chinaface

Funding thesis

Suncor Power (NYSE:SU) is an absolute oil and fuel celebrity, given the corporate’s robust profitability, which permits it to generate substantial free money flows. The administration’s capital allocation method is phenomenal as the corporate efficiently balances between reinvesting within the enterprise, holding a clear steadiness sheet, and holding shareholders pleased with stable dividend payouts and inventory buybacks. The corporate is prepared to capitalize on tailwinds for vitality commodities markets, which I describe in my evaluation. Furthermore, my valuation train means that the inventory is massively undervalued. All in all, I assign Suncor a “Strong Buy” score.

Firm data

Suncor is an built-in vitality firm headquartered in Calgary, Canada. The operations embody oil sands improvement, manufacturing, and upgrading; offshore oil and fuel; petroleum refining in Canada and the U.S.; and the nationwide Petro‑Canada retail distribution community.

The corporate’s fiscal yr ends on December 31. Suncor operates through the next segments: Oil Sands, Exploration & Manufacturing [E&P], Refining & Advertising and marketing [R&M], and Company. For the first nine months of 2023, Oil Sands accounted for 58% of the full SU’s pre-tax earnings, and R&M’s share was 39%.

Financials

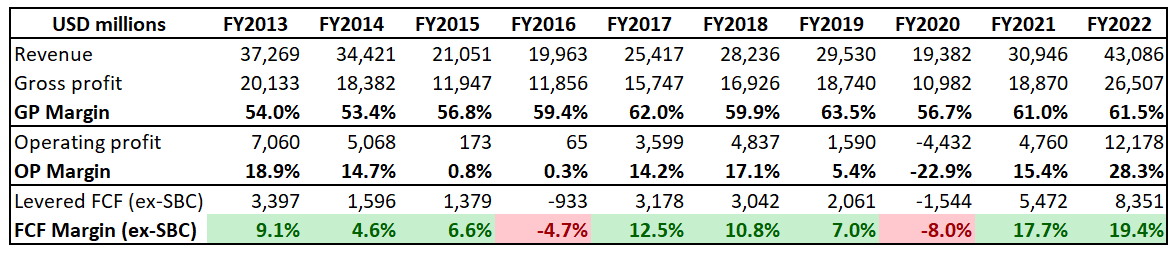

The corporate has demonstrated stellar monetary efficiency during the last decade. Income was considerably unstable given the character of Suncor’s enterprise, the place the highest line of oil and fuel firms closely is determined by the cyclicality of commodity costs. However even throughout years of low oil costs, the corporate delivered respectable profitability and free money circulation [FCF] with the one adverse outlier within the COVID-19 panic yr, 2020. The staggering nearly 20% FCF margin in 2022 suggests the corporate is robust in absorbing intervals of sky-high oil costs.

Writer’s calculations

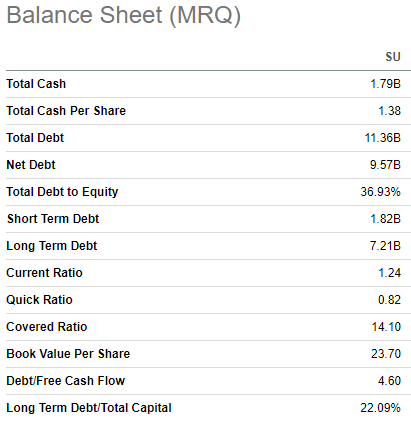

Suncor’s vast FCF metrics enable the corporate to efficiently steadiness between sustaining a wholesome steadiness sheet, increasing operations in a capital-intensive enterprise, and holding shareholders pleased with constant dividend payouts and inventory buybacks. Liquidity metrics are agency and the leverage ratio could be very prudent. A sound and balanced capital allocation method is an efficient high quality signal for me as an investor as a result of it demonstrates that the corporate’s earnings are deployed effectively and strategically to maximise shareholder worth. That mentioned, I consider that the at present supplied by the inventory’s 5.1% dividend yield is secure and has stable development prospects, given a really reasonable 37% payout ratio. The newest 5% dividend enhance was introduced a month ago.

Searching for Alpha

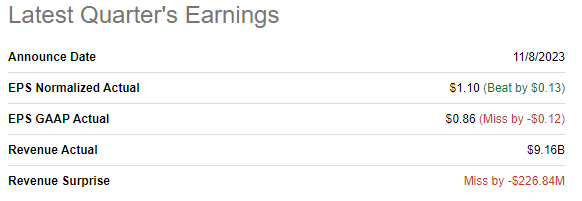

The newest quarterly earnings had been launched on November 8, when the corporate missed consensus income and EPS estimates. However, there was a constructive shock by way of the non-GAAP EPS. Income decreased by 16.4% on a YoY foundation as a result of decreased crude oil costs.

Searching for Alpha

Regardless of income lower, the corporate delivered a stable quarter from the profitability perspective. The working margin was notably above 20%, which allowed to generate $1.9 billion in FCF, which helped to additional solidify the corporate’s monetary place.

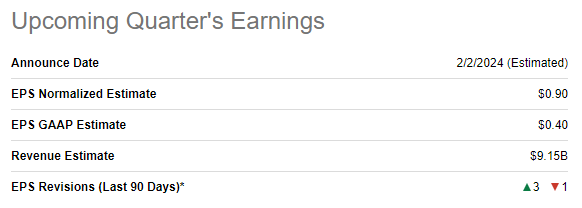

The upcoming quarter’s earnings launch is scheduled for February 2, 2024. Quarterly income is anticipated by consensus at $9.15 billion, which signifies a 12% YoY decline because of decreased crude oil costs. The adjusted EPS is anticipated to observe the underside line and shrink from $1.36 to $0.90.

Searching for Alpha

The income decline in 2023 shouldn’t mislead traders as a result of inherent cyclicality of oil and fuel firms’ revenues. Furthermore, it’s essential to recall that final yr was an outlier for crude oil costs after large panic in nearly all commodities markets after Russia’s invasion of Ukraine, which led to the financial isolation of one of many largest world crude oil exporters.

This yr, crude oil costs demonstrated softness in comparison with the 2022 value spike. Nonetheless, you will need to keep in mind that the largest oil consumer, america, noticed the tightest financial coverage over a number of many years. It was weighted on the financial exercise stage, leading to weaker oil demand. Nonetheless, regardless of the cruel setting, oil costs had been high in 2023. This week’s Fed’s announcement that three rate cuts are on the desk in 2024 is nice information for commodities markets. Decrease Federal funds charges imply decreased borrowing prices for companies and people, seemingly stimulating financial exercise and funding, in the end fostering elevated demand for vitality commodities out there.

Aside from the constructive shifts within the U.S. financial coverage, I see a pair extra stable tailwinds for the oil and fuel business. Joseph Biden’s administration aggressively utilized the U.S. Strategic Petroleum Reserve [SPR] in 2022 to stem inflation and lately started to refill it. As stock ranges in SPR are at multidecade lows, I believe the tailwind is stable and is prone to last longer. Additionally it is necessary to needless to say the worldwide geopolitical state of affairs could be very unsure with two large ongoing navy conflicts. A number of oil-rich nations are concerned in these conflicts, each straight and not directly. Sure, plainly oil sanctions against Russia do not work, however aside from geopolitical uncertainties within the Center East, we have now lately seen escalating territorial disputes between oil-rich Venezuela and Guyana.

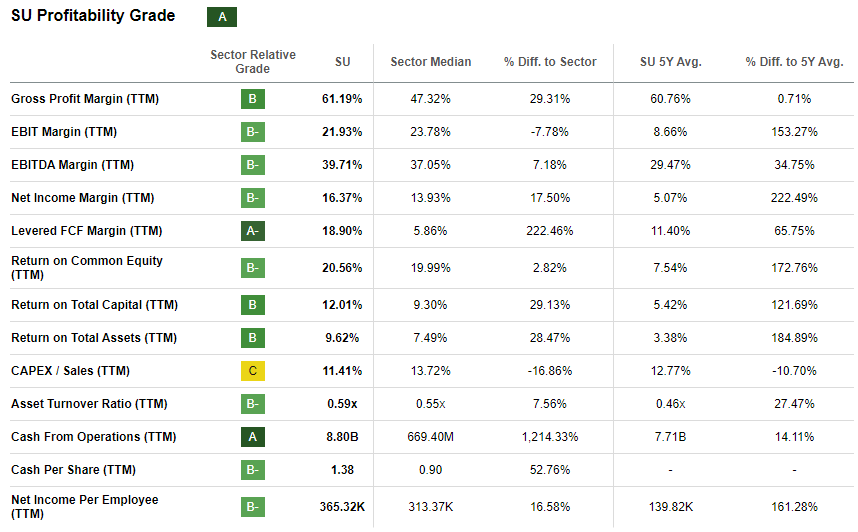

That mentioned, business tailwinds appear to be robust sufficient to help Suncor’s high line over the subsequent years. However for worth traders high line and FCF are the components that matter probably the most. Suncor traditionally has demonstrated exceptional profitability, being best-in-class throughout a number of key metrics.

Searching for Alpha

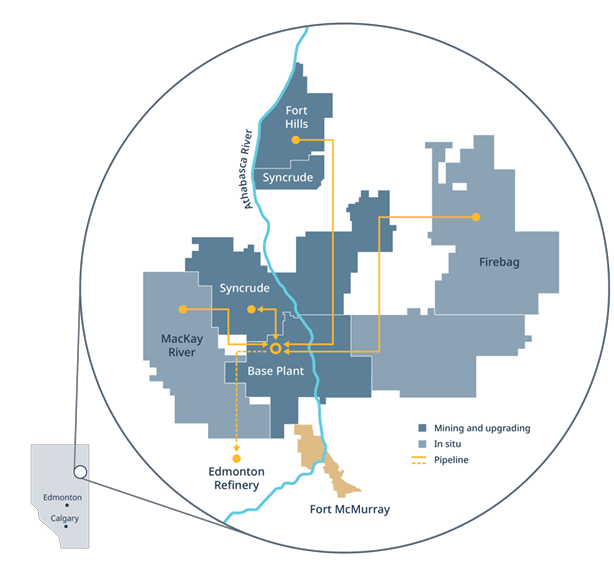

Suncor’s stellar profitability is achieved with a diversified base of high-quality property which counterpoint one another. Oil sands reserves have stable longevity with an estimated 26 years and the geographical location of key fields additionally helps to enhance effectivity. Websites are in shut proximity and linked by pipeline which permits to optimize provide chain and produce down prices. The corporate’s vast profitability metrics enable it to speculate closely in capex to additional enhance infrastructure and create extra alternatives to drive extra effectivity.

Suncor’s newest earnings presentation

Valuation

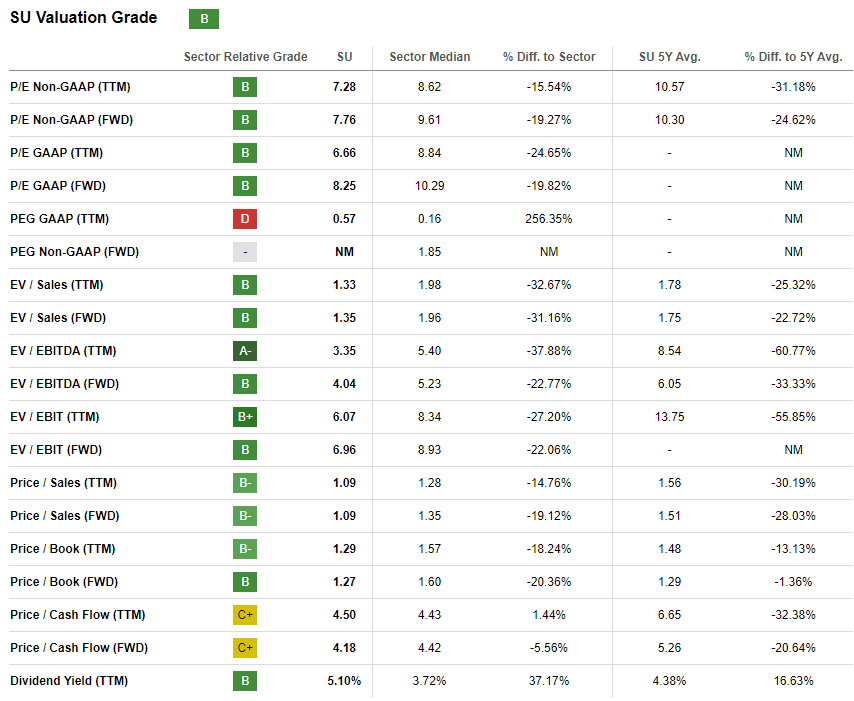

The inventory value elevated by 3.5% year-to-date, considerably lagging behind the broader U.S. market. Nonetheless, SU demonstrated higher 2023 efficiency than the American vitality sector (XLE). Seeking Alpha Quant assigns Suncor’s inventory a beautiful “B” valuation grade as a result of ratios are at present considerably beneath the sector median and the corporate’s historic averages. That mentioned, the inventory seems very attractively valued from the attitude of valuation ratios.

Searching for Alpha

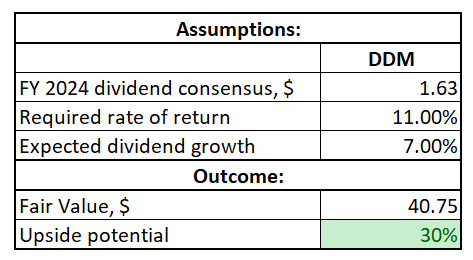

SU has constantly paid dividends during the last three many years. Subsequently, the dividend low cost mannequin [DDM] simulation seems like a dependable valuation technique. I exploit an 11% WACC as a required price of return. I incorporate $1.63 as the present dividend, which is the consensus estimate for FY 2024. Suncor has a robust dividend growth document. To be conservative I exploit a 7% final 5 years CAGR.

Writer’s calculations

In line with my DDM calculations, the inventory’s truthful value is barely beneath $41. This means a 30% upside potential from the present ranges. To sum up, Suncor’s inventory could be very attractively valued.

Dangers to think about

The truth that the U.S. averted recession in 2023 does not mean that it could possibly achieve this infinitely. In case of a recession on the planet’s largest financial system, the commodities market will extremely seemingly be adversely affected, which is able to undermine Suncor’s earnings. However, OPEC and OPEC+ demonstrated a number of instances this yr that the group is ready to chop oil manufacturing to handle adverse shifts within the world oil demand. OPEC’s flexibility to adjust supply seems like a stable safety towards sharp oil value drops except a brand new black swan, just like the pandemic, seems.

Investing in oil and fuel firms may not be an excellent match for long-term traders, given the secular shift to scrub vitality. Whereas it’s inconceivable to think about our world with out utilizing oil and fuel, the business could be very mature and the U.S. Power Sector SPDR Fund ETF (XLE) demonstrated no inventory value appreciation during the last ten years. Investing in firms like Suncor higher matches dividend traders and those who’re in search of a chance to document capital positive factors on the business’s cyclicality.

Backside line

To conclude, SU is a “Strong Buy”. The corporate has been traditionally robust in absorbing excessive oil costs and my evaluation means that the current softness in oil costs is non permanent and a number of business tailwinds are behind Suncor’s again. The inventory at present gives a beautiful 5.1% dividend yield and a large 30% upside potential, in accordance with my valuation evaluation.