ImagineGolf

Funding Thesis

Russian authorities simply ordered its oil producers to cut oil output to contribute to OPEC+ cuts. This comes on the similar time when EIA dramatically lowered its manufacturing estimate for US shale oil. The present narrative is looking for an oil worth of $100 a barrel this yr.

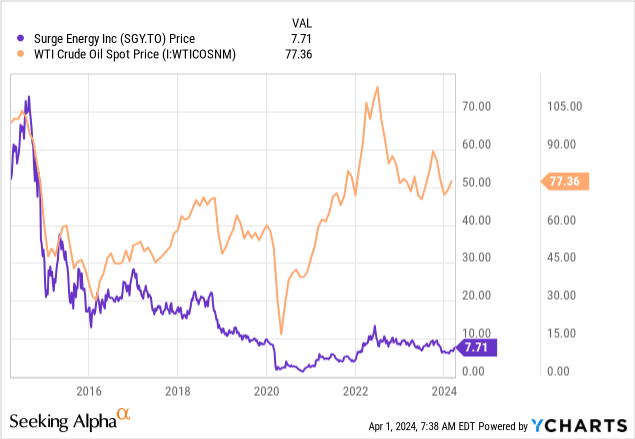

The narrative drives the inventory costs, and as a price investor, I might a lot slightly put money into occasions when the narrative requires $40 costs with no future for oil. Nonetheless, regardless of the bullish narrative, the shares of Canadian O&G producers stay low cost.

Surge Vitality (TSX:TSX:SGY:CA)(OTCPK:ZPTAF) has increased prices in comparison with its bigger friends, which makes its FCF technology extra delicate to grease costs. For my part, Surge is without doubt one of the finest methods play the thesis of a excessive decline in US shale oil manufacturing, driving the oil worth increased for longer.

In the long run, all of it is dependent upon valuation and your private perception in future oil costs. With the present close to $80 WTI strip worth and required 12.5% return, Surge shares counsel a 39% upside, which makes it a Purchase with a worth goal of C$11 per share.

Whereas tempting, regardless of a budget valuation and potential massive positive factors within the case of upper oil costs, Surge doesn’t presently make its approach to my private portfolio.

Introduction to Surge Vitality

Surge Vitality is a Canadian small-cap typical producer with operations throughout Alberta and Saskatchewan.

Its common manufacturing over the past yr was 24,438 boe/d (barrel of oil equal per day), with a profile consisting of 87% liquids. This generated $94M of FCF (12% FCF yield).

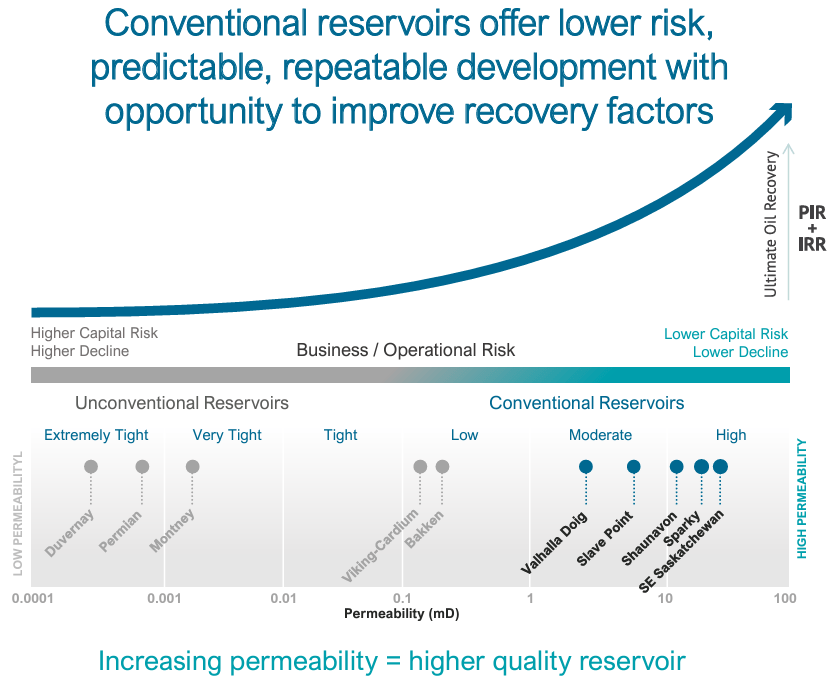

The corporate technique lies in long-cycle, low-risk, low-declines reservoirs. Whereas the bottom manufacturing decline price is about 23%, the corporate offsets this with water flooding.

See the evaluation of the standard reservoir traits as introduced by Surge within the graph under.

Standard Reserves (Surge Vitality Presentation)

If you’re new to the corporate, I might suggest to learn by the company’s presentation first.

Underestimated Belongings

Impartial firm Sproule assessed the value of Surge’s 2P (Proved+Possible) reserves at C$17.63 per share. This valuation assumes a ten% low cost price. Discounted by 15%, the worth could be C$14.6.

Surge focuses on typical reservoirs with excessive OOIP (Authentic Oil In Place) and low base declines. What precisely does it imply?

In line with Surge’s inner estimation, the corporate sits on over 3 billion barrels of web OOIP, of which 7.7% has already recovered. In Sproule valuation, Surge solely booked a restoration issue of 11.5%, which implies solely a further 3.8% restoration of the OOIP.

These booked restoration elements enormously underestimate the potential and longevity of those reservoirs, as typical reservoirs can usually attain as much as a 15-20% restoration issue on major manufacturing. Contemplating that secondary manufacturing by way of waterflooding is a core of Surge’s operations, we will add one other 10% restoration.

This represents a big quantity of recoverable oil and is a key a part of the funding thesis for long-term traders, because the share worth doesn’t mirror this actuality.

With over 13 years of future drilling packages and extra potential for waterflooding, Surge doesn’t must spend a penny on acquisitions for a very long time and might select to extend Capex at any time to spice up manufacturing in case of upper Oil costs.

2024 Steerage

In December, Surge launched its budget guidance for 2024. Capex is predicted to be C$190M, together with C$10M for water flooding. The drilling program contains 37 web wells within the Sparky space and 32 horizontal wells in SE Saskatchewan. That is anticipated to counter the declining manufacturing and to not improve manufacturing ranges.

With a steady manufacturing of round 25,000 boe/d, US$80 WTI, we will anticipate FCF earlier than debt compensation of round C$132M (17% FCF yield with a share worth of C$7.7).

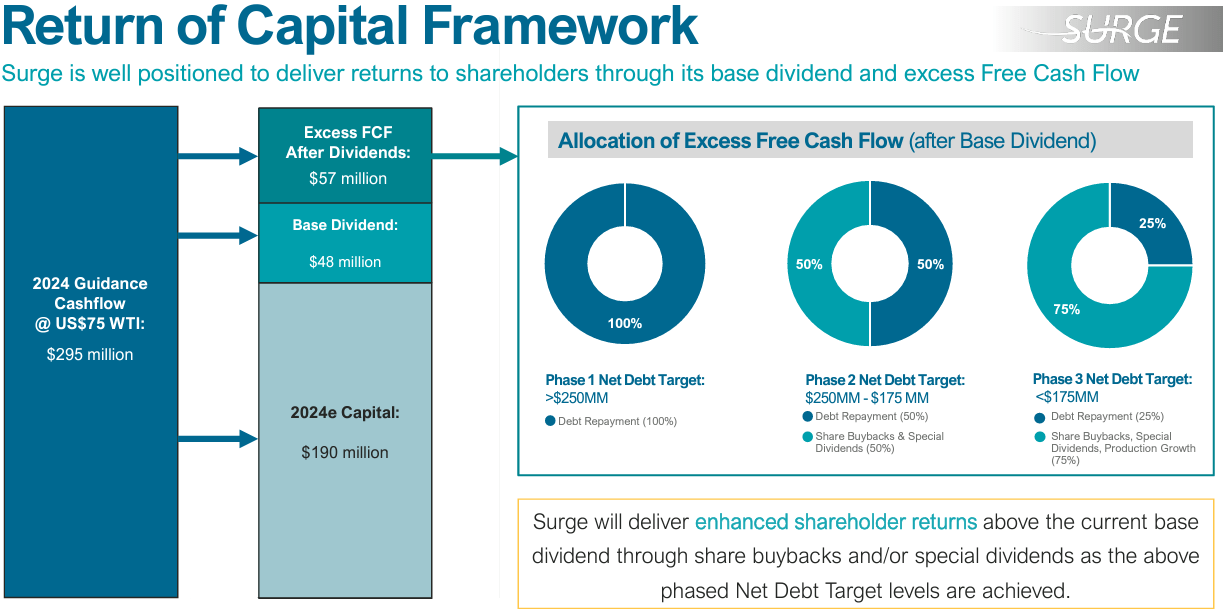

Improved Capital Allocation

Surge has outlined a strategic three-phase method to its capital allocation framework.

Capital allocation (Surge Vitality Presentation)

Part 1 focuses on debt compensation whereas holding the present dividend of C$0.48 per share (6.2% yield).

With $80 WTI, they need to attain part 2 at first of 2Q2024, and we may see a lift within the payout. The promised 50% payout may yield 8.5% by way of base dividends, particular dividends, and buybacks, whereas the opposite half of FCF would go to debt repayments.

Part 3 may very well be reached by the tip of 2Q2025, assuming $80 WTI costs. We may then see an additional improve in payouts.

Dangers

On account of its low-risk method and excessive manufacturing predictability, I assess the dangers as under friends’ common. Whereas the manufacturing danger profile is low, it can’t be stated about its sensitivity to grease costs.

I calculate the WTI worth wanted to earn sufficient money circulation to offset the manufacturing decline in a spread of $55-60 WTI. Whereas costs are presently increased and the corporate generates wholesome FCF, it shortly reverses when the worth strikes decrease.

Since 2015, when oil costs dropped and stayed decrease, the corporate was operating FCF destructive, and the CEO needed to concern new shares and considerably dilute shareholders. That is typical for a lot of small-cap firms and an excellent cause to demand increased returns for taking this danger.

Operational leverage is a double-edged sword. Whereas threatening in a low-price atmosphere, it might make for substantial positive factors in rising oil worth occasions. Because the 2020 lows, the inventory is up over 500%.

Valuation

Whereas I’ve already introduced the case of 2P-NAV valuation, I discover most Canadian O&G producers undervalued based mostly on this metric. It appears to me that the market doesn’t totally recognize the long-term lifetime of reserves, as if assuming the world doesn’t want oil 20 years from now.

Merely evaluating DACF (debt-adjusted money circulation) yields doesn’t inform the entire story both, because it doesn’t account for progress Capex.

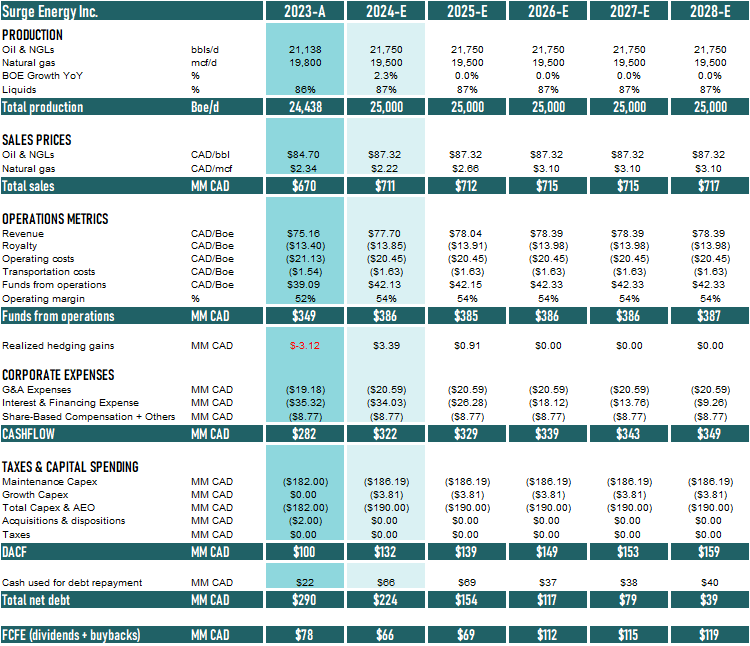

My method is by way of commonplace DCF (discounted money circulation) valuation. I’m constructing the base-case projection mannequin with the next:

- WTI of US$80 with a WCS differential of solely US$11, reflecting the approaching TMX expansion.

- AECO following the strip pricing, reaching C$3.5 in 2026. With a 13% gasoline manufacturing on a “boe basis,” the AECO pricing has little or no relevance in Surge valuation.

- Capex of C$190M for subsequent yr with flat manufacturing ranges, because the capital spending suggests.

- Zero tax as the corporate has a C$1.2B tax pool

- Whole debt of C$290M with capital allocation following Surge’s framework

- Totally diluted share depend of 101M

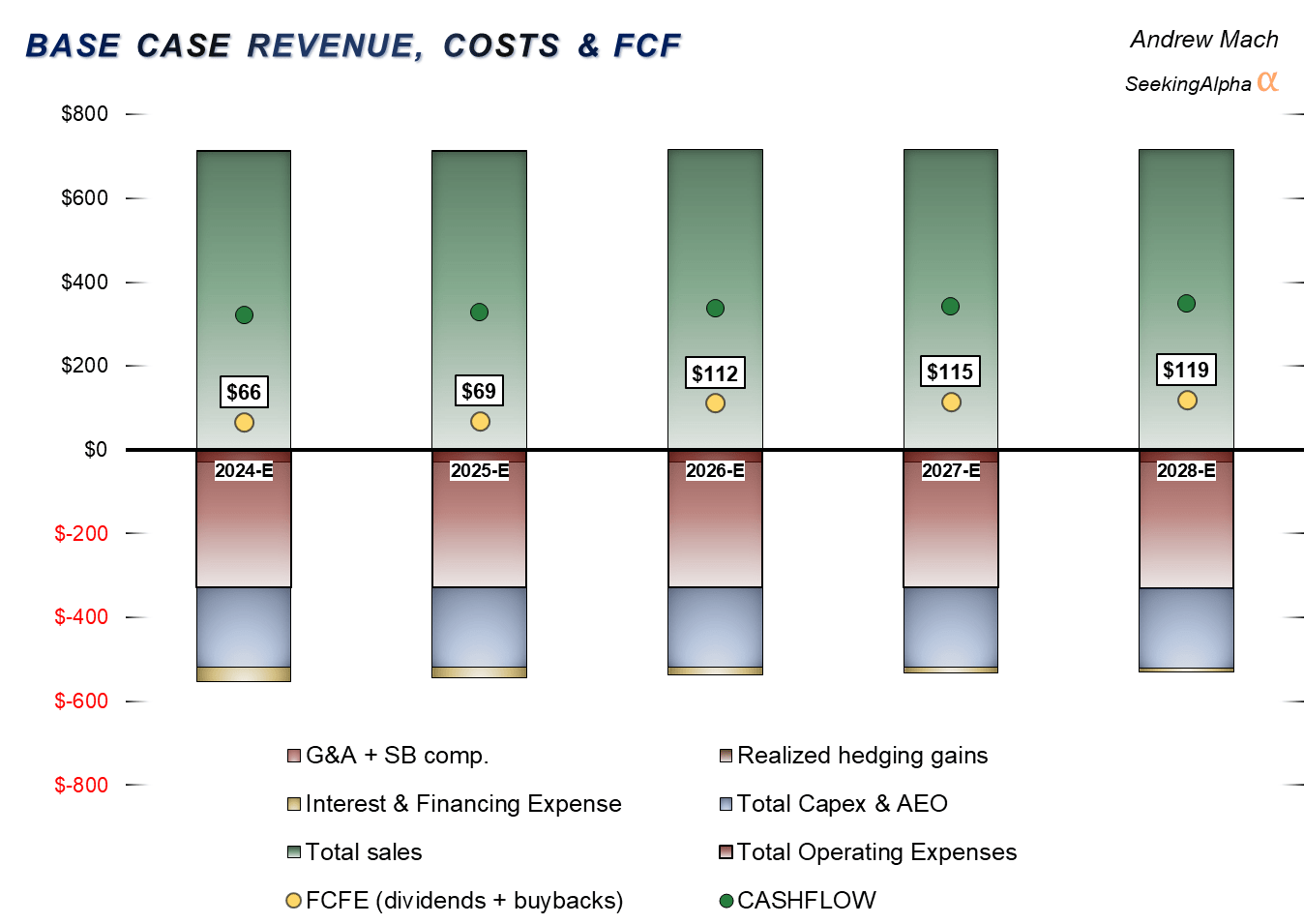

5 Years Projection (Writer’s Calculation)

The graph above summarizes the projection. Whereas flat manufacturing is nothing to write down about, the big 60% bounce in 2026 FCFE is attention-grabbing. C$112 allotted in direction of dividends and buybacks offers you a 14.4% yield.

That is after I anticipate solely 25% of FCF to be allotted to debt repayments. That is additional enhanced by decrease curiosity funds. Contemplating that Surge presently pays round C$35M, this could save round C$20M in 2026.

You possibly can evaluation all assumed numbers within the projection desk under.

5 Years Projection (Writer’s Calculation)

The following step to evaluate the worth is to low cost the ensuing dividends and buybacks by 12.5%, which I take advantage of throughout the Canadian O&G upstream sector so I can simply examine firms contained in the business.

Discounted Money Move Mannequin (Writer’s Calculation)

After discounting, the bottom case situation, assuming $80 WTI, ends in a good worth of C$11 per share, suggesting a hefty 39% upside to honest worth.

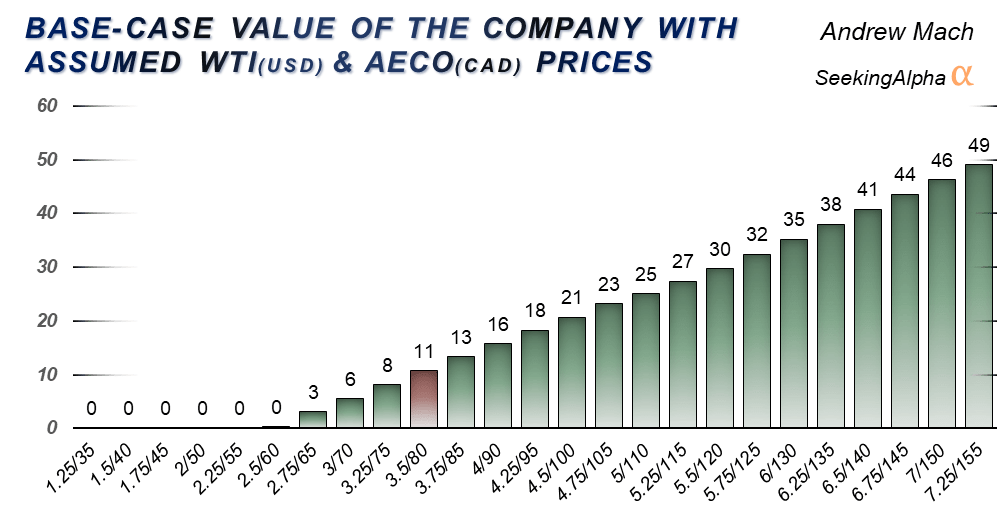

The desk under represents the honest worth of Surge inventory for a 12.5% return beneath completely different long-term O&G costs. This exhibits that Surge is presently pretty priced for $75 WTI.

O&G worth sensitivity (Writer’s Calculation)

Funding Determination

The long-term potential is there, with undervalued high-quality property and issues impring with debt repayments. The corporate has additional methods to extremely develop its reserves because of enhancement in its restoration elements by way of water flooding.

The short-term potential in share worth appreciation is as effectively. With excessive sensitivity to grease costs and the present bullish narrative for oil costs, Surge may very well be the very best performer in such occasions.

Whereas valuation outcomes level to undervaluation, I’ve my favourite in Crescent Level Vitality. You might be welcome to evaluation my CPG write-up.

CPG vs. SGY DACF & Development (Writer’s Calculation)

Put it merely – whereas buying and selling at the same yield, Crescent is rising its manufacturing by 10% yearly whereas Surge manufacturing stays flat.

Right here is the comparability of the up/draw back in share worth with the required 12.5% return, based mostly on my DCF valuation fashions beneath completely different pricing environments.

CPG vs. SGY sensitivity (Writer’s Calculation)

I do know that CPG is gassier, however even when I assume the AECO worth of C$0, CPG nonetheless offers me increased anticipated returns.

Traders have completely different approaches, and I consider that Surge’s inventory, with its present worth, makes a fantastic match for a lot of portfolios, particularly if you wish to wager on increased oil costs. I price the inventory as a BUY with a worth goal of C$11.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.