sinseeho/iStock by way of Getty Pictures

Intro & Thesis

I commenced protection of Sterling Infrastructure, Inc. (NASDAQ:STRL) inventory in mid-July 2023 when its share was buying and selling at $59.11. Since then, the inventory has skilled a powerful surge of practically 50%, outperforming the broader market, which has grown by 6.75% throughout the identical interval. Nonetheless, this upward trajectory has not been totally constant. All through the autumn season, there was a notable consolidation within the STRL share value, prompting issues amongst buyers in regards to the viability of holding this small-cap consultant inside the Industrials sector. In response to those developments, I carried out a complete replace of my protection in mid-October and, after cautious evaluation, reaffirmed my ‘Purchase’ score. Following a short interval of volatility, STRL as soon as once more demonstrated its resilience, registering a achieve of ~24%, outpacing the broader market’s 15.23% development.

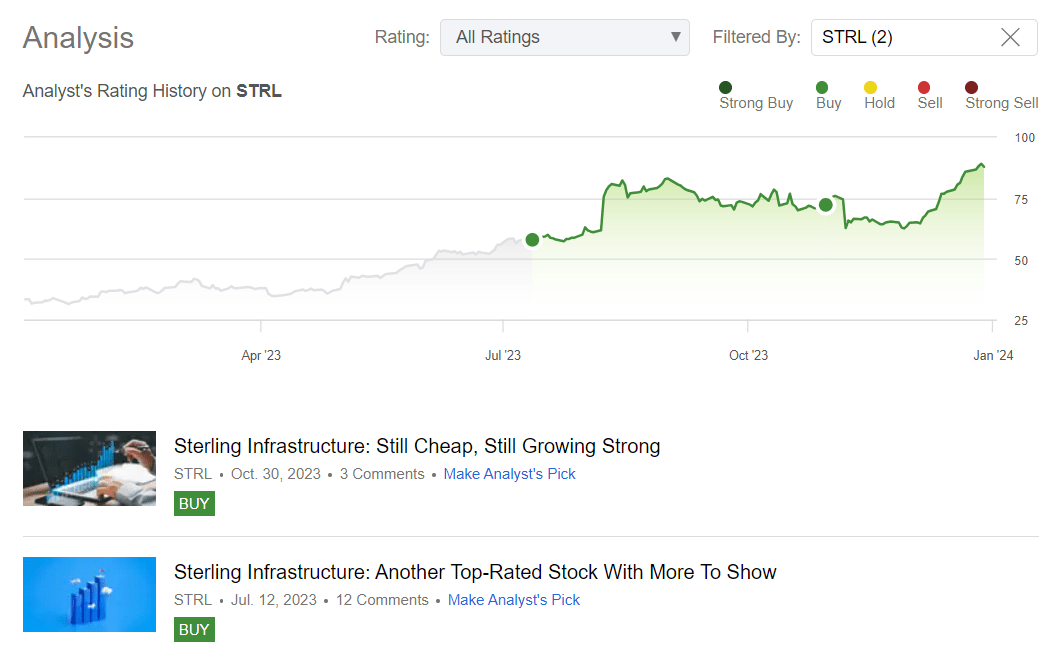

The creator’s protection of STRL inventory on Searching for Alpha

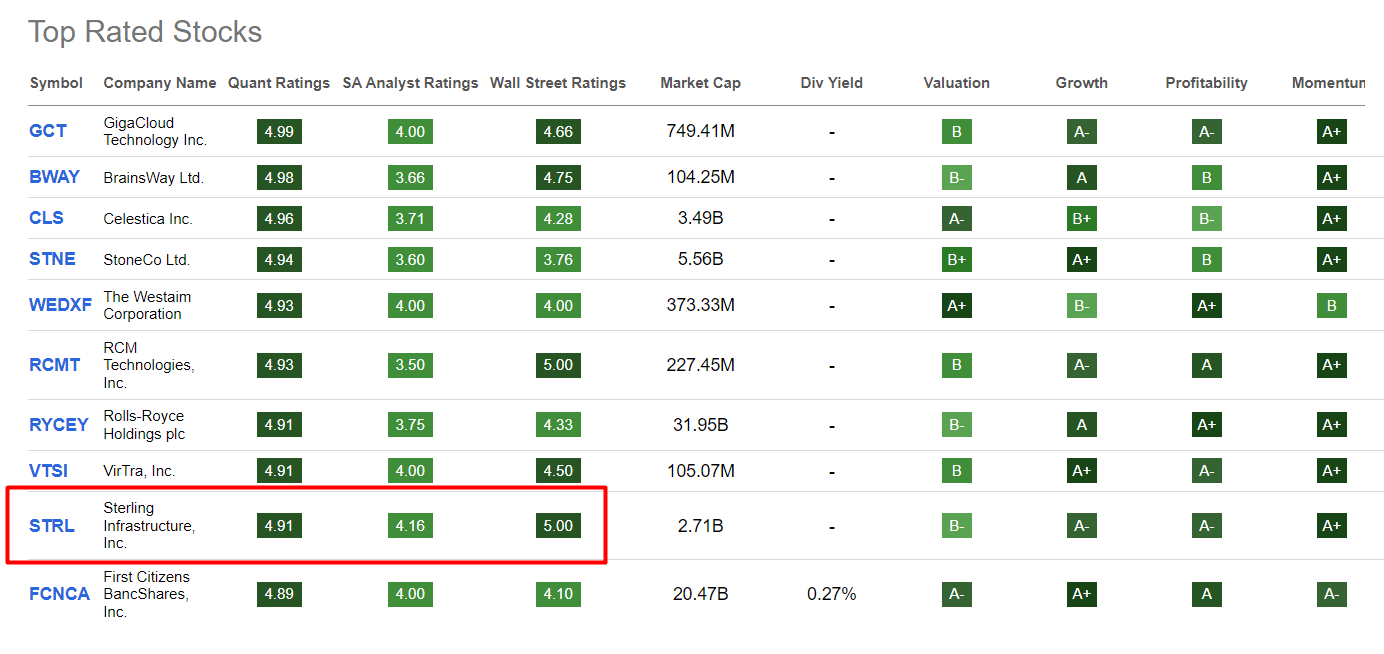

Sterling continues to be one of many top-rated shares right here on Searching for Alpha:

Searching for Alpha’s important web page, creator’s notes

For my part, STRL has this standing fairly rightly: this inventory nonetheless appears like one of the promising concepts in the marketplace regardless of its 169% year-on-year growth.

Why Do I Suppose So?

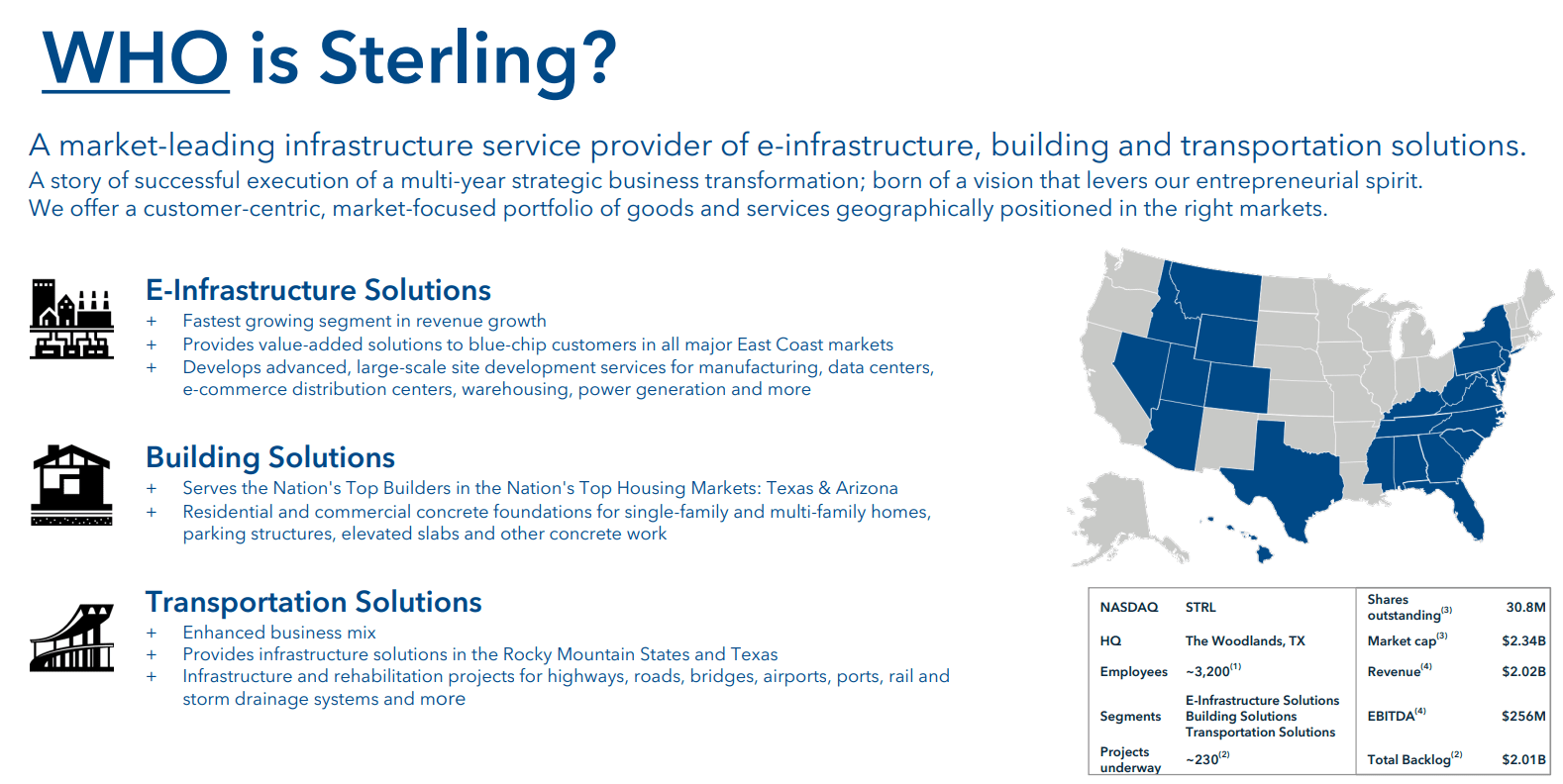

Sterling Infrastructure, Inc. is a $2.7-billion market cap firm working throughout E-Infrastructure (45% of Q3 FY23 income), Transportation Options (35%), and Constructing Options (20%) segments in the USA. The company specializes in web site improvement providers, infrastructure initiatives, and concrete foundations. Notably, it strategically divested its partnership with Myers & Sons Development in December 2022 to enhance margins.

STRL’s IR supplies

As I discussed final time, Sterling Infrastructure’s administration foresees long-term development alternatives in E-Infrastructure (information facilities, manufacturing), Transportation Options (federal and state funding), and Constructing Options (residential and business demand).

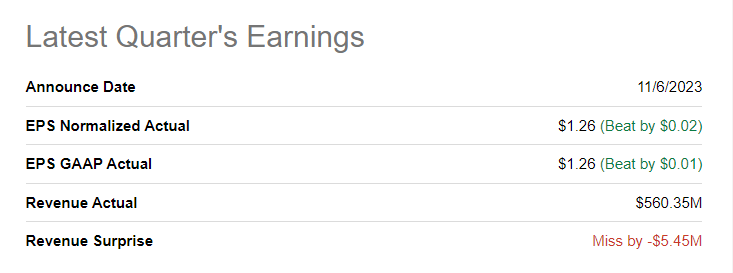

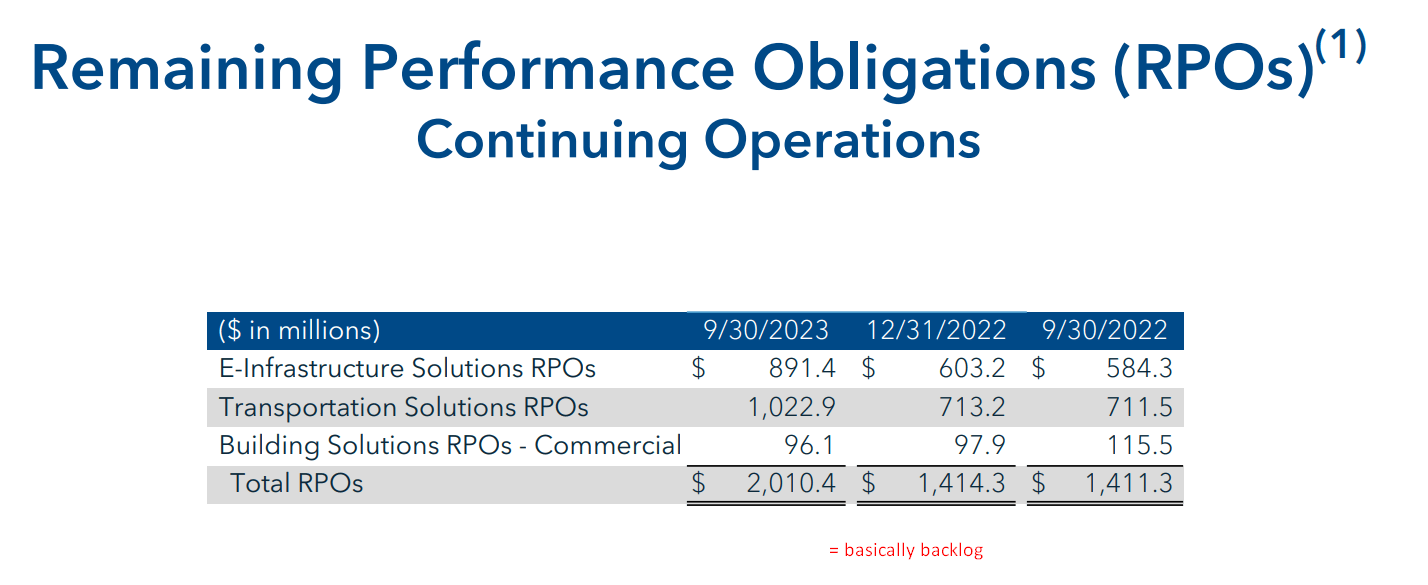

Primarily based on what I can see from the corporate’s newest Q3 outcomes, the administration’s phrases concerning finish market tailwinds are certainly coming true. Sterling reported a record quarter with diluted EPS at $1.26, reflecting a major 25% enhance from the identical interval in FY2022. The corporate couldn’t beat the revenue consensus, nevertheless it sustained sturdy development of 13.7% (11.7% organically) and maintained a sturdy backlog, surging by 42% because the starting of the 12 months, exceeding $2 billion.

Searching for Alpha

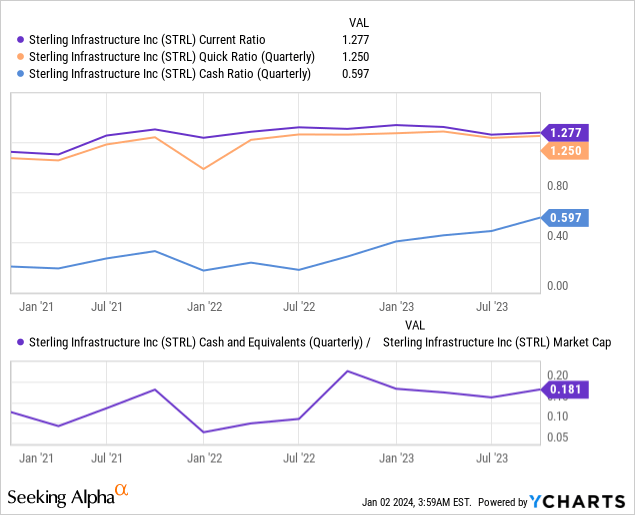

Working money circulate reached $150 million, contributing to a powerful whole money place of $409 million (i.e. ~18% of the entire market cap as of as we speak). On the identical time, a take a look at the corporate’s liquidity place exhibits that it’s at one of many highest ranges in recent times.

Emphasizing a strategic give attention to acquisitions and adherence to the “Sterling Way” rules, the latest earnings name highlighted anticipated development alternatives in E-Infrastructure, Transportation Options, and Constructing Options (type of the identical imaginative and prescient as prior to now quarters). On the identical time, the corporate doesn’t need to sacrifice margins because it expands its working actions; quite the opposite, STRL is attempting to push forward with margin growth.

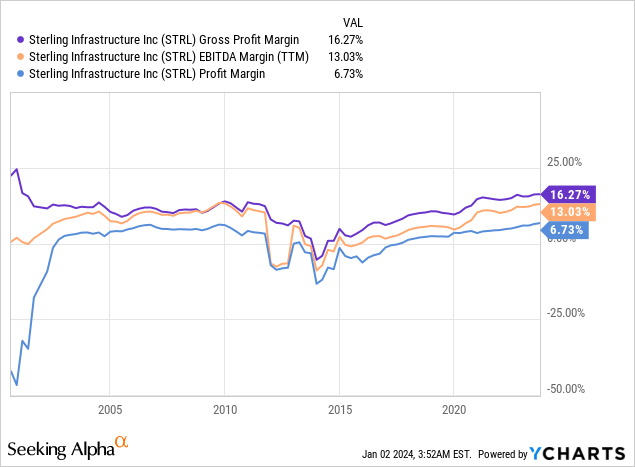

Certainly, the corporate’s revenue margins have been considerably higher than in earlier quarters and approached the very best in Sterling’s public historical past:

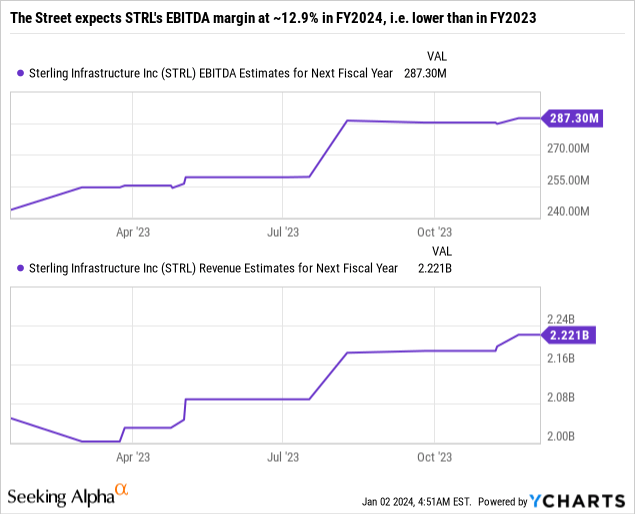

I count on this pattern to proceed additional as a result of thus far STRL’s gross margin doesn’t even attain the industry median.

Relating to future initiatives, the CEO talked about that the massive initiatives deliberate to bid in 2024 and 2025 are multi-billion greenback endeavors, comparable in scale to the lately introduced report bookings. He emphasised that the corporate’s backlog is robust, up over 40% from the start of the 12 months, indicating a optimistic development trajectory.

STRL’s IR supplies, creator’s notes

With the corporate elevating its full-year steering, and projecting a 32% development in EPS over FY2022, Sterling Infrastructure’s administration workforce appears optimistically towards continued success in FY2024, supported by a positive monetary outlook, a robust backlog, and a wholesome money place. And judging by how administration’s phrases have been carried out within the current previous, I’ve no motive to not imagine on this outlook as we speak.

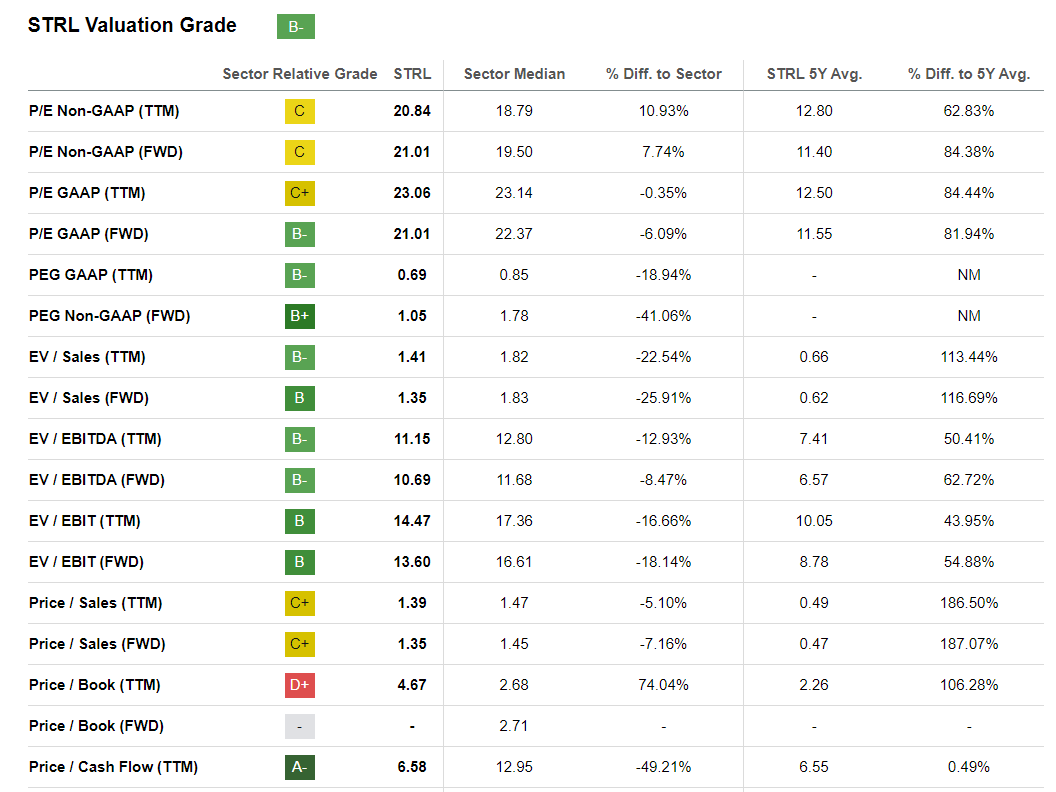

So far as STRL’s valuation is anxious, the inventory nonetheless appears engaging regardless of the sturdy rally in current months.

Searching for Alpha, STRL’s Valuation

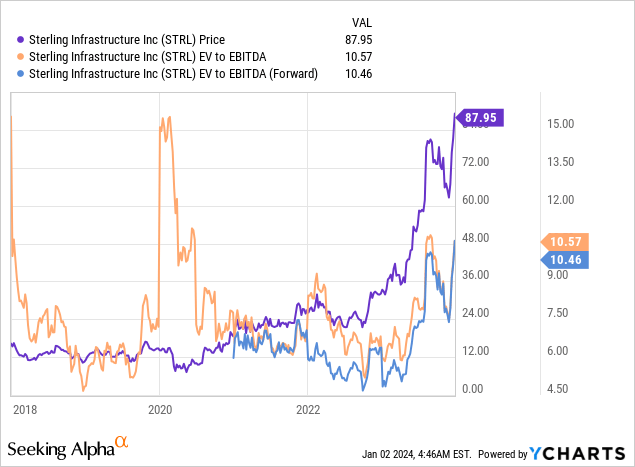

From a historic perspective, nonetheless, the STRL share appears considerably overheated with an EV/EBITDA of 10.46x for the approaching 12 months [based on YCharts data].

Nonetheless, I believe the inventory may proceed to rise regardless of the already excessive multiples, because the Road seems to be ignoring the corporate’s potential for margin growth.

If we preserve the identical EV/EBITDA stage as as we speak and with an EBITDA growth to solely 14% in FY2024, we get an implied enterprise worth of ~$3.25bn. After deducting web debt, I calculate upside potential of ~19%, so I reiterate my earlier ‘Purchase’ score on the inventory.

The Backside Line

Each investor ought to be mindful, that purchasing Sterling Infrastructure inventory entails dangers, together with the corporate’s sensitivity to financial downturns and the cyclical nature of the development business, which might affect demand for its providers. Dependency on authorities contracts exposes STRL to adjustments in authorities insurance policies and finances allocations. Potential venture delays, price overruns, and intense competitors within the building business are extra dangers, together with the geographic focus of operations. Materials price fluctuations, political and regulatory uncertainties, and the vulnerability to weather-related disruptions are additionally notable elements that buyers ought to think about when evaluating the potential dangers related to investing in STRL inventory.

Regardless of all of the potential dangers, STRL doesn’t appear like a extremely undervalued firm as we speak, however its success when it comes to margin growth towards the backdrop of fast backlog development can solely encourage admiration. I imagine that Mr. Market continues to be underestimating the prospects for its EBITDA and EPS development as we speak, which is able to in the end result in a re-rating and realization of the upside potential (+19%) I calculated in as we speak’s article. Due to this fact, I’ve determined to reiterate my earlier ‘Purchase’ score.

Thanks for studying!