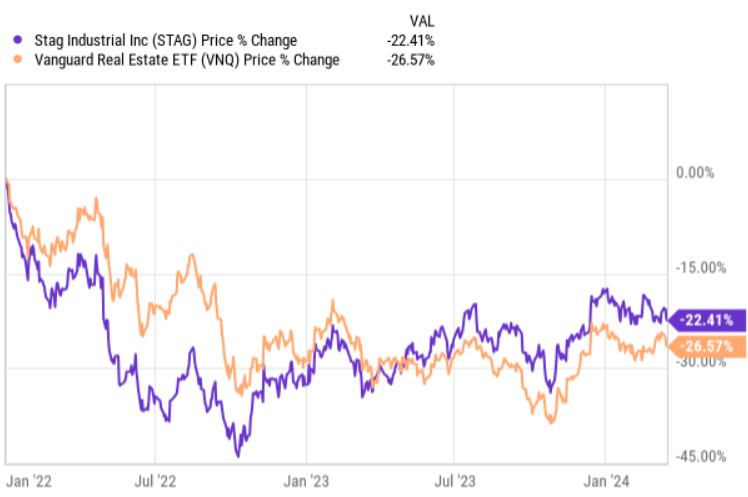

If we zoom again and assess STAG’s efficiency because the begin of 2022, we are going to discover a lower within the Share value that occurred in a coordinated method with the general REIT sector dynamics.

Over this era, the Share value is down by ~ 23%, which offers a possibility for long-term buyers to enter the place at a extra attractive stage.

YCharts

Within the chart above we will additionally discover a slight outperformance of STAG relative to the broader REIT sector. For my part, such tiny unfold appears not absolutely justified by the underlying fundamentals.

In different phrases, now we have to keep in mind that the REIT index can be comprised of sectors that face notable headwinds corresponding to workplace and retail house. Related challenges (albeit to not an extent to what has occurred within the workplace house) could be noticed throughout self-storage and healthcare REITs, the place the inflationary pressures have launched an enormous strain on the AFFO era.

Nevertheless, if we contextualize these sectors with the industrials (and STAG), that are uncovered to secular tailwinds and experiencing rising NOI figures, I do suppose that the hole of “alpha” needs to be a lot wider than simply ~ 4%.

One may argue that that is one thing STAG-specific and if we in contrast the REIT index with different industrial REITs, the image can be completely different. Effectively, the precise state of affairs is the other, the place STAG has carried out significantly above the commercial REIT sub-sector on YTD, 1-year, and 3-year foundation.

Lastly, by way of the entry level, STAG is attractively priced at P/FFO of ~15.6x, which is ~ 10% under the sub-sector average and ~ 30% under the related common if we modify for the extremes.

#2 Fortress steadiness sheet

To seize predictable and rising dividends along with some upside potential from the value appreciation angle, it’s crucial to have a well-structured steadiness sheet.

As of now, STAG’s internet debt to annualized run price adjusted EBITDAre is at 4.9x, which is 0.3x under the 2022 stage and ~ 0.4x under the sub-sector common.

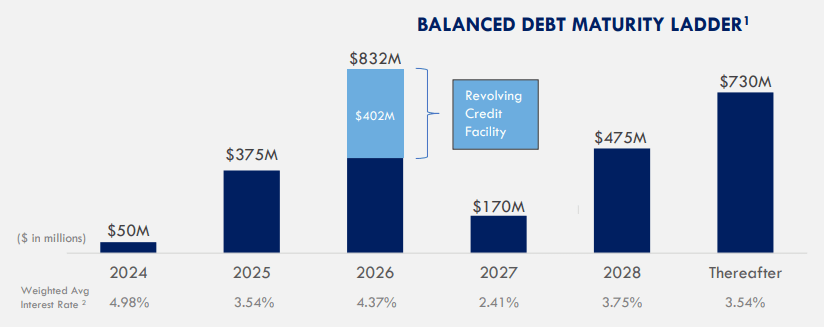

On prime of the balanced leverage ranges, STAG has managed to construction its debt maturity profile in a slightly favorable method that helps maintain the financing prices in test in addition to keep away from the build-up of elevated refinancing danger.

Within the chart under, we will see that this yr solely $50 million will probably be topic to refinancing and/or partial compensation. Then, solely in 2025, there will probably be extra tangible borrowings to refinance, which offers STAG with ample time to optimize the debt rollover course of and, hopefully, try this in a extra accommodative rate of interest setting.

STAG Investor Presentation

As well as, when considering of the steadiness sheet and total monetary danger, retained money stream profile performs additionally an necessary function.

Right here, the dividend payout ratio in 2023 continued to enhance, declining from 78% at year-end 2022 to 75% at year-end 2023. Because of this, STAG managed to seize circa $90 million of surplus money after all the prices and dividend distributions.

These proceeds may very well be, for instance, directed in the direction of natural repayments of forthcoming debt maturities or channeled in the direction of M&A and/or natural CapEx alternatives thus stress-free the necessity to supply exterior leverage at a probably extreme scale.

#3 Notable progress potential

Throughout 2023, STAG registered a really sound efficiency rising its like-for-like money NOI by 5.6% in comparison with 2022. This resulted in one other annual like-for-like money NOI progress report for the Firm. An enormous driver behind the NOI progress was the success within the money leasing spreads that in 2023 produced a 31% improve.

All of this was doable because of the mixture of favorable secular dynamics and the belief of STAG’s accretive capital deployment program.

On the secular dynamics facet, all the pieces revolves across the following:

- Rising demand for industrial properties stemming from e-commerce, nearshoring, and onshoring.

- Constrained setting for the formation of recent provide.

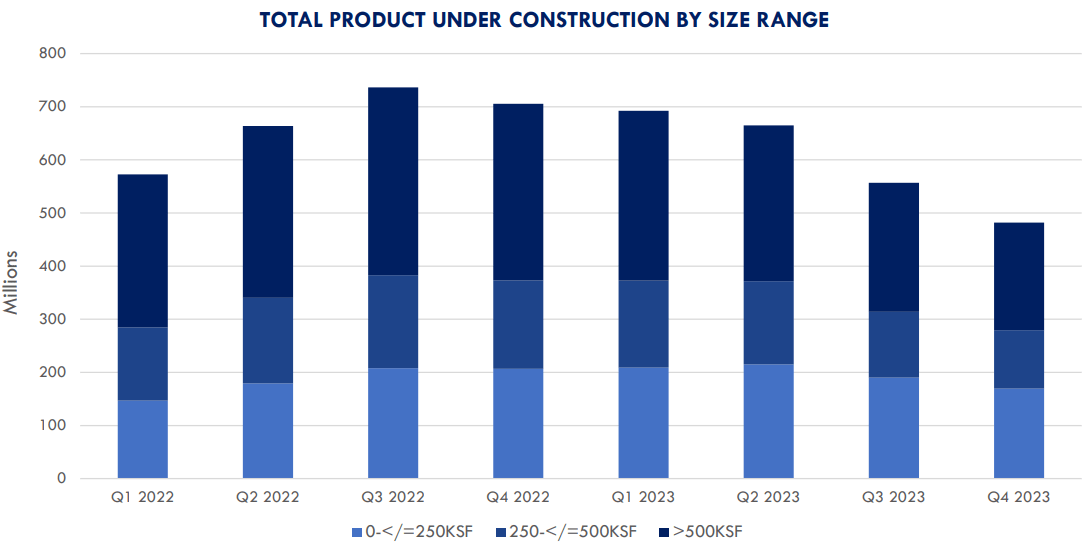

For instance, the chart under captures properly the lower in building progress of recent services because the FED began to hike the rates of interest.

STAG Investor Presentation

All of that is going down regardless of the rising demand for industrial properties.

Within the latest earnings call, Invoice Crooker – Chief Govt Officer – summarized the essence fairly elegantly:

Whereas provide stays elevated, new building begins have declined nationally by roughly 65% on a year-over-year foundation as of This fall of 2023. As well as, forecast for 2024 and 2025 deliveries are anticipated to lower to simply 2.2% of inventory. Emptiness charges will seemingly proceed to rise within the close to time period, however we anticipate the height to happen someday within the second half of 2024, with normalization round year-end. We nonetheless anticipate market hire progress for our portfolio to be within the mid-single digits for 2024.

On account of the aforementioned state of affairs available in the market, STAG is well-positioned to learn from this within the type of stable NOI progress. The issued steerage by the Administration for 2024 signifies a variety of like-for-like NOI progress between 4.75% and 5.25%. And that is even contemplating the report NOI efficiency in 2023.

The underside line

For me, STAG looks as if a transparent purchase that is ready to supply attractive mixture of ~4% month-to-month dividend and progress potential.

The presence of sturdy steadiness sheet, industry-level tailwinds, and powerful NOI steerage bode nicely for the Share value appreciation and dividend progress.

Lastly, the entry level at this stage may be very enticing as STAG has misplaced ~ 23% of the market cap since early 2022. A number of-wise, STAG Industrial, Inc. trades under its friends, making the funding case much more interesting.