Jeremy Poland

SunPower Company (NASDAQ:SPWR) is along with Sunrun (RUN) and Sunnova (NOVA) one of many main suppliers and installers of distributed photovoltaic programs in america. Since January 2021, the share worth skilled a regular decline, and within the meantime, SPWR has considerably restructured its enterprise. As I believe was clear from my earlier Sunnova’s article, I’m not notably interested in this phase of the photo voltaic trade, as it’s characterised by excessive set up and upkeep prices, problem in constructing a scalable enterprise, and excessive preliminary capital necessities. Furthermore, SunPower seems to me to be an early-stage firm, which has bought all its most respected belongings and now needs to focus solely on the residential phase. It certainly now immediately or not directly installs photovoltaic and storage programs for people, providing them by direct sale, leasing, or loans. In my opinion, the poor monetary outcomes reported, and the stringent competitors might additional weigh on the long-term outcomes. Nonetheless, within the brief time period, administration presented a plan within the convention name to scale back working prices by about $100m. The lower within the worth of photo voltaic panels and vitality storage programs, along with the tax credit score launched by the Inflation Reduction Act could also be further optimistic elements to assist the monetary ends in the following 2 years. Nevertheless, I imagine this is not going to be sufficient to achieve a revenue, particularly contemplating the more and more robust competitors from China, thus I at the moment fee the inventory as a Promote.

Listed here are hyperlinks to my latest articles on renewable-related firms: Clearway Energy (CWEN), Ormat Technologies (ORA), Northland Power (NPI:CA), TransAlta (TAC), Innergex (INE:CA) and Enlight Renewable Energy (ENLT).

Enterprise overview publish restructuring

SPWR has considerably restructured its enterprise prior to now 4 years: in August 2020 it accomplished the spin-off Maxeon Photo voltaic Applied sciences (MAXN), a Singapore-based firm coping with design, distribution and set up of photovoltaic programs. In October 2021, it finalized the acquisition of Blue Raven Solar for $145m. Then in February 2022 it proceeded to the sale of the Commercial & Industrial enterprise unit to TotalEnergies SE (TTE) for $250m, together with $60m of earn-out topic to regulatory evolution.

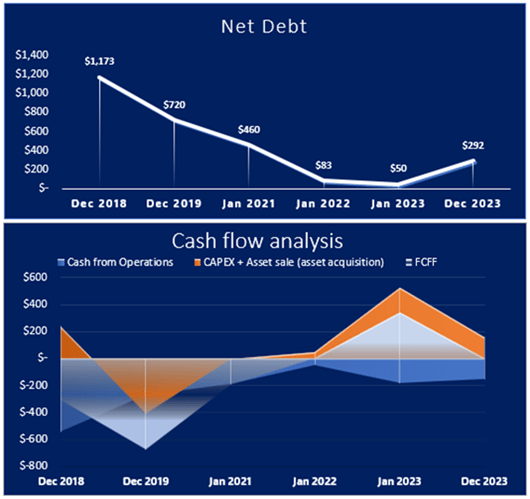

This restructuring course of allowed SPWR to supply optimistic Investing Money Flows which, though coupled with damaging Working Money Flows, led to optimistic FCF aimed to scale back web debt from $1.1B as at Dec18 to $292m as at Dec23. In the identical interval, whole belongings dropped from $2.4B to $1.3B, with PP&E declining by $755m, from $932m as at Dec18 to $177m as at Dec23. Though the present enterprise is downsized, it has many similarities from an operational standpoint with the previous one, because the photo voltaic panels put in by SPWR are nonetheless bought by MAXN by MSAs (master service agreements).

SPWR SEC Filings and Writer’s Evaluation

The deleveraging carried out by administration has definitely made the corporate extra financially safe, thereby facilitating the enterprise enlargement within the residential phase. However, the stability sheet exhibits a scarcity of present belongings as at Dec23, with a fast ratio of 0.64x. This, for my part, will trigger an extra improve in debt within the following quarters.

The corporate presents 2 foremost merchandise, to each single-family and multi-family residential clients:

OneRoof consisting of concrete roofing tiles substitute with a totally built-in roof plus-solar answer, making certain a 25-year guarantee for panels and 10-year guarantee for batteries. Photo voltaic panels are primarily bought from MAXN whereas inverters from Enphase Vitality (ENPH).

SunVault™ Storage consisting of a storage system linked to OneRoof, enabling the vitality utilization even at night time. SPWR additionally presents a real-time monitoring service by way of PC or cellular with mySunPower.

Since FY21, SunPower additionally presents monetary providers together with loans organized by their third-party lending companions, in some circumstances for no cash down, or leases at aggressive charges. The introduction of this service, already applied by Sunnova, goals to supply photo voltaic panels electrical energy as a service paid for by the patron by lease or mortgage.

FY23 outcomes and FY24-FY25 outlook

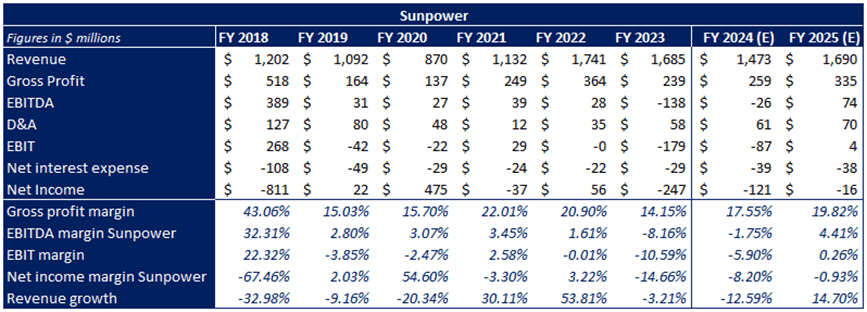

After a part of decline resulted in FY20, revenues resumed a optimistic trajectory, aided principally by the brand new inclusive leasing and loans providing. In FY23, revenues fell by 3.2% on account of lower-than-expected demand within the loans phase, which was deprived by excessive rates of interest disincentivizing clients from coming into this sort of contract. Leasing, however, recorded wonderful outcomes, virtually ending the money made obtainable by the financing companions.

SPWR SEC Filings and Writer’s Estimates

In FY24 outlook, administration expressed a willingness to focus extra on rationalizing prices and rising margins. That’s the reason I imagine that revenues will proceed to say no on account of low demand and the persistence of excessive rates of interest within the economic system. As well as, administration goals to attain a gross revenue of 17-19% for FY24, rising to twenty% in FY25, with GAAP web revenue anticipated within the -$80/160m, a considerable enchancment in contrast with -$247m in FY23.

If the plan to scale back prices is profitable, SPWR will transfer nearer to profitability, additionally as a result of optimistic impact of the brand new tax credit launched permitting lower-cost capital elevating and decrease money outlays. Nevertheless, elevated curiosity overhead on account of new debt and better depreciation will act in the other way dampening the associated fee enchancment. I count on a discount within the worth of photo voltaic panels for SPWR in FY24 and FY25, due to each the coming into into a brand new MSA with Maxeon and the anticipated drop in batteries worth arising from the lower within the price of lithium. These two elements ought to assist enhance the associated fee construction by performing immediately on the gross margin. The majority of the associated fee financial savings introduced within the convention name refer principally to those elements slightly than to precise monetary engineering operations. Such operations in truth require vital funding within the manufacturing chain and should not achievable within the brief time period. In conclusion then, I count on that for the following two years we’ll see an enchancment within the working outcomes, however these can be pushed by exogenous elements slightly than by administration’s work.

Friends Evaluation

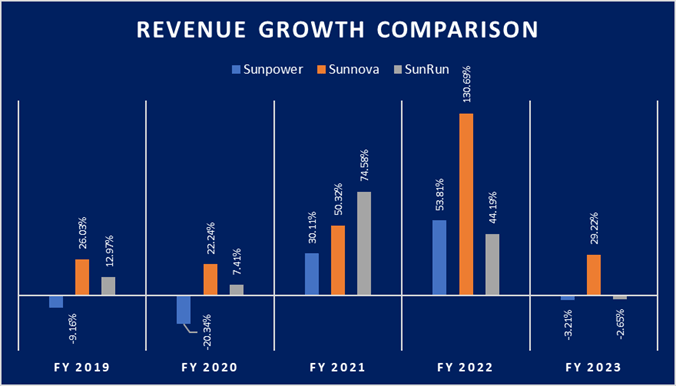

SunPower operates in a really aggressive trade for my part, which is why I’ve doubts concerning the precise implementation of the plan mentioned above. Each SPWR, RUN and NOVA are at the moment attempting to decrease the price of providers provided as a lot as doable to realize market share over opponents. This generates decrease margins and working money flows, requiring further debt to implement the traditional actions required by the enterprise. Taking a look at income progress, it’s fairly obvious that Sunrun and Sunnova have skilled higher progress stability than SunPower during the last 5 years.

Firms SEC Filings and Writer’s Evaluation

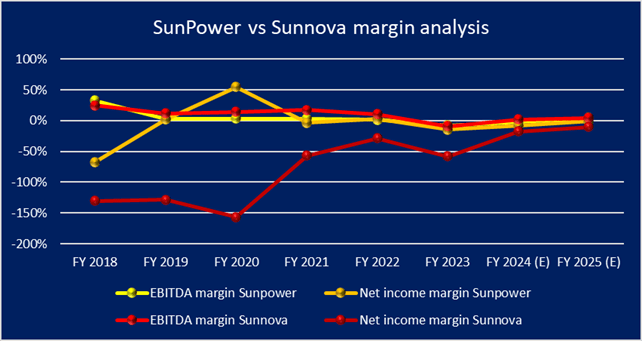

By evaluating SunPower and Sunnova marginality, it may be famous that SPWR recorded larger profitability in the identical time-frame. Nevertheless, Sunnova development is clearly enhancing, due to the turnover progress permitting a discount in marginal prices, whereas SunPower one was flat. The evolution of this competitors within the coming years may have super relevance for the way forward for SPWR. Right now, I’ve discovered no cause to think about SunPower higher positioned than its two foremost opponents.

Firms SEC Filings and Writer’s Evaluation

Chinese language Competitors as a foremost danger

David R. Baker of Bloomberg, in his March 12, 2024 article, highlighted how subsidies from the Inflation Discount Act, particularly, 7 cents per watt for home panel factories that use imported cells, should not sufficient to distinction Chinese language competitors. That’s as a result of imports from China are so low-cost that such subsidies can’t maintain US home manufacturing. He expects home costs for panels to plunge from ~$0.23/watt in 2024 to $0.16/watt by year-end 2025. Though SPWR isn’t a photo voltaic panel producer, virtually the entire provide is supplied by MAXN. The latter might notably endure from Chinese language competitors, which is why will probably be essential to observe its efficiency to which SunPower can be inextricably linked.

Different Dangers

For my part, there are additional 5 dangers to think about:

Rates of interest danger is among the foremost elements affecting firms on this trade. SunPower, following the intensive restructuring marketing campaign, has its debt below management as of December 2023. Nevertheless, between FY24 and FY25, the event of the residential enterprise may lead SPWR to wish further debt. The latter, given the present rate of interest surroundings, may lead to a major and sudden improve in curiosity expense in a brief time frame, additional damaging profitability.

SPWR has skilled very damaging monetary outcomes to this point, and the identical applies to the 2 different trade leaders, NOVA, and RUN. This highlights an underlying drawback of this sort of enterprise devoted to people. Making such many installations is considerably costlier than making a single utility-scale set up, in addition to requiring an working construction by which it’s troublesome to attain economies of scale. Furthermore, upkeep prices may improve exponentially, given a rising variety of purchasers unfold throughout america. That is the primary cause why the three firms should rely generally on third-party firms, resulting in an extra lower in margins because the third-party accomplice may also demand a revenue.

Tesla, Inc. (TSLA) seems to be an amazing risk for all firms within the trade. That’s as a result of TSLA foremost objective is to offer a whole ecosystem ranging from the Electrical Automobile to the charging station, batteries, and photo voltaic panels. These options permit Tesla to have the ability to have extra flexibility in pricing than its opponents, even promoting beneath the price of manufacturing if vital as a result of synergies created between the completely different merchandise it markets.

In FY22 Annual Report, plenty of regulatory dangers are reported. For my part, probably the most related is the chance of adjustments within the Solar Investment Tax Credits. Administration itself reported that this might materially and adversely have an effect on each the enterprise and the monetary outcomes.

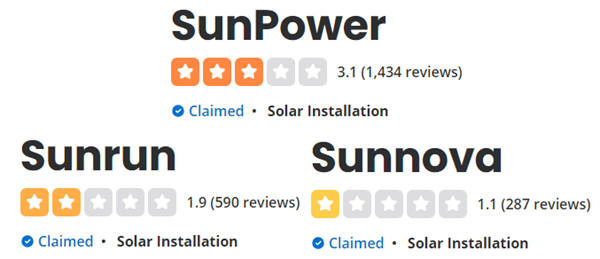

The shopper care service, which is meant to be one of many pillars of the corporate, as admitted by the corporate on its web site, at the moment hides a number of darkish spots. SunPower presents a really unhealthy ranking on the Yelp website, with an total 3.1 stars. Though its ranking is larger than that of its two opponents, I contemplate this information not good for the trade. The opinions discuss roof issues in installations, not working programs, too gradual upkeep, and others that made me imagine that at the moment the service doesn’t fulfill the shopper base.

www.yelp.com

Valuation

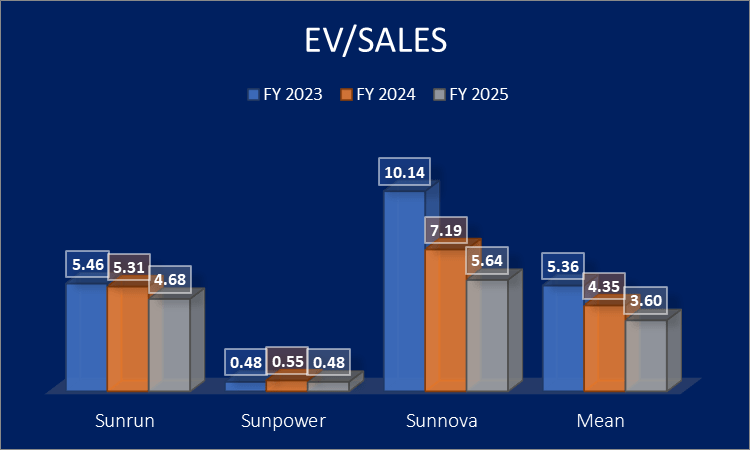

SPWR has damaging working money flows, in addition to producing losses in many of the latest fiscal years. The identical applies for the 2 foremost friends. Because of this, I used to be not capable of carry out both a DCF evaluation or a multiples evaluation with typical earnings-based ratios. Nevertheless, by wanting on the EV/gross sales ratio, it may be famous that SPWR is at the moment less expensive than friends. SunPower has certainly a FY24E EV/Gross sales of 0.55x, versus 7.19x of Sunnova and 5.31x of Sunrun. In my opinion, this distinction is partly attributable to 1) the restructuring of SunPower, which was negatively considered by the market, resulting in a lower in its market cap and a pair of) SunPower’s decrease debt contributing to a decrease EV in contrast with friends.

seekingalpha.com and Writer’s Evaluation

Conclusion

As could be inferred from the earlier paragraphs, I at the moment fee SunPower as a Promote. The primary cause for this ranking considerations the enterprise, which, for my part, will current problems in turning a revenue even within the coming years. Creating an environment friendly organizational construction for the set up and upkeep of photo voltaic panels and batteries has been troublesome to this point, and I see no main elements within the area to reverse such a development. Furthermore, the restructuring characterizing the SPWR’s operations since 2020 has excluded some fascinating enterprise areas, notably Business & Industrial BU, which was characterised by larger profitability than residential, as a result of bigger measurement of installations and orders.

However the above, I imagine that the SPWR depressed valuation in contrast with foremost friends may signify a short-term funding alternative for a risk-averse investor assured that multiples ought to align with these of NOVA and SUN. In the long term, nonetheless, the concerns I made about your entire sector stay, making it, for my part, unattractive to a long-term investor. The one different that I believe could be vital to alter my thoughts could be the emergence of an undisputed chief out there, with higher pricing energy due to dominant place within the trade. For now, we’re removed from this epilogue as SunPower isn’t the market chief I’m searching for.