Scott Olson

Funding Thesis

Stellantis N.V. (NYSE:STLA) is a real deep-value scenario. On this occasion, it seems to be extremely undervalued with out presenting any particular causes to doubt its high quality and warrant a decrease valuation.

On this article, I’ll evaluation key points to find out why I do not see any grounds for valuing it so cheaply. From the transition to electrical autos to assessing its high quality in comparison with opponents and exploring potential catalysts for the market to regulate the valuation within the quick time period. Moreover, I’ll conduct a valuation to justify why I imagine the corporate is a transparent ‘purchase‘ on the present worth.

Enterprise Overview

Stellantis N.V. is a worldwide automotive firm fashioned from the merger of Fiat Chrysler Vehicles and PSA Group. The merger was accomplished in January 2021, ensuing within the creation of Stellantis because the fourth-largest automotive producer on the earth by quantity.

Stellantis is house to a number of well-known automotive manufacturers, together with Fiat, Chrysler, Jeep, Dodge, Ram, Peugeot, Citroën, Opel, and others. The corporate operates in numerous markets globally and has a various vary of autos, from passenger automobiles to vans and industrial autos.

Stellantis Manufacturers (Stellantis)

As you may see, Stellantis manufacturers will not be inherently inferior or in a much less aggressive place in comparison with different opponents resembling Ford Motor Firm (F), Common Motors Firm (GM), or Volkswagen AG (OTCPK:VWAGY). The truth is, the company estimates that it holds a 10% market share in North America, because of the sturdy model presence of Jeep and Ram, in addition to roughly 20% of the market share in Europe.

Due to this fact, based mostly on this side, we can’t think about that the corporate deserves to be quoted at such a low valuation.

Electrical Autos

Alternatively, the biggest threat dealing with all these automobile manufacturing firms is the transition towards electrical autos. This shift will necessitate substantial investments in growing their very own electrical autos to stay sufficiently aggressive in comparison with the present market chief, Tesla, Inc. (TSLA), which is considerably forward when it comes to know-how and manufacturing functionality. All this whereas striving to make their electrical autos worthwhile sufficient to keep away from monetary losses throughout this transformative course of.

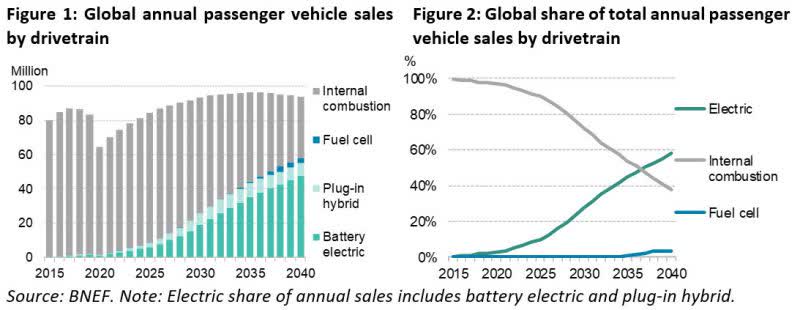

It’s value noting that the transition to electrical autos shouldn’t be anticipated to occur anytime quickly. In accordance with BloombergNEF’s latest research, titled ‘Lengthy-Time period Electrical Automobile Outlook,’ electrical fashions are projected to comprise 58% of recent passenger automotive gross sales globally by 2040 and 31% of the whole international automotive fleet. In different phrases, even inside the subsequent 20-25 years, it isn’t anticipated that 100% of gross sales will probably be solely electrical autos.

Electrical Automobile Outlook (BloombergNEF Report)

Because of this expectation, the Inner Combustion Engine automobile market anticipates important development on this decade. In the USA alone, practically 10% growth is expected, and rising economies can even play a vital function within the sector’s enlargement. That is because of the international lack of EV infrastructure, main customers to proceed choosing conventional autos, which are sometimes extra inexpensive in sure fashions, regardless of Tesla’s efforts to considerably cut back its costs.

In conclusion, I additionally don’t imagine that electrical autos pose an imminent threat of extinction for conventional automobile producers and wouldn’t justify such a low valuation.

Key Ratios

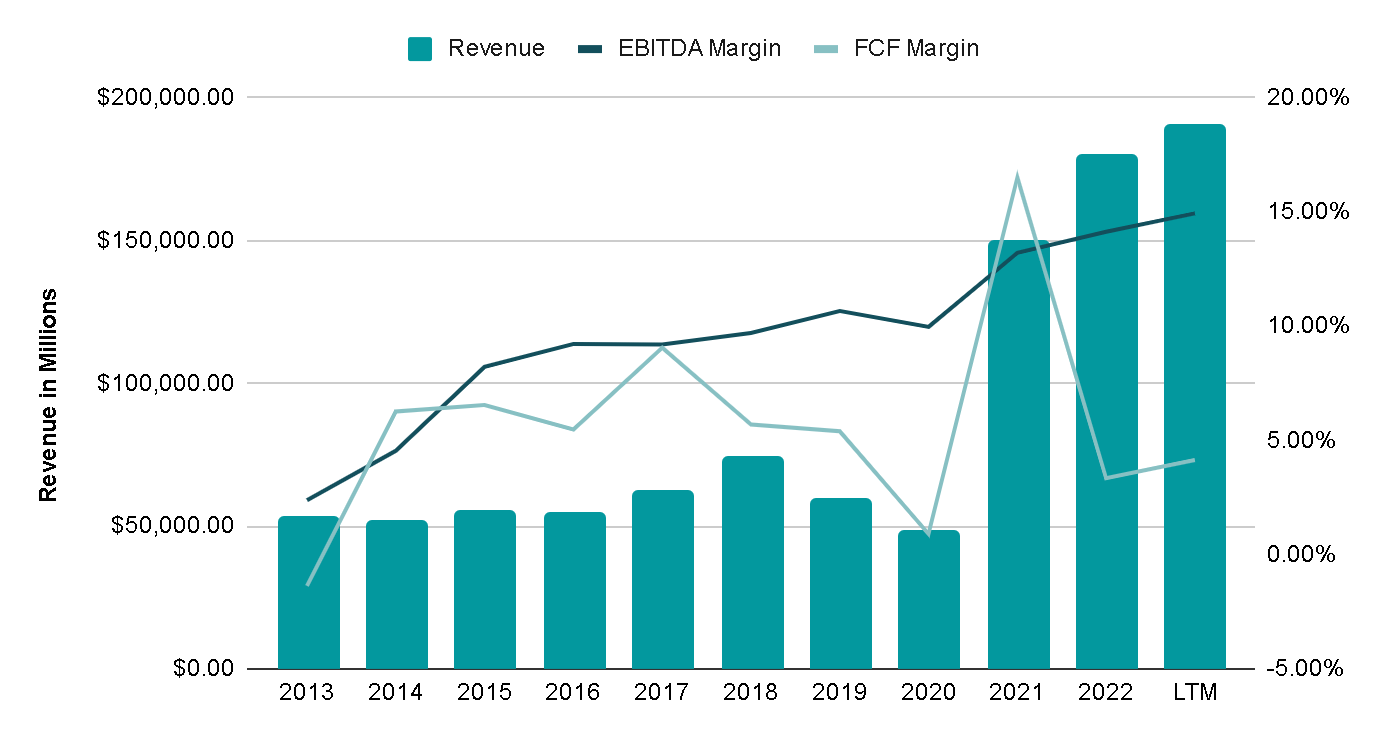

As talked about, the merger between Fiat Chrysler and PSA Group occurred in 2021. When analyzing the pre- and post-merger numbers, we observe not solely a major enhance in income, rising from $47 billion in 2020 to $149 billion in 2021, but in addition an enchancment in margins. This means that the merger notably enhanced the general high quality of the enterprise.

The truth is, from 2013 to 2020, income skilled an annual lower of -1.5%, sustaining common EBITDA margins of 8%. Nonetheless, between 2021 and the final twelve months, income has grown by 12.75%, with common EBITDA margins of 14%, reaching nearly 15% within the final twelve months. This confirms that the merger created a stronger firm, and the elevated scale and price effectivity in the end benefited earnings.

Writer’s Illustration

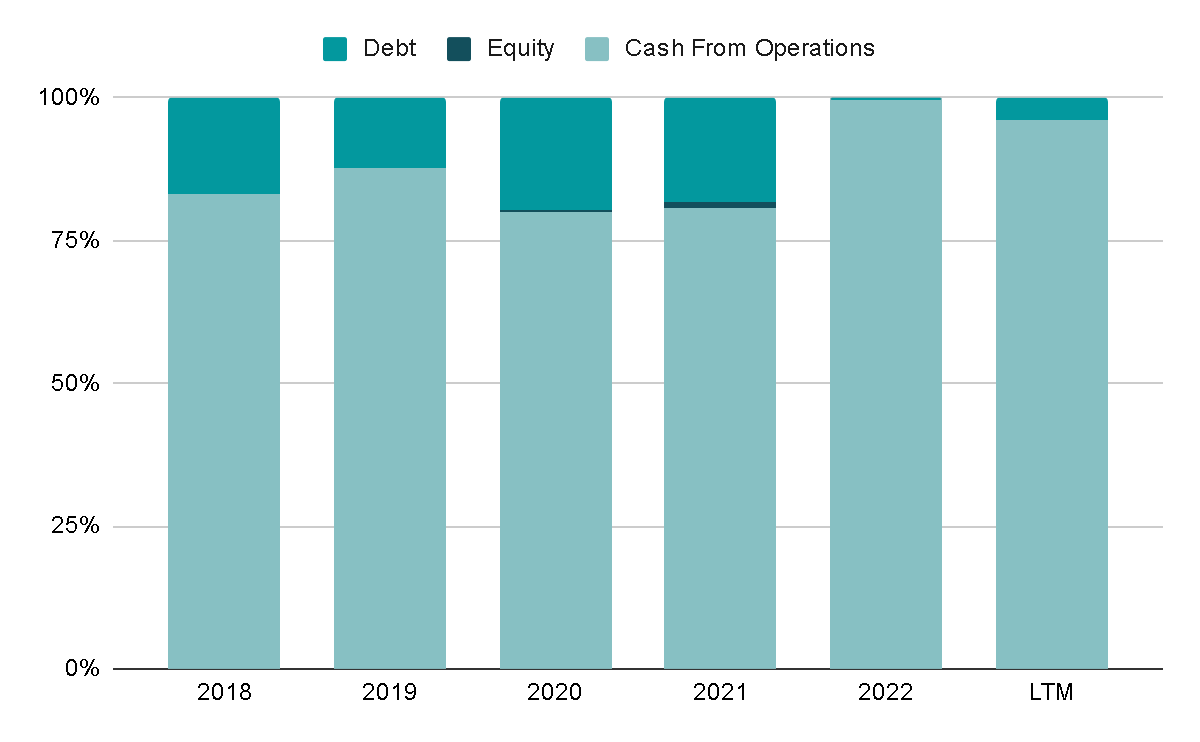

Between 2018 and 2020, the corporate was primarily financed by Money From Operations, with a smaller portion, roughly 15%, coming from Debt. Nonetheless, since 2021, there was a radical shift, and within the final two years, not even 5% of the financing has originated from Debt.

Writer’s Illustration

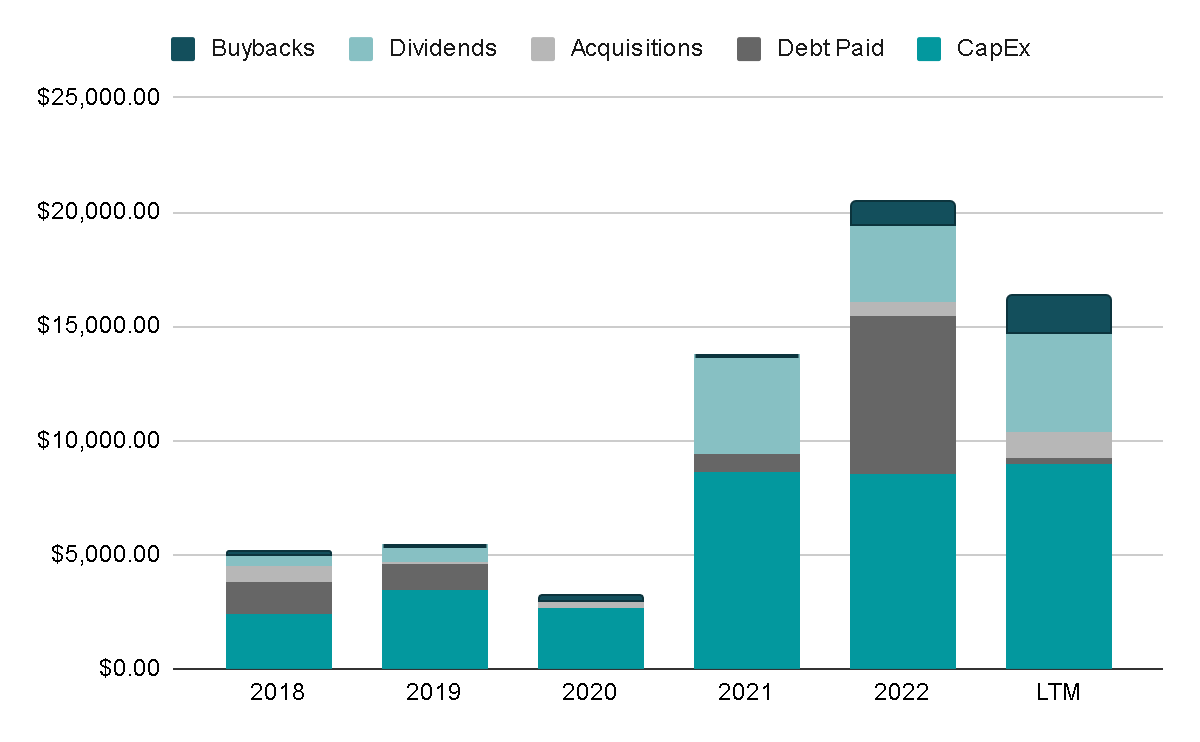

Over the previous 5 years, half of this capital has been allotted to CapEx for enterprise reinvestment, one other 20% to pay down debt, and 20% to reward shareholders by dividends and buybacks. The truth is, €8.6 billion in dividends and €1.1 billion in buybacks have been distributed, and there may be an energetic €1.5 billion buyback plan. That is potential as a result of the corporate is a uncommon case within the car sector, having no debt, and its web debt is -€23 billion. In different phrases, with the money on the steadiness sheet, they may repay all their debt and nonetheless have 23 billion euros remaining.

Writer’s Illustration

Are Rivals Higher?

Now, to contextualize this knowledge compared to its opponents, I’ve created a desk evaluating key ratios resembling EBITDA margins, return on invested capital, web debt (in billion), and essential valuation metrics like EV/EBITDA and P/E ratios.

On this regard, Stellantis stands out as the corporate with the best EBITDA margins, the one one with unfavourable web debt, and the best returns on capital. Furthermore, additionally it is the most attractively valued. The EV/EBITDA ratio is 80% decrease than the typical of different opponents, and the P/E ratio is 50% decrease.

Writer’s Illustration

There’s undoubtedly a important hole in each necessary aspects-Stellantis excels when it comes to high quality, whereas additionally being some of the attractively valued firms available in the market. Due to this fact, we can’t conclude that the corporate is cheaper because of a poorer high quality enterprise mannequin.

Valuation

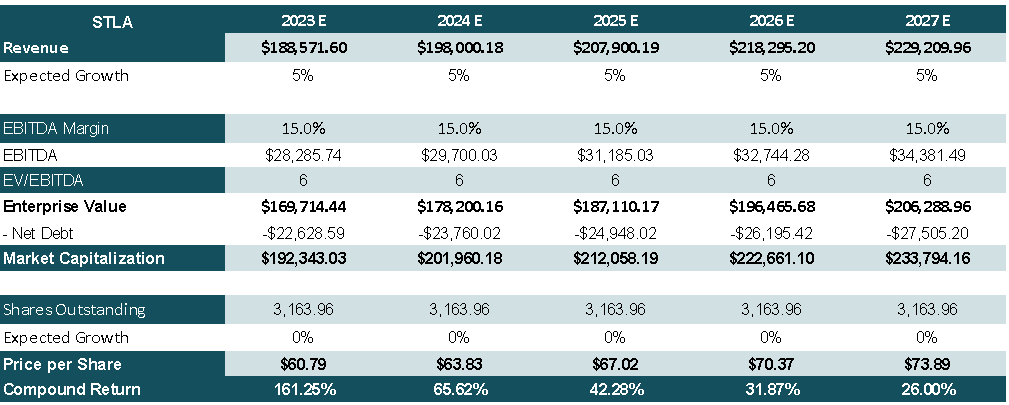

At this level, it seems that Stellantis’s valuation enhances this deep worth scenario, however, if we conduct a valuation with the idea of a 5% annual income development over the subsequent 5 years, sustaining EBITDA margins just like the present 15%, and making use of an EV/EBITDA a number of of 6x-lower than the typical of 8x for its competitors-without contemplating buybacks within the subsequent few years, we may anticipate an annual return of 26% over the subsequent 5 years on the present worth.

This represents an exceptionally enticing efficiency at a conservative valuation. The evaluation assumes that the corporate will develop lower than market expectations, is not going to interact in share repurchases, and the a number of will stay under the typical of its opponents.

Writer’s Illustration

Why Is So Low-cost?

At this level, there is no such thing as a doubt that Stellantis is a deep-value alternative and is very undervalued with no clear motive. In my view, it’s a mixture of mistrust relating to the corporate’s continued relevance in an electrical automobile surroundings, which we now have already seen is unlikely to occur anytime quickly, and fears in regards to the macroeconomic scenario. The outlook for 2024 suggests there will probably be no additional rate of interest hikes, whereas inflation is declining, and the financial system seems to stay strong.

Moreover, I need to point out the dangers that the corporate faces. Though its valuation relative to its friends could be very low-cost, this sector doesn’t often commerce at excessive multiples as a result of it’s structurally tough to succeed right here. Amongst a few of the dangers I need to spotlight are the next:

- Financial Downturns: The automotive business is delicate to financial cycles. Financial downturns can result in decreased shopper spending, decrease demand for brand new autos, and monetary challenges for automotive producers. This is without doubt one of the essential the reason why the market is distrustful of the sector proper now.

- Technological Adjustments: Speedy developments in know-how, significantly in electrical autos, autonomous driving, and connectivity, pose each alternatives and challenges. Stellantis must adapt to those adjustments to stay aggressive, however the tempo of technological evolution could be a threat.

- Competitors: Intense competitors within the automotive business can have an effect on market share, pricing, and profitability. Stellantis wants to repeatedly innovate and differentiate its merchandise to remain forward of opponents.

Ultimate Ideas

Having thought of the dangers, the standard of the enterprise, and the present valuation, it appears to me that the corporate is a transparent ‘purchase‘, and I see no compelling motive for it to be buying and selling at such a low valuation. Though I additionally perceive the elements contributing to this distrust.

At present, most of the fears are fading, particularly these associated to the macroeconomic scenario and the current points with strikes in the automotive sector. Whereas it’s nonetheless too early to say victory, if the financial system continues to enhance, discretionary consumption may strengthen, and Stellantis is likely to be seen as one of many essential beneficiaries. Even when this situation doesn’t unfold, the valuation offers sufficient margin of security to supply potential upside, even when issues don’t go based on expectations.