Klaus Vedfelt

One of many huge classes from the 2010-2020 setting was that headline payrolls might improve considerably with out placing upward stress on inflation. This may be complicated as a result of there’s typically an assumption that extra jobs imply extra demand and better costs. Nevertheless it’s extra complicated than that. Consider it like inventory costs. Costs will rise when the eagerness of consumers outpaces the eagerness of the sellers whatever the depth of the market. The identical primary factor occurs within the labor market. So, even if in case you have an growing variety of individuals working, the price of that labor can truly gradual if capital has extra negotiating energy over labor. That is primarily the story of the complete decade of the 2010s when the labor market expanded by a median of 190K monthly and inflation was 1-2% virtually the complete time. That occurred, largely, as a result of capital had so a lot negotiating energy over labor.

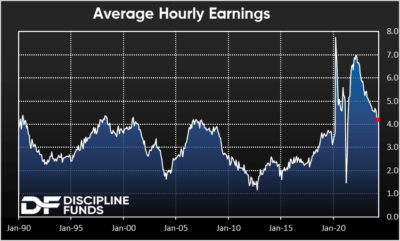

And one of the best ways to see that relationship is in hourly wages. Briefly, does capital have to pay you extra to work? And the plain reply within the 2010s was no.

Importantly, the identical development is taking part in out now and Powell has been very clear about this. In the newest press convention, he mentioned:

“in and of itself, strong job growth is not a reason for us to be concerned about inflation”

So the headline employment knowledge can look sturdy (and has) and you may nonetheless get a falling fee of inflation if capital is not compelled to pay up for labor. And what will we see in hourly earnings? This month’s labor report confirmed one of many sharpest slowdowns of latest years with the speed of change slowing from 4.6% to 4.2%. I count on this to gradual additional and stabilize within the excessive 3% vary throughout 2024. However for now, the development is clearly nonetheless to the draw back and that’s according to a labor market the place staff have much less negotiating energy than capital. And that ought to finally movement by to decrease charges of inflation.

I’m a damaged report on this by now, however this isn’t remotely near what occurred within the Seventies or Nineteen Forties after we noticed giant resurgences in inflation. These narratives look useless within the water with wage charges falling the way in which they’re. So, regardless of a comparatively sturdy labor market, the underlying traits are according to a labor market that is not overly tight. You possibly can even argue that metrics like full time employment, short-term assist and the give up fee are according to a labor market that’s free. So do not let the headline determine idiot you into believing that the labor market is essentially tight.

What does all of it imply for the Fed and short-term fastened revenue traders?

This labor report provides the Fed some respiratory room to attend on fee cuts. The labor market is robust sufficient that they need not rush something. Inflation remains to be shifting in the correct path, however it’s been sticky sufficient in early 2024 that they do not wish to threat a resurgence in inflation from reducing too early. That is the best situation for the Fed. They’ve managed to deliver wages down and funky the labor market with out inflicting a dramatic decline in jobs. And which means they do not need to rush to conclusions and reduce charges simply but.

All that mentioned, the calendar for potential cuts is getting attention-grabbing now. I had been within the June camp and creeping to July, however now I’m beginning to suppose that November could be the primary reduce. And this is the issue – I feel we’ll be at about 2.5% core PCE by Might, and if we proceed to get sturdy employment studies, then the Fed’s going to be just a little uneasy about reducing in June. So June might be off the desk. July is a possibly, however similar primary story there the place core PCE remains to be a contact too excessive to make certain about development inflation. After which the following assembly is September which is simply three weeks from the election. Will they provoke their first reduce proper earlier than the election? Boy, I doubt it. I can solely think about the headlines there with individuals screaming that the Fed is working for the Democrats. And that leaves the November assembly and the December assembly which might imply two cuts in 2024.

It isn’t essentially unhealthy information. We proceed to see a really powerful setting for anybody who wants credit score, however we additionally see excessive rates of interest for anybody dwelling on a set revenue. So, I assume it is determined by which one you depend on extra as a result of excessive charges are unhealthy for brand new debtors and nice for savers.

Editor’s Observe: The abstract bullets for this text had been chosen by In search of Alpha editors.