TERADAT SANTIVIVUT

Introduction

Final month, I issued the Simplify Volatility Premium ETF (NYSEARCA:SVOL) a downgrade to “hold” attributable to developments concerning their distributions and underlying holdings adjustments.

These developments have reversed and on this column, I’ll clarify why I’m altering my outlook to a “buy” score once more.

If you happen to’re not caught up on this saga, yow will discover the final article, here.

My buy-and-hold scores thus far have held up and been pretty well timed, though my protection did not begin till the previous few months.

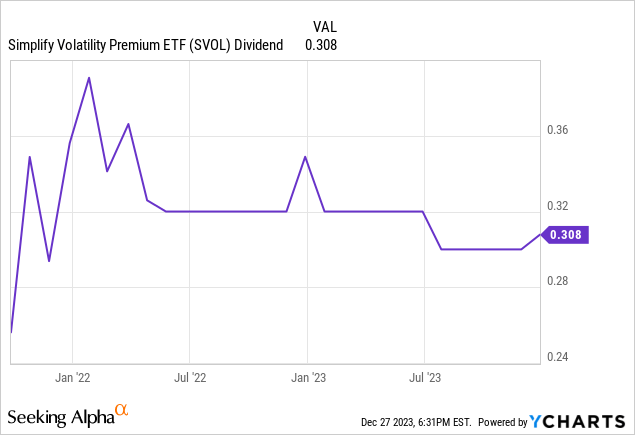

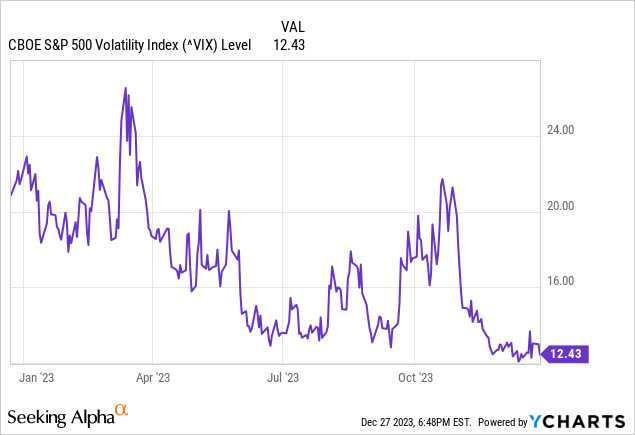

Determine 1 (In search of Alpha)

Overview

The Simplify Volatility Premium ETF (SVOL) is an ETF that’s quick the VIX, a gauge of volatility within the markets. Usually, SVOL is 0.2x-0.3x uncovered to being quick the VIX, however could find yourself with dynamic publicity day-to-day due to its positioning alongside the time period construction. Extra on that later.

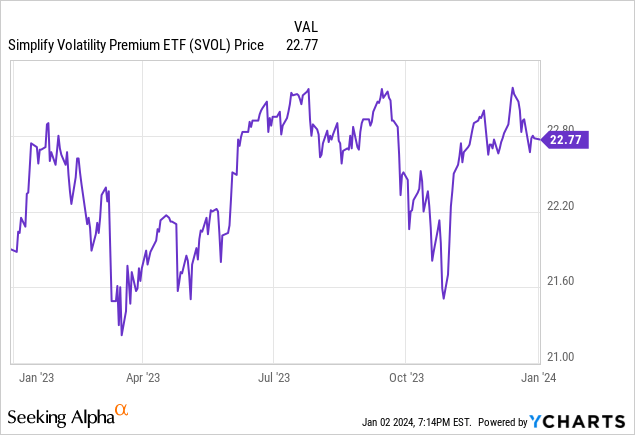

The fund primarily goals to commerce in a good vary and challenge month-to-month dividends. Be cautious of this once you see return charts for SVOL.

Pattern Reversal

Right here have been the first points I raised in November:

- Adjustments to dividend distributions to primarily embody the return on capital distributions

- Inclusion of the Simplify Tail Danger Technique ETF (CYA) as a substitute of the extra capital-efficient answer, VIX name choices

- With a low VIX, the necessity to push additional out on the curve might present for decreased future yields

These points have begun to be addressed by the portfolio managers, with the adjustments to distributions being totally reverted to bizarre earnings. There’s progress being made on the tail hedging and time period construction placement as nicely.

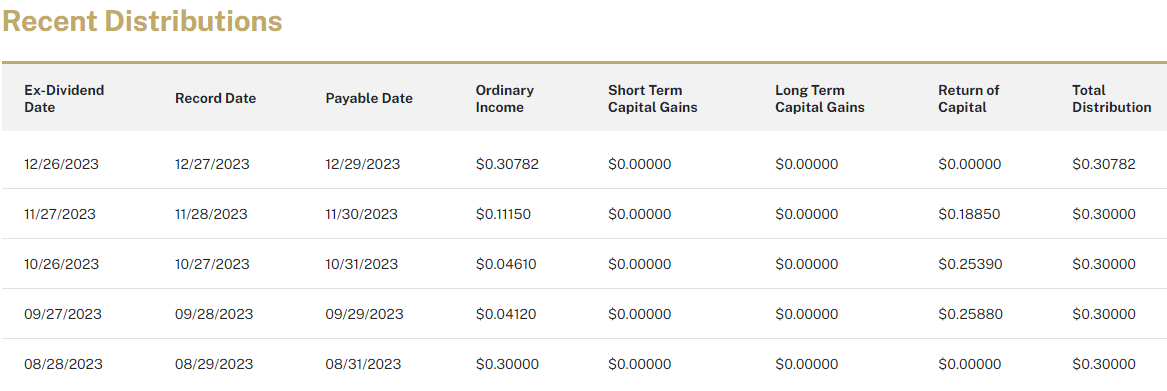

Adjustments in Dividends/Distributions

December’s dividend was declared to be totally bizarre earnings, indicating an finish to the return of capital (“RoC”) development that has been ongoing since September.

Determine 3 (Simplify ETFs)

I’m assured from seeing this that the return of capital distributions was a results of inside actions like rebalancing and was not a everlasting shift in technique carried out by the portfolio managers.

As a cherry on high, the distribution was nearly $0.31 as a substitute of the standard $0.30 that traders have gotten used to this yr, down from $0.32 again in 2022 when the VIX was increased. I will settle for this token of goodwill from Simplify and hope it’s signaling a return again to the $0.32 month-to-month distributions.

Decreasing CYA, Including VIX Calls

In November, I wrote:

The final time I coated SVOL, its solely hedges towards an antagonistic transfer within the VIX have been far OTM VIX calls. The present technique has integrated certainly one of Simplify’s different funds, the Simplify Tail Danger Technique ETF (CYA).

The extra capital-efficient strategy could be to extend the place in OTM VIX calls or create a ladder of calls to cut back some prices. SVOL might additionally make use of the form of name spreads utilized by CYA itself without having to spend money on CYA.

VIX name spreads are much more capital environment friendly to hedge antagonistic strikes towards the VIX than the hedges CYA employs as a result of CYA contains fairness hedges. These are usually not helpful to SVOL’s technique, or not less than not as helpful as that very same capital getting used for extra publicity to OTM VIX calls.

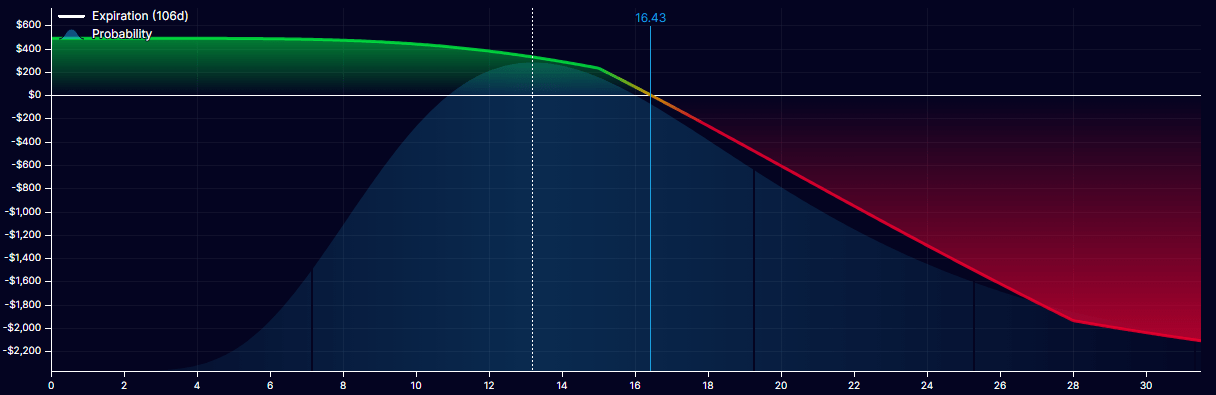

In comparison with a standard short-call payoff grid, including in these hedges adjustments the slope and steepness of the draw back, permitting for some hedging in a sudden crash. These OTM VIX calls do not need to finish spreads consistent with the quick futures however do have to have sufficient weighting to have a measurable influence throughout a crash.

Determine 4 (OptionStrat)

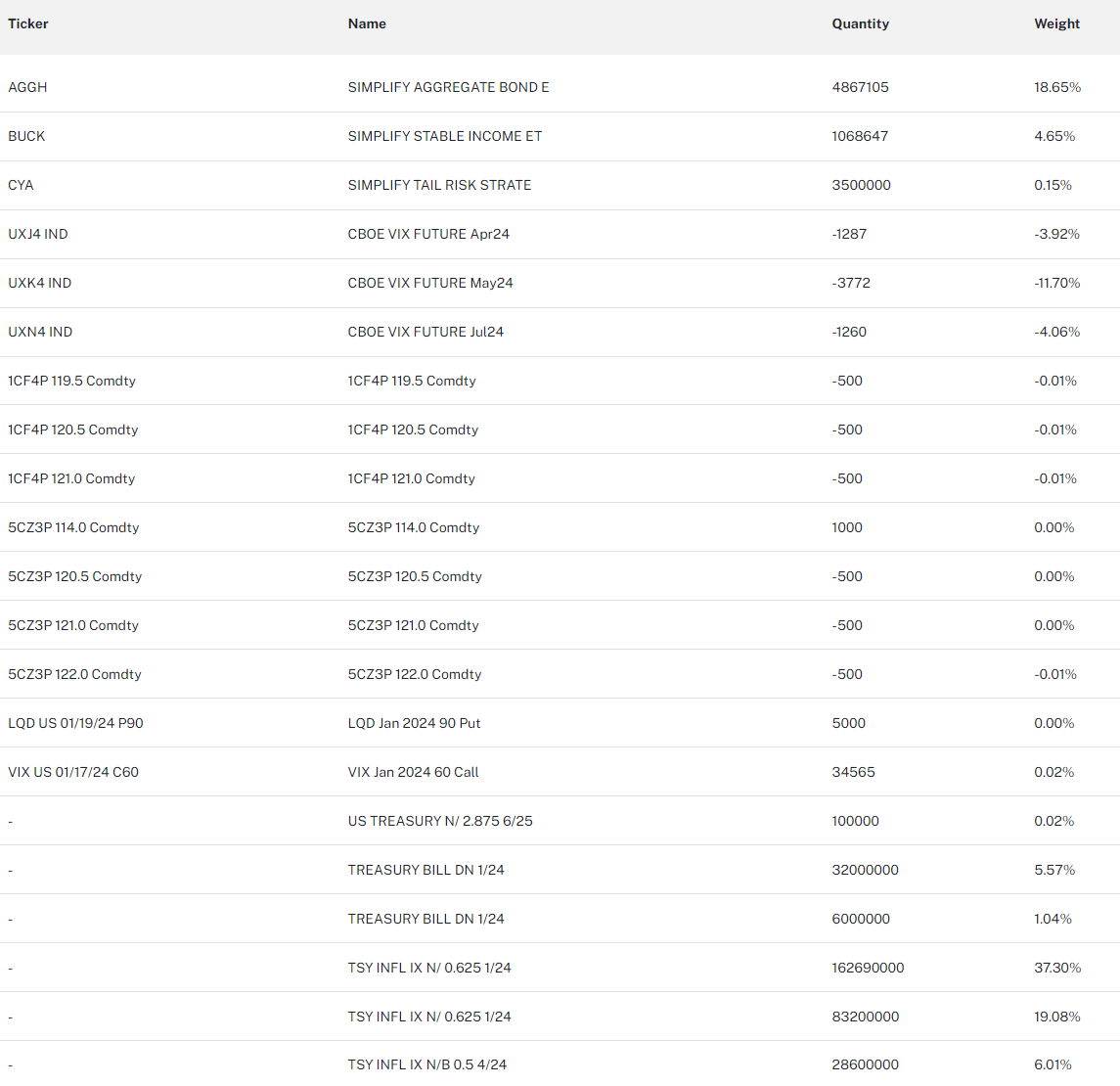

The folks (or particular person, not less than; I do not know if anybody aside from me has been fist-shaking at Simplify for this) requested, and the folks acquired: CYA’s allocation has greater than halved since that was posted.

I made a remark in certainly one of my articles that I hope Simplify’s portfolio managers learn my column as a result of I’d completely like to take credit score for this one. (They comply with me right here on In search of Alpha, however the jury remains to be out.)

AGGH can be certainly one of SVOL’s incestuous holdings and SVOL’s stake in AGGH is sort of 80% of AGGH’s complete AUM. There’s a number of regarding inter-mingling happening underneath the hood, not simply restricted to CYA.

On the time my maintain score was printed, SVOL’s holdings of CYA represented about 0.36% of NAV. As we speak, that has dropped to 0.15%. A few of that has been moved into VIX name choices, which you’ll be able to see from in the present day’s holdings.

Determine 5 (Simplify ETFs)

Whereas I am nonetheless not totally completely happy as a result of I am not a fan of the incestuous nature of Simplify’s funds. SVOL nonetheless has a substantial place in AGGH, representing greater than $106M of AGGH’s $141M NAV.

That comes out to 75% of the NAV in AGGH coming from SVOL’s holdings. Nevertheless, that determine was even increased as of the final article, the place it sat at 80%.

I don’t like this sort of liquidity challenge in my holdings, and this grievance stays considerably unaddressed for now.

Rolling out to July

The keen-eyed could have noticed in Determine 5 above that we have now a brand new place on the curve out in July.

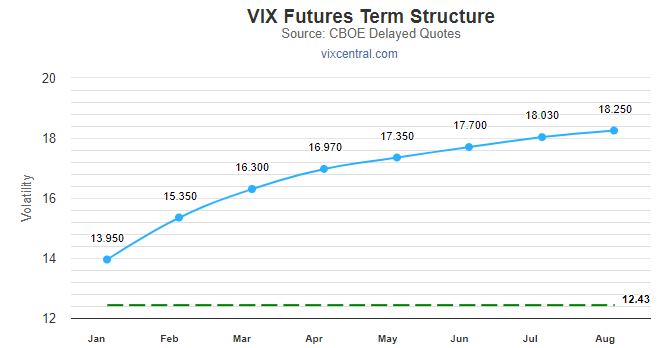

Determine 6 (VIXCentral)

I agree with the portfolio managers that being additional out on the curve is healthier for our present volatility surroundings than the entrance months. The place of all the curve is simply too low to tackle early expirations proper now.

The VIX being so low does pose a danger to quick volatility merchants, however the portfolio managers are avoiding holding positions shorter than April to mitigate a few of that danger.

SVOL would profit immensely from a gradual, grinding rise within the VIX, and would earn a powerful purchase score from me in a greater volatility surroundings.

Dangers Nonetheless Linger

SVOL has but to outlive an occasion like a Volmageddon or March 2020 crash, because it did not exist throughout these occasions. Due to this, it is unclear how the tail hedges SVOL employs will work in a real-world situation.

The Simplify Volatility Premium ETF is a leveraged ETF offering -0.2 to -0.3x publicity to the VIX, reset each day. This implies that there’s a danger of great antagonistic strikes within the VIX that might have an effect on the fund. SEC paperwork define VIX Futures Risks:

VIX futures contracts may be extremely risky and the Fund could expertise sudden and huge losses when shopping for, promoting or holding such devices; you may lose all or a portion of your funding inside a single day. Investments linked to fairness market volatility, together with VIX futures contracts, may be extremely risky and should expertise sudden, massive and sudden losses. VIX futures contracts are in contrast to conventional futures contracts and are usually not primarily based on a tradable reference asset. The Index isn’t instantly investable, and the settlement value of a VIX futures contract is predicated on the calculation that determines the extent of the VIX. Because of this, the habits of a VIX futures contract could also be totally different from a standard futures contract whose settlement value is predicated on a particular tradable asset and should differ from an investor’s expectations. The marketplace for VIX futures contracts could fluctuate extensively primarily based on a wide range of elements together with adjustments in general market actions, political and financial occasions and insurance policies, wars, acts of terrorism, pure disasters (together with illness, epidemics and pandemics), adjustments in rates of interest or inflation charges. Excessive volatility could have an antagonistic influence on the efficiency of the Fund. An investor in any of the Funds might probably lose the complete principal of his or her funding inside a single day.

Whereas this isn’t a totally leveraged fund that offers with worth decay like (SVIX) or (VIXY), and SVOL has a constructive anticipated return attributable to constructive choice convexity and a hedge towards excessive VIX strikes (as mentioned earlier), there are nonetheless inherent dangers.

Simplify explains higher than I can, from the prospectus:

The choice overlay is a strategic, persistent publicity meant to hedge towards market strikes and so as to add convexity to the Fund. If the market goes up, the Fund’s returns could outperform the market as a result of the adviser will promote or train the decision choices. If the market goes down, the Fund’s returns could fall lower than the market as a result of the adviser will promote or train the put choices. The adviser selects choices primarily based upon its analysis of relative worth primarily based on price, strike value (value that the choice may be purchased or offered by the choice holder) and maturity (the final date the choice contract is legitimate) and can train or shut the choices primarily based on maturity or portfolio rebalancing necessities.

The Fund’s returns are meant to own convexity as a result of the connection between the Fund’s returns and market returns isn’t designed to be linear. That’s, if market returns go up and down in a linear vogue, the Fund’s returns are anticipated to rise sooner than the market in constructive markets; whereas declining lower than the market in unfavourable markets. The worth of the Fund’s name choices is anticipated to rise in proportion to the rise in worth of the underlying belongings, however the quantity by which the Fund’s choices enhance or lower in worth relies on how far the market has moved from the time the choices place was initiated.

Buyers must be cautious about investing in any product they do not perceive or are usually not ready to take the related dangers with. Whereas SVOL is on the safer facet of those sorts of funds, since it’s by no means greater than 0.3x quick, we can not deny these dangers nonetheless exist and should be understood. Please pay attention to them. Observe that the lowered publicity to the VIX in comparison with conventional leveraged futures merchandise units SVOL other than (SVIX), (SVXY), and many others.

There are two main issues that I will likely be watching shifting ahead, which might change my stance on SVOL:

- Additional inclusion of higher-risk, higher-yield belongings like AGGH and BUCK over the standard TIPS and T-Invoice holdings, which might point out that the quick VIX technique can not maintain the goal 15% yield

- A return of the RoC distributions, which might point out some “NAV cannibalism,” which earned SVOL the downgrade in November

I can even re-evaluate the fund after the following two dividends to see if it is ready to stabilize again on the $0.30 mark or, as talked about earlier, return to the $0.32 dividend traders noticed again in 2022. A return to this mark would earn SVOL an improve to a powerful purchase if the fund can present that the extent of earnings is sustainable with out returning capital to traders.

Expectations for Q1’24

If the VIX stays low, anticipate SVOL to proceed to commerce in a good sample, probably even again down into the decrease finish of 21 like we did again in April, Could, and October this yr.

I imagine the dividend will likely be sustainable, not less than for $0.30, as we have seen with the energy in December’s distribution. Anticipate consistency from SVOL until we see a sudden rise within the VIX.

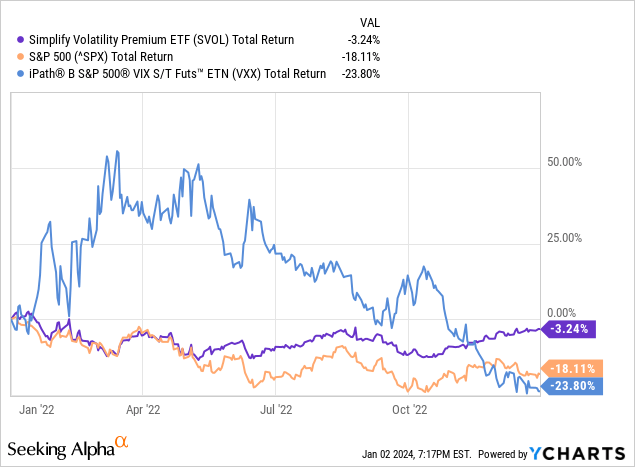

A gentle grind could be excellent for SVOL, as is evidenced by its 2022 efficiency.

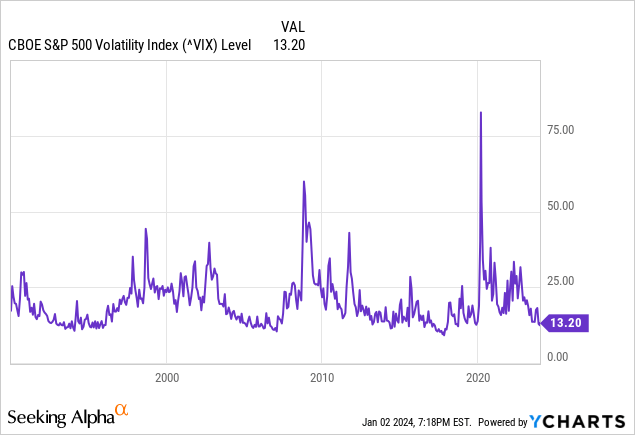

That yr left the VIX at an inflection level, one which it’s nonetheless at now. Solely time will inform, as it’s nearly at all times unclear what is going to spike the VIX till after it occurs.

Conclusion

I’m reinstating my purchase score for the Simplify Volatility Premium ETF (SVOL) as a result of it addressed a number of of the issues I raised in my earlier downgrade article.

These adjustments have been:

- Adjustments made to exclude return of capital from dividends, returning to bizarre earnings distributions.

- A reduce of the Simplify Tail Danger Technique ETF (CYA) as a substitute and inclusion of VIX name choices.

- With a low VIX, the managers pushed out to the July expiration to keep away from being caught quick a sub-13 VIX.

SVOL continues to carry a spot in my earnings portfolio, and with a present distribution yield of 15.88%, it is onerous to not obese it.

For now, I warning traders to not place greater than 15% of an earnings portfolio on this asset, as it might be too dangerous in a VIX spike.

Presently, SVOL has a ten% allocation in my earnings portfolio, which I wrote about in additional element here.

I will likely be keeping track of future distributions for adjustments, in addition to the place the managers resolve to roll out from right here. By positioning in July, we’re organising for a sustained low VIX for the following few months. If this performs out, earnings ought to stay regular.

Thanks for studying.