SeanShot/E+ by way of Getty Photos

Simplify Volatility Premium ETF (NYSEARCA:SVOL) is without doubt one of the most fascinating earnings funds on the market. Most income-oriented funds have a lot less complicated methods, like diversifying into dividend shares or writing coated calls. Equally, their yields are normally within the high-single digits or the low-double digits. Yielding over 16%, many may suppose SVOL is a yield entice at first look. But, I feel its technique is a sound one that may command such a yield over time, so I am going to give my very own rundown as to why SVOL is a superb Purchase for long-term, income-focused buyers.

Idea of the Fund

SVOL is an actively managed fund that seeks to supply distributable earnings to its shareholders. A signature a part of its technique is its relationship to the Volatility Index (VIX). It generates a part of its earnings by committing between 20% and 30% of its portfolio to brief positions on VIX’s future contracts (principally writing calls on VIX).

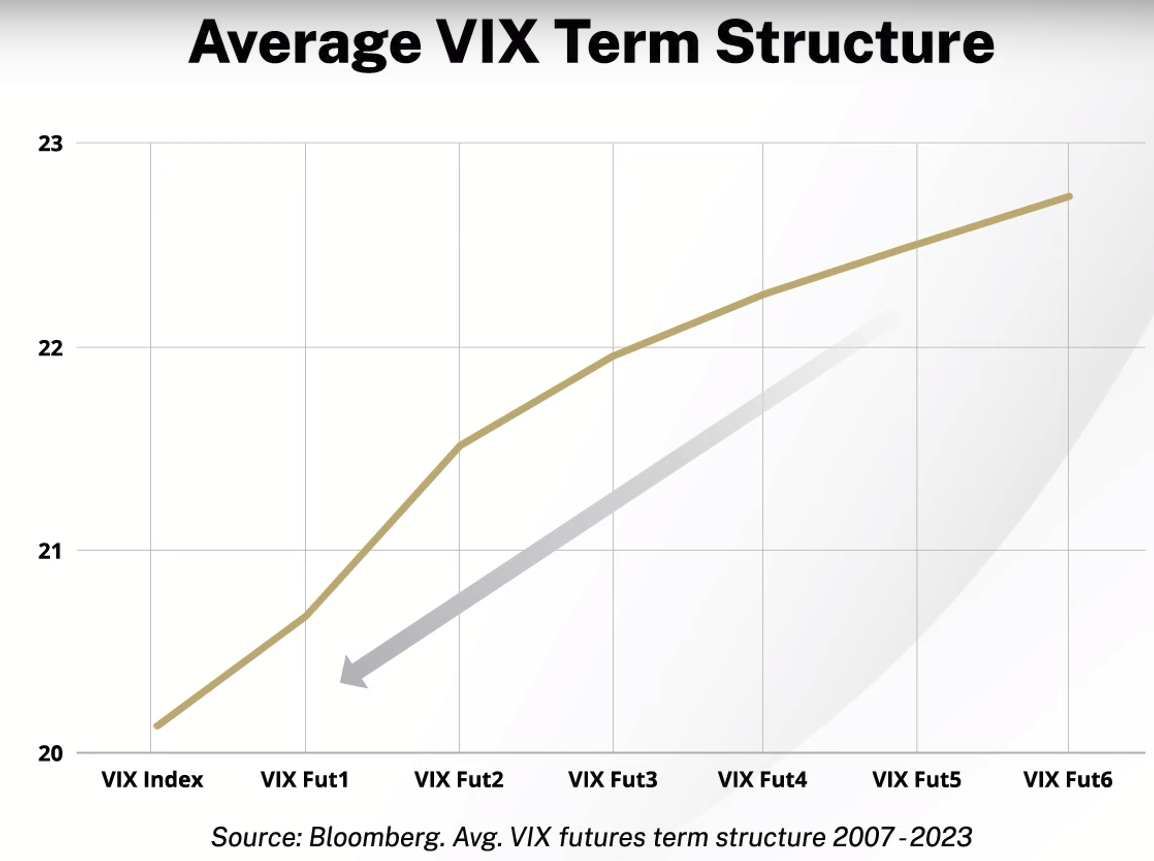

Fund Supervisor Offical YouTube

SVOL will brief these futures as they’re a number of months out from expiration. Because the graph above exhibits, contract costs decline as they strategy the current. This is identical as how requires inventory choices lose time value as they close to expiration. Utilizing this dynamic, SVOL can purchase again these contracts for a revenue, with positive factors that they will both roll into new positions or distribute, which they usually do throughout staggered expirations. Over time, I anticipate this will probably be a principally sturdy supply of earnings.

The remainder of the portfolio is diversely invested into varied fixed-income belongings that contribute to and assist to “smooth out” SVOL’s yield in periods the brief technique on VIX can disappoint (extra on that to return).

Holdings

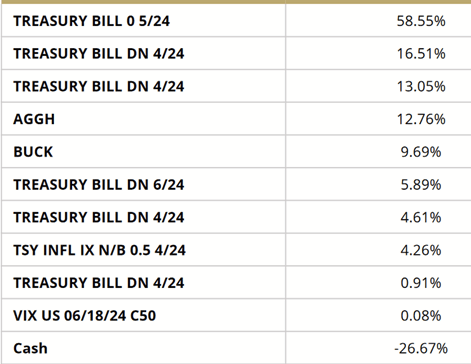

In the newest fund fact sheet the managers offered, the holdings are like so:

March 2024 Reality Sheet

Clearly Treasury Payments, with their yields close to 5%, are engaging for the managers proper now. But, about 24% of the portfolio is allotted towards Simplify Mixture Bond ETF (AGGH) and Simplify Secure Revenue ETF (BUCK). What about these? Effectively, BUCK is just like T-Payments, being primarily invested in those, whereas yielding barely greater (therefore “Stable”).

AGGH, in the meantime, can also be primarily invested in Treasury securities, however a lot of that portfolio is invested in iShares Core U.S. Mixture Bond ETF (AGG), which in turn is a fixed-income fund in Treasuries, Company points, and investment-grade company points.

All of this to say – I feel the mounted earnings facet of the portfolio is sound and of reliable credit score high quality.

Efficiency So Far

The Fund hasn’t been round a very very long time (spring of 2021), however to this point, it has executed properly. First, let’s take a look at the dividend historical past.

SVOL Dividend Historical past (Looking for Alpha)

Since its first distribution in late 2021, the fund has efficiently paid month-to-month dividends within the neighborhood of $0.30 per share, usually extra.

Yield On Price (Looking for Alpha)

Consequently, the fund has loved a pretty yield on price, regardless of the entry value one might need had throughout its lifetime. These yields are available in round 14% – 15%.

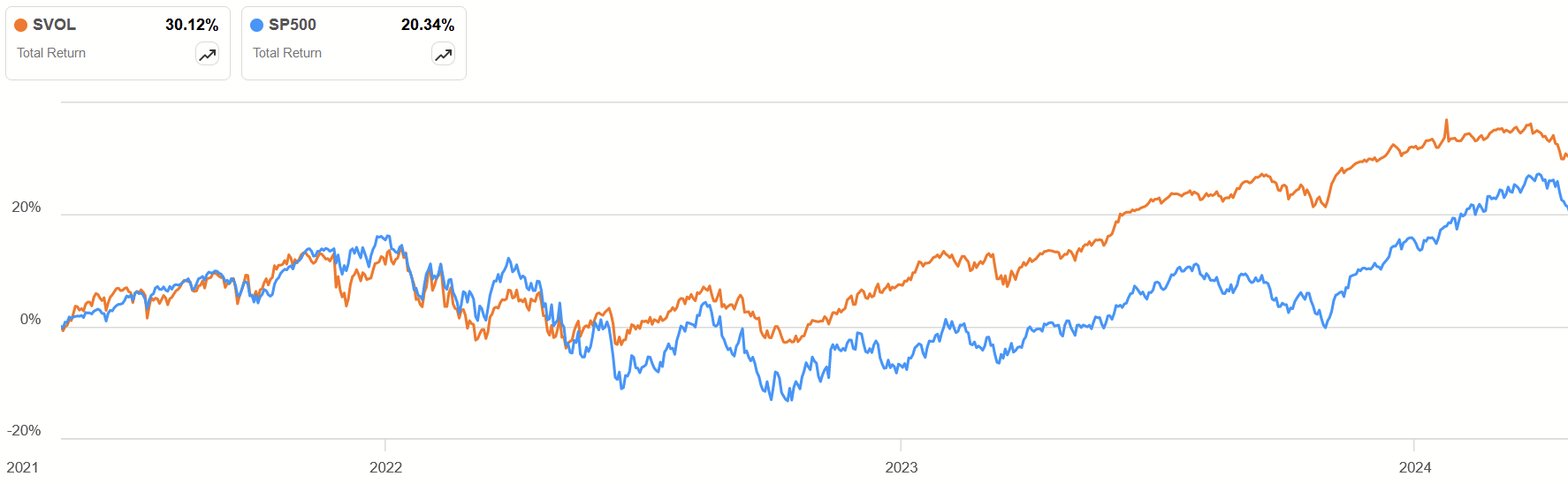

SVOL Complete Return vs. S&P 500 (Looking for Alpha)

Intriguingly, the fund has crushed the S&P 500 since its inception virtually three years in the past. We would debate if this can be a long-enough time period time frame to check the 2, whereas additionally remembering that it is capturing a interval of traditionally fast rate of interest hikes, but it surely’s nonetheless good to notice.

Future Dangers

So I’ve given loads of hints about what’s good about this fund, however a few issues might weaken returns going ahead and are vital to bear in mind.

Curiosity Charges

If rates of interest drop once more, this could scale back the potential yield from the fixed-income portion of their portfolio. As they’re extra invested in T-Payments than securities with longer durations, they’re additionally not poised to see a lot capital appreciation and thus an increase in NAV per share from this. Whereas administration can reallocate accordingly to profit from such at any time, we’ve got to belief that they’d transfer accordingly.

Peculiar VIX Occasions

Whereas I discussed earlier than that the depreciation of VIX futures is normally a given as time worth is misplaced, there could be eventualities wherein returns are damage by its inverse-VIX strategy. Lest we overlook, VIX and the S&P 500 are negatively correlated normally, and a sufficiently unstable market surroundings might exceed the positive factors from the shorts on VIX futures. A brief technique that’s on the fallacious facet of the market additionally has the potential for heavy lack of upside as properly.

Dan Caplinger discussed this in a 2018 piece in regards to the decline of pure inverse-VIX ETFs:

But in the long run, all it took was a single day to convey inverse volatility ETFs to their knees. With the VIX having been at extraordinarily low ranges, it did not require too massive of an increase to characterize a 100% each day enhance in volatility. That is what occurred on Feb. 5, when February VIX futures rose from their opening stage of 16 into the low 30s by the afternoon.

He is not exaggerating when he says they have been dropped at their knees. These funds have been worn out. Since a few of SVOL’s portfolio will probably be deployed like this (20% – 30%), there’s room for it to take successful.

Mitigating Components

But, it’s out of those classes that knowledge is gained, and it is not unintentional that this fund was launched after these occasions, so let’s discuss in regards to the methods the fund is ready as much as mitigate danger.

Nearer-Time period Futures

In intervals the place the VIX rises (volatility climbs), administration can roll the income from its closed-out positions into nearer-term futures. That is an strategy they talk about of their deep dive video on their official fund page. This has the good thing about permitting them to seize the next contract premium in a shorter span of time, which may even liberate the place sooner to readjust to the extra typical allocation (of farther-term contracts) when favorable. Once more, we rely on administration being proactive sufficient to grab on this.

Different Choices Methods

The fund additionally hedges a few of its danger by taking part in another spinoff positions. Administration discusses this in their Prospectus (pg. 154):

The choice overlay is a strategic, persistent publicity meant to hedge towards market strikes and so as to add convexity to the Fund. If the market goes up, the Fund’s returns might outperform the market as a result of the adviser will promote or train the decision choices. If the market goes down, the Fund’s returns might fall lower than the market as a result of the adviser will promote or train the put choices.

It will usually contain buying market places since market declines are correlated with VIX positive factors that consequently hurt inverse-VIX positions. Equally, administration opportunistically trades choices on a few of its fixed-income positions. These items may also assist to easy out distributable money flows and are good examples of this fund’s versatile strategy.

Constructive Relationship with Shares

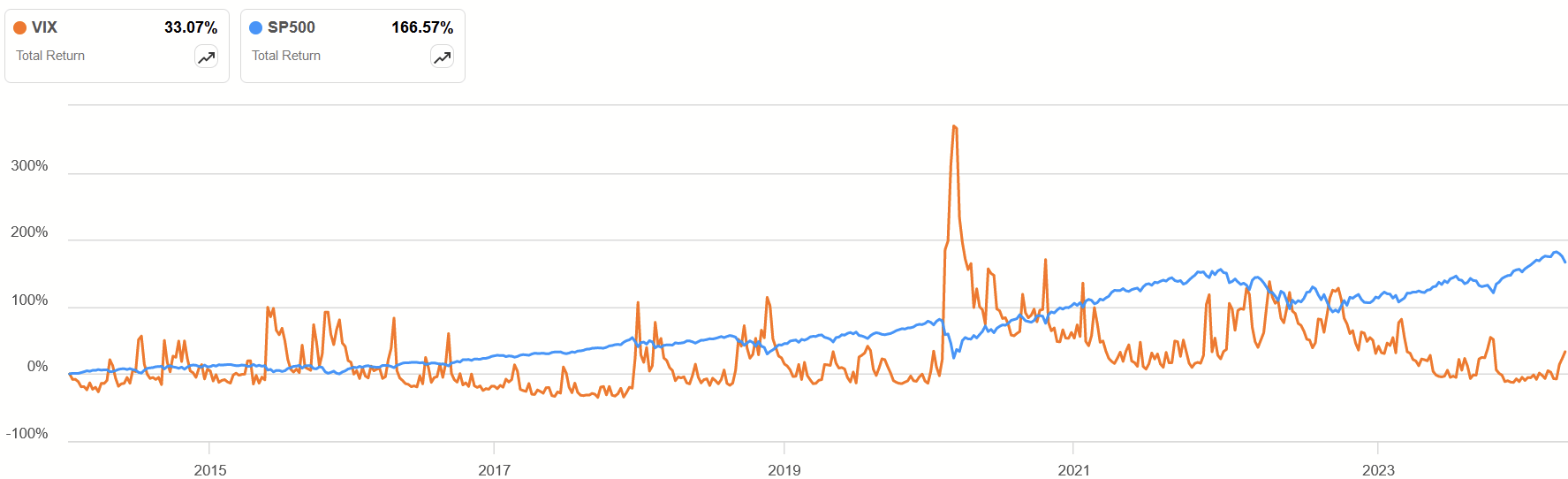

Now, that is the half that I feel deserves probably the most consideration for the long-term investor: SVOL’s constructive correlation with shares. I’ve talked about it right here and there, and the entire returns chart I confirmed earlier shows it, however I additionally need to present VIX versus the S&P 500:

Complete Returns Final 10Y (Looking for Alpha)

Now, the connection between the market and VIX is not completely destructive; each have had constructive whole returns during the last decade. Sharp peaks of VIX’s rallies normally accompany declines within the S&P 500. On the similar time, these peaks decline because the market begins to get well. VIX’s whole returns solely beat the S&P 500 throughout very temporary moments, however throughout most environments shares pull forward, and I consider the SVOL is positioned to profit in an identical means.

I consider this distinguishes it from different earnings/yield funds. Fastened earnings can profit from declining rates of interest like shares can however with a lot much less upside. The reason being apparent: mounted earnings is debt, and debt’s full upside is reimbursement. Equally, with coated name ETFs, the decision contracts usually cap the upside. In SVOL’s case, they don’t seem to be immediately uncovered to capped upside like this.

Lengthy-term, I feel it is rather potential that SVOL could be each a high-yield ETF with extra room for long-term compounding than you get from related funds. It is a new fund, and time would be the final take a look at of lively administration, however these are assuring indicators.

Conclusion

Revenue funds with excessive yields are sometimes attractive however harmful. Those that have dipped their toes in and been bitten earlier than be taught to have a look at a 16% yield and ask, “Okay, what’s wrong with it?”

But, I feel little or no could possibly be stated that’s fallacious with this one. With a fixed-income portfolio of dependable credit score, usually constant traits of VIX futures pricing, and lively administration that may modify at moments the place the norm is not sensible, I’ve a tough time seeing the place the yield entice is. Even disappointment would produce a excessive yield with the sort of fund.

The extra doubtless unhealthy state of affairs, in my eyes, is that VIX has a kind of spikes that causes a short dip within the month-to-month distributions. Wherein case, that is a cause to diversify throughout a number of earnings sources. For the long-term investor who can deal with the intermittent aberration, nevertheless, SVOL comes throughout as among the best yield funds one can purchase.