AlizadaStudios

Summit Midstream Companions (NYSE:SMLP) has seen its market cap persistently sit under $200 million. The corporate has a formidable portfolio of property, however it’s been held again by its rising debt load. As we’ll see all through this text, the corporate has a danger of rising rates of interest with its debt, which may damage its future shareholder returns.

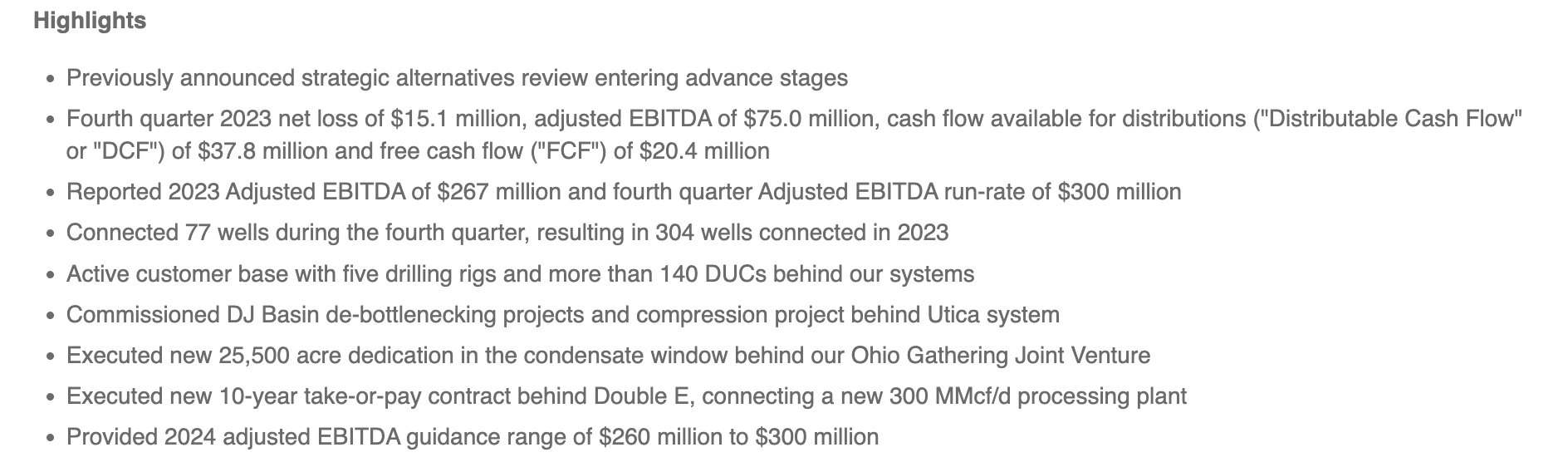

Summit Midstream Companions Highlights

The corporate had a robust 2023, because it continues to have a look at strategic options for its long-term survival.

Summit Midstream Companions Press Releasee

For the fourth quarter, the corporate had adjusted EBITDA of $75 million and DCF of just below $40 million. FCF was simply over $20.4 million. The corporate related 77 wells, with annual properly connections of greater than 300, though pure gasoline costs stay fairly weak, particularly as we enter the summer time when demand is weaker. The corporate is engaged on de-bottlenecking ventures, and new ventures.

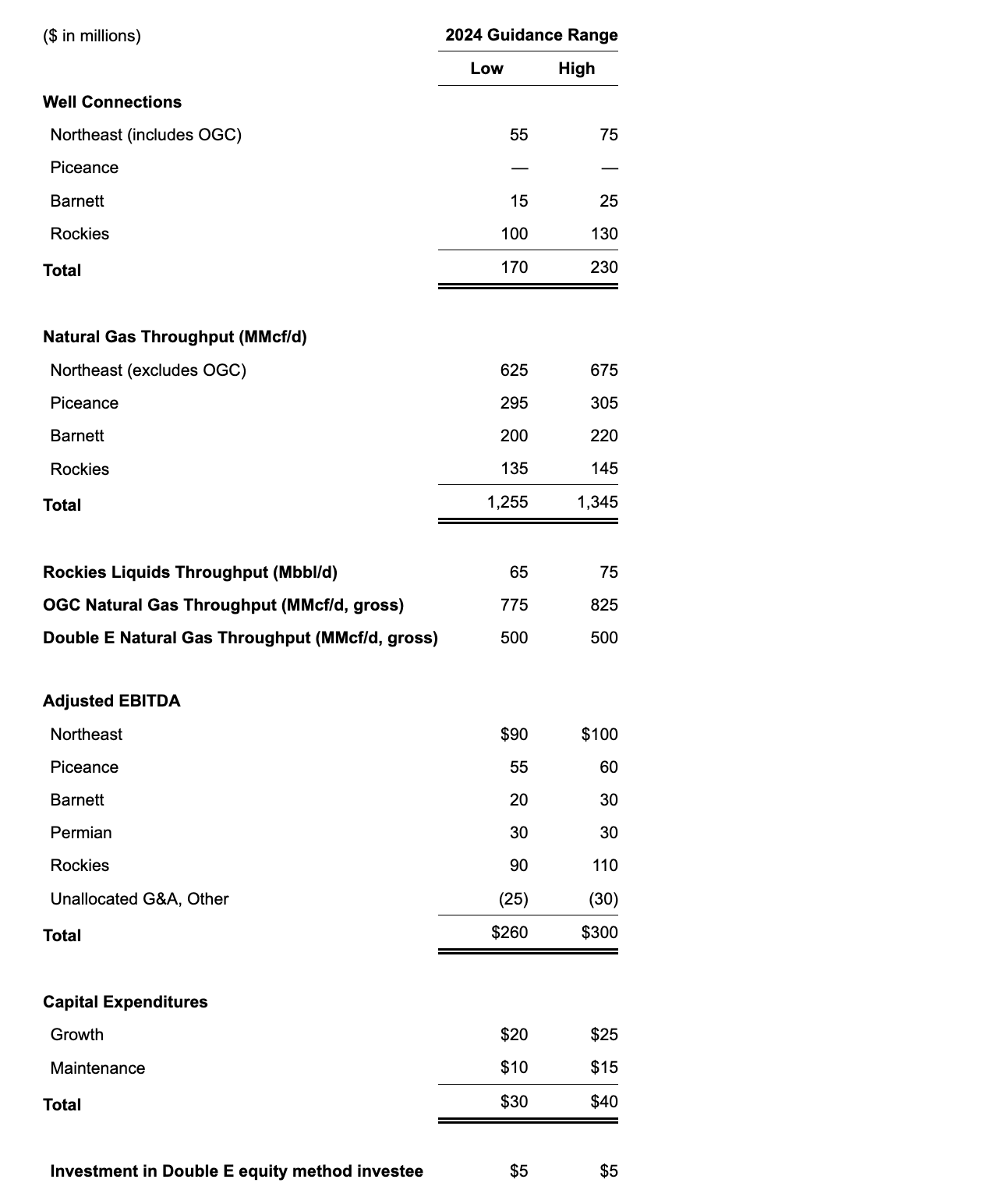

There are some enormous wins. A brand new dedication acreage behind the Ohio Gathering Joint Enterprise is extremely spectacular. A ten 12 months take-or-pay contract behind Double E is gigantic for the corporate’s success. The corporate’s 2024 EBITDA steerage is $280 million, ~5% above 2023, and robust efficiency for the corporate.

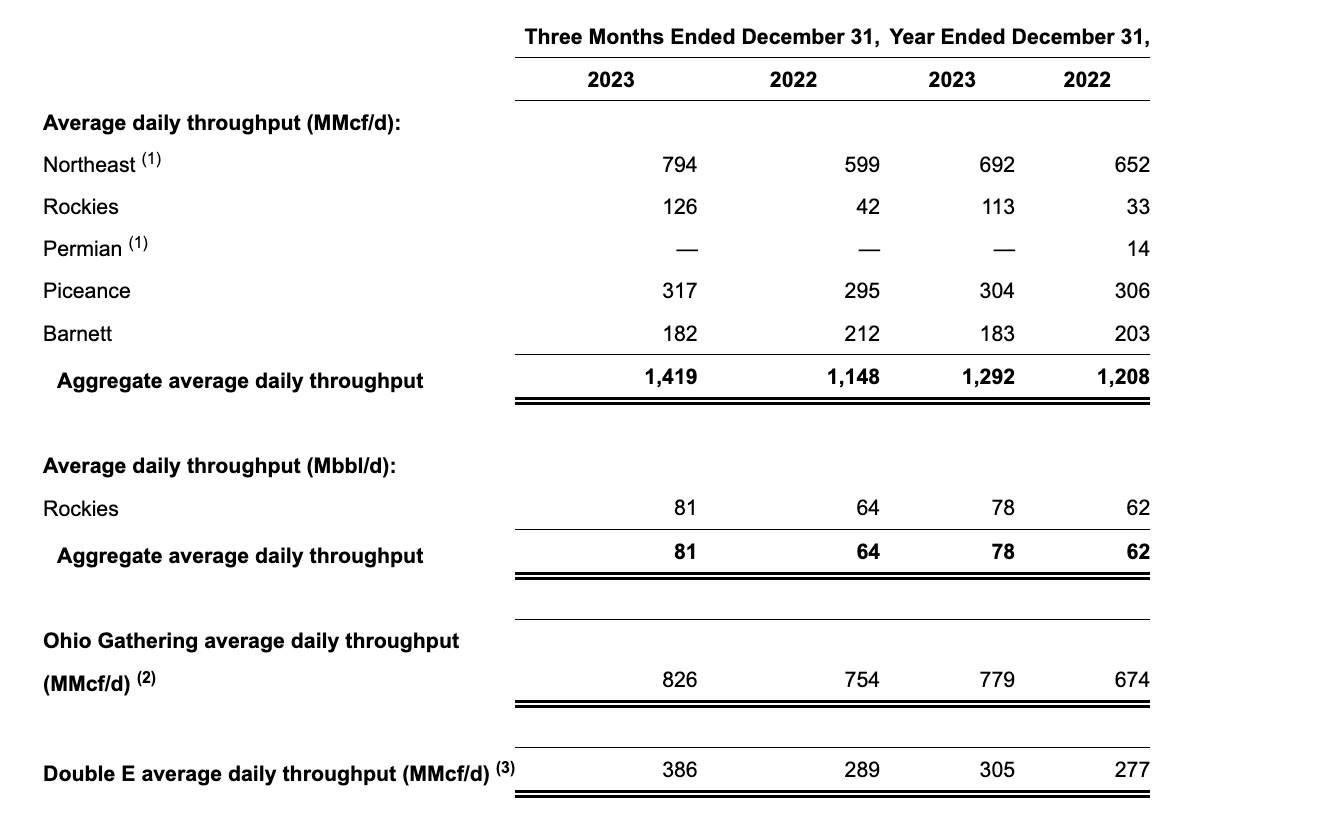

Summit Midstream Companions Volumes

The corporate’s focus is on sustaining what has been extremely risky volumes after weak point.

Summit Midstream Companions Press Releasee

The corporate noticed sturdy quantity enhancements alongside key areas in 2023. Particularly the corporate noticed sturdy quantity enhancements in its key northeast section. Rockies quantity additionally elevated dramatically because it turn out to be worthwhile as soon as once more. The corporate’s solely quantity decline was within the Barnett, however total volumes elevated by sturdy double-digits.

The Double E additionally noticed a robust improve in volumes going into the again half of the 12 months. The Ohio Gathering system noticed double-digit will increase, and noticed a brand new gathering system added. That can assist total energy in these segments going ahead. These volumes present the corporate’s continued portfolio energy.

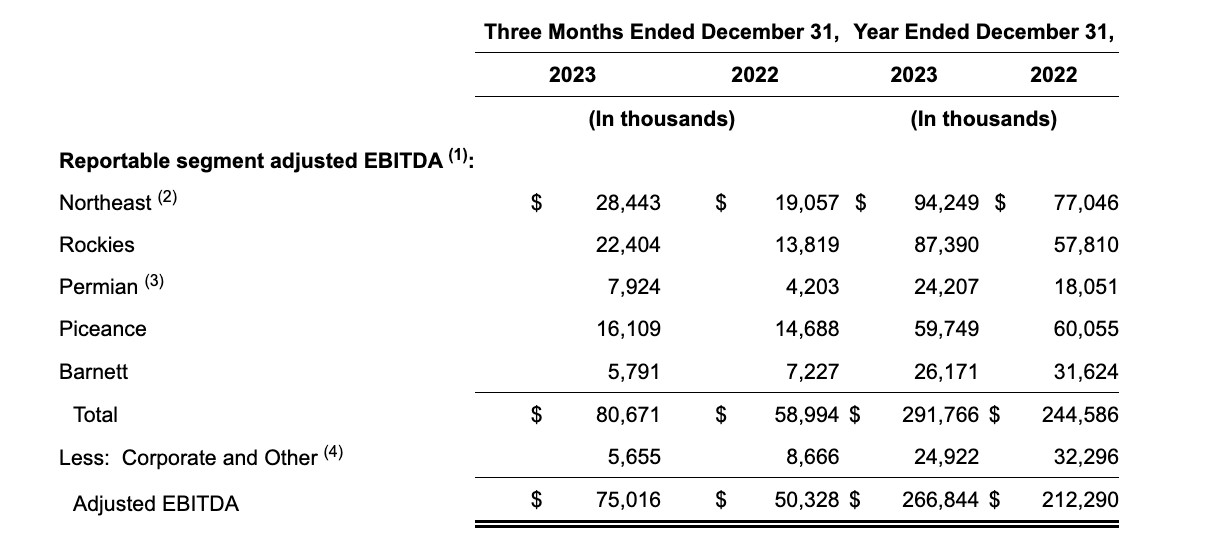

Summit Midstream Companions Financials

The corporate’s monetary image has improved dramatically quarter over quarter.

Summit Midstream Companions Press Releasee

The corporate’s quarterly adjusted EBITDA elevated by greater than 50% YoY, and the corporate’s 12 months EBITDA elevated by greater than 20%. The corporate’s present steerage for 2024 is a lower than 10% EBITDA improve, however it’s nonetheless a slight decline from how strongly the corporate completed the 12 months. Nonetheless, the corporate’s 2024 steerage signifies that that would decline barely.

Nonetheless, the corporate managed to beat it is prior steerage. We stay optimistic that the corporate will are available and the upper finish of its steerage.

Summit Midstream Companions Press Releasee

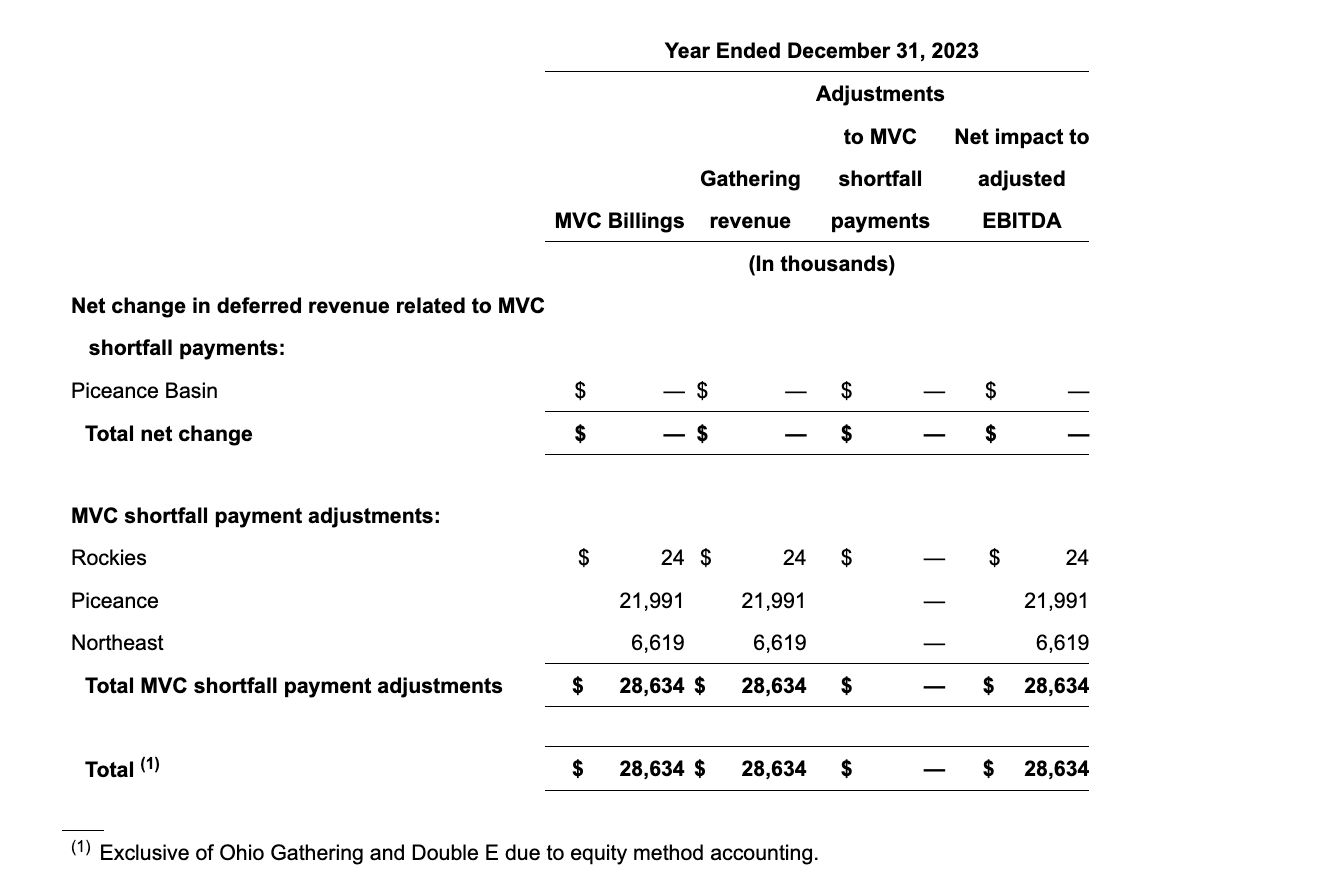

A priority throughout the firm’s portfolio is MVCs, notably in Piceance. These are prices for purchasers not assembly minimal volumes, which is sort of $30 million per 12 months, nearly $22 million of which is from the Piceance. No firm desires to pay MVCs, it is based mostly on a contract that they signed at a distinct time.

Sooner or later the contract will finish and the MVCs will go in the direction of 0. That can damage Summit Midstream Companions. A powerful environmental enchancment is required to alter this in pricing. The corporate’s total monetary image and its money circulate stay fairly sturdy.

Summit Midstream Companions Outlook

The corporate’s outlook is for continued success in its portfolio.

Summit Midstream Companions Press Releasee

Piceance continues to indicate no properly connections, which explains the MVCs. The corporate’s steerage proper now could be for ~200 properly connections, a 30% decline from 2023, and a regarding preliminary steerage. Nonetheless, with present costs, that is not notably surprising. The corporate’s properly connections on the finish of the day is predicated on pure gasoline costs and their energy.

The corporate expects on the center of its steerage a ~10% decline in volumes, one other signal of weakening costs. Nonetheless capital expenditures might be greater than manageable and volumes will are available sturdy throughout the corporate’s segments. That outlook signifies that the corporate will probably proceed to generate sturdy money circulate.

The true query right here is the corporate’s debt.

The corporate has nearly $1.4 billion in debt costing it greater than $100 million in annual curiosity. That’s dramatically hurting the power to generate shareholder returns. The corporate’s shareholder returns could possibly be greater than its market cap assuming it had no bills. The corporate’s debt comes due beginning subsequent 12 months.

The corporate is clearly directing its DCF to drive returns, however with $150 million in annual DCF, it might probably solely achieve this a lot. Meaning by the point this debt is all due, the corporate can pull its debt to under $1 billion. Nonetheless, present rates of interest and the way they alter versus 2 years in the past, is dependent upon the corporate’s means to refinance.

That is as a result of if the corporate’s DCF doubles, it not has any additional money to pay down debt. We factor that is unlikely given present forecasts for rate of interest cuts. The corporate’s rates of interest are at 8.5% and if it might probably present a capability to pay down debt, a 1% decrease price might save $20+ million in curiosity. We expect there is a ~20% likelihood the corporate goes bankrupt.

Nonetheless, given money circulate and upside, the funding continues to be price it.

Thesis Threat

The biggest danger to our thesis is refinancing. There isn’t any doubt that Summit Midstream Companions should refinance its debt. With altering rates of interest and continued uncertainty within the crude markets, the corporate may not be capable of refinance its debt, or curiosity obligations could be so excessive that the corporate will get trapped.

That mixture might lead to chapter or a sluggish debt for the corporate. The corporate’s administration is doing one of the best they’ll, however there is no assure their technique pans out.

Conclusion

Summit Midstream Companions is an extremely dangerous funding. The corporate has a lot debt, with the related rate of interest bills, that even a rise in rates of interest might push it out of business. Nonetheless, the corporate is doing one of the best it might probably, making an attempt to repurchase its debt at a reduction or pay it off.

Nonetheless, even in a low pure gasoline worth surroundings, the corporate is enhancing its portfolio and doing properly. The following two years might be intense for the corporate. The corporate is predominantly reliant on the markets. If it might probably survive although, it might probably generate sturdy shareholder returns, making the corporate a beneficial funding.